MITT - MITT.PA And MITT.PC; Still Getting A Hold Rating At Best

2023-07-12 02:00:00 ET

Summary

- The article provides an update on MITT Preferreds, focusing on two of them: AG Mortgage Investment Trust 8.25% PFD SER A and AG Mortgage Investment Trust, Inc. 8% CUM PFD SER C.

- It's important to understand the issuer before investing. MITT seems riskier than other mREIT stocks, which is something potential investor needs to consider.

- For those willing to take on more risk for the 150-250bps yield bump, these Preferred stocks would be a Buy; for me, at best, a Hold.

(This article was co-produced with Hoya Capital Real Estate )

Introduction

Risk = return: I remember my Investments 101 class drilled that into us Finance majors. The corollary being, "If it seems too good to be true, it probably is!". Preferred stocks have risks that differ from common stocks or bonds, partially from where they stand in the capital structure. mREIT ones have their own unique risks because of the underlying issuer; thus requiring the investor to research not just the preferred itself, but the issuer too. I list several of these in the Portfolio strategy section later.

I also reference another Seeking Alpha contributor's review of MITT at the end of this article but I agree this stock, thus its preferreds, have higher risks than other preferreds in general and compared to other mREIT preferreds available. For those willing to take on that risk for the 150-250bps yield bump, they would be a Buy; for the risks I take, at best, a Hold.

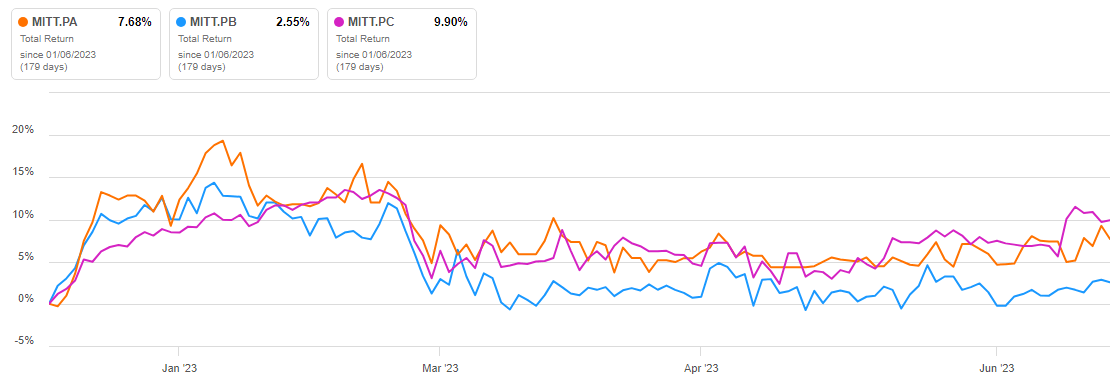

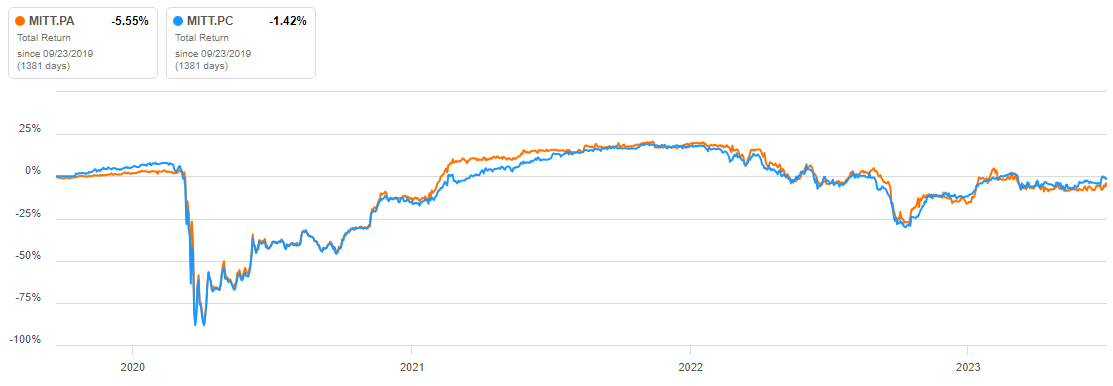

Now that we are hopefully past the banking crisis caused by several large bank failures in March of this year, I thought it was a good time for an update on my AG Mortgage Investment Trust Preferreds Reviewed article. Here is how the three have done since that publication in January.

