MEGI - MEGI's Income Opportunities In Infrastructure Megatrends

2023-08-31 10:34:54 ET

Summary

- Factors reshaping the demand for infrastructure assets.

- MEGI's unique approach and potential opportunities presented by the fund.

- CBRE Investment Management Lead Product Strategist, David Leggette discusses the infrastructure sector, MEGI and the current market.

CEFA:

Welcome to CEF Insights, your source for closed-end fund information and education, brought to you by the Closed-End Fund Association. Today we are joined by David Leggette, Lead Product Strategist and Head of Investor Relations with CBRE Investment Management, a leading investment manager of global real assets. CBRE is sub-advisor to the MainStay CBRE Global Infrastructure Megatrends Fund, ticker MEGI , and New York Life Investment Management is the investment manager of the fund. David, we are happy to have you with us today.

David Leggette:

Thank you. Pleasure to be here. I appreciate the opportunity.

CEFA:

David, infrastructure investing continues to gain investor interest, but one of the challenges investors may find is that there is a wide range of definitions of the asset class. Can you describe how CBRE defines the infrastructure asset class and what differentiates MEGI's investment strategy?

David Leggette:

Sure. Happy to do that. MEGI is a closed-end fund. It trades on the New York Stock Exchange. It's an actively managed portfolio. It's built around three megatrend investment themes. The fund's objective is to seek to deliver high total return with an emphasis on current income.

In terms of the definition of the asset class, we invest in core infrastructure assets, owners and operators. These core sectors include utilities, transportation, midstream energy, and digital infrastructure. Core infrastructure assets are monopolistic by nature, an essential part of our everyday lives. And as a result of their essential nature, the demand drivers are relatively consistent and cashflow growth is relatively consistent regardless of the macroeconomic conditions.

This is an asset class that has delivered mid to high single digit earnings and consistent income growth across a full market cycle. While, this might seem boring relative to higher growth equities, our position is that boring is beautiful.

MEGI's thematic orientation, in my view, is what makes the portfolio interesting and is a key differentiator relative to peers. We believe three secular investment themes, decarbonization, asset modernization, and digital transformation are reshaping demand for infrastructure assets, which is increasing the required investment in essential infrastructure and therefore enhancing the earnings and income growth potential of the companies we own in our portfolio.

CEFA:

One of the important characteristics of closed-end funds is a fund's distribution policy. Can you please provide a brief overview of MEGI's policy?

David Leggette:

MEGI pays distributions on a monthly basis. And the fund utilizes a managed distribution policy which allows the fund to include realized capital gains as well as income in each of its regular monthly distributions. Our goal is to maintain a relatively attractive distribution rate, which over time does not exceed the NAV growth of the fund, thereby preserving the fund's capital base and limiting distributions of return of capital.

To that end, on July 26th, the fund announced a 15% increase to its regular monthly distribution. The new rate is 12 and a half cents per share on a monthly basis or a $1.50 annualized. We believe the combination of MEGI's now higher regular monthly distribution rate combined with its market price trading at a greater than 10% discount to NAV, represents a compelling opportunity for investors today.

CEFA:

David, given the market backdrop of persistent inflation and higher-for-longer interest rates, what are the key factors that support the decision to increase the fund's distribution?

David Leggette:

The decision to raise the distribution at this time is a reflection of our positive outlook, underlying fundamentals of the asset class, as well as global infrastructure's total return potential. There are three key things supporting our high level of confidence in the sustainability of our distribution.

