MGM - MGM Resorts: Trading At Attractive Multiples Potential For +40% Price Appreciation

2023-08-18 08:13:33 ET

Summary

- MGM has undergone major structural changes as a company over the last few years.

- However, it emerged stronger than ever from the pandemic with a deleveraged balance sheet and an impressive portfolio of properties.

- We think it is trading at very attractive multiples and see the potential for a +40% appreciation in the stock price.

- The management knows the stock is cheap, has been buying back stock like crazy, and they will continue to do so.

Investment Thesis

MGM Resorts International ( MGM ) is one of the largest global gaming operators. In the last few years, the company has undergone major restructuring changes but has emerged stronger than ever. With a strong balance sheet and portfolio of assets, we think the current price point and substantial capital returns from the management in the form of buybacks will propel the stock higher during the next few years.

Company Overview

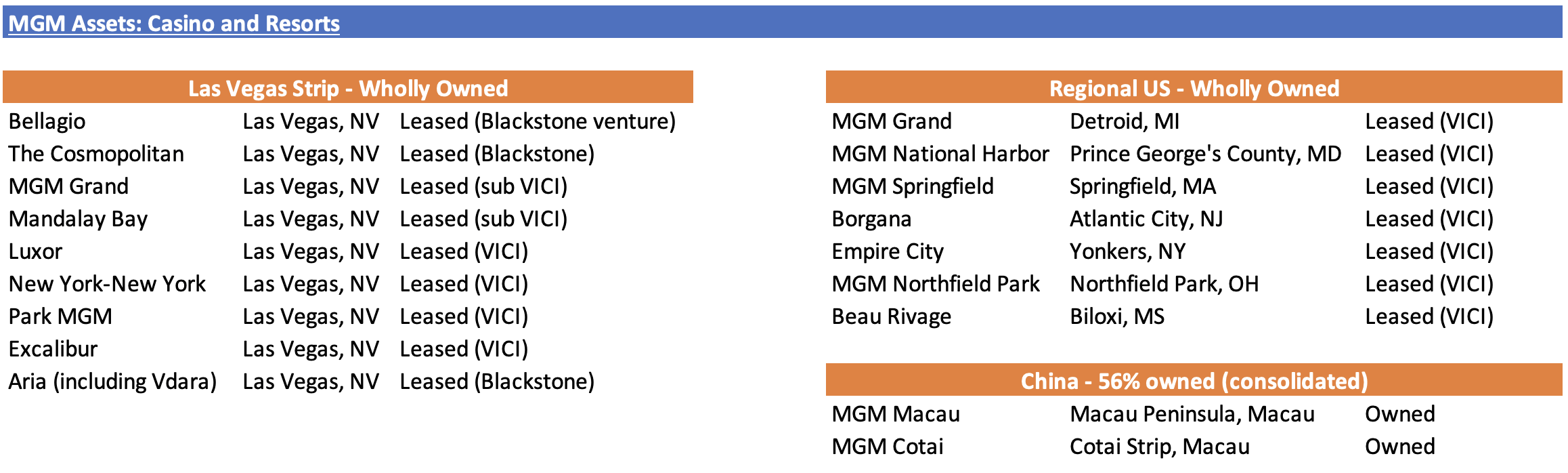

MGM operates 16 casino resorts in the US and, through their 56% controlling interest in MGM China, operates two casino resorts in the region of Macau. They also have global gaming operations through their consolidated subsidiary LeoVegas and their unconsolidated 50% owned venture BetMGM. Here is a view of all the casino and resorts operations of MGM as of Q2, 2023:

{kind=link}

As opposed to other US peers, MGM doesn't operate all that many properties relative to the company's size, preferring to concentrate their portfolio in large and premium properties. Also, as you can see, MGM doesn't actually own the casinos and resorts in the US; instead, they lease these properties. This is because MGM restructured in 2016 and, in an effort to become a more asset-light business, IPOd a dedicated REIT, MGM Growth Properties ( MGP ). MGP was the owner of the real estate underneath most of MGM's assets. Then, in 2021, MGP was acquired by VICI Properties ( VICI ), another REIT formed in 2017 as part of Caesar's bankruptcy restructuring. As part of the deal, VICI paid $4.4 billion for MGM's stake. MGM has generated several billions from these transactions that have gone toward acquisitions, debt reduction, buybacks, and general padding of the balance sheet. Most notably, shares outstanding have decreased ~35% and long-term debt ~50% since 2018.

