PLOW - Miller Industries Still Has Room To Ride

Summary

- Compared to the market, Miller Industries has performed quite well in recent months, with sales and profits rising nicely in the latest quarter.

- This is a sign of strength during uncertain times and the near-term outlook for the company will likely continue to look this way.

- Shares are also cheap and should be considered appealing to value-oriented investors.

The towing and recovery equipment space may not strike investors as a particularly appealing market segment. However, like most parts of the economy, it continues to grow. And one company in this niche that has done quite well for itself as of late is Miller Industries ( MLR ). Even with the market plunging over the past several months, Miller Industries has done well to see its share price rise. This move higher has been backed by mixed but largely positive financial results, especially the results provided most recently. At this time, I wouldn't exactly call the company a home run prospect. However, given how shares are currently priced, I would say that some additional upside is likely warranted. As such, I have decided to retain the ‘buy’ rating I had on MLR stock previously.

Mixed but mostly positive so far

Back near the end of March of 2022, I wrote an article talking about my view that the risk-to-reward scenario regarding Miller Industries looked positive for investors. Up to that point, the company had been experiencing a bit of pain, largely as a result of the COVID-19 pandemic. The problems included, amongst other things, continued supply chain pressure and high inflation. Even after factoring in those issues, however, I felt as though shares looked no worse than fairly valued, with a recovery in performance leading to potential upside for investors. This led me to rate the company a ‘buy’, reflecting my belief at the time that shares should generate returns that would outperform the broader market for the foreseeable future. Since then, the market has come to agree with me. While the S&P 500 is down 8.3% since the publication of that article, Miller Industries has generated upside for investors of 7.4%.

