MMD - MMD: A Solid Muni Fund That Is Worth Putting On A Watchlist

2023-10-03 06:21:56 ET

Summary

- MainStay MacKay DefinedTerm Municipal Opportunities Fund is a CEF focused on generating current income from investment grade municipal bonds.

- MMD has a conservative management team and a history of peer-leading performance in the municipal bond asset class.

- While I am cautious on long-duration bonds at the moment, I believe the MMD fund is worthwhile to put on a watchlist for when the bond markets eventually turn.

A few weeks ago, I wrote a cautious article on the Guggenheim Taxable Municipal Bond & Investment Grade Debt Trust ( GBAB ), arguing investors should consider switching out of the amortizing 'return of principal' fund.

I believe a good alternative to GBAB may be the MainStay MacKay DefinedTerm Municipal Opportunities Fund ( MMD ). The MMD fund has peer-leading historical performance and a management team that is conservative with its distribution, ensuring the distribution rate is in line with the returns of the asset class.

Although I am cautious on the municipal bond asset class due to their high duration, I am placing the MMD fund on my watchlist for when my macro view on interest rate changes.

Fund Overview

The MainStay MacKay DefinedTerm Municipal Opportunities Fund is a close-end fund ("CEF") that seeks current income from a portfolio of investment grade municipal bonds.

Under normal market conditions, the MMD fund will invest at least 80% of its managed assets in municipal bonds, the interest on which is generally excluded from U.S. Federal income tax (although they may still be subject to state taxes and the Federal Alternative Minimum Tax).

Although the MMD fund may invest in municipal bonds rated in any rating category, the manager has chosen to invest at least 75% of the managed assets in investment grade municipal bonds rated BBB- or above by at least one rating agency. The fund may invest up to 25% in non-investment grade municipal bonds ("junk bonds").

As of June 30, 2023, the MMD fund had $478 million in net assets and $744 million in managed assets for 36% effective leverage (Figure 1). The MMD fund charged a 2.89% net expense ratio in the most recent fiscal year ended May 31, 2023.

{kind=link}

Portfolio Holdings

As can be seen from Figure 1 above, MMD's portfolio is very long duration, with a portfolio leveraged duration to worst of 9.0 years and average portfolio maturity of 20.5 years.

Allocation-wise, the MMD fund's largest sector allocation is in Special Tax bonds at 22.2%, Transportation bonds at 21.3%, and Electric bonds at 13.1% (Figure 2). Only 15.9% of the assets are invested in general obligation ("GO") bonds.

Figure 2 - MMD sector allocation (newyorklifeinvestments.com)

{kind=link}

Historically, GO bonds are considered safer than revenue bonds, as they are backed by the full faith and credit of the issuing municipality whereas revenue bonds are issued against a specific revenue source, such as an electric utility or a special tax. GO bonds have historically suffered lower defaults (Figure 3).

Figure 3 - GO bonds have historically suffered less defaults (schwab.com)

Figure 4 shows the credit quality allocation of the MMD fund as of June 30, 2023. The majority of MMD's managed assets are invested in AA-rated securities (54.9%), followed by A-rated (7.7%), BBB-rated (6.5%), and AAA-rated (6.0%). The fund has 24.9% of assets non-investment grade rated.

Figure 4 - MMD credit quality allocation (newyorklifeinvestments.com)

{kind=link}

Returns

Figure 5 shows MMD's annual and trailing returns. Historically, MMD's returns were modest, with an average annual return of 6.8% from 2013 to 2021. However, 2022's return of -15.5% wiped out several years of modest returns and left MMD with -3.0% average annual returns on a 3 year basis to September 30, 2023. 5 year average annual returns are slightly better at 0.5%, while 10 year average annual returns are at 5.2%.