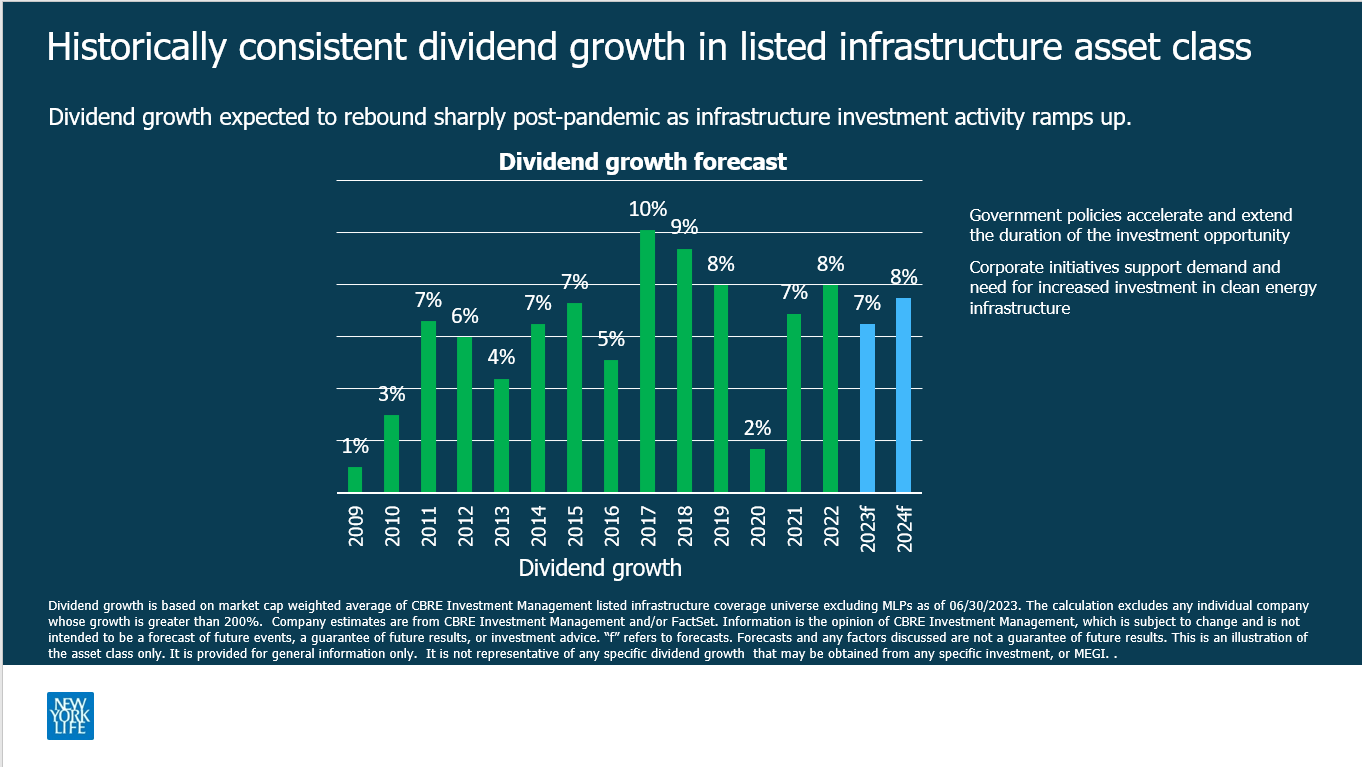

Number one, relative strength of earnings and consistent income. Our team is underwriting consistent earnings growth of 7% to 9% over the next two years with a similar growth potential for underlying income distributions from the companies.

{kind=link}

Point number two, positive inflation sensitivity of infrastructure company cash flows. Inflation management is a hallmark of the asset class. And one of the characteristics we look for in selecting securities for the portfolio is a company's ability to pass through rising costs to the users of their assets.