{kind=link}

Author - SEC EDGAR Data

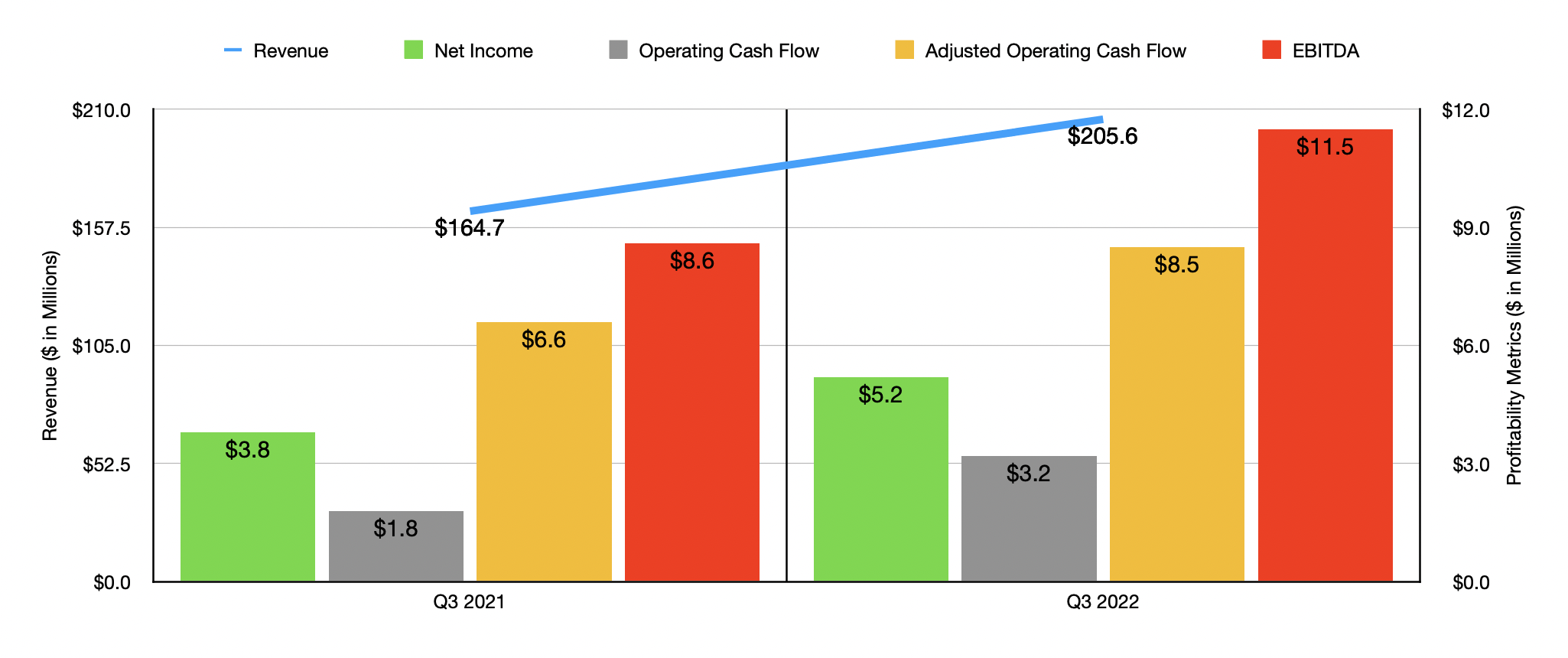

To really understand why Miller Industries continues to outperform the market, we should discuss the most recent financial data provided by management. This data covers the third quarter of the firm's 2022 fiscal year. During that time, revenue came in strong, totaling $205.6 million. That's 24.8% higher than the $164.7 million generated the same time one year earlier. According to management, this rise was largely the result of price increases and higher production volume, the latter of which was attributed to steady supply chain improvements. Growth was particularly strong in the domestic market, with revenue spiking 28% year over year.

On the bottom line, the picture also improved. Net income of $5.2 million dwarfed the $3.8 million reported one year earlier. In addition to benefiting from the increase in sales, the company also saw its gross profit margin rise from 10.8% to 11.3%. When applied to the revenue achieved in the third quarter alone, that margin improvement contributed a little over $1 million in additional pretax profit to the company. Other profitability metrics followed suit. Operating cash flow rose from $1.8 million to $3.2 million. If we adjust for changes in working capital, it still would have risen, climbing from $6.6 million to $8.5 million. Meanwhile, EBITDA for the company also increased, rising from $8.6 million to $11.5 million.

