AGGH - Meet The 8% Yield Portfolio With Negligible Equity Risk

2023-12-04 20:07:50 ET

Summary

- Most income-oriented portfolio models exposure investors to too much market risk and haven't adjusted to the current rate environment where fixed income is shining.

- I have created a mix of income producing assets that offer investors a compelling model free from market risk that can still yield 8%.

- In addition to credit and fixed income, adding in alternatives offers us hedges against rates, inflation, and beta.

Introduction

As an analyst that mostly covers income-oriented investments, I've been seeing a lot of articles about model portfolios advertising yields of 8-10% p.a., but they are full of REITs, BDCs, common stock, and have few actual credit or fixed income holdings.

As an income investor, these model portfolios are not always very valuable to me, as they are laden with risks I'm not interested in taking on. Many of them have high beta holdings, very high volatility, strong correlations to traditional equity indices, and worst of all, often do not offer stable returns as the underlying holdings' income streams can be very unreliable.

Goals

In this article, I'm going to propose a model portfolio that achieves the following objectives:

- Achieves current income in the 8% p.a. range

- Doesn't directly hold equities or equity indices or CEFs, BDCs, or REITs

- Achieves an annualized standard deviation of ?8%, and a beta of ?0.25

- Presents favorable risk-adjusted return metrics (Sharpe & Sortino) compared to the aggregate bond index ( AGG )

- Is constituted entirely by ETFs or other publically available, liquid assets

- Allocates to multiple asset types and strategies

- Provides a hedge against inflation and future rate changes, both up or down

- Achieves a mid-low duration, ?5yr

The Portfolio

Without further ado, let me I introduce you to my creation ("It's alive!").

