MCW - Mister Car Wash: Limited Near Term Visibility

2023-11-05 01:42:15 ET

Summary

- MCW is a leading car wash company with 450+ locations with over 2.1 mn UWC loyalty members.

- The company has been able to leverage its brand positioning within its UWC members to stave off the current weakening macro.

- It expects to focus on converting users to its recently launched Titanium plan but expects slowing growth in UWC member adds which had been key growth driver historically.

Investment Thesis

We ascribe a Neutral rating on Mister Car Wash ( MCW ) primarily as a result of weakening consumer environment along with the company's expectation of slower growth in its UWC membership additions. We believe MCW is positioned well driven by its strong brand image amongst is consumers to stave off the current challenging backdrop along with a well-timed planned rollout of its premium 'Titanium 360' program. However, we believe the near term outlook appears choppy and the current valuation provides limited margin of safety. Initiate at Neutral.

Company Background

Mister Car Wash is the largest car wash brand in the US with a total of over 450 locations across 20+ states in the country. It offers express exterior and interior cleaning services to a wide range of customers including individual retail as well as through its membership program 'Unlimited Wash Club' ( UWC ). It boasts a total of 2.1 mn UWC members with base subscribers paying a subscription fee of $20 per month while premium platinum exterior subscribers paying a subscription fee of $30 per month with the premium service offering a complete car washing experience including tire shine and underbody wash. Over 50% of its UWC members are in its platinum exterior subscription plan which spends an average 1.7x the average ticket price on a platinum wash. It recently launched its Titanium 360 subscription service at $40/month offering additional premium services and expects to complete rollout by Q1 2024.

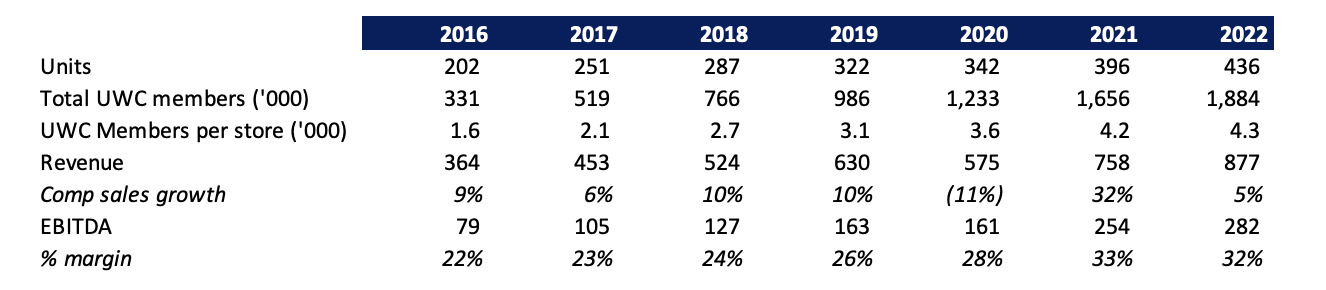

Strong Financial Track Record

The company had a strong track record of growth driven by its continued expansion with total units doubling over the 6 year period. Revenues grew at a record 16% CAGR over 2016-2022 period primarily driven by strong growth in its UWC membership which forms more than 65% of the car wash sales. Comp sales growth remained in high single digits to low double digits on an average except for 2020 where in its operations were thwarted by almost complete stoppage of travel. EBITDA margins expanded handsomely by over 10 percentage points primarily driven by the strong uptake of its UWC member plan which has higher gross margins along with SG&A leverage due to operational efficiencies. However, EBITDA margins in 2022 declined slightly primarily due to input cost inflation on chemicals as well as wage hike inflation.

{kind=link}

Company filings

In line Q3 Results

The company reported an in-line quarter amidst an otherwise challenging macro scenario with revenues up 8% YoY to $234 mn on the back of a 1.7% growth in comp store sales growth and rest of the growth coming from the additional 42 locations compared to the year ago period. Its retail business was still down MSD to HSD, however was sequentially better where in Q1 it was down double digits and in Q2 it was down HSD. The 1.7% comp growth was sequentially better with Q2 comp growth of just 0.5% and has been stellar compared to Driven Brands ( DRVN ). In contrast, DRVN Car wash segment reported a 4% decline in comp store sales growth in both Q2 and Q3 2023 . This demonstrates the strength of its UWC subscription plan which has been its key growth driver. Companies have been pausing investments and relooking on the overall car wash business which has enabled MCW to grab market share driven by its outperformance of UCW subscription.

Given continued weak consumer demand and increasing competition in the US Car Wash sector, we are strategically pausing capital investment in this business.

- Jonathan Fitzpatrick, President and CEO, Driven Brand Holdings ( Source )

The company added 6k net new additional UWC subscribers, up 11% YoY, ending with total UWC members of 2.1 mn. UWC sales represented ~72% of total car wash sales (up sequentially as well as on YoY basis) demonstrating the loyalty and perceived benefits by the subscribing user. Gross margins contracted by 60 bps primarily due to higher store operating expenses as a result of an increase in rent payments as a result of additional locations along with completion of sale and leaseback for certain units partially offset by normalization of commodity costs which leveraged by 20 bps. SG&A expenses $ inched up marginally while G&A leveraged by 20 bps as a result of strict cost control. This eventually lead to Adj. EBITDA margin improved by 20 bps YoY to 30.6%, in line with the estimates. Interest expenses doubled primarily as a result of higher average interest rates in the current period. In all, the company reported a non-GAAP EPS of $0.08, marginally ahead of the estimates.

Balance sheet position remained stretched with the company ending with cash balance of $65 mn compared to $62 mn at the beginning of the year. Total debt remained at $897 mn compared to $895 mn at the end of last year. Net Debt / TTM EBITDA remained at 4.1x primarily as a result of weakness in operational performance.

