MIN - MIN: Avoid This Return Of Principal Fund And Consider High Yielding Alternatives

2023-10-12 06:42:55 ET

Summary

- The MFS Intermediate Income Trust has struggled to earn sufficient returns to support its 8.5% distribution yield.

- The fund has been relying on liquidating assets to fund its distributions, resulting in a decline in its net asset value.

- Investors should consider alternative high-yielding investments that earn more than they pay in distributions, such as treasury bill funds or AAA CLO ETFs.

In January, I wrote a cautious article on the MFS Intermediate Income Trust (MIN), arguing that the fund's 8.5% distribution yield was at risk as the MIN fund only earned 1.9% p.a. over 10 years. Since my article, the MIN fund has continued to struggle, with its market price declining by about 4% (Figure 1).

Figure 1 - MIN has struggled since January (Seeking Alpha)

In this article, I will revisit my thesis on the MIN fund and explain why investors should avoid 'return of principal' funds like the MIN. I will also discuss some alternatives to the MIN fund.

Fund Overview

The MFS Intermediate Income Trust is a pretty simple closed-end fund ("CEF") to understand. Its strategy is to invest in investment grade ("IG") corporate bonds and treasuries to fund a monthly distribution yield that is equal to 8.5% of trailing NAV.

The MIN fund can invest in corporate bonds, securitized securities like commercial mortgage-backed securities ("CMBS"), U.S. government securities ("treasuries"), municipal securities, and foreign government securities with portfolio duration between 3 to 10 years.

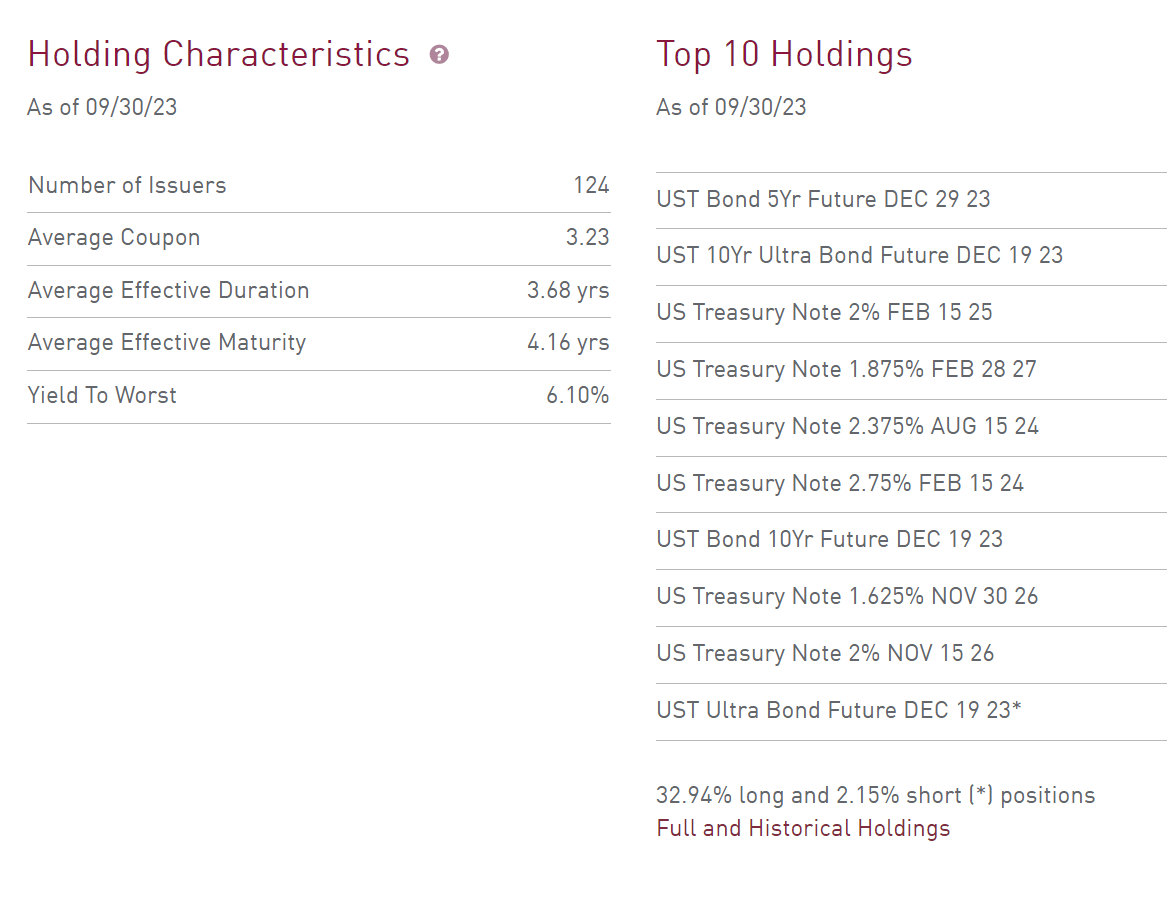

Currently, the MIN fund's portfolio holds 124 securities with average effective duration of 3.7 years and portfolio yield of 6.1% (Figure 2).