| Ticker |

| Name |

| Allocation |

| Yield |

| AGGH |

| Simplify Aggregate Bond ETF |

| 15% |

| 9.36% |

| SPIP |

| SPDR Portfolio TIPS ETF |

| 9% |

| 3.97% |

| WIP |

| SPDR FTSE Intl Govt Inflation-Protected Bond ETF |

| 6% |

| 7.34% |

| BKLN |

| Invesco Senior Loan ETF |

| 10% |

| 9.52% |

| Janus Henderson AAA CLO ETF |

| 7% |

| 5.85% |

| JBBB |

| Janus Henderson B-BBB CLO ETF |

| 4.5% |

| 7.98% |

| CRDT |

| Simplify Opportunistic Income ETF |

| 7.5% |

| 8.04% |

| VPC |

| Virtus Private Credit Strategy ETF |

| 5% |

| 11.41% |

| HIGH |

| Simplify Enhanced Income ETF |

| 10% |

| 4.79% |

| DBMF |

| iMGP DBi Managed Futures Strategy ETF |

| 5% |

| 8.22% |

| KMLM |

| KFA Mount Lucas Managed Futures Index Strategy ETF |

| 5% |

| 13.30% |

| RISR |

| FolioBeyond Alternative Income and Int Rt Hdg ETF |

| 6% |

| 6.65% |

| QIS |

| Simplify Multi-QIS Alternative ETF |

| 10% |

| 4.37% |

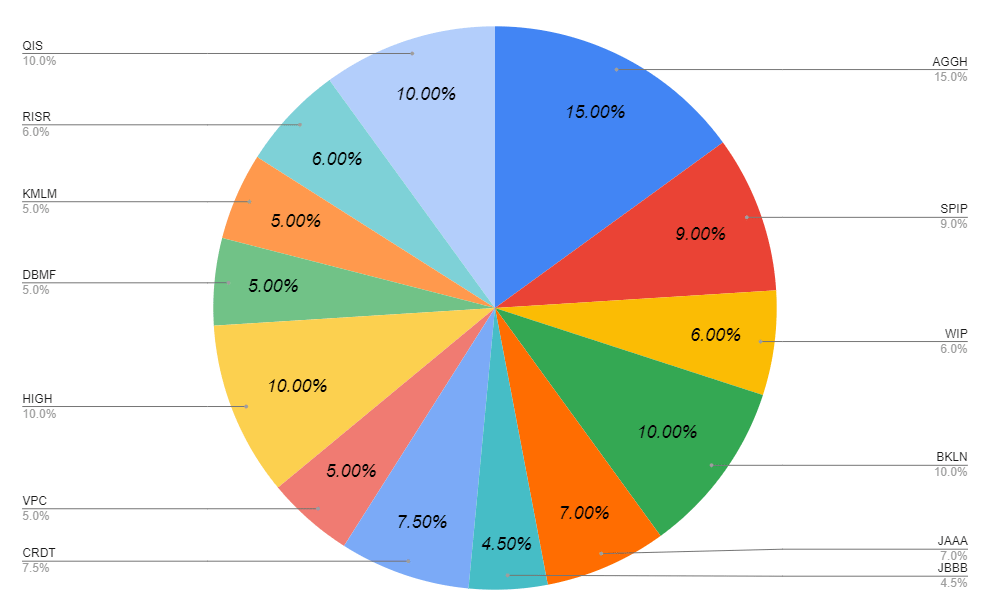

Instead of ordering them by allocation size, I've ordered them thematically and will cover them in order from top to bottom of the table or clockwise around Figure 1 starting in the darkest blue slice at the top right. That will be in for the "holdings" section below.

{kind=link}

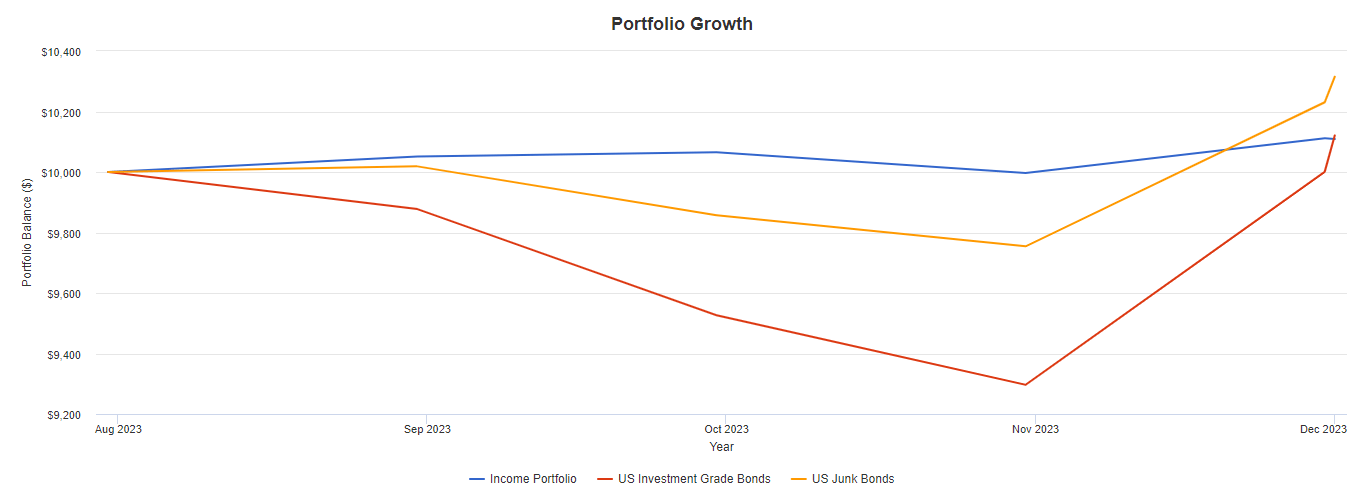

This portfolio's largest fault is its inability to be backtested well. Because many of the funds it uses are new, as are some of the best alternatives and options-overlay funds. We can only successfully backtest from 8/1/23–12/1/23.

If you'd like to see the backtest and play around with allocations, substitute assets, etc., here you are .

Figure 2 (PortfolioVisualizer)

{kind=link}

In that time, we can see immediately see how the low beta and volatility mandates shape the portfolio's return profile against the bond market.

