ARCH - Met In The Arena: Switching From Arch To Warrior

2023-08-28 08:32:46 ET

Summary

- My old position, Arch Resources, has underperformed peers in the met coal industry year-to-date.

- The new "floor" for met coal index prices is expected to be around $200-250/ton, which makes all major US producers very intriguing investments.

- I favor Warrior at this juncture due to their low-cost production and growth opportunity from Blue Creek.

I’ve covered many stocks on Seeking Alpha, and sometimes I must write a piece owning up to a mistake. Some have been “good mistakes”, like thinking GameStop ( GME ) could fix their business and instead I benefited from the ensuing mania. Today is another one of those, as my long position in Arch Resources ( ARCH ) has been highly profitable over the past 18 months. However, I’ve switched horses, and wanted to share my thinking with the community.

Arch: What Changed?

My thesis on Arch was fairly simple – they're a low-cost producer with both Thermal and Metallurgical ("Met") coal exposure, and they have a strong history of generous capital returns. Well, what I expected was what played out . If you bought the stock when I first published in 2022 , you've experienced 30% price appreciation and over 30% of your cost basis in dividends. Not bad in this market. Unfortunately, year-to-date Arch has under-performed peers Alpha Metallurgical Resources ( AMR ) and Warrior Met Coal (HCC) on total return after hanging very close in 2022. I expect this underperformance to persist for the following reasons:

-

Thermal Weakness : Arch benefited tremendously with their thermal exposure in FY22, with tons sold out of their West Elk mine approximating extra met tons with how strongly realizations rose. This reversed in FY23 when they hit a clay seam that has reduced yield from the mine. Worse, the reduced tons are those that usually went into the export market for better realizations. Fortunately, Arch expects this headwind to be behind them in Q4-23. Unfortunately, this has also been accompanied by reduced Powder River Basin (“PRB”) demand (lower-quality thermal coal), which is facing headwinds from new EPA regulations . Peer Peabody Energy ( BTU ), continues to grossly underprice their PRB tons, making the likelihood of increased profitability in this region remote.

-

High-Vol Glut : Due to the increase in tons from Leer South, and the newly opened Allegheny Met mine , there is now a bit of a “glut” developing of high-vol, high sulfur met coal coming out of West Virginia. If Arch maintains a ~$10/ton cost advantage over their primary peers, this will be neutralized by realizations coming in lower compared to low-vol and mid-vol met coal producers. Alpha noted on their latest call that with the Australian index at $246/ton ( now ~$260 ), US low-vol was $215, high-vol A was $203, and high-vol B was $193. To illustrate further, consider the most recent quarters for Arch, Alpha, and Warrior:

-

Alpha sold 2.7m export tons (aside from 1.1m domestic) for a realization of ~$168/ton, with an average cost of $106/ton, for $62/ton margins .

-

Arch sold 2.3m tons for a blended realization of $153/ton, with cash costs of $90/ton. This includes some domestic tons sold near $184/ton, which helped support Q2 pricing and $63/ton margins .

-

Warrior sold 1.8m tons in Q2, though their numbers are presented somewhat differently than Arch and Alpha, with transportation costs included. Total realization was $209/ton with $129/ton costs, almost exclusively into the export market for $80/ton margins .

In summary, despite being a “low-cost” operation, Arch is seeing no margin advantage versus comparably sized US peers in the export market, and Alpha has a significant edge in the domestic market, where margins are highest for now.

Higher For Longer?

It is worth considering what the new “floor” should be for met prices, given significant cost increases across the industry.

