MEGI - MEGI: Megatrends Infrastructure Looking Attractive With A Deep Discount

2023-12-26 06:57:34 ET

Summary

- MainStay CBRE Global Infrastructure Megatrends Term Fund continues to trade at a deep discount despite an increased distribution earlier this year, making it an interesting consideration.

- The fund is unique in its approach to investing in a broad range of infrastructure with a "megatrends" thematic-based portfolio.

- Saba Capital Management's increased ownership recently crossed over the 10% mark, and that could be an additional catalyst in the future.

Written by Nick Ackerman, co-produced by Stanford Chemist.

MainStay CBRE Global Infrastructure Megatrends Term Fund (MEGI) crossed its second anniversary recently after being launched in late October 2021. The fund continues to trade at a deep discount even after they ramped up the distribution to investors, pushing it to a double-digit distribution yield. The fund's coverage is fairly attractive in terms of generating some solid net investment income relative to peers.

Our last coverage of the fund was in August 2023 , and the fund's performance since then has been essentially flat. However, as we can see, it certainly wasn't straightforward to get to this point. During that period, the fund took a significant dip along with the rest of the market as Treasury Rates surged. That was before more recently receding, and that's helped drive the recovery.

I still believe that utilities and infrastructure investments look attractive at this time as they've struggled. Additionally, renewables were hit especially hard over the last year, where MEGI, more specifically, has some exposure through its thematic tilt. Combining that with the fund's discount makes MEGI an even more interesting prospect.

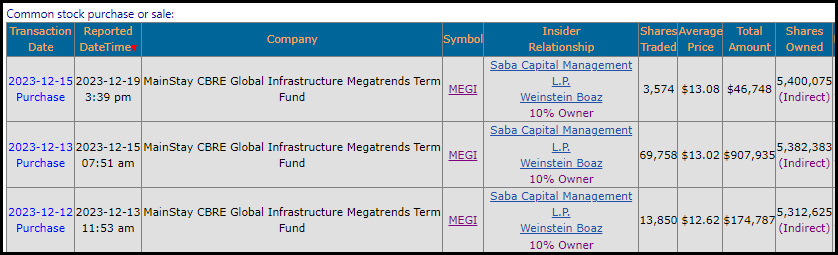

Another factor to consider going forward is what Saba Capital Management's involvement might be if anything. They took a position in this fund early this year and then just over doubled it at the start of December . That has pushed them to the threshold of over 10% ownership.

{kind=link}

The Basics

- 1-Year Z-score: 0.28

- Discount: -15%

- Distribution Yield: 11.82%

- Expense Ratio: 1.45%

- Leverage: 28%

- Managed Assets: $999.5 million

- Structure: Term (anticipated liquidation date, December 15, 2033)

MEGI is your fairly standard closed-end fund , with the fund "seeking a high level of total return with an emphasis on current income."

To set this fund apart, the fund's twist compared to other infrastructure or utility funds is a "thematic theme." They are "focused on the investment megatrends of decarbonization, digital transformation, and asset modernization, which are reshaping the demand for infrastructure assets and driving income and growth potential."

The fund utilizes leverage through borrowings, and as we have noted previously, that meant seeing higher costs in this higher-rate environment. That pushed the fund's total expense ratio to 3.07% as of their fiscal 2023 from their abbreviated fiscal 2022 at 1.92%. The fund's fiscal year end is May 31, meaning that since then, the Fed hiked rates one more time in July since this report. Therefore, the borrowing costs would have bumped up a bit further.

More specifically, the fund pays a rate of OBFR plus 0.75%. Through fiscal 2023, that was an average of 4.16%. Today, OBFR is at 5.32%, pushing MEGI's borrowing costs to 6.07%.

If rates are cut next year as widely expected, that would be a positive for this fund (and mostly all leveraged funds.) Still, rates aren't expected to go back to the zero rate environment that we mostly had since the Global Financial Crisis. Therefore, it will still take some effort and success for leverage to pay off rather than the period when you could unquestioningly leverage up and it mostly just worked. All the while, it still adds additional volatility to the position, and that increases risks.

