MIR - Mirion Technologies: Wait When The Targets Are Met

2023-08-28 04:26:35 ET

Summary

- Mirion Technologies is a radiation detection and monitoring company with a market cap of $1.6 billion.

- Both the Medical and Industrial segments of the company outperformed market expectations in terms of revenue. But the bottom line is still negative.

- Mirion is expected to launch the third generation of Instadose technology in FY2024, which should contribute to its growth.

- The expectations implied by the market today don't give a sufficient upside potential for MIR stock any time soon.

- I'd avoid buying this stock until the deleveraging and EPS targets are really met. MIR gets a Hold/Neutral rating from me today.

The Company

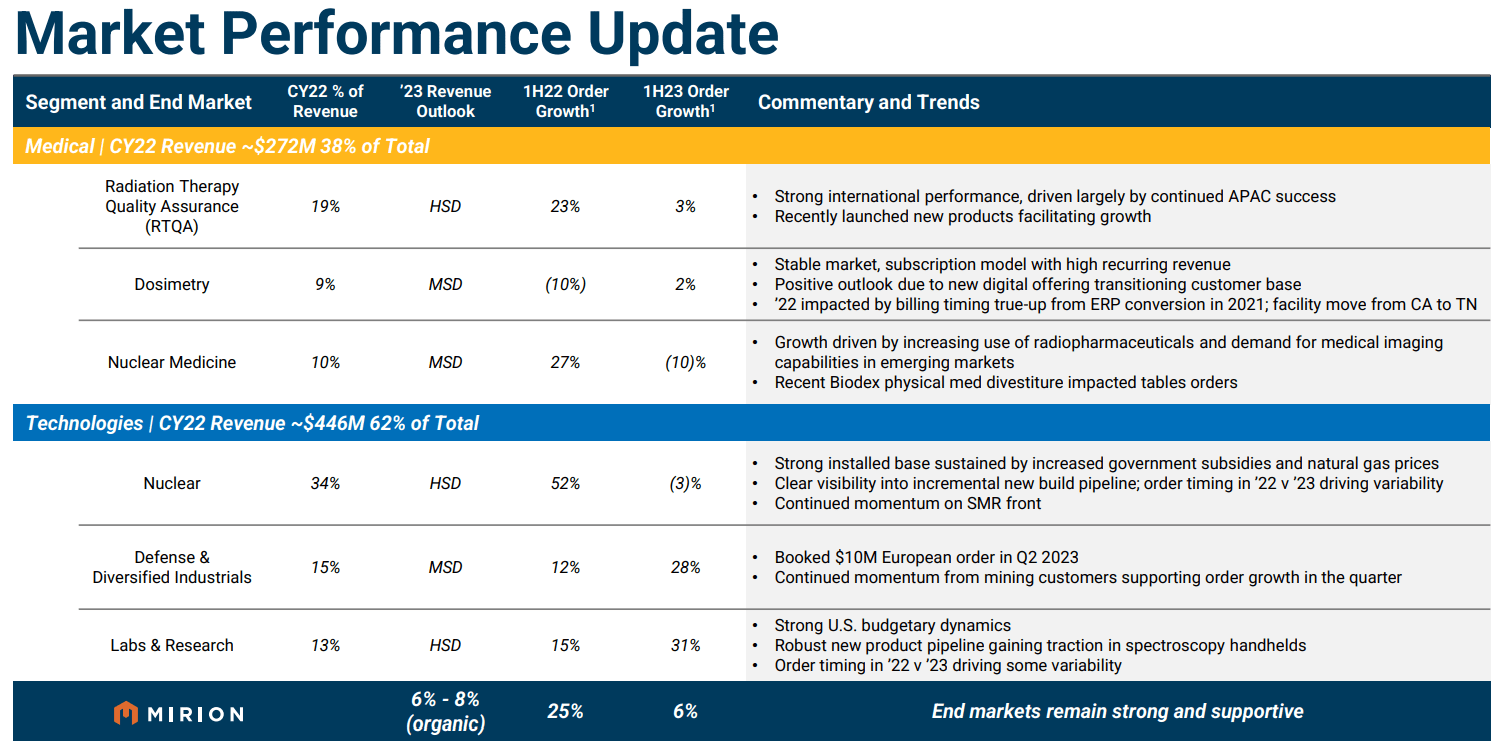

Mirion Technologies ( MIR ) is a $1.6-billion market cap Atlanta-based firm that provides radiation detection and monitoring products in the Medical and Industrial sectors. The Medical segment [34.5% of total sales] offers solutions for radiation therapy quality assurance, patient safety, and nuclear medicine applications. The Industrial part [65.5% of total sales] focuses on radiation safety equipment and analysis tools. The company serves medical, industrial, and governmental clients worldwide.