{kind=link}

Author - SEC EDGAR Data

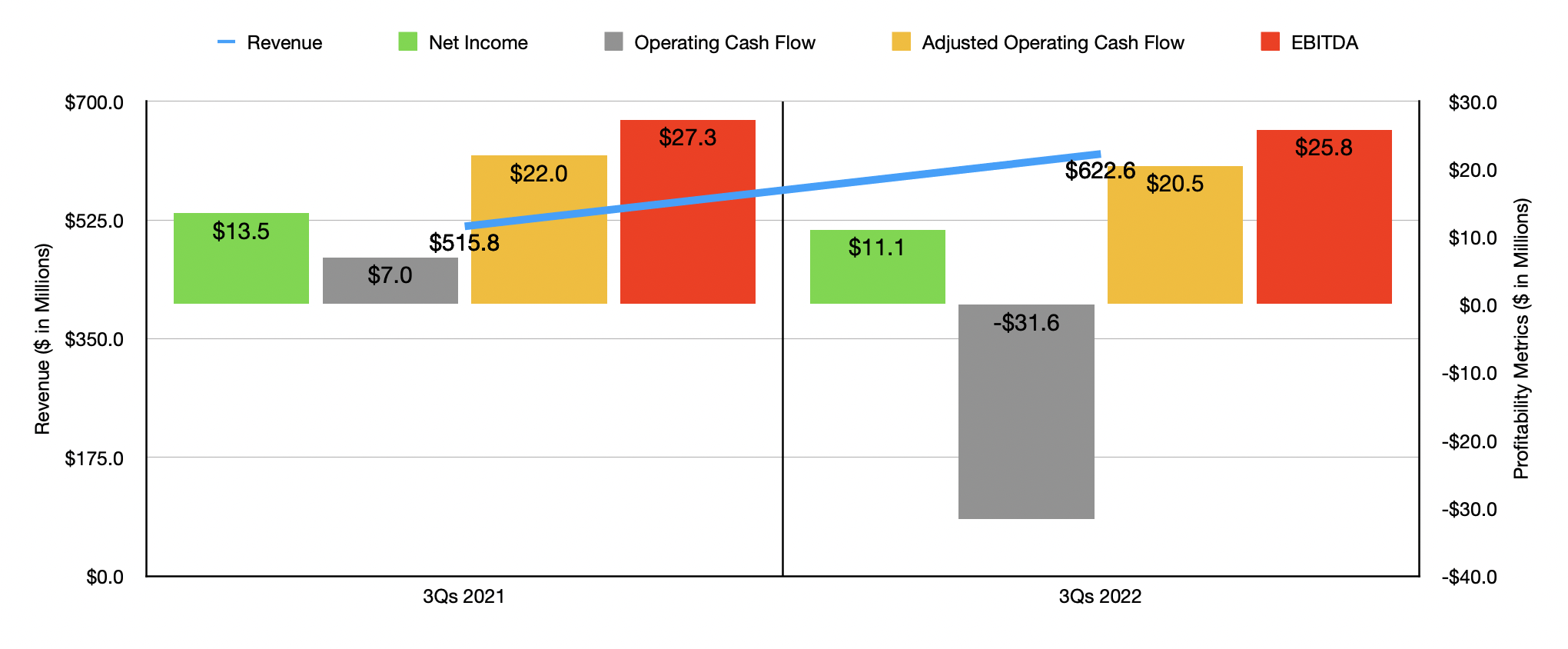

The third quarter was particularly noteworthy because of its strength across the board. When you look at the first nine months of 2022 relative to the same time one year earlier, you see that the data is more mixed than that. Yes, revenue still did increase, climbing 20.7% from $515.8 million to $622.6 million. But net income during this time was actually down, having fallen from $13.5 million to $11.1 million. The other bottom line performance during the 9-month window was also worse than it had been in the third quarter alone. Operating cash flow plunged from $7 million to negative $31.6 million. On an adjusted basis, the metric fell from $22 million to $20.5 million. And finally, EBITDA for the enterprise sank from $27.3 million to $25.8 million. What this demonstrates is that the company is strengthening as time goes on. The third quarter on its own was very impressive, while the results for the first nine months as a whole were undeniably mixed. This is a good sign in my opinion.

Management has not offered any guidance when it comes to the 2022 fiscal year in its entirety. But if we annualize results experienced so far, we would anticipate net income of $13.4 million, adjusted operating cash flow of $26.4 million, and EBITDA of $33 million. For full transparency, I think that this is more conservative than what we will ultimately see. As I mentioned already, the company is showing good signs of strengthening. By annualizing the results like I did, we are actually incorporating year-over-year declines as a whole. But as a value investor, I would prefer to err on the side of caution.