{kind=link}

In terms of portfolio allocations, the MIN fund currently has 51.3% exposure to IG corporate bonds, 41.8% exposure to treasuries, and 4.3% weight in municipal bonds (Figure 3).

{kind=link}

The MIN fund's portfolio is investment grade or better by design, with only 12% of the portfolio rated below BBB or unrated.

Modest Historical Returns...

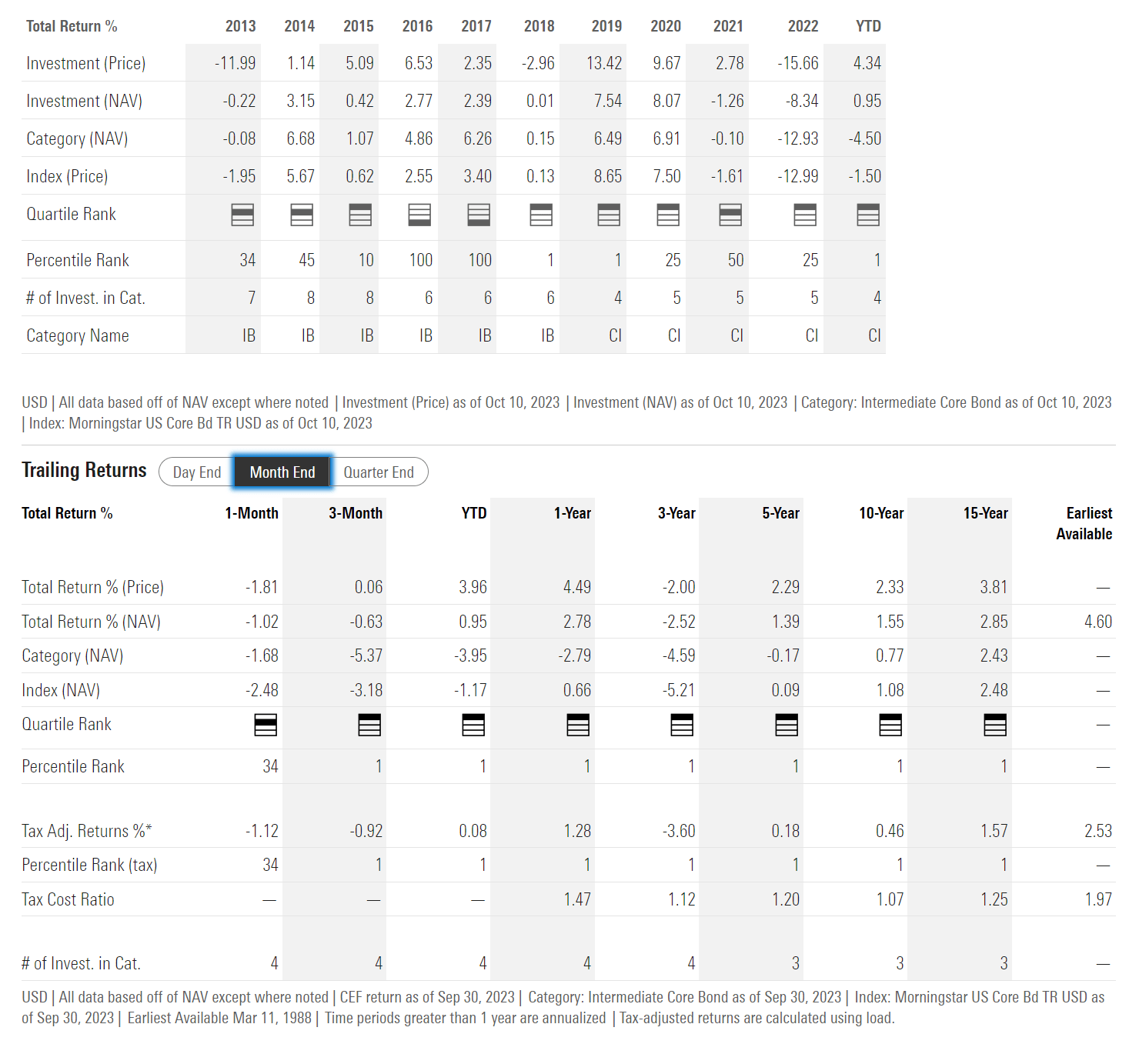

In terms of returns, the MIN fund has delivered very modest long term returns, with 3/5/10/15Yr average annual returns of -2.5%/1.4%/1.6%/2.9% respectively to September 30, 2023 (Figure 4).

{kind=link}

On an annual basis, the MIN fund's returns do not exhibit large volatility, ranging from -8.3% in 2022 to 8.1% in 2020. This is because the fund has fairly limited duration risk (3.7 year effective duration) and credit risk (IG corporate bond and treasuries-focused).