In Q2 both segments outperformed market expectations in terms of revenue, and this trend is expected to drive momentum into the year's second half of FY2023. Margins were in line with expectations as the company navigated supply chain disruptions, the executives noted during the latest earnings call .

The CEO highlighted strong order growth, particularly in labs, research, defense, and diversified industrials. In the Medical segment, radiation therapy quality assurance saw robust growth, while dosimetry and nuclear medicine segments remained stable. The Technologies segment showed strong performance in nuclear power, labs, and defense markets.

MIR's IR materials

{kind=link}

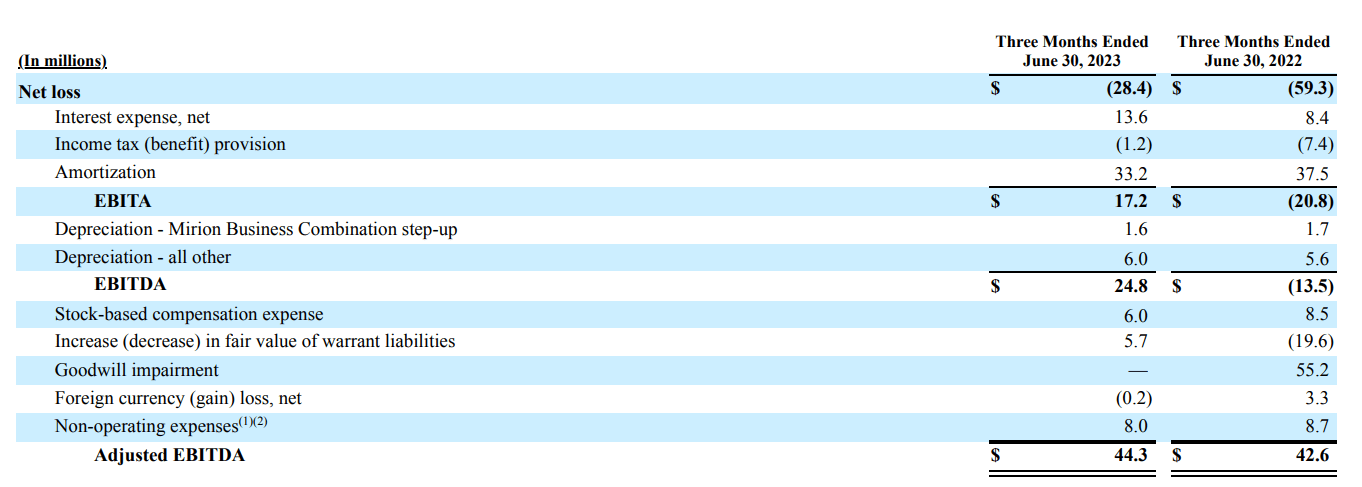

Q2 saw around 9% adjusted order growth compared to the previous year, leading to an expanded backlog for the 4th consecutive quarter. Total company revenue grew by 12.2% in the quarter, with organic growth of 8.4%. Adjusted EBITDA was $44.3 million, with a margin of 22.5%. But the adjusted EBITDA figure flows from a net loss, just like the last few quarters:

{kind=link}

{kind=link}

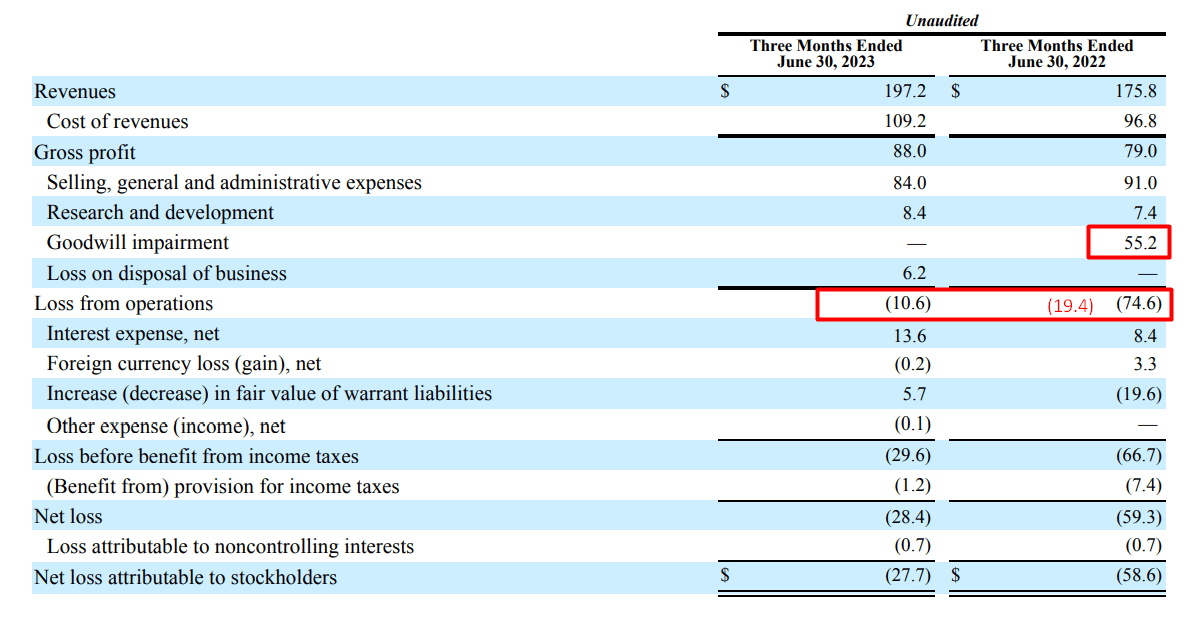

What does look positive, however, is the development of EBIT: if we deduct last year's goodwill impairment from the calculation of the operating result, we get an almost 2-fold decrease in operating costs compared with Q2 FY2022:

{kind=link}

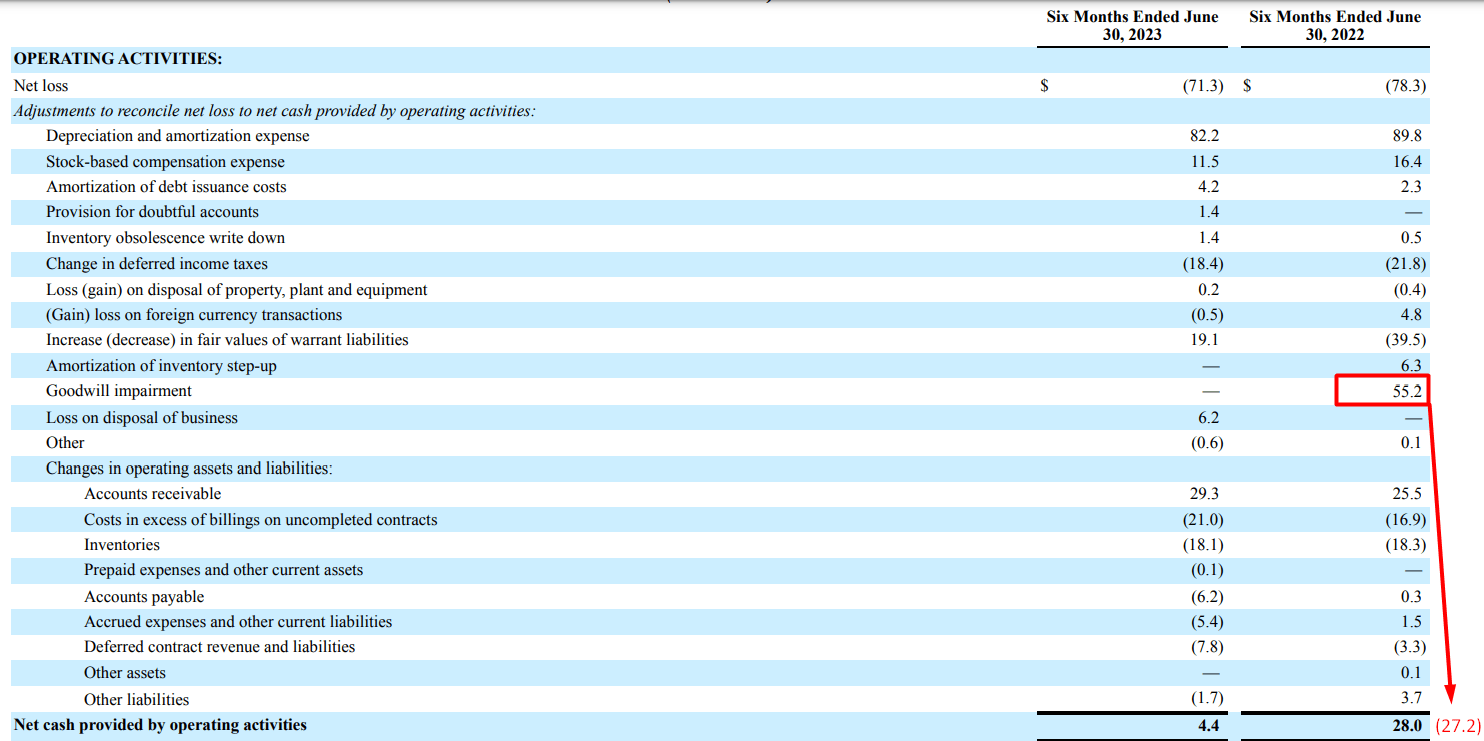

If we continue to adjust for the goodwill impairment, we'll see a significant improvement in operating cash flow generation. Yes, $4 million for a company with a market cap of $1.6 billion doesn't look very impressive, but compared to last year's adjusted results, it's at least something:

{kind=link}

The management explained during the call that supply chain disruptions had prompted them to build strategic inventory buffers, and now they are focusing on improving inventory turnover through better demand planning, production scheduling, and distribution planning (that's probably why the cash flow is still weak). They expect these efforts to yield positive results in the latter part of the year.