They've also taken their borrowings down from $301.8 million at the end of their fiscal year to around $284 million, according to the latest fact sheet for the period ended September 30, 2023. This was likely to keep the leverage level below 30%, as that is their target level of leverage.

MEGI Asset Facts (MEGI Fact Sheet)

Performance - Attractive Discount

Naturally, a comparison will want to be drawn between peers. However, with MEGI, they are a bit different. Peers such as Cohen & Steers Infrastructure Fund ( UTF ) and Reaves Utility Income Trust ( UTG ), probably the two most popular in this space, have outperformed MEGI since its launch. Also worth noting is that MEGI holds a preferred sleeve, which is more similar to UTF and also includes a preferred investment sleeve in its portfolio. In addition to that, the fund also takes a global approach, whereas UTG is primarily U.S.-based, with most of its portfolio in equities.

That said, it also highlights how poor utilities and infrastructure funds have really done during this period, as both of those funds show losses as well.

Ycharts

In the above, we can see that the total NAV returns for MEGI had really started to lag in the last few months relative to the others. On a total share price basis, the fund sunk significantly further, but that's where the fund went to a deep discount after launching.

As we can see below, the fund followed the traditional path of a CEF launching, and that is a massive drop to a deep discount. It has continued to bounce around the teenage range, and while it is off the bottom of that range, it is still at an attractive valuation.

Ycharts

In the last year, the performance of MEGI has been closer to that of UTF and UTG on both a total NAV and share price basis.

Ycharts

With all that being said, UTF and UTG aren't necessarily great peers because while there is overlap and they are investing in infrastructure, MEGI has a tilt that sets it apart. That is through investing in decarbonization, digital transformation and asset modernization.

Two other funds that come to mind that have a more unique twist on infrastructure.

One would be the Ecofin Sustainable and Social Impact Term Fund ( TEAF ). TEAF likewise takes an approach of investing not only in renewable investments but also in other infrastructure such as schools and elderly care facilities. However, a big differentiating factor with that name would be the fund's emphasis on private investment at nearly 50% of the fund. Additionally, the fund has meaningful exposure to corporate bonds.

NXG NextGen Infrastructure Income Fund ( NXG ) would be another. That fund primarily focused entirely on a split between energy and renewable energy sources. This fund was hit particularly hard with the renewable sell-off lately.

So, even within this category of unique infrastructure closed-end funds, there are significant differences that set each apart. For these reasons, I wouldn't necessarily see MEGI as a replacement for one of the other infrastructure funds in one's portfolio but as an additional diversifier in the portfolio. As we've already seen, there can be a divergence in the performance. Earlier in 2023, that even included MEGI outperforming on a total NAV return basis above these more popular traditional peers.

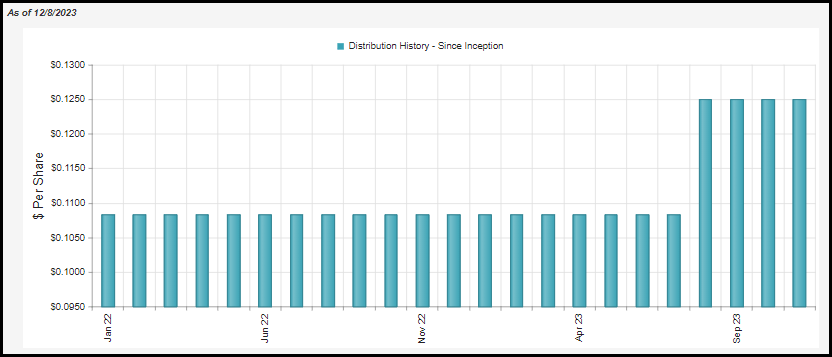

Distribution - Receives A Hike

Right around the time of our previous update, MEGI announced a bump in their distribution. While it wasn't warranted necessarily due to the weak environment, it generally has the positive impact of reducing a fund's discount when distributions start to get to the double-digit level. There's always a sort of balancing act between what is really sustainable and what can drive results through a narrowing discount.