{kind=link}

seekingalpha.com charting

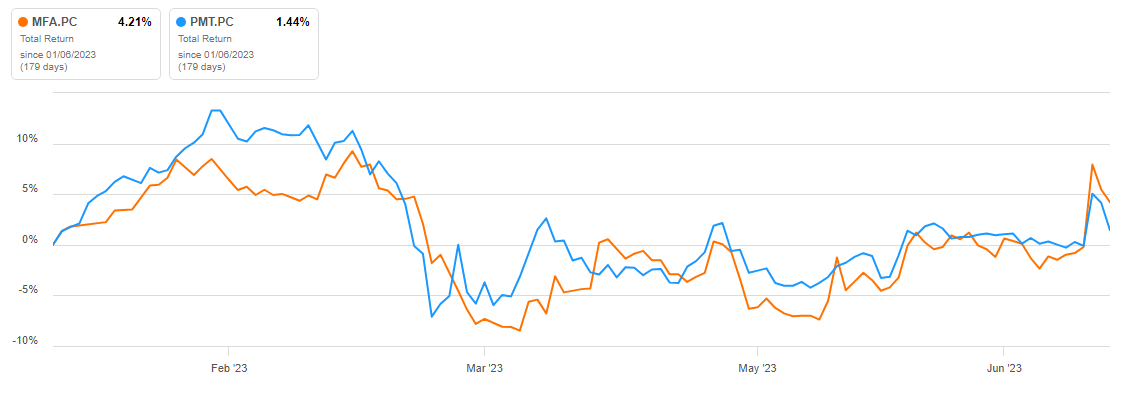

All three were rated as Holds as MITT held extra risk that I saw even then. This is how they did over the same period versus an MFA Financials and PennyMac preferred, which I recently reviewed.

{kind=link}

seekingalpha.com charting

Compared to these, the MITT "A" and "C" reviewed again here were better investments.

While my previous article covered all three available Preferreds, here the review will focus on two with major feature differences. The third one is very close to the first of those reviewed this time, these being the:

- AG Mortgage Investment Trust, Inc. 8.25% PFD SER A ( MITT.PA )

- AG Mortgage Investment Trust, Inc. 8% CUM PFD SER C ( MITT.PC )

Before those reviews start, understanding the Issuer is important as Will Rogers, the Comedian cowboy once said, "I am more interest in the return of my money, not the return on my money!".

AG Mortgage Investment Trust review

Before looking and comparing the preferred stocks, here is a brief but important overview of the issuer. Seeking Alpha describes the issuer as:

AG Mortgage Investment Trust, Inc. operates as a residential mortgage real estate investment trust in the United States. Its investment portfolio comprises residential investments, including non-agency loans, agency-eligible loans, re-and non-performing loans, and non-agency residential mortgage-backed securities. The company qualifies as a real estate investment trust for federal income tax purposes. It generally would not be subject to federal corporate income taxes if it distributes at least 90% of its taxable income to its stockholders. The company was incorporated in 2011 and is based in New York, New York.