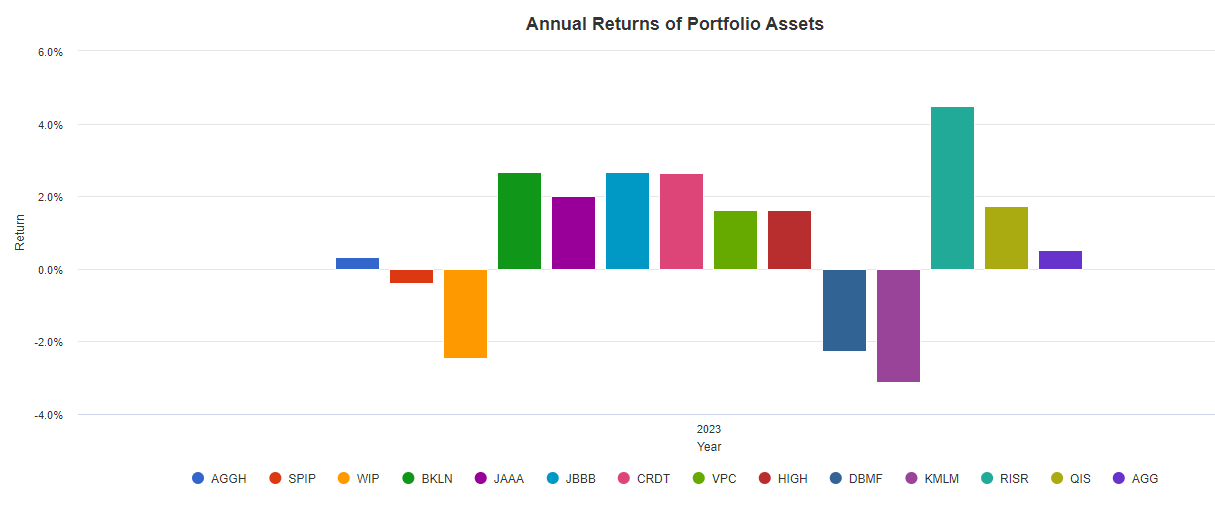

Here is how the assets performed on an individual basis from August to now.

Figure 3 (PortfolioVisualizer)

{kind=link}

In this short timeframe, investment grade ("IG") bonds exhibited a 15% annualized standard deviation ("stdev"), high-yield ("HY") bonds' stdev was 8.86%, and our portfolio's was 2.34%.

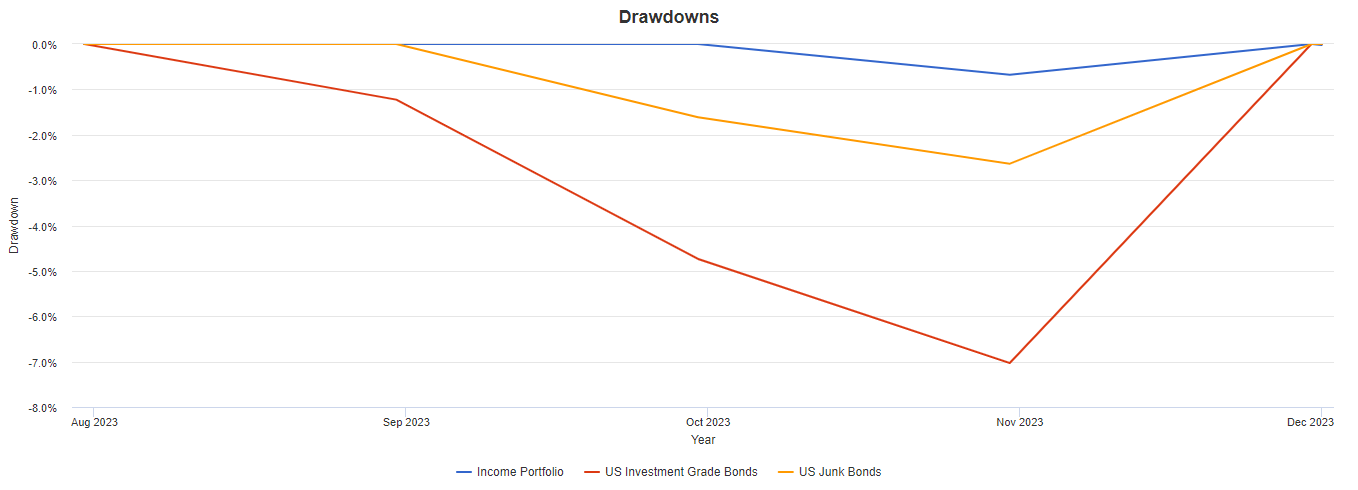

This is more noticeable in the drawdown chart, as our portfolio had a maximum drawdown of 0.68% compared to IG's 7.03% and HY's 2.64%.