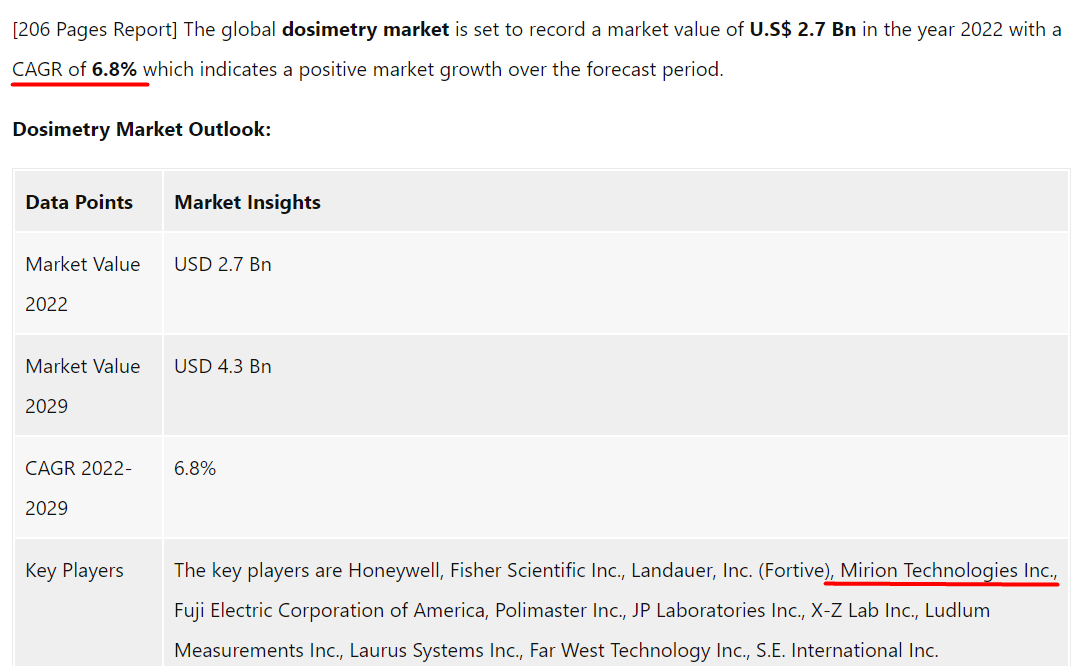

MIR is going to launch the third generation of Instadose technology somewhere in FY2024 [not mentioned when exactly], so this will likely contribute positively to the business's growth. And the overall dosimetry market's long-term CAGR of 6.8% should help MIR here:

{kind=link}

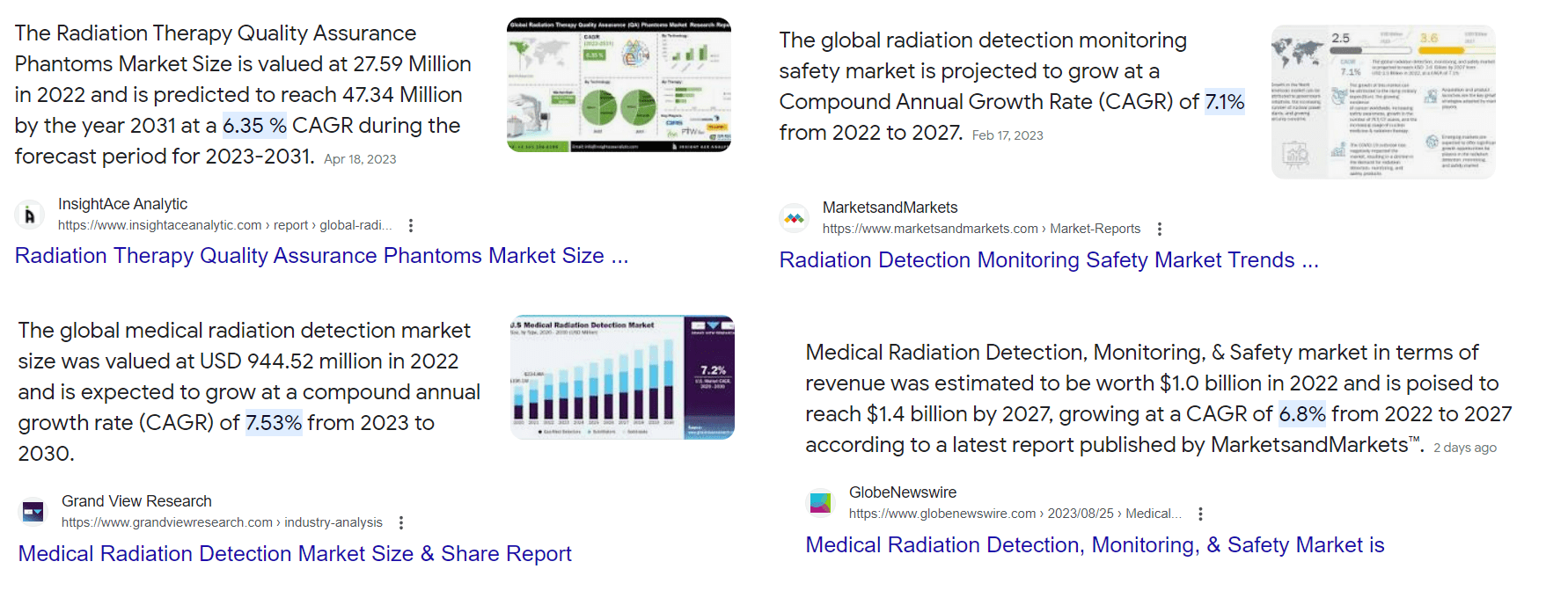

My quick research has confirmed that all major MIR's addressable markets are set to grow by 6-8% annually over the next few years, so with the introduction of new technological solutions, MIR has every chance of finally making a book profit again in the foreseeable future.