...Insufficient To Fund A High Distribution Yield

However, MIN's modest 1.6% average annual return over 10 years is insufficient to fund the target 8.5% of NAV distribution.

So year-after-year, the MIN fund ends up having to liquidate assets to fund its distribution. this shows up as 'return of capital' in the fund's annual reports (Figure 5).

Figure 5 - MIN has used ROC to fund distribution (MIN annual report)

{kind=link}

Investors Should Avoid Amortizing NAV Funds

Funds that do not earn their distributions are called 'return of principal' funds, as explained in an Eaton Vance whitepaper . 'Return of principal' funds are characterized by amortizing NAVs and shrinking distributions over time.

The MIN fund shows both characteristics, with its NAV in a perpetual decline (Figure 6), while its annual distribution rate has shrunk from a peak of $0.66 / share in 1993 to $0.25 / share in the trailing 12 months.

Figure 6 - MIN has a perpetually shrinking NAV (morningstar.com)

{kind=link}

Real Life Analogy With Return Of Principal Funds

While accounting concepts like 'return of capital' may be hard to grasp for those not steeped in financial markets, there is a simple real life analogy that I believe is very apt for describing amortizing funds like the MIN.

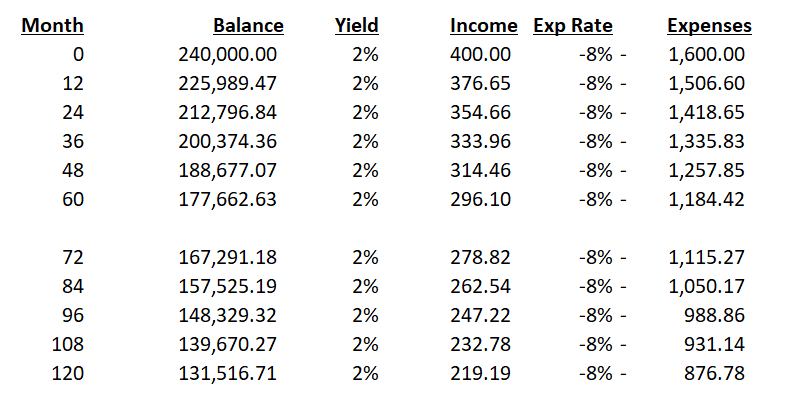

Imagine Jane Doe is a retiree living off a 2% savings rate on a $240,000 savings account balance, which translates into $400 a month in retirement income (i.e. MIN earns 10Yr average annual returns of 1.9%). Unfortunately, she has high monthly expenses of $1,600 / month or 8% of her retirement savings (MIN pays a target 8.5% yield).

In the short-run, Jane Doe's monthly overspending is not a big issue, as her large savings account balance ($240,000) is more than sufficient to cover the monthly shortfall ($1,200).

However, measured over long periods of time, her savings will be quickly depleted as she outspends her earnings significantly every month. After 5 years, her savings account balance will have shrunk by 26% to $178k and her monthly income will only be $300 (Figure 7). After 10 years, she would be left with only $132k in savings and $220 / month in income.

Figure 7 - Illustrative return of principal concept (Author created)

{kind=link}

Alternatives For Income Investors

Instead of amortizing 'return of principal' funds, I recommend investors consider other high yielding investments that earns more than they pay in distributions. For example, for ultra-conservative investors, they can look at treasury bill funds like the iShares 0-3 Month Treasury Bond ETF (SGOV) that invest in short-term treasury bills currently paying a 4.9% forward yield. I last wrote about the SGOV ETF here .

For investors who can bear more risk, they can consider the Janus Henderson AAA CLO ETF (JAAA) that invest in the highest quality tranches of CLO securities. The JAAA ETF is currently paying a trailing 5.7% distribution yield. I last wrote about the JAAA ETF here .

For those willing to take equity-level risks, they can consider the Simplify Volatility Premium ETF (SVOL) that short VIX futures to harvest the VIX term structure. The SVOL ETF pays a trailing 17.0% yield. I last wrote about the SVOL ETF here .

My point is that there are lots of high yielding alternatives for investors to choose from, so they should not have to invest in amortizing 'return of principal' funds where they are simply paid back their capital through the distribution.

Conclusion

The MIN fund aims to provide an attractive 8.5% of NAV distribution yield from a portfolio of investment grade bonds and treasuries. Unfortunately, the MIN fund has historically not earned its distribution. Instead, the fund has been funding distributions with return of investors' own capital. Over time, investors lose out in both principal and income.

Instead of the MIN, there are a plethora of non-amortizing high yielding funds investors can choose from that provides attractive yields with varying levels of risk. I rate the MIN a sell.

For further details see:

MIN: Avoid This Return Of Principal Fund And Consider High Yielding Alternatives