MCW - Mister Car Wash: Massive Margins And More Hiring Imply Undervaluation

2023-06-28 07:46:45 ET

Summary

- Mister Car Wash's scalable business model and high EBITDA margin make it an attractive investment opportunity, despite risks from inflation, limited suppliers, and potential loss of key employees.

- The company's growth in net revenue, adjusted EBITDA, and unit count, along with its focus on hiring and training quality employees, could lead to increased efficiency and free cash flow growth.

- MCW stock price could trade at a higher level if Mister Car Wash continues to expand its network, acquire competitors, and maintain its strong financial performance.

Mister Car Wash, Inc. ( MCW ) shows a scalable business model and fat margins. It also appears to be coping well with the growing inflation. If the company continues to hire, as promised, and acquires other small competitors as noted in the last quarter, I would expect FCF growth. Yes, there are risks from the limited number of suppliers of equipment, an increase in interest rates, and losing key members of the team. With that, I believe that the stock price could trade at a higher level.

Business Model

Founded in 1996, Mister Car Wash presents itself as the largest national car wash brand offering cleaning services to customers across 21 states. We are talking about a firm that reports close to $758 million in sales and adjusted EBITDA of close to $254 million.

Source: Investor Relations

In my view, Mister Car Wash offers a quality service thanks to successful hiring programs and engaging strategies. The company repeated many times how important human resources are for the organization. In this regard, I would like to include the following lines.

As a result, our team members are highly engaged and deliver memorable experiences to our customers. We have proven our people-first approach is scalable and has enabled us to develop a world class team, comprised of both internally developed talent and external hires from top service organizations. We believe our purpose-driven culture is critical to our success. Source: 10-k

Apart from the large network of locations among many regions in the United States, I believe that the most interesting about Mister Car Wash is the EBITDA margin. We are talking about a business model that has an adjusted EBITDA margin of close to 32% including stock-based compensation.

Source: 10-k

In my view, such an impressive EBITDA margin would not be possible without the efficient, repeatable, and scalable process that management calls Mister Experience as well as the monthly subscription program, Unlimited Wash Club.

According to recent presentations that I could find, the subscription model offers a significant amount of net sales and FCF predictability, which most market participants would appreciate. It is also worth noting that the average membership per store increased significantly since 2016. Clearly, Mister Car Wash developed a business model and know-how that are working pretty well. With this in mind, I do not see why previous performance would be better than future performance.

Source: Investor Relations

The net revenue, adjusted EBITDA, and unit count increased significantly since 2010. According to a recent presentation, net revenue increased by 18% CAGR, and adjusted EBITDA increased by close to 28% CAGR. With this level of business growth, I think that the EV/EBITDA and EV/FCF would most likely be very decent.

Source: Investor Relations

Optimism And Beneficial Market Expectations

I believe that the company was quite optimistic about the future. In the last quarterly report, the company expects to acquire new locations and deliver EBITDA growth and annual unit growth. According to management, the state of the balance sheet provides sufficient flexibility to grow organically as well as inorganically.

Source: Investor Relations

I believe that investors may be interested in having a look at the expectations of financial analysts. The expectations appear quite beneficial. They include net sales growth, net income growth in 2024, and positive FCF in 2023 and 2024. Analysts are expecting that Mister Car Wash would report 2024 net sales of about $1.023 billion, with 2024 EBITDA of $317 million, 2024 EBIT of $229 million, and 2024 net income of $118 million. Finally, 2024 free cash flow would stand at close to $45.7 million.

Source: marketscreener.com

Stable Balance Sheet

The last balance sheet included total assets growth driven by cash increase and an increase in property, plant, and equipment. The total amount of liabilities also increased, so I do not believe that investors would be that optimistic about the change in the balance sheet. Long term debt, deferred tax liabilities, and deferred revenue increased.

