MIN - MIN: You Have To Understand What You Buy

2024-01-12 00:02:55 ET

Summary

- MFS Intermediate Income Fund attracts retail investors with its high, unsupported dividend yield of 9%.

- MIN utilizes artificial yields by distributing more than its actual cash flows, leading to a decreasing net asset value.

- Despite the artificial yield, MIN's total return is competitive compared to similar ETFs.

- Despite its overdistribution features, the fund is correctly set up for the current monetary cycle, with an expected 7% total return in the next 12 months.

Thesis

As a retail investor, you always need to understand what you are buying. If you do not understand what an instrument does, or what its risk factors are, then you are better off by not putting your capital into that particular security. Not understanding what you are buying is tantamount to gambling. You just bet that the odds will be in your favor.

One 'trick' used by many CEF managers is the utilization of high, unsupported dividend yields. The idea is that a retail individual will be attracted by that particular fund via the high dividend yield, and they would be telling themselves that they will get their money back via the dividend no matter what. The MFS Intermediate Income Fund ( MIN ) is one of those investments. While not intrinsically bad (the fund has generated decent long-term total returns), the vehicle lures in buyers via its eye-popping 9% dividend yield.

We covered this name more than a year ago, in the context of rising rates and our view on the impact to the fund. MIN is a fixed-income CEF that invests mainly in treasuries and investment-grade bonds, thus rates represent its largest risk factor. With rates on a path lower, we are going to revisit this CEF given our view of ongoing long fixed income at this stage of the monetary cycle.

How does a manager create artificial yields

A CEF is an actual company. The company engages in buying securities and then chooses to make distributions. Via this structure, the company can in fact set whatever yield it deems necessary. It is not bound by any specific range. While investors wrongly assume CEFs are pass-through vehicles, they are not.

The unique CEF structure that entails an actual company, versus the continuous creation of shares for ETFs is what makes the asset class different. While some portfolio managers choose to distribute what they make via CEFs, many take a targeted distribution approach, mainly for marketing purposes. Retail investors love to see high yields because they falsely give the sentiment of wealth creation. An instrument's earnings power does not reside solely in its yield but should be quantified from a total return perspective.

MIN falls in the marketing category, where the manager has taken a portfolio of treasuries and investment-grade bonds and slapped a junk bond yield on top of the structure. As a retail investor, you should understand that treasuries and high-grade bonds cannot pay you 9% when Fed Funds are at 5.25%.

The direct result of the artificial distribution of a higher yield is an ever-decreasing NAV:

From a mechanics standpoint, it simply represents the utilization of 'principal' to pay interest. Let us assume a very simple example - let us say you invest $100 with us for 10 years, and we put it in 5% yielding 10-year treasuries. So every year we are going to receive an actual cash flow of $5. Yet we choose to distribute $9. Where does the $4 come from? Well from the original $100. So after the first year, we will need to sell some treasuries to pay the $4 shortfall, hence our 'principal' will only be $96. Thus in the second year, we are going to earn less than $5 in actual cash since our cash-generating pool is down to $96. This mathematics game will continue for 10 years, at the end of which you will receive back a much lower amount than your original $100.

Fundamentally MIN is correctly set up for the macrocycle

While its dividend yield is artificial, and the fund's cash-flow yield is somewhere closer to 5%, the fund's portfolio is not poorly set up for today's cycle:

{kind=link}

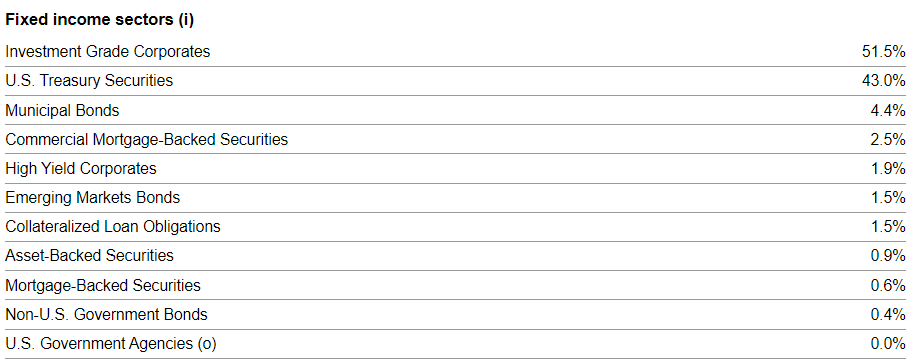

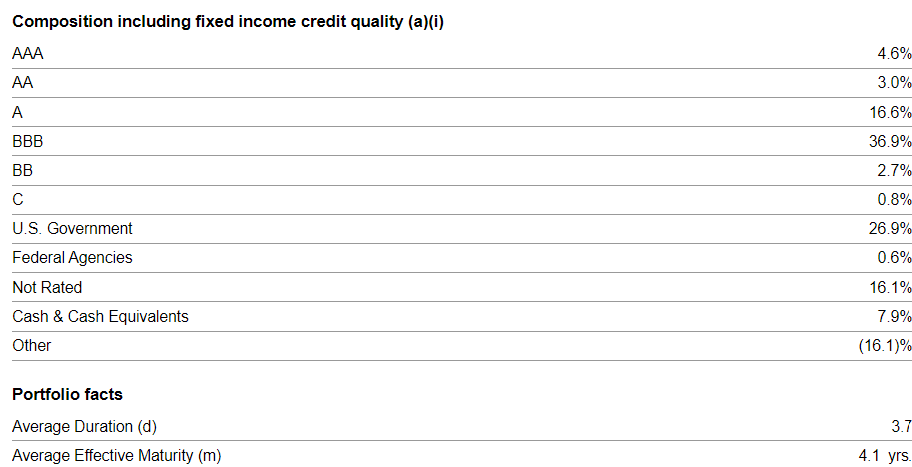

The CEF invests in investment-grade bonds and US Treasuries mainly and does not currently have leverage. This setup translates into a fund that has rates as its main risk factor, followed by investment grade spreads. The CEF's rating breakdown is as follows:

{kind=link}

Outside of Treasuries, the CEF is long single-A and BBB securities, which make up most of the corporate portfolio.

The fund's duration is close to 4 years, meaning that point in the curve will be the main driver of rates-driven price moves.

We have just experienced a very violent monetary tightening cycle, that has seen Fed Funds increase by roughly 5% in a 2-year span. With the Fed done with rate increases, the market has been fervent around discussing rate cuts into the new year, with estimations varying from bank to bank. However, all analysts are in agreement 2024 will see a number of rate cuts, the only question is how many. This macro set-up is favorable to fixed income, especially Treasuries and IG bonds, which have a low sensitivity to credit spreads.

What should you expect from MIN in terms of performance

CEFs with artificial yields are best analyzed from a total return perspective because only factoring in NAV and dividends paints an accurate picture:

You might be surprised to find out that from a total return perspective, MIN actually delivers when compared to the iShares Intermediate Government / Credit Bond ETF ( GVI ) and the iShares 3-7 Year Treasury Bond ETF ( IEI ). We are comparing MIN to GVI because both benchmark themselves on the same index, namely the Bloomberg U.S. Intermediate Government/Credit Bond Index:

{kind=link}

So while MIN has an artificial yield, its total return is actually competitive. Investors just end up with higher yearly yields and a capital loss when they actually sell the name (decreasing NAV feature). If one ignores the tax implications which vary from person to person, then the total return picture is not a poor one.

Going forward we are contemplating a 4-year duration portfolio with a treasuries / IG bonds mix that yields roughly 5% on a cash-flow basis. Given the assumption for lower rates by 50bps, on a 12-month basis, we should expect a +7% total return here, coming from the 5% cash-flow yield and 2% from the duration implications of lower rates. So the expected total return is positive, although from a price perspective, the CEF will lose value because it is paying 9% when it is projecting to make just 7%.

Discount to NAV

Given its propensity to overdistribute, this CEF has been trading at a discount to NAV:

However, the discount has been fairly stable in the past 5 years, fluctuating around the -4% mark. We do not expect to see substantial changes here.

Conclusion

MIN is a fixed-income CEF. The fund invests in treasuries and investment-grade bonds, without any leverage currently. What sets this name apart is its unsupported junk bond CEF dividend of 9%. A retail investor needs to understand that the cash flows generated by a portfolio of treasuries and IG bonds will not amount to 9% when Fed Funds are at 5.25%.

The overdistribution feature is a big detractor for us for the name, but it serves its marketing purpose. From a fundamental perspective, however, the fund performs. On a 5-year basis, its total return is superior to simple ETFs such as GVI or IEI. Moreover, its portfolio is correctly set up for a lower rates environment, with the fund's 4-year duration and low exposure to credit spreads providing a back-wind.

If you are already in this CEF you should hold, since we predict a 7% total return in the next year, but new money should stay away from MIN. We fundamentally do not like CEFs with such high overdistribution percentages, and there are also individual tax implication perspectives. Retail investors looking for treasuries and IG bond exposures should look at funds in the space we have covered with buy ratings, such as SHY or WEA, which act more like path-through vehicles.

For further details see:

MIN: You Have To Understand What You Buy