Figure 4 (PortfolioVisualizer)

{kind=link}

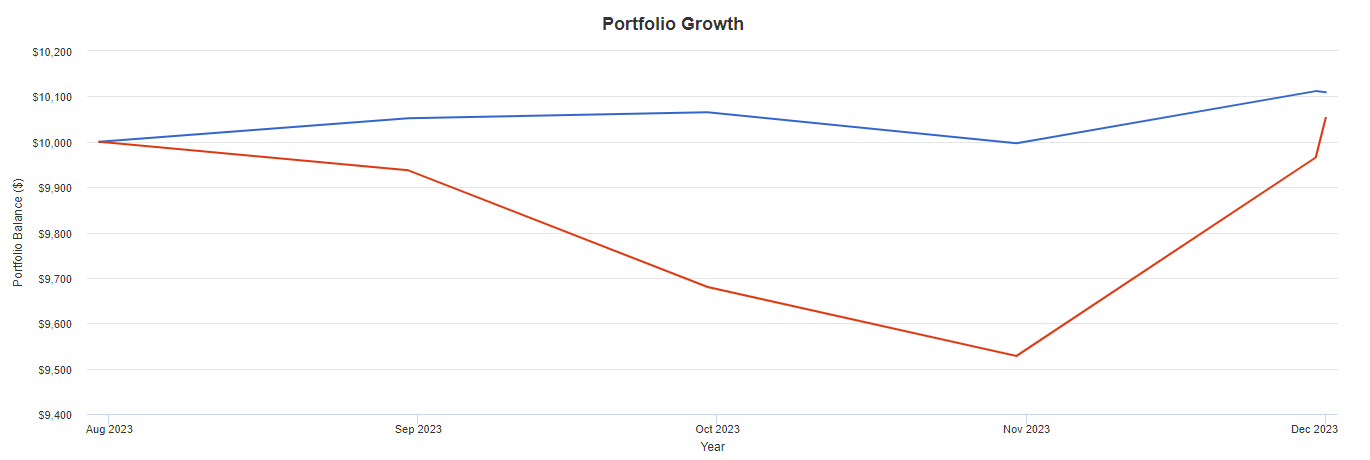

Here is the portfolio's performance against its benchmark, the aggregate bond market ( AGG ).

Figure 5 (PortfolioVisualizer)

{kind=link}

This is not nearly a long enough timeframe to judge this portfolio. Future updates will be needed to show the strategy's performance.

Here is the credit breakdown, for those interested. Note our large exposure to non-IG bonds, which provide a significant portion of our yield.

Figure 6 (PortfolioVisualizer)

Here is the rough asset allocation. Options and derivatives complicate this, so expect a bit of deviation if you try to replicate this.

Figure 7 (PortfolioVisualizer)

Holdings

Simplify Aggregate Bond ETF ( AGGH ) — 15%

AGGH is Simplify's modern and complex take on a core bond fund. I covered it back in October , and encourage folks to check that out to get a longer, more detailed take on this fund.

Using futures and options, AGGH has been able to outperform its benchmark (and the portfolio's benchmark) and do so without adding in too much unnecessary risk.

While I am not bullish on AGG itself, I do recognize the need for a solid core holding in this portfolio, and I believe AGGH is the most appropriate tool we have for that job.

Inflation Protection ( SPIP ) & ( WIP ) — 15%

These two funds complete our core holdings and provides us with exposure to inflation-linked bonds. I've broken them down to roughly market weight, a ratio of 6:4 US to international, and have excluded emerging markets. This gives the portfolio its first access across geographic markets, as WIP is only international inflation-protected bonds and is primarily focused on bonds denominated in Euros and British Pounds.

I decided on these two because they offer the most broad access while not increasing our duration too much. These are the highest duration holdings in the portfolio and may be the first to go if the Fed signals that they intend to begin cutting rates. You can see how the yields have come down since their spike this past summer, but have started to level off.

For now, I'm happy with the large allocation to these two.

Senior Notes & CLOs ( BKLN ), ( JAAA ), & ( JBBB ) — 21.5%

Right now, I prefer senior bank loans and CLOs to corporate bonds for their lower duration and easier access to broad diversification. In the past, I've written about a CEF that holds bank loans , for which BKLN is the passive index. I've also covered JAAA and JBBB . For those interested in these funds, I go into much greater depth in those articles.