As of March 31, 2023, Mister Car Wash reported cash and cash equivalents worth $69 million, other receivables worth $14 million, inventory of close to $8 million, and prepaid expenses and other current assets of close to $10 million. Total current assets would be close to $104 million, below the total amount of current liabilities. I do not like this part of the balance sheet. However, taking into account the amount of property, equipment, and goodwill, I believe that management will most likely not suffer a liquidity crisis. I believe that banks would help the company. The property and equipment stood at $596 million, with operating lease rights of use assets worth $776 million, goodwill of $1.109 billion, and total assets close to $2.717 billion.

Source: 10-Q

The list of liabilities includes accounts payable worth $30 million, accrued payroll and related expenses of close to $20 million, and current maturities of operating lease liability worth $41 million. Total current liabilities were equal to $153 million.

With a long-term portion of debt of about $896 million, operating lease liability close to $758 million, and financing lease liabilities worth $14 million, total liabilities stood at $1.888 billion. The asset/liability ratio stands at more than 1x, so I think the balance sheet stands in good shape.

Source: 10-Q

My Financial Model

Under my financial model, I assumed that new members will continue to increase, and penetration may also creep higher. In my view, further increase in membership per location could occur, which may bring FCF growth. In this regard, management provided the following optimistic commentary in the last annual report.

We estimate that the average UWC Member spends more than four times the retail car wash consumer, providing us an opportunity to increase our sales as penetration increases. At both new greenfield and acquired locations, we have developed proven processes for growing UWC membership per location. Source: 10-k

Besides, I believe that considering the state of the balance sheet and expertise in the M&A markets, we could expect further acquisition of new locations. As a result, we could expect significant FCF generation in the next decade.

We will continue to employ a disciplined approach to acquisitions, carefully selecting locations that meet our criteria for a potential Mister Car Wash site. We have a track record of location growth through acquisitions and have a process for integrating acquired locations, which includes a variety of upgrades to each location that has led to the successful integration of over 100 acquisitions during our history. Source: 10-k

Moreover, I believe that more locations, further economies of scale, and efficiency will most likely bring increases in the EBITDA margin and the FCF margin. As a result, I believe that we may see an eventual increase in the EV/FCF and the EV/EBITDA.

As we open and acquire new locations and maximize throughput at our existing locations through our ongoing focus on operational excellence, we believe we will have an opportunity to generate meaningful efficiencies of scale. Source: 10-k

Source: Ycharts

With regards to the recent reduction in employees, under my DCF model, I assumed that the company will hire once again soon. The company hired a lot in the past. I do not see why hiring would stop. As I said earlier, I think that one of the main talents of Mister Cash Wash is its ability to hire and train good employees.

As of December 31, 2022, we employed approximately 6,350 team members, which is a 6% reduction from the prior year, even while adding 40 locations throughout the year. This reduction was achieved primarily through natural attrition combined with more precise staffing guidelines for our wash locations and converting eight of our interior clean locations to express locations. Source: 10-k