{kind=link}

I am puzzled by the growing net debt on the balance sheet - in the last reporting period, it increased by almost 21% year-on-year, while net debt to EBITDA [adjusted for M&A] increased from 3.6x to 4.3x. The management said they are committed to reducing leverage to or below 3.1x by the end of the year - time will tell.

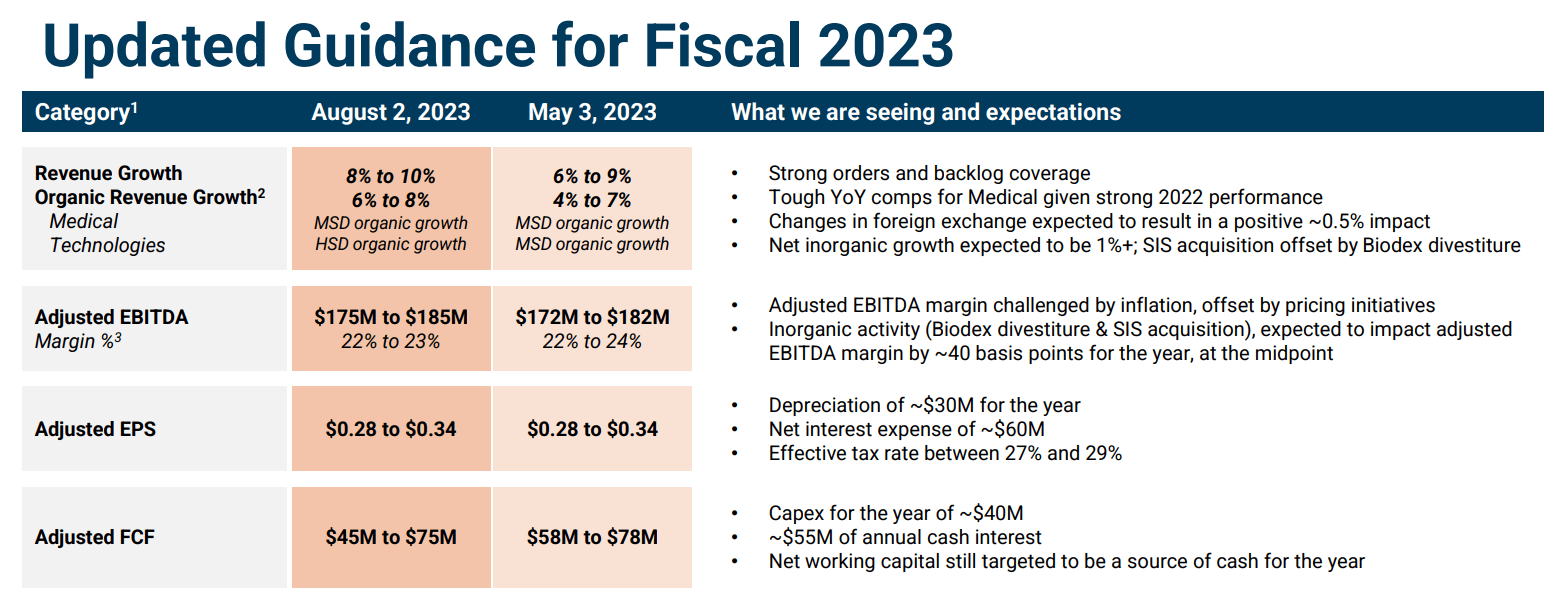

They also updated their 2023 financial guidance with higher and more focused revenue growth expectations and adjusted EBITDA and FCF targets:

{kind=link}

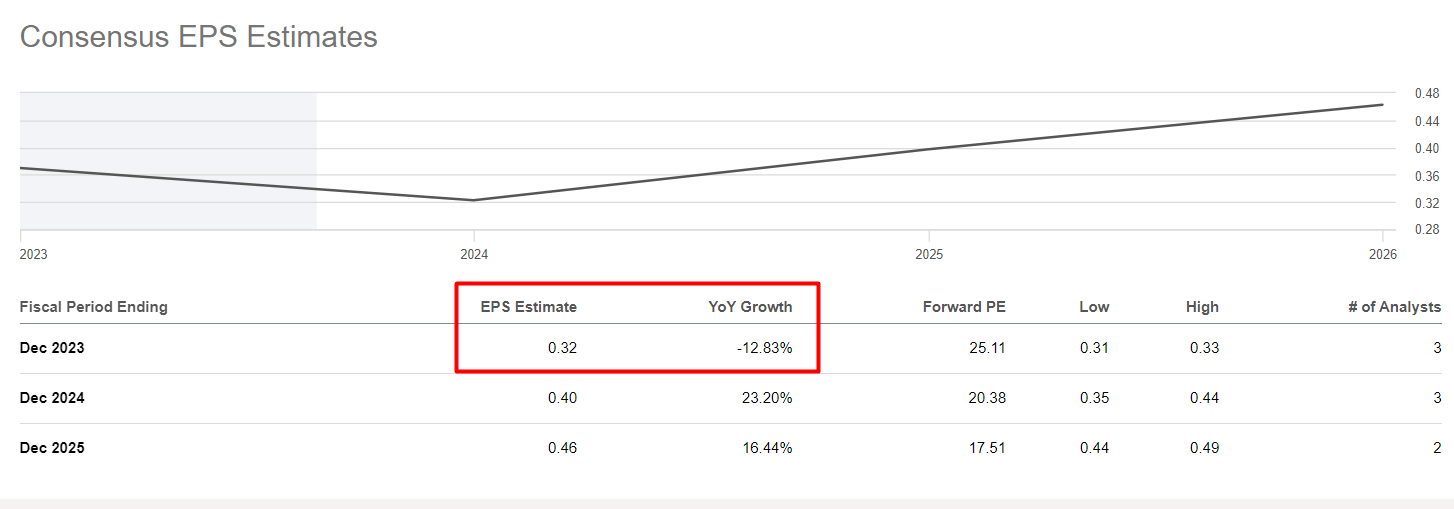

The market agrees with these projections: Fiscal 2023 revenue growth is projected at 9.1% [slightly higher than the guided mid-range above], and the consensus EPS of $0.32 is 1 cent higher than management's guided figure.

