MSEX - Middlesex Water Company - Continues To Be Too Expensive

2023-08-18 09:41:12 ET

Summary

- Middlesex Water Company continues to trade very expensive.

- The quality of the business is there as the services are essential.

- Based on the quality though, the value for investors holding shares is present enough to warrant a hold.

Investment Summary

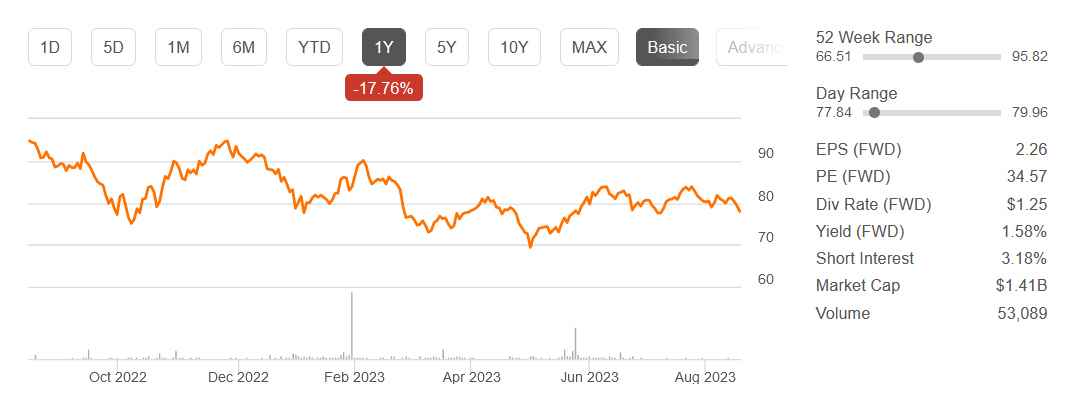

It seems that almost all water utilities stocks are trading at a high multiple these days and Middlesex Water Company ( MSEX ) is no different. With an FWD p/e of around 35 can the company provide any value to investors right now? Well, in my view, the company does pose some significant danger as a buy because of the rich valuation, but because of what seems to be the nature of the industry, water companies might continue trading at high multiples due to their relative stability for generating revenues and handling margins.

That isn't to say it should be rated a buy, I find it too uncertain and MSEX continues trading at these price levels and premiums in the long run. Investors can still capitalize on some positives here though I think, most notably the dividend and the stability of the market the company operates in. As a result of this, I am rating MSEX a hold right now instead of a buy.

A Look At The Business

As we have gone over with the MSEX already, it operates in the water utilities sector where giants like American Water Works Company Inc ( AWK ) also exist and operate in. In comparison, MSEX is significantly smaller at a market cap of $1.4 billion to the $27 billion somewhat that AWK has. What they do have in common though is a high multiple as both of them trade around the 30x earnings mark.

Segments (Investor Presentation)

Looking at how MSEX has divided its operations there are essentially two different segments right now that make up the business. The first one is the Regulated segment and secondly, we have the Non-Redulated Contract Services. The first segment primarily focuses on collecting, treating but also distributing water on both a retail and wholesale scale. Customers include both residential and commercial ones in the area of New Jersey and Delaware.

The second segment in the business places its focus instead on the operation and maintenance of municipal and private water and waste systems in the same areas as the first segment.

Growth (Investor Presentation)

The market for water does lack significant catalyst as no real new technology is going to revolutionize the need for it or how we manage it. Rather, MSEX needs to find innovative ways of growing revenues, like expanding and taking market share through contracting. Acquisitions are also a great way for the company to drive more growth and acquiring investors has also been a priority for the company. This added influx of capital perhaps could be an explanation for the high p/e that the business receives.

Customers (Investor Presentation)

Looking at the chart above here further underscores that MSEX is unlikely to see a catalyst in terms of customer growth, but rather a focus should be placed on that the company can maintain existing ones and drive some growth YoY at least, which they have done with their Delaware operations. As for the performance of MSEX, they have managed to maintain a strong ROA of 3.3% and an ROE of 9.3% which has made them able to maintain dividend growth for the last 19 years. The dividend is where I think most of the value can be derived for investors. A 5-year average growth rate of 6.82% is solid and highlights the quality you are getting here.

Quarterly Result

In terms of the results from the last quarter both the top and bottom lines impressed I think. Quarterly operating revenues were up 7.9% and the EPS rose by 10% YoY. The growth of the revenues where primarily due to the implementation of the final phase of the 2021 New Jersey Board of Public Utilities approved base rate increase. This resulted in higher contract customer demand.

Operating Results (Earnings Report)

Operating expenses seem to be growing every year for the company, so seeing revenue growth is indicative of solid EPS results still. Some of the growing expenses have been operations and maintenance and depreciation. What continues to negate the buy case is the fact that despite the second quarter to 2023 showing solid results, the 6 months so far into 2023 show a different picture as the net incomes are down. For investors in the company, it will be crucial to see an improvement in the coming quarters.

Risks

The current valuation indeed appears to be on the higher side which seems to be a factor for the sector and in general for water utilities. However, predicting the potential correction in this scenario becomes a complex task due to the absence of an apparent catalyst. It's noteworthy that stocks exhibiting low volatility like this one can often exhibit a disconnection from the underlying fundamentals for extended periods. I think there needs to be a significant change in either regularity policies that would negate companies like MSEX from making too much profit, or that a portion of it would need to be diverted to the government instead as a special tax. I think we are far from that happening and the relative safety of water companies is going to ensure the high valuation remains, but neglecting the risk of it would be a mistake still in my opinion.

These low-volatility stocks tend to have a certain level of resilience and stability that can sometimes defy immediate market trends. In the absence of significant market catalysts, they can continue to hold their ground, remaining insulated from abrupt price adjustments. This phenomenon is particularly noticeable during bear markets, where these defensive stocks, characterized by their low beta, have the potential to outperform for longer durations than one might initially anticipate. I think these qualities are what ultimately makes it such a decent hold for investors still.

Valuation & Wrap Up

One factor that seems to be true for water utility companies is that they mostly trade at what most would consider high valuations. For MSEX that means a p/e closer to 35 then some more normal like 20. This premium seems to be derived from the stability of the industry and the reliance investors can have on the company and the reassurance that both revenues and earnings are going to continue.

{kind=link}

I am still not comfortable buying at these prices and will be instead rating it a hold. Part of the reason I have a hold comes from the dividend and the history of it. Raising it for the last 19 years speaks volumes and with a nearly 7% annual growth over it the last 5 years in total I think the future is still positive for investors and there is value to be extracted.

For further details see:

Middlesex Water Company - Continues To Be Too Expensive