Source: Ycharts

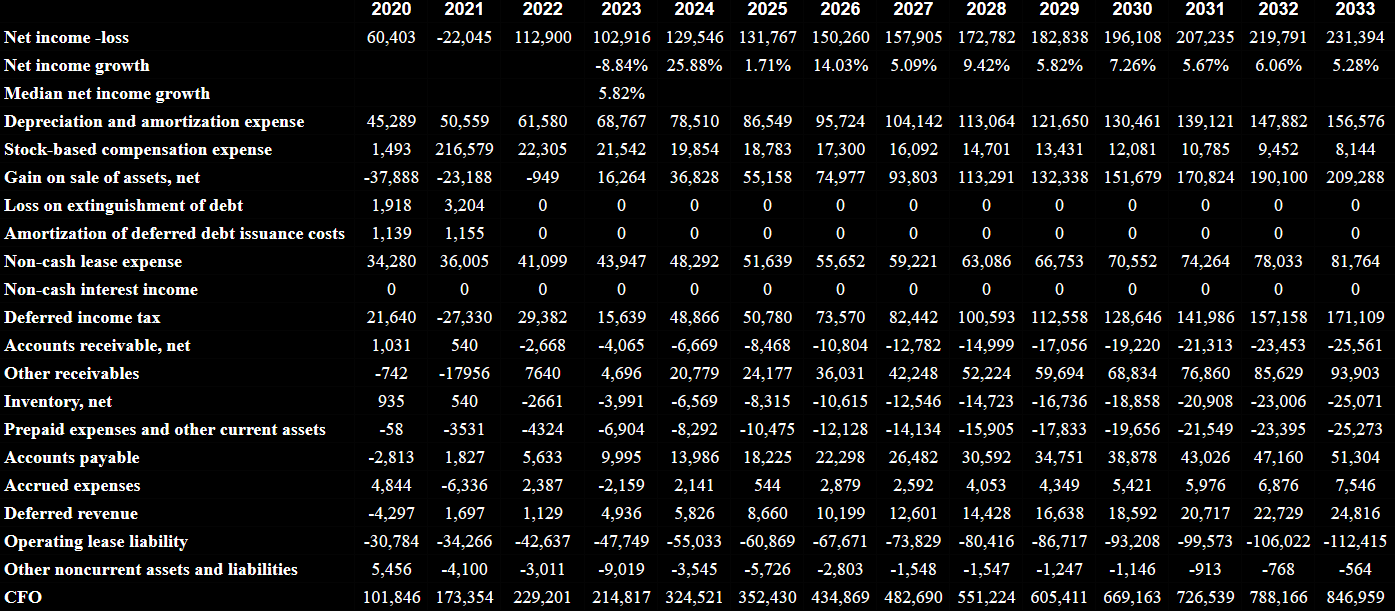

Considering previous growth, my DCF model included median FCF growth of 13.78% and median net income growth of about 5.82%. I believe that my figures are conservative, and are in line with the inorganic and organic growth that Mister Car Wash could deliver in the near future.

Source: My DCF Model Source: My DCF Model

{kind=link}

{kind=link}

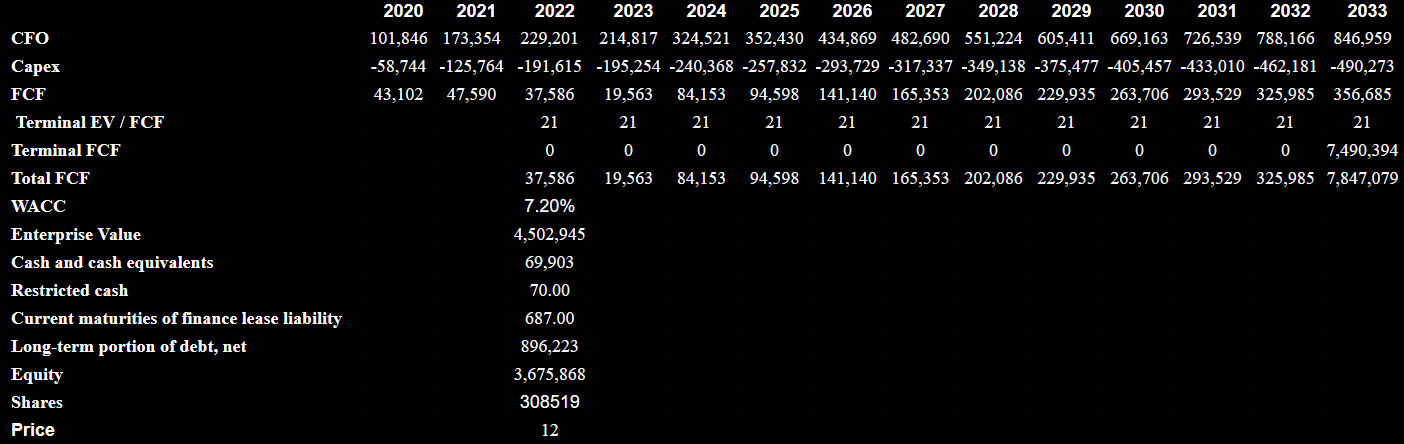

My financial model included 2033 net income of close to $231 million, depreciation and amortization expenses of close to $156 million, stock-based compensation expenses of $8 million, accounts receivable close to -$26 million, accounts payable of about $51 million, accrued expenses of $7 million, and 2033 deferred revenue worth $24 million. Besides, with operating lease liability of -$113 million, I obtained 2033 CFO of $846 million, capital expenditures of -$491 million, and 2033 FCF of close to $356 million.