The company reiterated its comp growth outlook to a range of -1% to 1% including an ~40 bps favorable impact to FY23 comp from the rollout of Titanium 360. Excluding this benefit, the lower FY23 comp outlook implies 2H'23 trends would be flat to modestly negative. On profitability front, it expects Adj. EBITDA range of $270 - $283 mn in line with its previous guidance. This flows through to an updated EPS outlook of $0.28 - $0.32 (vs. $0.30 - $0.35) driven by the company's additional rent expenses, higher utility expenses and testing of its new marketing strategies. In all, we expect a ~24% decline in EPS in 2023 to $0.30 at mid point and expect the EPS will rebound to 2022 levels in 2024.

Valuation

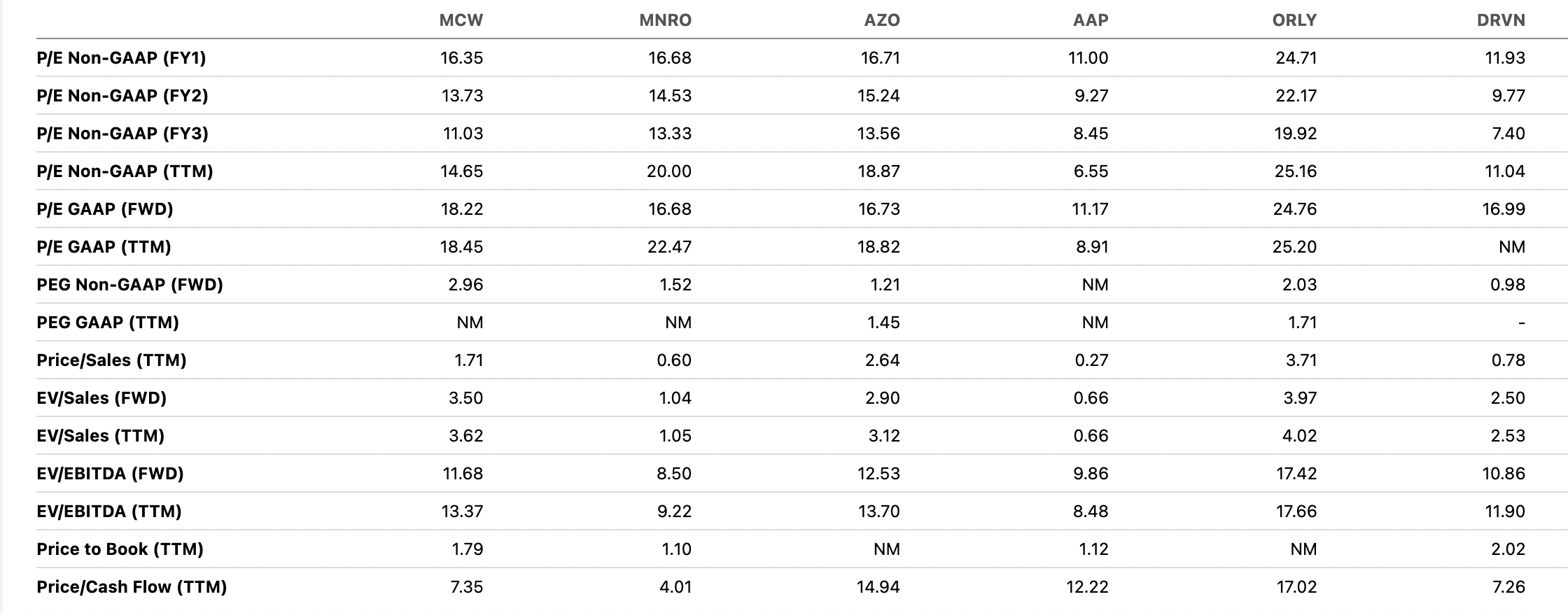

We compare MCW with other listed consumer oriented aftermarket automotive companies. Despite the recent decline, the stock currently trades at 13.7x P/ FY24 EPS which is at a discount to its long term average and compared to its peer average of 14.2x. We believe the current discount is warranted given the weakening consumer backdrop and earnings momentum with massive debt load. We believe its planned rollout of Titanium 360 which has been launched in 317 locations enables them to materially offset the weakness in retail business currently. In addition, the company noted that upselling its existing UWC members to Titanium may come at the expense of slower net UWC membership additions in the near term which can put a dampener on the growth. We initiate with a Neutral outlook amidst softening consumer environment, cautious outlook and limited margin of safety from valuations perspective.

{kind=link}

Seeking Alpha

Risks to Rating

Risks to rating include

1) Macro pressures and inflationary headwinds can lead to an increase in DIY car wash sales which will adversely impact its operations

2) MCW operates in a highly fragmented and competitive market including several local, regional and national chains which can limit its ability to provide services catering to specific targeted users at competitive rates

3) The company has high debt load and any further rate hikes can lead to significant jump in its interest expenses, as witnessed during the current year

4) Upside risks include stronger addition to its UWC business, better than anticipated uptake of its Titanium 360 program and any shareholder activity such as dividends or share repurchases

Final Thoughts

MCW has been facing with weakening consumer environment but its UWC membership plan have been able to stave off a substantial decline. We believe the company's strong brand resonance amongst its customers positions them well to tide off during this period of uncertainty, however, much of the growth historically has come from UWC member additions and development of new units. While new unit adds guidance have largely been unchanged, current environment means that the UWC member additions is likely to slow which can dampen recovery. In addition, we believe the company will likely be able to have Titanium as 10% of its subscription revenue and add in an extra 1$ to the subscription revenue. However, this will likely be prolonged and may not accrue immediate benefits. Initiate at Neutral.

For further details see:

Mister Car Wash: Limited Near Term Visibility