-

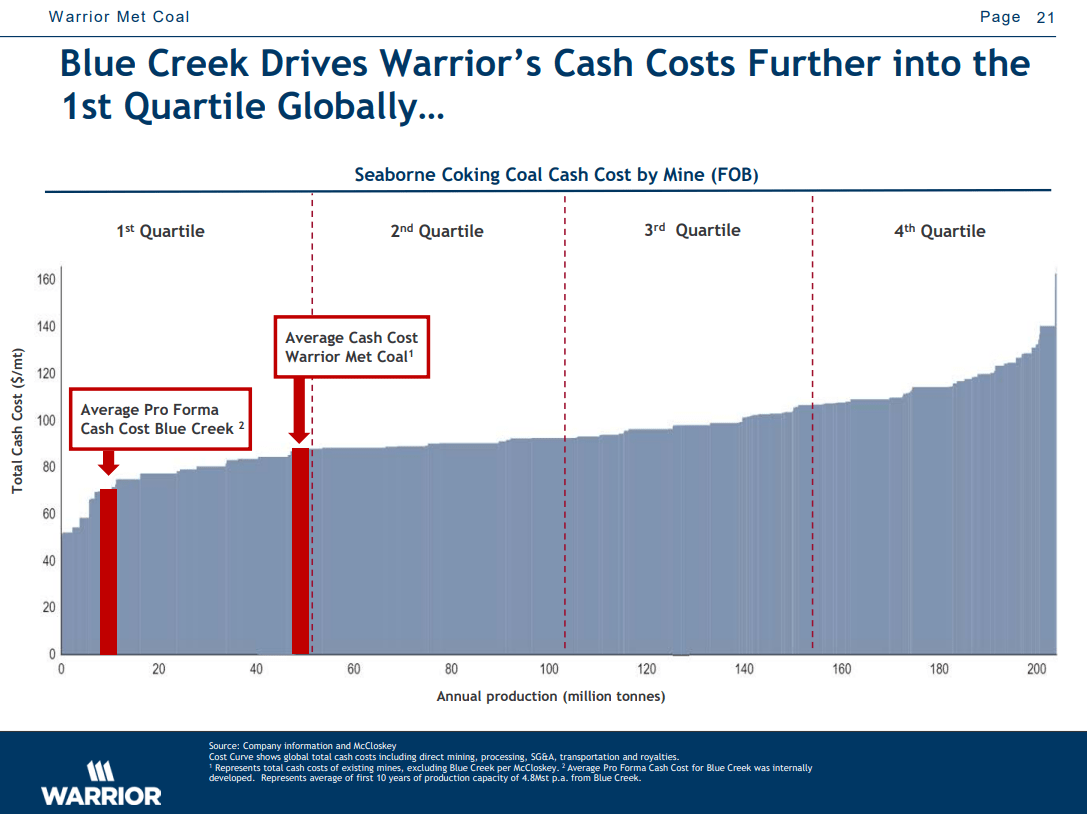

Arch noted on their Q1 call that marginal US production costs appear in the range of $130/ton, suggesting current east coast ~$200 index prices are about as low as can be sustained after deducting rail expenses, CapEx, and taxes. The slide below from Warrior seems to support this.

-

Given new Australian royalties , if you’re a met coal producer there is very little incentive to bring a new mine online with index prices at $210/ton. This serves as an important difference for those trying to compare costs to pre-covid times. Case and point, one large Australian producer is now looking at all-in costs north of $200/ton for FY24.

I think this is a key item being missed by analysts looking at the met coal space. People can see index prices around $150/ton pre-Covid and assume these remain possible again, but few operators have a cost profile that makes this tenable going forward. Unless new, lower cost tons appear in the market, I expect $200-250/ton on the indexes is going to be the new floor.

Global Cost Curve (Warrior Investor Deck)

{kind=link}

Impact

With Arch generating met margins equal to Alpha, their cost advantage evaporates compared to Alpha’s significantly higher production rates. Arch’s Q2 costs were at the high end of their guide, and they should be able to do a bit better, but there is now evidence they’re being forced to take a hefty benchmark discount on coal sales. Arch continues to tout their thermal contract book being very strong for the next several years, and it likely can drive $200-300m of annual EBITDA once West Elk returns to form. This just isn’t enough to offset Alpha’s >50% advantage on met production volumes.

The comparison that’s tougher is Arch and Warrior. A union strike has suppressed Warrior’s volumes, resulting in them only producing 5.7m of their 8.0m tons of nameplate capacity in FY22. Volumes are increasing in FY23 and they have guided to business as usual in FY24. In FY25, tons from their Blue Creek operation will start to hit the market, and full longwall deployment is expected in FY26. So Warrior has the benefit of incremental growth coming for each of the next several years , but the huge headwind of CapEx spending at Blue Creek absorbing their current net cash balance. However, Warrior can produce at better margins than Arch. Back in 2019, Arch achieved met margins of $39/ton, versus $71 for Warrior, and the gap persists today despite Warrior’s strike-depressed production.

Which Is Most Attractive

I think something remains for everyone here, and that investors in Alpha, Arch, and Warrior will all do very well over a 3-5 year timeline.

-

Arch trades for about a $2.3B enterprise value (“EV”). If met margins stay around $70/ton for them, and thermal can produce $200m EBITDA annually, the business should be able to maintain $500m of FCF. Splitting that between buybacks and dividends, this generates a nice ~11% yield for shareholders, while shrinking outstanding shares annually at a similar rate. For income-oriented investors this will be the most attractive, or those who have a bullish view of Arch’s US thermal assets.

Arch Met Production (Arch Investor Presentation) Arch Thermal Production (Arch Investor Presentation)

{kind=link}

{kind=link}

-

Alpha trades at a slightly higher EV of $2.5B, and $70/ton margins should be enough to generate $700m of free cash flow annually. Alpha can deploy this at a ~25% yield buying back stock, and their recent capital allocation update was to cease any dividends and focus on the buyback. The risk is the price goes up, but the earnings don’t follow, and soon Alpha’s return on buybacks diminishes. For example, met margins are weak at the moment yet Alpha trades near all-time highs. This is aided by their continued reduction in share count, but if margins are closer to $50/ton long-term, Alpha’s cash flow yield will be ~15% here. Still a nice capital allocation option, and if earnings spike again, they will be spread over a progressively smaller share count.