{kind=link}

Author - SEC EDGAR Data

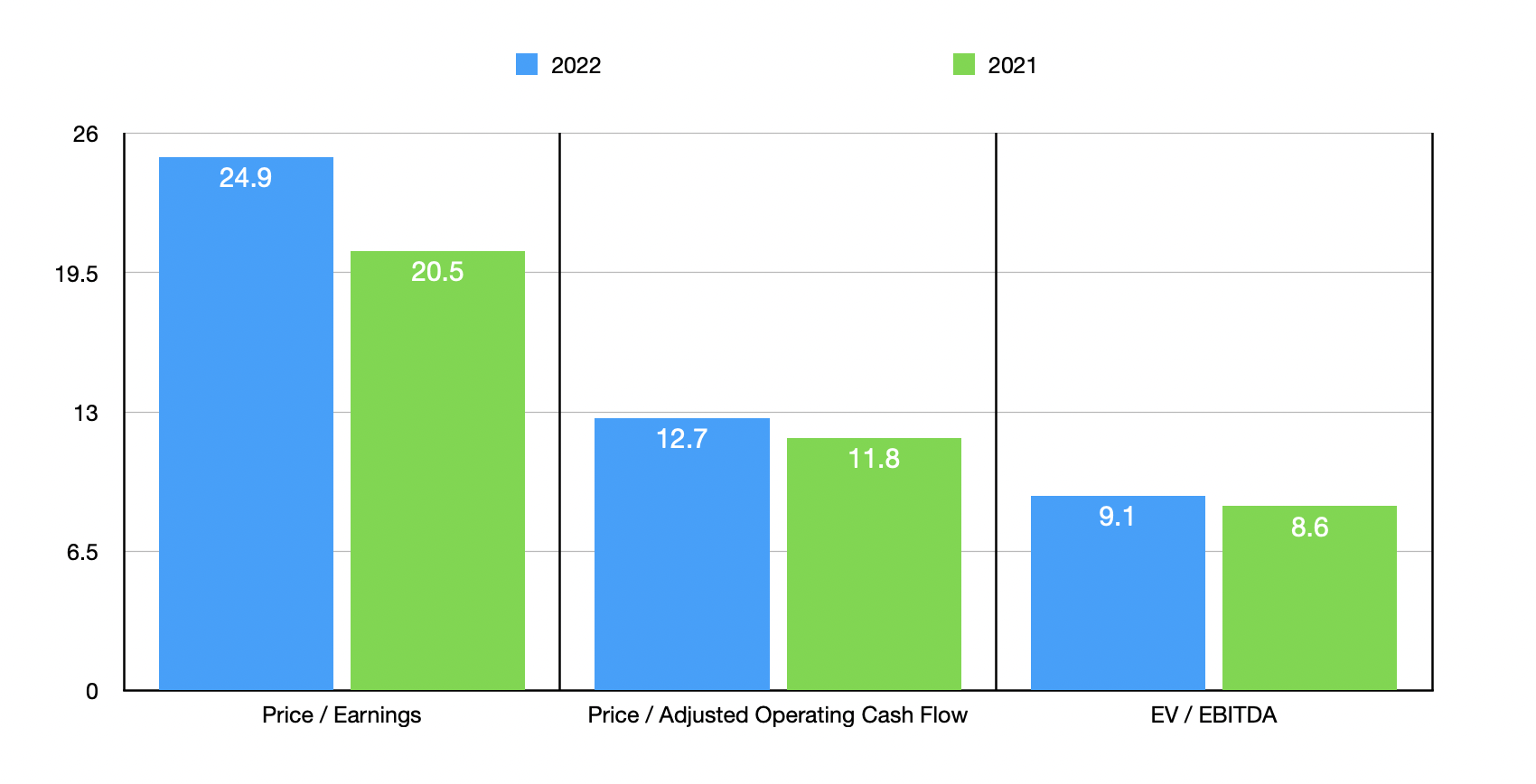

Taking these figures, I calculated that the company is trading at a price-to-earnings multiple of 24.9. On its own, this is rather lofty. However, the price to adjusted operating cash flow multiple should be lower at 12.7, while the EV to EBITDA multiple should come in at 9.1. As you can see by looking at the chart above, these results are higher than what we would get if we used data from 2021. As part of my analysis, I also compared the company to five similar businesses. On a price-to-earnings basis, these companies ranged from a low of 6.9 to a high of 76.1. In this case, two of the five firms were cheaper than our prospect. Using the price to operating cash flow approach, the range for the companies was from 11.2 to 171. And when it comes to the EV to EBITDA approach, the range was from 7.8 to 44.7. In both of these cases, only one of the five companies was cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Miller Industries |

| 24.9 |

| 12.7 |

| 9.1 |

| Westport Fuel Systems ( WPRT ) |

| 6.9 |

| N/A |

| 32.1 |

| Commercial Vehicle Group ( CVGI ) |

| 21.8 |

| 11.2 |

| 9.6 |

| Manitowoc ( MTW ) |

| 29.4 |

| 65.7 |

| 7.8 |

| Douglas Dynamics ( PLOW ) |

| 27.5 |

| 171.0 |

| 16.2 |

| Astec Industries ( ASTE ) |

| 76.1 |

| 132.6 |

| 44.7 |

Takeaway

Fundamentally speaking, Miller Industries is not exactly the best company on the planet. The volatility the company has experienced is less than desirable. On the other hand, we are seeing some improvements and it's also worth noting that the company has no debt and enjoys $33.2 million in cash and cash equivalents on its books. When you add on top of this the level at which shares are priced, both on an absolute basis and relative to similar firms, I believe that some additional upside could be warranted from here. As such, I've decided to rate the company a soft ‘buy’ at this time.

For further details see:

Miller Industries Still Has Room To Ride