Unfortunately, as highlighted above, it actually didn't seem to drive the discount to narrow - at least not during this short period. Then again, rates surging put a damper on everything and this was a relatively short period of time as well. Today, the NAV rate comes in at 10.05%, and thanks to the immense discount, the fund's distribution rate for shareholders comes to 11.82%.

{kind=link}

As we noted above, the fund's expenses have become pricier due to their leverage. We noted that this was going to have a negative impact on the fund's net investment income. Despite that, the fund's NII coverage came in at around 60% in their last report, which is still fairly strong on a relative basis.

MEGI Operations (MEGI Annual Report)

Of course, there are several variables to consider due to the increased payout leverage level and costs. On a per-share basis, the fund's NII came to $0.78 during this period. Against the now higher annualized distribution rate of $1.50, that would bring coverage down to around 52%.

With the fund deleveraging a touch while having their borrowing costs tick up a bit higher. Given the fund is generally paying more than what it is earning in terms of yield from underlying holdings, that impact could actually be net neutral. By having their borrowings decrease, they are paying less, but since costs were over 6% and the portfolio's NII rate is around 4.5%, it shouldn't be a negative on the income-generation front. On the other hand, it could also mean that there was less of a rebound due to deleveraging, as those assets wouldn't have been there to participate in the upside.

Ultimately, though, this fund's NII is quite strong relative to peers, even if it has come down to around 50%. UTG's NII coverage was around 30% , and UTF's NII coverage was around 27% .

For tax purposes, the fund has mainly seen the characterization of its distribution as largely ordinary income. However, with some time under its belt, some long-term capital gains are beginning to show.

MEGI Distribution Tax Classifications (MEGI Annual Report)

While the sizeable ordinary income might seem worrying, especially if one is holding in a taxable account, they also noted that $55,921,173 was designated as qualified dividend income.

MEGI's Megatrend Infrastructure Portfolio

The portfolio is invested primarily in equity securities. However, they still run with around 15.3% preferred, and that is a meaningful sleeve. That's about where the weighting was at the start of the year as well when it came into 2023 at a 14.5% allocation. Turnover of the portfolio as of the last report was 26%, so some of this could be simple gyration of valuations or some active changes by the management. Overall, the composition of asset allocation hasn't seen a material divergence through most of the last year.

MEGI Asset Allocation (MEGI Fund Website)

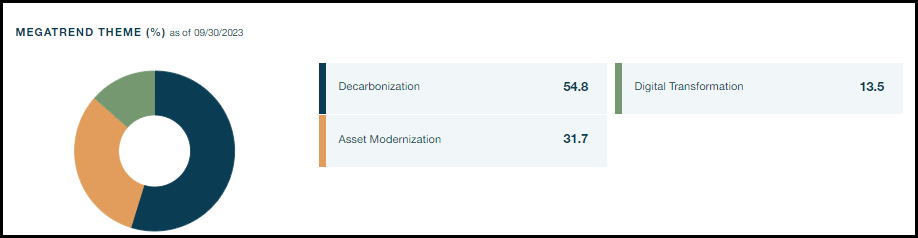

The fund's claim to fame is the "Megatrends thematic," and that comes through the three segments they've highlighted. They are mostly invested in the decarbonization theme, but asset modernization is certainly a significant weighting as well. These weightings are quite similar to where they were previously .

{kind=link}

Within these broader categories, they break out more specific subcategories . Within decarbonization, the fund is invested 36% in renewables and 19% within the "electrification/smart grid." Asset modernization category mostly belongs to 16% energy transition, 7% clean water/responsible waste and 6% transport mobility.