Source: seekingalpha.com MITT

{kind=link}

agmortgageinvestmenttrust.com Q1 PDF

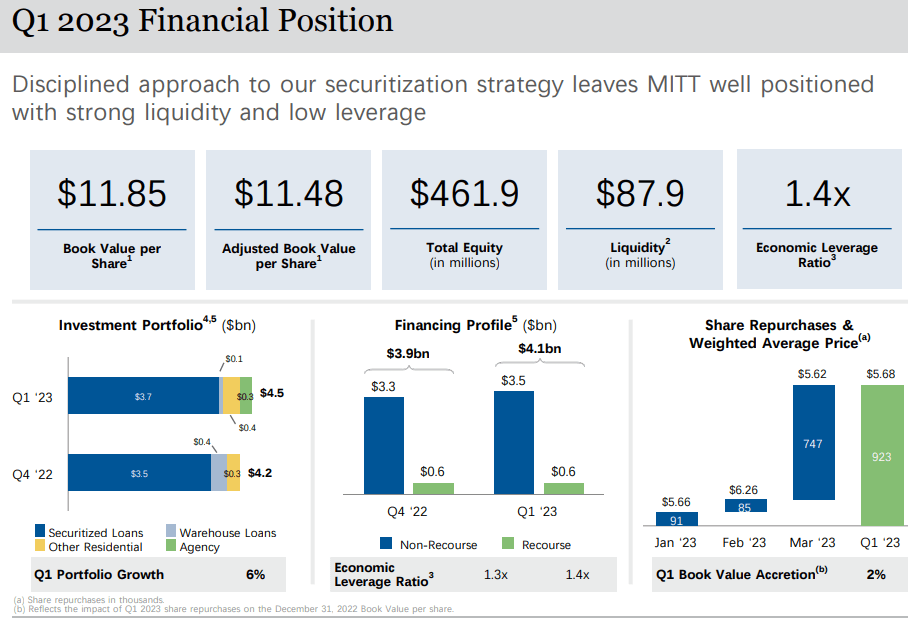

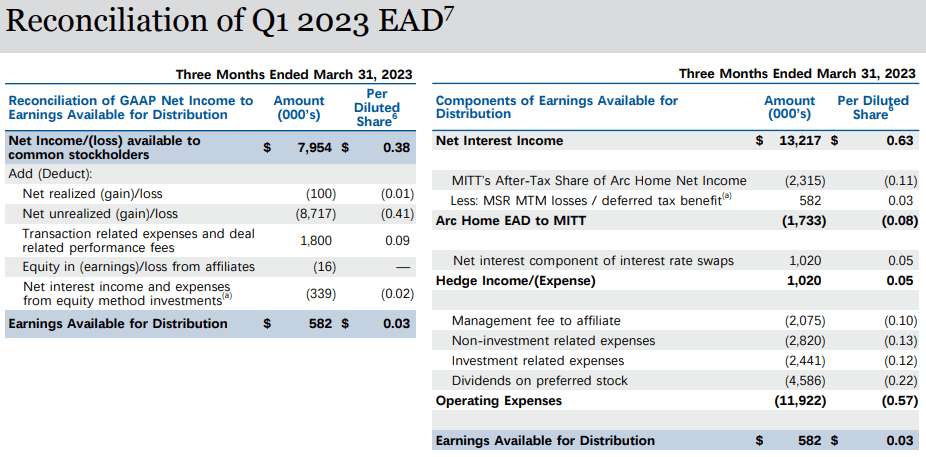

The Book Value climbed 4% from the prior quarter; earning came in at $.38, up $.05 from the prior quarter. The next set of data shows that income available to common stockholders ($7954) is 1.74X, what is needed to pay the preferred stockholders ($4586).

{kind=link}

agmortgageinvestmenttrust.com Q1 PDF

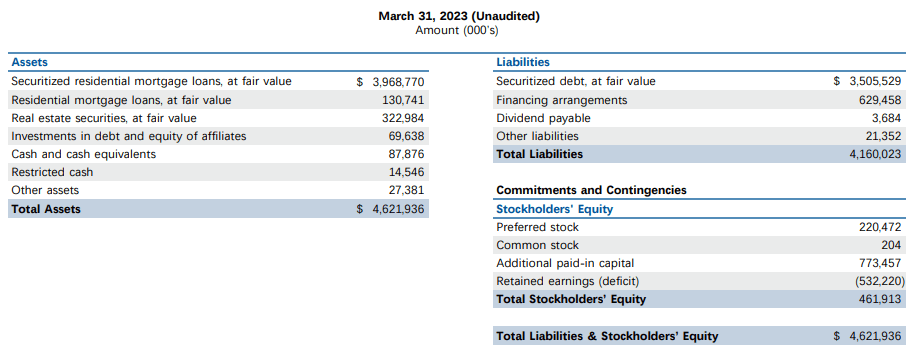

Analyzing Balance Sheets is not one of my strengths, but we should take a look.

{kind=link}

agmortgageinvestmenttrust.com Balance Sheet

What Preferred holders want to know is simple: "Are there assets going to pay me back, not just make the dividend payments?". The post-PFD stockholders' equity says yes as there is about $241m to cover $220m in Preferred stock. So currently, there is both the cash flow to make the dividend payments and redeem the preferred stock if MITT failed.