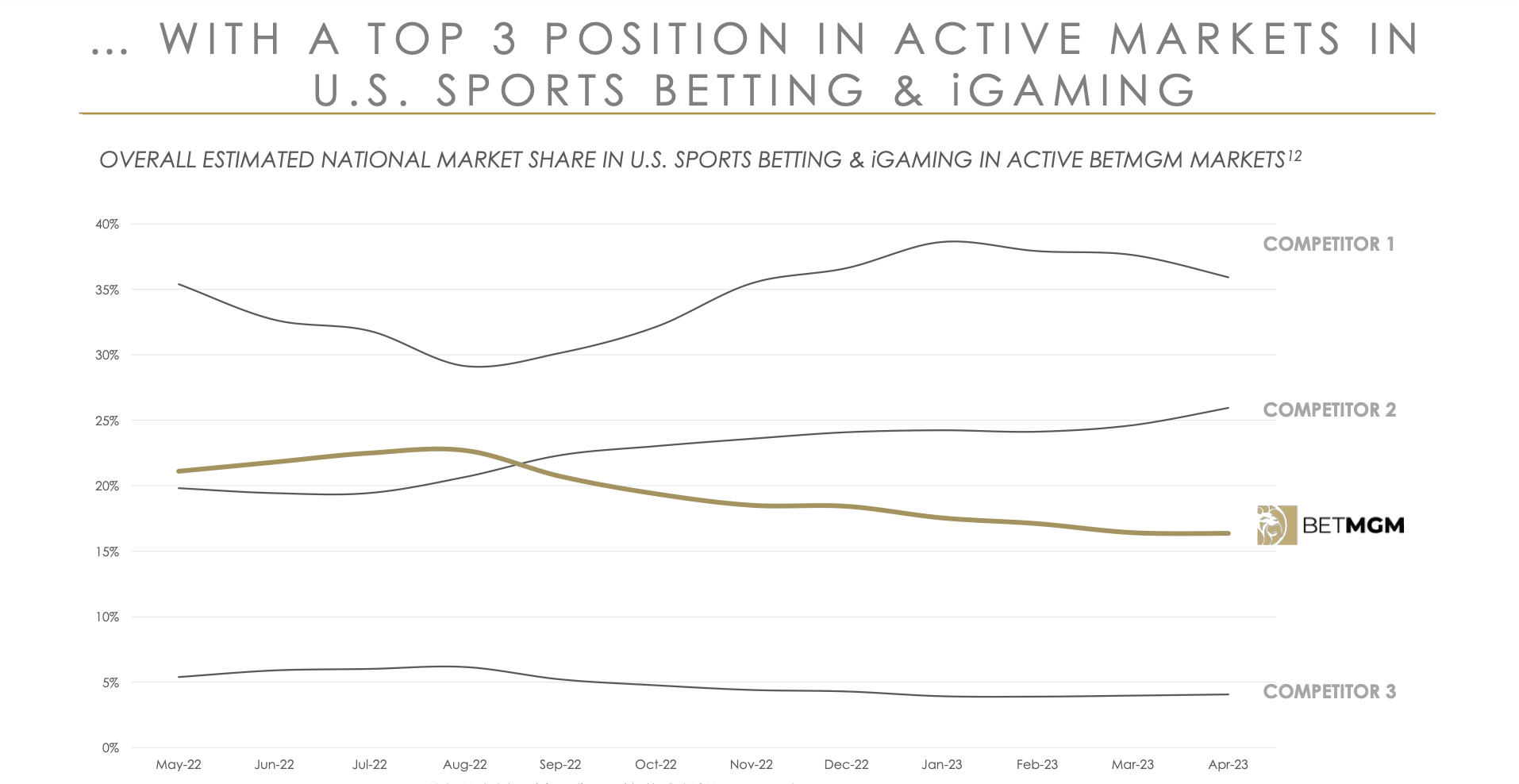

MGM is also a big player in the online betting market. In July 2018, MGM and UK-based online operator Entain ( GMVHF ) announced BetMGM as a 50/50 venture. The basic idea was that Entain provided the best tech stack and MGM had a big brand, broad day-1 market access, and a large database of loyalty members and bettor profiles in the US. As of Q2, 2023, BetMGM was active in 26 out of the 50 US states, with an overall market share of around 18%. Although it has been trending lower, BetMGM is much larger in the iGaming category than sports betting, which is a more regulated activity and legal in only 6 states so far. Their biggest competitors are DraftKings ( DKNG ) and FanDuel.

{kind=link}

MGM is also pursuing the online betting market internationally through LeoVegas, a similar operation to BetMGM with presence in Canada and 9 European countries. They acquired the company through a tender offer last September and paid a total of $556 million.

Overall, we think of the company as a luxury casino and resort operator with a call option in the online betting market, not only in the US but internationally as well.

Q2 2023 Financial Results

MGM reported Q2 financial results on August 2. They recorded $3.94 billion in net revenue, a 21% increase YoY and an all-time quarterly record. Revenue from Las Vegas and Regional operations were flat and slightly down YoY, while MGM China grew 418% YoY, or just 5% vs. Q2 2019.