Alpha Share Reductions (Alpha Investor Presentation)

{kind=link}

-

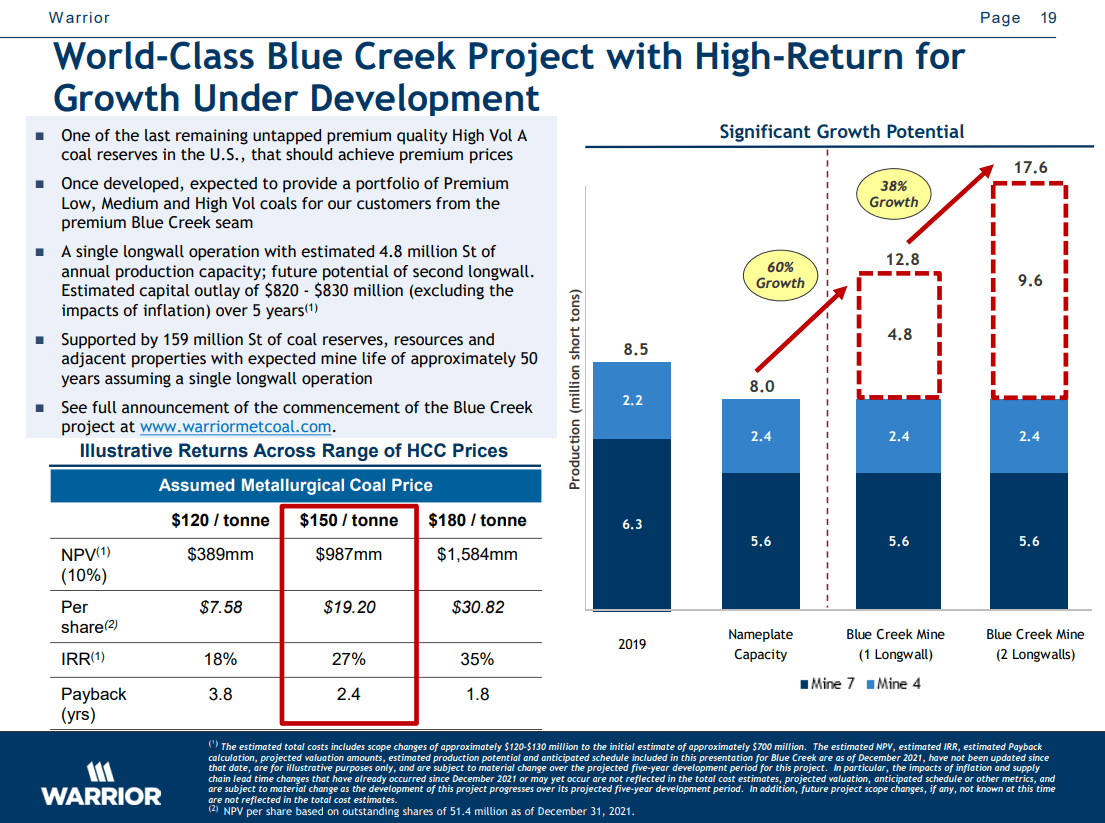

Warrior is not yet buying back shares, as they have been stuck protecting NOLs set to be exhausted this year. Their focus is getting Blue Creek fully operational by FY26, spending nearly $1B at what should be 40% IRRs with met coal indices at $250. In other words, this is the highest rate of return available to these met coal producers in a $250 price environment. Warrior would exit FY26 with ~12m tons of production and the best margin profile of the three major US producers.

Blue Creek Economics (Warrior Investor Presentation)

{kind=link}

As a result, I favor Warrior as an investment, as I prefer the safety that comes with lower-cost commodity producers, and I like the upside that comes with the highest-upside IRR at current coal prices. All three should be able to generate >20% IRRs at current prices between growth, buybacks, and dividends, making which one to buy a bit of a “champagne problem”.

I’m also long shares of Corsa Coal ( OTCQX:CRSXF ) due to their recent stabilization via fixed contracts and their windfall settlement with PennDOT , but that is more of a special situation. The long term Met coal thesis runs through the big US players, and that is the focus of this piece.

Risks

Coal companies are exposed to generic commodity producer risks: volatile prices, inflated raw material costs, and vulnerability in a recession. With the balance sheet repair that has taken place in the past 2 years, I think these producers are better situated to weather a future downturn.

Because of China's significant share of global steel production, a decrease in Chinese demand for coal could be a headwind . However, note that very little US Met coal currently ships to China.

Warrior will be at risk of revisions to their Blue Creek project until it can be delivered.

Conclusion

Met coal producers like Alpha, Warrior, and Arch seem very well positioned for the “new normal” operating environment post-Covid, with indexes appearing to stabilize in the $200-250/ton range. Using different assumptions and investment goals, I believe you can justify any of the three at an attractive rate of return, but I have pivoted from Arch to Warrior. Their Blue Creek project and cost advantage on produced tons, along with incremental other growth avenues make it the most attractive for me at this stage. Think I’m crazy? Let me know why in the comments.

For further details see:

Met In The Arena: Switching From Arch To Warrior