The Board and Executive Officers own 3.6% of the common shares; Beach Point Capital another 10.8%; showing some level of confidence in MITT's ability to be an ongoing mREIT. Also, in 2022, it appears MITT was able to issue about 8m shares of the common stock.

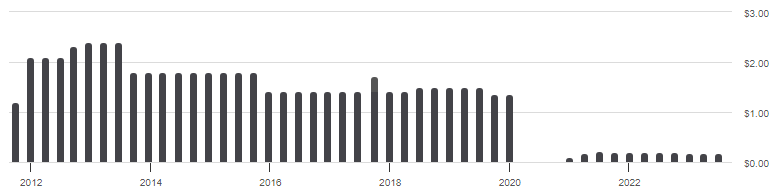

MITT distributions

{kind=link}

seekingalpha.com MITT DVDs

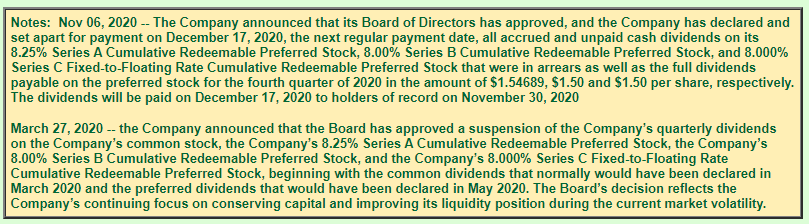

Dividends have never totally recovered from COVID. With mREITs basically trading on their yield, this explains why the MITT stock price is running at 10% of its pre-COVID levels when payouts peaked at $1.50. MITT cut the payout bac to $.18 at the end of 2022.

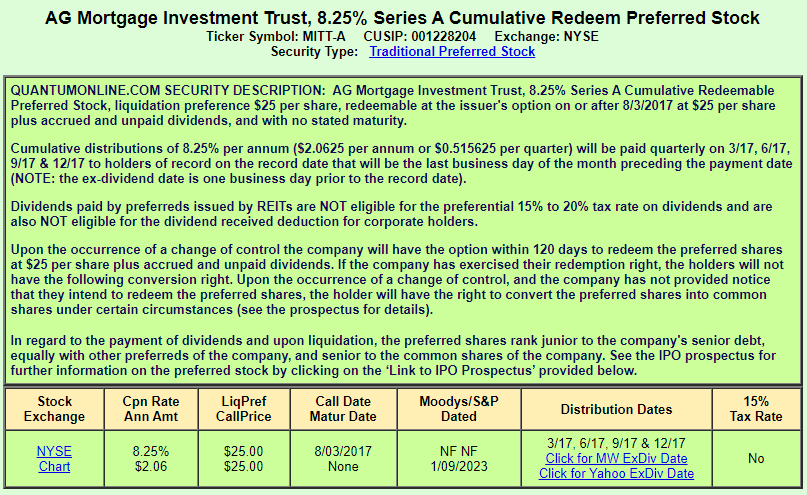

AG Mortgage Investment Trust, Inc. 8.25% PFD SER A review

{kind=link}

QuantumOnline.com

All the Preferreds are on the same level of the capital structure. "A" has been callable for years but hasn't been. With interest rates much lower over that period than now, being called seems very unlikely.