Operating income was also strong, coming in at $371 million. This represented a 9.4% margin vs. 3.2% in Q2 2022 (after adjusting for dispositions related to the sale of MGP). EBITDAR, on the other hand, was $1.1 billion. Although it decreased -6% and -14% for Las Vegas and Regional operations, it rose +21% for MGM China. Net income, on the other hand, was $201 million or $0.55 per share.

Year to date, the company generated $887 million in free cash flow, although they returned a lot more to shareholders. They repaid $2 billion of debt and bought back $1.1 billion of stock. As a result, shares have risen 28% in 2023. Moreover, the company still has $2 billion in excess cash and equivalents, which will be used to continue to buy back shares in the second half of the year.

We think MGM had a great quarter, and it's experiencing strong momentum, especially in China. The lack of revenue growth in the US operations has to do with the dispositions of a few resorts during the last year, but the overall market remained very strong. Occupancy was at 96% with an average daily rate of $234, up 4% YoY. Another thing we really like is the aggressiveness that management is buying back shares. It is evident that they see value at current prices, as we will discuss later.

Outlook

One of the biggest projects MGM has in the pipeline is the development of a casino and resort in Osaka, Japan, in a joint venture with ORIX, which was approved by the government earlier this year. The resort would have ~2,500 total guest rooms, ~400,000 square feet of conference facilities, and a ~3,500 theater. They expect the total cost would be ~$10 billion and project more than 20 million visitors each year. MGM will control 40% of the resort's operations when everything is finished. The company is also looking to obtain a commercial gaming license in New York.

The company also continues to invest in its existing properties: they started a three-year remodel project at the Bellagio, they are fully-upgrading The Mandalay Bay Convention Center and also are pursuing major remodeling projects at the Borgana as well as the New-Yor.

They didn't provide any guidance, but the market expects full-year revenue and EPS to come in at $15.75 billion and $2.42, which would represent 20.4% and -30% change YoY respectively. Note that the EPS in 2022 was affected by the disposition of various casinos and resorts.

Valuation

We believe that MGM should be valued in two parts: their casino operations and their online-betting ventures, mainly because BetMGM is not consolidated in their results.

MGM is currently trading at 9.5x EV/Forward EBITDA. Its peers such as Las Vegas Sands Corp. ( LVS ), Wynn Resorts ( WYNN ), and Caesars Entertainment ( CZR ) are trading at an average of 10.5x. In our view, this means that the market fairly valuing their casino operations, but they are assigning no value to their BetMGM venture.

BetMGM generated $1.44 billion in revenue in 2022 and had an operating loss of $469 million (estimated). They did not disclose EBITDA, but we know it was around negative $400-450 million. DraftKings, on the other hand, made $2.24 billion in revenue and had an operating loss of $1.51 billion, with a negative EBITDA of $721 million. Despite the lower revenue, BetMGM is more profitable than DraftKings. This has to do with the fact that iGaming, where BetMGM holds a bigger market share, is much more profitable than sports betting. For 2023, BetMGM is estimated to do $1.8-2 billion in revenue and achieve positive EBITDA in the second half of the year.

How much is DraftKings worth today? A staggering $12.7 billion. Although we think that DraftKings is way overvalued, in Europe top online gaming operators have typically traded at >10x EBITDA. If we assume that BetMGM will be able to maintain its market share and factor in long-term EBITDA margins of 35% as management expects, with the addition of new iGaming markets, it can comfortably generate $3-4 billion in revenue in 2025 and an EBITDA of $1 billion. This equates to a $10 billion asset, of which $5 billion is accrued to MGM shareholders.

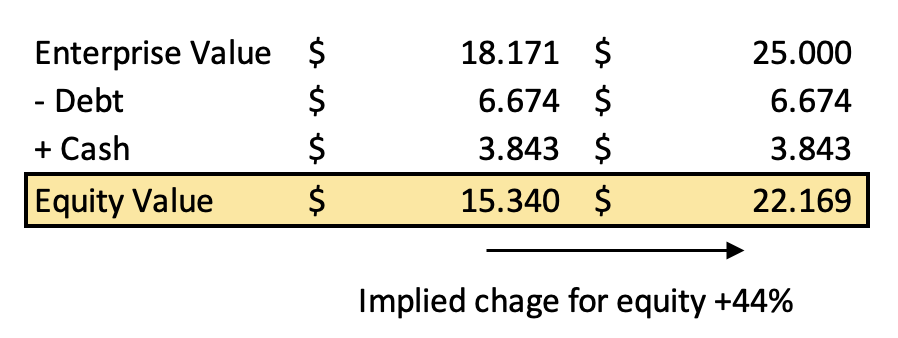

Overall, we believe MGM EV should trade in the range of $25 billion: 10 times their 2023 expected EBITDA (~$2.04 billion) for their casino operations plus $5 billion from BetMGM. This implies an increase of 44% from current levels.