This unique split makes it an interesting infrastructure fund that isn't necessarily dedicated to any specific theme. Renewables continue to gain momentum and are expected to do so over the long term . That is, even if they are getting hit with higher interest rates that set them back more recently, NextEra Energy Partners ( NEP ) was a name that came out slashing growth expectations . This caused a sell-off across the board in the renewable space, though they've been able to rebound off of the lows, some better than others.

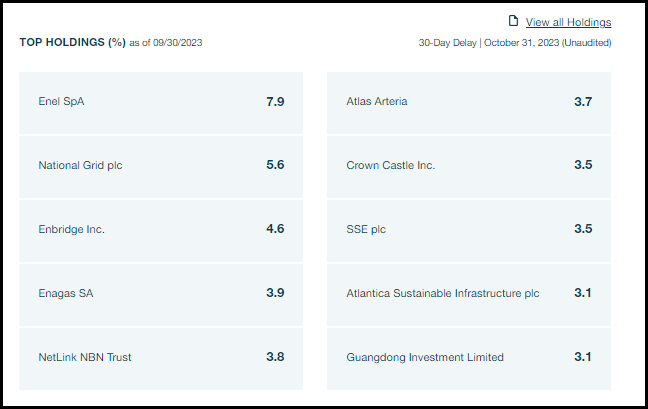

At the same time, the digital infrastructure bucket means we get some exposure to tower REITs such as Crown Castle ( CCI ), making an appearance in the top ten, or Digital Realty Trust ( DLR ), providing data storage. The fund doesn't hold any position in the equity of DLR but has three different preferred holdings in smaller allocations.

At the same time, the MEGI still holds positions in more traditional infrastructure plays such as Enel SpA ( OTCPK:ENLAY ), National Grid plc ( NGG ) and Enbridge ( ENB ). The simple fact is the vast majority of utility and infrastructure companies are including more and more CAPEX to push into renewables. This is really whether they want to or not, as regulations dictate that they do.

{kind=link}

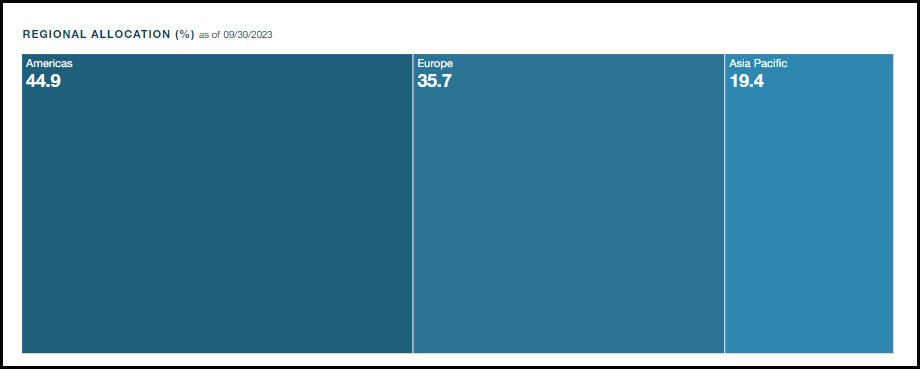

In the geographic bucket, we also see that this fund does place an emphasis on global investments. Other global funds don't tend to have greater than 50% of their allocation outside of U.S. securities. That included MEGI at the start of 2023, as the weighting was 50.1%, just ever so slightly pushing it over the edge. Though again, here, the overall shift hasn't been dramatic.

{kind=link}

Conclusion

MEGI is an interesting fund that provides unique exposure to not only renewables but a wider basket of "megatrend" themes in the infrastructure space. That can make it a perfect fit for an investor looking for added infrastructure diversification to go along with their more traditional infrastructure funds. At the same time, and more importantly, the fund is trading at an attractively deep discount.

For further details see:

MEGI: Megatrends Infrastructure Looking Attractive With A Deep Discount