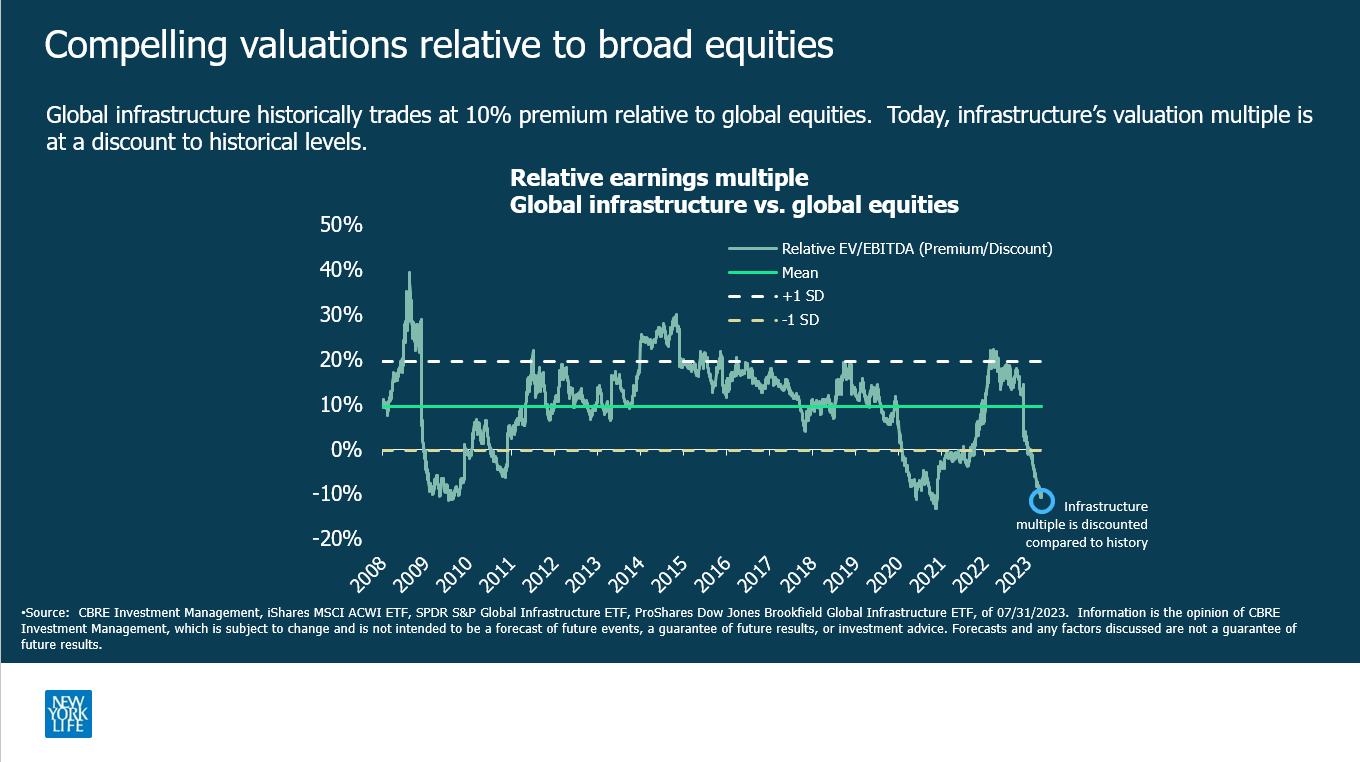

And number three, listed infrastructure valuations are at historic discounts relative to broad equities. While infrastructure has generated a positive total return year to date, it has trailed broad equities by a wide margin. We believe the market may have already priced in the rebound for broad equities and that global infrastructure valuations are attractive on an absolute basis as well as relative to equities. As we move into the second half of the year, we believe the consistency of earnings and discounted valuations will be a source of incremental demand and increasingly positive total return potential for global infrastructure.

{kind=link}

CEFA:

The current administration has placed an emphasis on infrastructure spending. How important is government spending to the success of the infrastructure companies in MEGI's portfolio?

David Leggette:

What I always like to point out to our clients is that it's really about favorable government policy as opposed to government spending. That's most beneficial to the company that we own. Infrastructure earnings are expected to benefit from consistent demand trends and favorable government policy. A great example is the Inflation Reduction Act, which was passed last year in August of 2022, and this really provides a favorable backdrop for this visible growth. The Inflation Reduction Act is designed in part to promote energy security for Americans and its goal is to ensure that we're not overly reliant on one single source of energy. We believe that utilities and midstream energy companies will be the primary beneficiaries of the act, which provides tax incentives for the production and development of clean energy, including new technologies.

CEFA:

How is the MEGI portfolio currently positioned?

David Leggette:

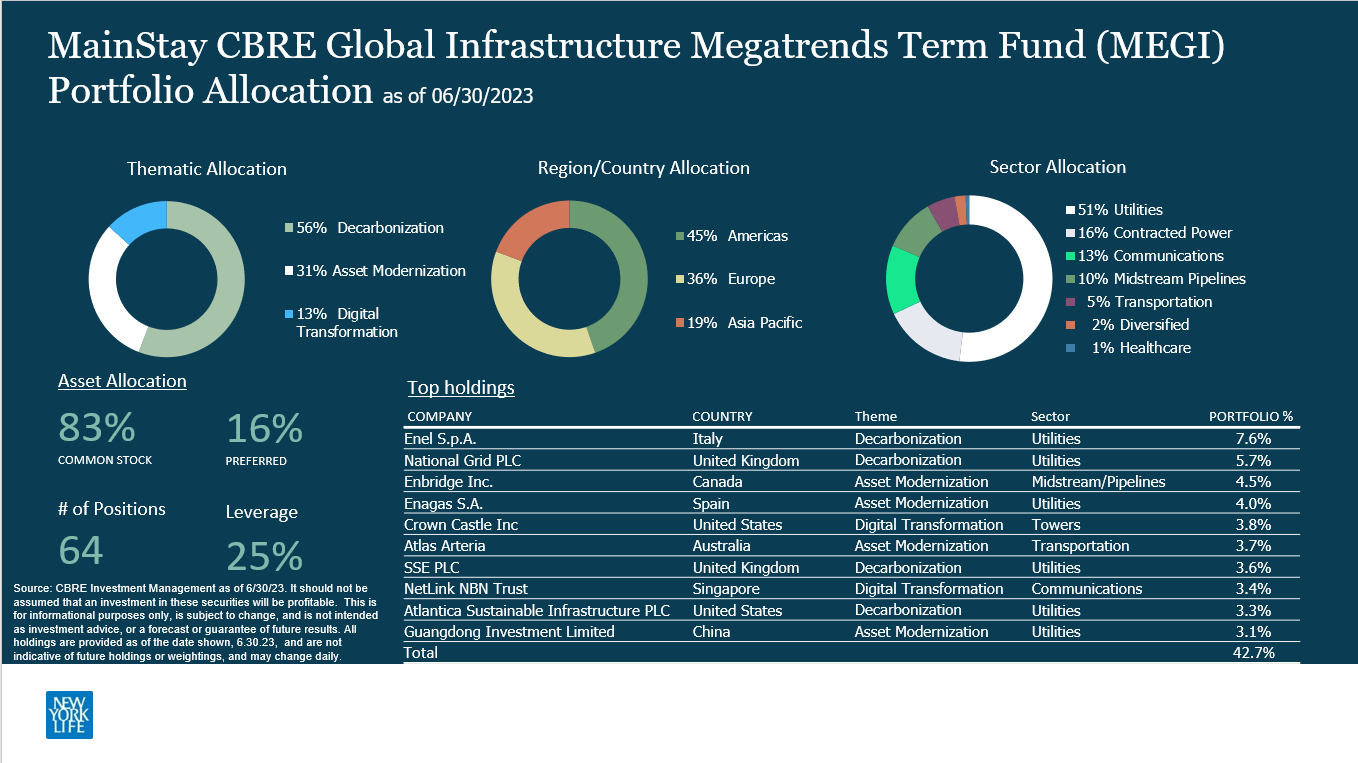

Our strategy is to target companies that own, operate, and develop core infrastructure assets. Our focus is on companies with resilient cash flows and what we believe to be sustainable income growth. The portfolio currently owns 64 positions, so relatively concentrated, 83% to common equity securities, 16% to preferred shares.

The portfolio uses leverage with the goal of enhancing distributions to our shareholders. At the end of the quarter, the leverage level was 25%. And we've reduced it. Nine months ago, leverage was at 32%. We've taken that down. But while we've reduced leverage, it remains elevated, and it reflects our positive total return outlook.

In terms of geographic focus, we focus on developed markets, so the portfolio is currently allocated across 46% to the Americas, US, Canada. We have some exposure to Latin America as well, Europe, UK, also the continent, 35% of the portfolio, and the Asia Pacific region, the remaining 19%.

In terms of the fund's thematic tilt, decarbonization is the largest thematic sleeve, 56% of the portfolio. The asset modernization, which owns approximately 31%, and there our allocation is across toll road companies as well as midstream energy companies. Digital transformation, 13% of the portfolio. This is our investments across communication towers, fiber networks, and data center assets.

Overall, we believe the portfolio is well positioned to continue to generate attractive returns in the current market environment.

{kind=link}

CEFA:

David, how do you see this thematic global infrastructure strategy best positioned in an investor's diversified portfolio?

David Leggette:

Infrastructure over the long term has had a low correlation to bonds and has delivered a total return in line with broad equities. As a result, many clients utilize the equity portion of their portfolio as a funding source. I believe that MEGI's a strong compliment to investor portfolios seeking high current income, supported by consistent inflation linked cash flows, and growth potential tied to the increased and changing demand for infrastructure assets.

CEFA:

David, thank you so much for taking the time to share your thoughts with us today.

David Leggette:

You're welcome. I appreciate the opportunity.

CEFA:

And we want to thank you for tuning into another CEF Insights podcast.

For further details see:

MEGI's Income Opportunities In Infrastructure Megatrends