There is some credit risk adding by the positions, especially with JBBB, as its holdings are lower in the payout order and investors may receive very little in the event of defaults in the underlying tranches.

These holdings all have virtually no duration, since their underlying holdings are all floating-rate and are based off SOFR plus a premium, usually 200–700 basis points, depending on the borrower's credit risk.

Opportunistic Credit ( CRDT ) & ( VPC ) — 12.5%

These two funds allocation across private credit markets and provides us exposure to distressed debt. VPC is riskier than CRDT as it has a more aggressive allocation strategy, so I have weighted it lower. The volatility of these funds can be impressive, but so can their returns and potential to provide very large dividends. This section is our "risk-on" component and may carry the portfolio through high rate environments where private credit becomes very expensive for borrowers.

CRDT is very new, and I expect the fund to take a bit of time to "spin up" and fill out its strategy completely. As of right now, I am very pleased with its inclusion of bond funds to balance out its private credit holdings.

With volatility comes returns. As of right now, I think that CRDT has less volatility than it will once its strategy is fully deployed and more time has passed. The current low rolling volatility is due to the amount of cash CRDT had when it launched. It took time to deploy that cash.

Options-Enhanced Cash ( HIGH ) — 10%

I intend to do a full write-up on HIGH as a standalone article in the future because it is fascinating to me. Essentially, the strategy is to hold treasury notes and use them to secure margin to sell options spreads on bond and equity indices.

Simplify uses a sub-adviser who employs an algorithm to decide on the options trades. These introduce a very small amount of equity risk. Ultimately, that risk is negligible from a portfolio perspective, but those taking much larger positions in this fund should be aware of that. HIGH has done well at providing consistent income, as well as stability, for investors since its launch last year.

Managed Futures ( DBMF ) & ( KMLM ) — 10%

This might throw some readers off, but please hear me out.

Managed futures offer investors access to a long/short strategy primarily deployed on commodities, currencies, and other derivatives like rate swaptions. These two funds do this beautifully and allow us to have exposure to these markets without needing to make directional bets on our own.

What's most useful about these two funds is that they are uncorrelated with bonds and equities. This allows for some "smoothing" of the portfolio as its sources of returns are not all coming from the same place.

This uncorrelated nature of managed futures funds also allows us to reduce portfolio beta. In our earlier backtest, in Figure 2, DBMF exhibited a beta of -0.91 and KMLM had a beta of -0.90. This did wonders to address the small amount of equity exposure in our other funds like AGGH and HIGH.

Last note about these funds is that they don't distribute monthly and instead distribute annually. That is very important for many income investors to be aware.

We can see the sheer difference in performance during times that have been poor for bonds like 2022. These funds can be a very useful hedge and warrant consideration from income investors.

Interest-Only Mortgages ( RISR ) - 6%

IO mortgages are my "dark horse" candidate for 2024. I believe we are going to see sustained <4% rates through the end of the year, and the Fed agrees with me.

The best way to prepare for this is to add negative duration to the portfolio. I only want a small bit of exposure to these, but they might be able to provide good returns in the event of a rate hike. This will provide a small bump to the portfolio, which may otherwise take some heat from rising rates.

This is not necessarily a "hedge" for anything other than rate changes, but also allows us to load up on newly issued interest-only mortgages as the fund rolls their holdings forward. With mortgage rates up above 7%, investors should expect the yield on this fund to climb a bit more and then level off until rates change.

I don't like the MBS index because it holds far too many low-rate mortgages purchased during the 0% effective rate environment. It was a great thing for folks like my parents who were able to refinance their home at 2.75%, but terrible for mortgage buyers having to buy their 2.75% mortgage.

In the future, I may swap this position with ( MTBA ), but it is too early for me to enter that fund or propose it. Its strategy is very new and definitely worth reading about over on the portfolio manager's blog .

Quant Strategies ( QIS ) - 10%

Lastly, we add in an alternative asset class. I've written an overview of QIS and encourage folks to check it out (as I'm the only analyst on this site that's written anything about QIS at all).

{kind=link}

Essentially, QIS aims to hold a portfolio of treasury notes and use those to secure total return swaps on opaque, quantitative trading strategies employed by hedge funds. This is not the same as trying to replicate hedge fund performance, which other ETFs have tried to do. Instead, this employs the same exact trading strategies by buying their returns.