{kind=link}

If we include a WACC of 7.2% and an EV/FCF of close to 21x, the implied enterprise value would be about $4.502 billion. Adding cash and cash equivalents of close to $69 million and long-term portion of debt of $896 million would imply an equity valuation of $3.675 billion. Finally, the implied fair price would be about $11.91 per share.

{kind=link}

Risk Factors

Mister Car Wash would most likely suffer if suppliers decide to renegotiate certain terms, or management cannot find certain car wash equipment. Supply chain issues coming from the limited number of suppliers is also a risk. These complications and others could lead to FCF margin decreases or lower net income expectations. As a result, I believe that certain market participants may sell their stakes, which would lead to lower stock prices.

We rely on a limited number of suppliers for most of the car wash equipment and certain other supplies we use in our operations. Our ability to secure such equipment and supplies from alternative sources as needed may be time-consuming or expensive or may cause a temporary disruption in our supply chain. In recent months, we have anticipated intermittent shortages of certain supplies from our standard vendors and, accordingly, we enhanced our sourcing procedures to identify alternative suppliers and avoid any actual shortages, albeit sometimes at additional cost. Additionally, we do not have a supplier contract with our main supplier of car wash tunnel equipment, and our orders are based on purchase orders. Source: 10-k

I also believe that a shortage of personnel and unnecessary or failed restructuring processes could lead to lower quality and even brand destruction. Besides, a generalized increase in salaries in the industry would also lead to lower FCF expectations or lower FCF margins. In this regard, Mister Car Wash offered the following explanation about further risks.

The operation of our locations requires both entry-level and skilled team members, and trained personnel continue to be in high demand and short supply at competitive compensation levels in some areas, which is likely to result in increased labor costs. Source: 10-k

While the competition for skilled labor is intense and subject to high turnover, we believe our approach to wages and benefits will continue to allow us to attract suitable team members and management to support our growth. Source: 10-Q

In my view, further increase in the interest rates may affect the ability of Mister Car Wash to refinance its debt in 2026. I believe that the interest rate expenses paid by Mister Car Wash are not worrying. However, if banks do not offer good financing conditions, the cost of capital may increase, which may lead to lower implied stock price.

Source: 10-k

The Amended First Lien Credit Agreement changed the interest rate spreads associated with the First Lien Credit Agreement where (i) the variable margin associated with the Base Rate interest rate plus a variable margin based on the Company’s First Lien Net Leverage Ratio changed from 2.25% to 2.50% to 2.00% to 2.25% and (ii) the variable margin associated with the Eurodollar Rate interest rate for one, two, three or six months plus a variable margin based on the Company’s First Lien Net Leverage Ratio changed from 3.25% to 3.50% to 3.00% to 3.25%. Source: 10-k

Finally, I believe that the company may suffer significantly from inflation. Salaries and other operating expenses may increase, which would lower the operating margin. If management cannot successfully increase the price of services offered, I think that FCF margin expectations may decline, which would drive the stock price down. In the last quarterly report, management provided some explanation about the growing risks from inflation.

While it is difficult to accurately measure the impact of inflation due to the imprecise nature of the estimates required, we have recently experienced the effects of inflation on our results of operations and financial condition. In light of the current inflationary market conditions, we cannot assure you that our results of operations and financial condition will not be materially impacted by inflation in the future. Source: 10-Q

Conclusion

Mister Car Wash recently delivered an impressive adjusted EBITDA margin thanks to a business model based on a diversified portfolio of locations and beneficial human resources practices. In my view, growing economies of scale, further hiring, and successful training will most likely lead to growing efficiency and FCF growth. Yes, I see risks from inflation, limited number of suppliers, loss of key employees, and growing interest rates. With that, I believe that Mister Car Wash could trade at higher price marks.

For further details see:

Mister Car Wash: Massive Margins And More Hiring Imply Undervaluation