{kind=link}

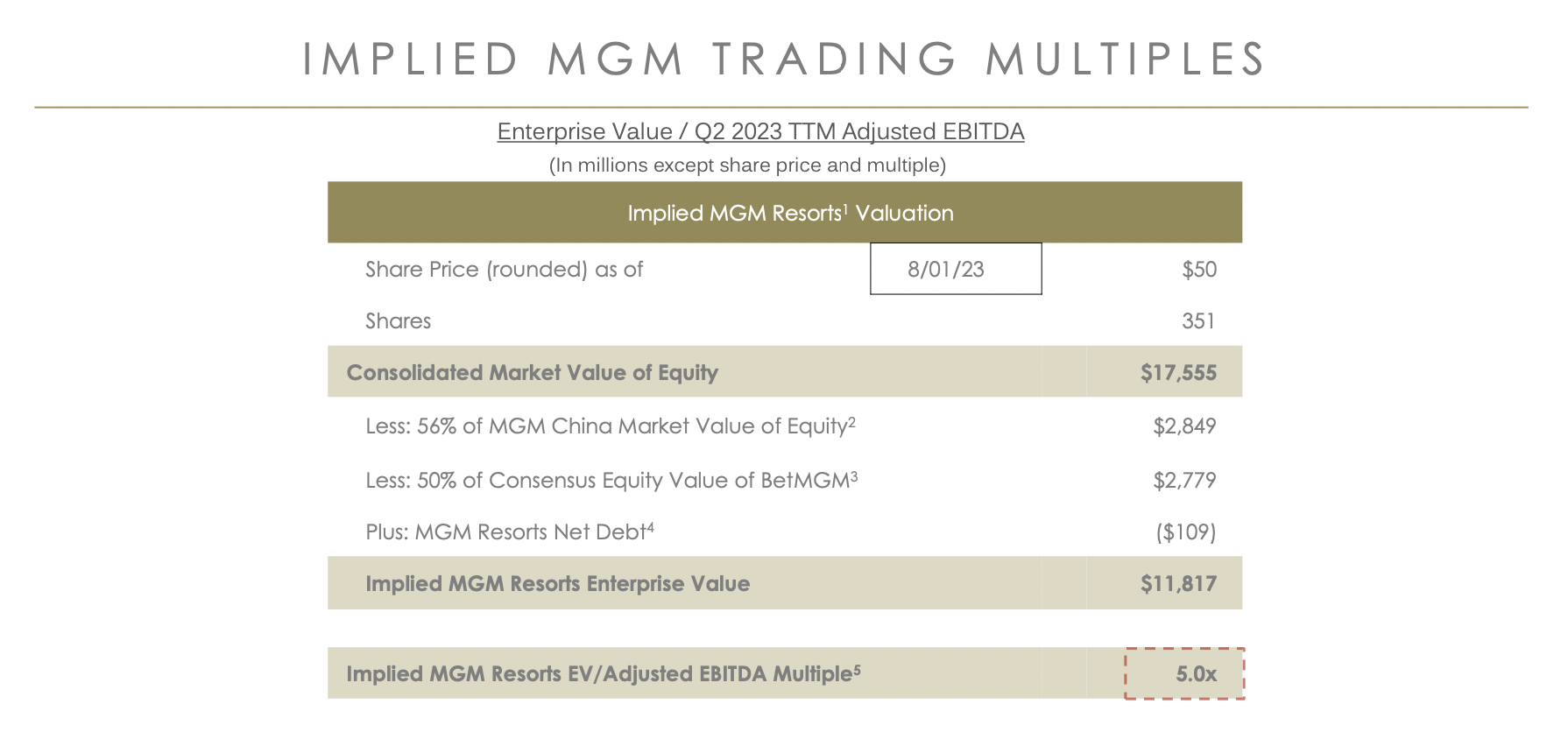

As we mentioned before, the management also believes the stock is cheap. They estimate that the market is valuing the casino and resort operations at 5x EV/EBITDA. The ratio is even lower now since shares have fallen from $50 to $42.

{kind=link}

Risks

MGM's business is very dependent on Las Vegas. Half of their casinos and resorts are located in that city. And they also suffer increased competition in the Strip like, for example, the new MSG Sphere.

The company is also very dependent on the economic situation. A potential recession would hurt leisure travel and spending all across the US. And although the company has a strong balance sheet, there is always a chance they start losing money and have to tap the credit market again.

Geopolitical tensions, especially between China and the US, can also impact the company's bottom line in unexpected ways.

Takeaway

MGM has done a phenomenal job over the past years deleveraging their balance sheet and returning capital to shareholders. We expect they will continue to do that in a substantial way and, given their valuation, we think it is an attractive stock that deserves to be part of your portfolio.

For further details see:

MGM Resorts: Trading At Attractive Multiples, Potential For +40% Price Appreciation