The ETF holds strategies trading across several asset classes and provides an uncorrelated return source that can further help us shape the portfolio's returns. QIS is also a negative beta fund, like managed futures, and in the earlier backtest exhibited a -0.68 beta. In fact, QIS is so uncorrelated with other assets that its correlation to the overall portfolio is a flat 0.

Objectives

How did we do on our objectives? I will review these same objectives in my follow-up next quarter.

-

Achieves current income in the 8% p.a. range

The fund's current yield (based on 30-day SEC yields) is 7.89%.I actually expect this to climb as QIS begins to pay out dividends moving forward, and it may reach up toward 8.5 — 9%. -

Doesn't directly hold equities or equity indices or CEFs, BDCs, or REITs

Check! The equity exposure that does exist through short options spreads are hedged by the inclusion of managed futures and QIS.Notably missing from this portfolio is SVOL , which could be a massive boon for this portfolio. Unfortunately, SVOL's strategy targets equity premium via shorting volatility. While this has paid off well for investors, it introduces equity risk into the portfolio, so I had to exclude. I do recommend SVOL to income investors generally, and have written about its underlying holdings and its recent change in distributions . -

Achieves an annualized standard deviation of ?8%, and a beta of ?0.25

Our stdev was far lower than 8%, at 2.34%. This is a huge win, but may be short-lived. Time will tell.The portfolio's beta, during the short backtest, was 0.09. Compared to IG's 0.80 and HY's 0.46, this is also a huge win for the portfolio.Looking at the individual funds' lifetime stdevs and averaging them by weight gets us a portfolio beta of 0.197, still within our limits. -

Presents favorable risk-adjusted return metrics (Sharpe & Sortino) compared to the aggregate bond index ( AGG )

Here is the first failure from the portfolio. As of the backtest I was able to do, the portfolio's Sharpe and Sortino ratios fall below the index's.The portfolio scored -0.73 and -0.93 respectively.The index ( AGG ) scored -0.27 and -0.46 respectively. -

Is constituted entirely by ETFs or other publically available, liquid assets

Check! Not much to say here, but every component is an ETF and trades on US markets. If I was more willing to include mutual funds, there might be some changes. -

Allocates to multiple asset types and strategies

Check! The inclusion of non-fixed income holdings like DBMF, KMLM, and QIS give us a total of 20% exposure to alternative strategies across global markets and various asset classes. -

Provides a hedge against inflation and future rate changes, both up or down

As for inflation, our TIPS allocation has us covered. While this is just one piece of the portfolio, it should allow us to enhance our real returns over time.We hedge against rate changes with our low overall duration and alternatives allocation, since DBMF, KMLM, and QIS employ strategies to trade rate changes.Notably, I did not include Simplify's ( PFIX ) in the portfolio. This is a more direct rate change hedge, but I didn't think the duration was long enough to warrant it. Instead, I chose to allocate that to RISR, which also hedges against rate changes. -

Achieves a mid-low duration, ?5yr

Success! Duration is around 3.13yrs, which is an estimate since I have shoddy duration data from some of the more complex funds that include derivatives.

Suitability

As with any investment or model portfolio, investor suitability is a very important factor. I would consider this allocation "moderate." It's not aggressive, something I tried to dial back from by avoiding market risk. It's also not conservative and could suffer from sustained drawdowns if the bond market tanks.

There is inherent risk in the portfolio, namely credit risk from the underlying bond allocations. There are a lot of corporate bonds in the portfolio, mostly from the US. The hedges employed may not work during a real bond rut and we won't know until that happens.

This model is for investors who are interested in pursuing high income but already have too much equity exposure.

Conclusion

As of right now, this is the portfolio I would put together to achieve the stated objectives. An 8% yield is nothing to sneeze at, and so long as rates stay level, that should also stay level.

It is important to note that if rates fall dramatically, this portfolio's yield may fall with them.

I have mocked this portfolio up in a paper trading account and will follow up on its performance in the future and re-evaluate whether it has met its objectives or not as times moves on. I will also make sure to note any changes to the portfolio's strategy or holdings.

For further details see:

Meet The 8% Yield Portfolio With Negligible Equity Risk