{kind=link}

The Valuation

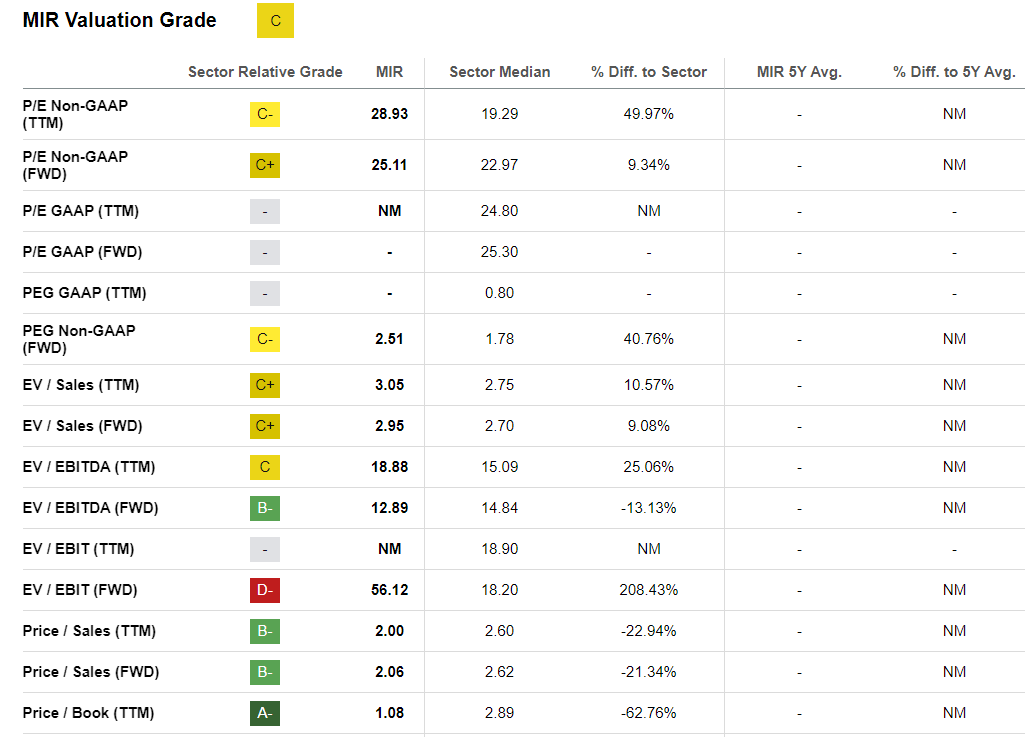

Seeking Alpha Quant System gives MIR a "C" in terms of its valuation levels: revenue-based multiples are about 10-20% lower than the medians of the IT sector, but profitability leaves questions as price-earnings and EBITDA-related metrics are weaker.

{kind=link}

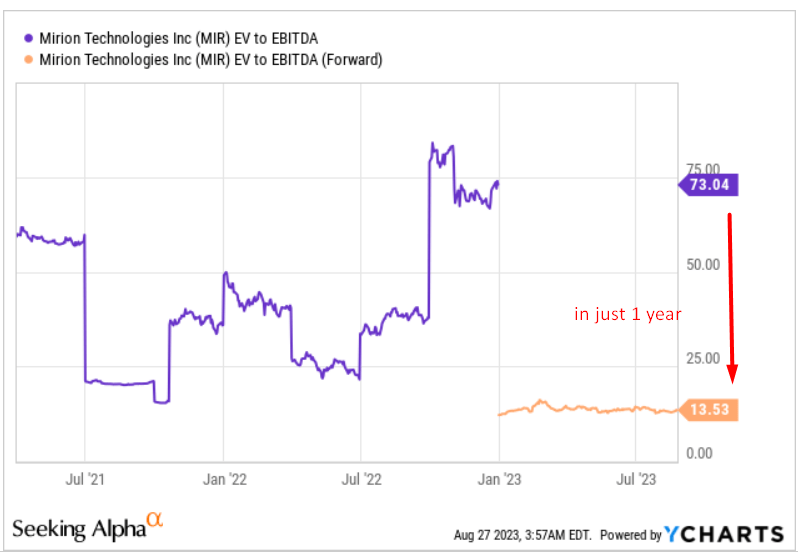

However, if we assume that management's guidance comes to pass, and a small premium to those forecasts from Wall Street analysts also turns out to be close to the truth (this has been possible in the past, looking at earnings surprises ), then MIR's EV/EBITDA ratio for just 1 fiscal year should drop from 73x to just 13.5x. That's a multiple contraction of ~81%, YoY:

{kind=link}

In this case, the company will be 9% undervalued [to its sector], and considering that EBITDA is projected to increase by 8.9% year-on-year in FY2025 [YCharts data], MIR stock may finally have a reason to leave its long-term consolidation base to the upside:

{kind=link}

But frankly, with EBITDA growth of less than 10% YoY [in 2 years], the upside potential seems limited to me.

The Verdict

Although the company is clearly operating in very important and undeniably well-growing addressable markets, and the EPS numbers projected for the next few years will make many competitors green with envy, I am not ready to rate the stock a "Buy" this time around.

That's because, in addition to the positive moments, there are worrying signs. For example, MIR has not been able to generate a profit for many quarters despite all its efforts. And its debt continues to rise. Management assures us that these are temporary difficulties, but I would rather wait for real results before buying this stock. Besides, the fundamental upside doesn't look very impressive - MIR will really have to surprise the market to offer value investors a chance for a good return.

Therefore, I rate MIR a "hold."

Thanks for reading!

For further details see:

Mirion Technologies: Wait When The Targets Are Met