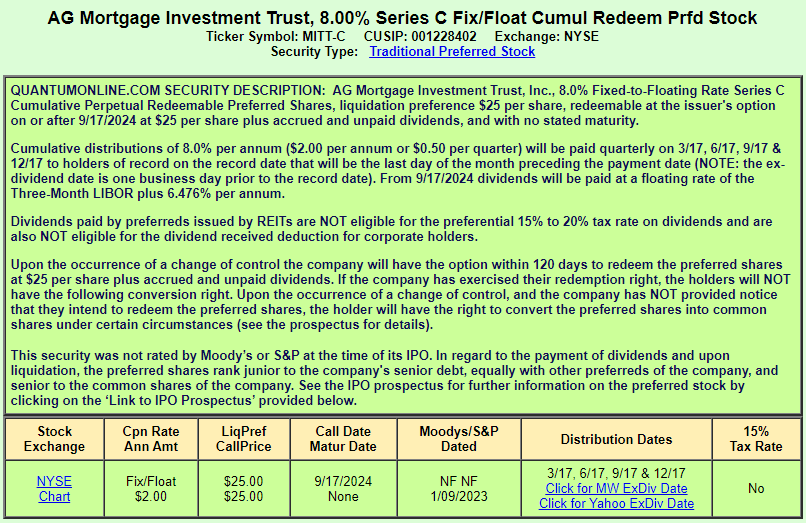

AG Mortgage Investment Trust, Inc. 8% CUM PFD SER C review

{kind=link}

QuantumOnline.com

Since I do not see "A" being Called, the fact that "C" cannot be until late 2024 provides little benefit. Depending on where SOFR is will determine which issue is more prone to get Called after "C" becomes eligible. A SOFR over 180bps would put "C" in front of "A" in the Call pecking order.

Comparing the Preferred stocks

{kind=link}

seekingalpha.com charting

One feature of both is their cumulative feature, which came into play for both with the onset of COVID. Both preferreds missed two dividend payments that were made up in the last payment of 2022.

{kind=link}

QuantumOnline.com

| Factor |

| "A" Pfd |

| "C" Pfd |

| Issue size |

| $51.8m |

| $114m |

| Price |

| $17.55 |

| $18.19 |

| Coupon |

| 8.25% |

| 8.00% |

| Yield |

| 11.40% |

| 11.34% |

| Call date |

| 8/3/2017 |

| 9/17/2024 |

| Post-Call Yield |

| 8.25% |

| 3-mo SOFR+ 6.476bps |

SOFR has replaced LIBOR as the floating-rate index. As the Fed pushed up rates, the 3-mo SOFR followed.

MITT can currently Call both the "A" and "B" issues. If a Call happens, I think MITT will wait and call the "C" issue first as currently its coupon will be over 11% with where the SOFR stands today.

Portfolio strategy

Risk and reward, two cornerstones of any investment strategy: how much of the first are you, the investor, willing to take to get price appreciation and/or income generated. MITT, as with all mREITs, face risks that can blow up any good investment thesis. Here are just a few MITT and its kind face.

- Interest rate risk: If interest rates rise, the value of mortgage-backed securities may decline, which can negatively impact the value of a mortgage REIT. Like the banks that failed, mREITs tend to borrow short, lend long.

- Credit risk: The risk of default by borrowers on the underlying mortgages increases with interest rates if they take at ARMs. Too many defaults and the value of the MBSs held may decline.

- Prepayment risk: If borrowers prepay their mortgages, it can cause the value of the mortgage-backed securities held by the REIT to decline. Higher rates can speed up payments on ARMs; lower rates spur refinancing turnover.

- Liquidity risk: mREITs may have difficulty selling their MBS assets when buyers leave or investor fear they will: think March 2020.

Action path

In summary, the two important features (differences) mentioned in the title are:

- Fixed ("A") or Floating ("C") coupons with "C" highly likely to be yield more once its floats in late 2024.

- While "A" is currently callable and "C" not until late 2024, there is that risk of owning "A". Considering "A" has been callable for yeas and hasn't been, I rate the first difference as much more important.

Assuming you are like Will Rogers, the first due diligence step is taking a deeper drive into the issuer, AG Mortgage Investment Trust, and a good starting point would be the last Seeking Alpha article from May: AG Mortgage: Good Signs Are Popping Up, But Still Not Enough . Assuming MITT passes the "smell test", I lean toward holding the "A" preferred as seeing the 3-month SOFR below 1.8% looks doubtful based in the levels seen pre-FOMC interference with ST interest rates. That said, looking at other mREIT preferreds, such as those issued by MFA Financial or PennyMac ( article link ) also need to be considered. Here is a short list of other possibilities.

seekingalpha.com HCIB

Final thoughts

As a disclaimer, I am not an expert on mREITs and depend on others to help me make those investment allocations. I recommend for reading the Mortgage REITs: High-Yield Risk And Opportunity as a great review of the sector in greater detail.

For further details see:

MITT.PA And MITT.PC; Still Getting A Hold Rating At Best