{kind=link}

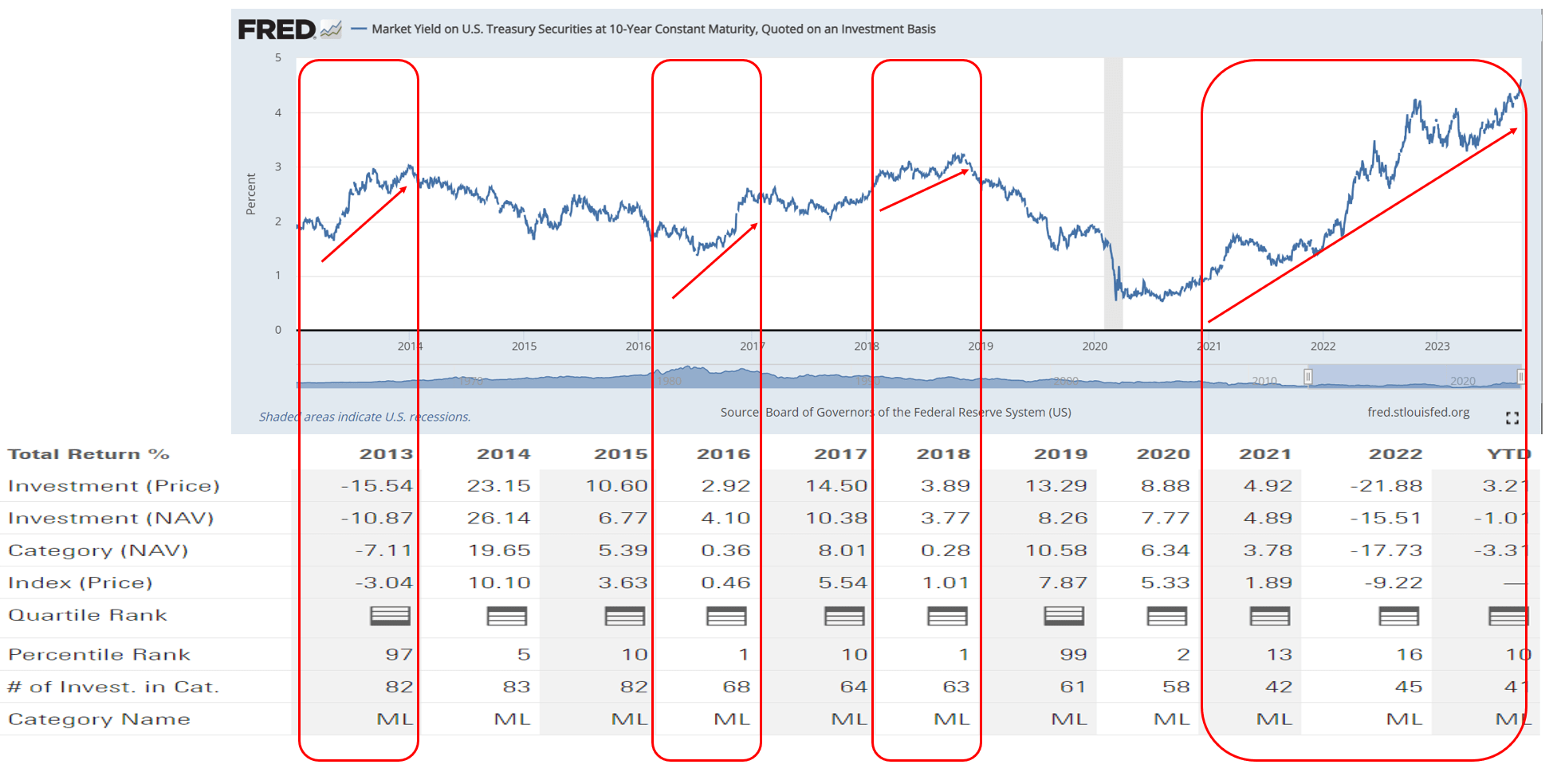

MMD's poor 2022 can be directly attributed to the fund's 9.0 year leveraged duration. Since March 2022, the Federal Reserve have increased short-term interest rates by 525 bps and long-term treasury yields have risen in sympathy, with the 10 year treasury yield rising from 1.5% at the end of 2021 to 3.9% at the end of 2022 and 4.6% recently (Figure 6). This has crushed long-duration assets like the MMD fund.

Figure 6 - 10Yr treasury yields have risen significantly (St. Louis Fed)

{kind=link}

On a first order approximation, the 2.4% increase in 10Yr treasury yields in 2022 applied to MMD's 9.0 years duration contributed 21.6% in MTM losses to the fund's returns. So the fact that the MMD fund only lost 15.5% in 2022 means the manager was able to mitigate some of the negative effects of higher interest rates through security selection and duration management.

In fact, the MMD fund is ranked first quartile compared to the Morningstar category, Muni National Long , across 1/3/5/10Yr time horizons, which is quite an achievement (Figure 5 above).

YTD 2023, the MMD fund is down 1.0% on a NAV basis as long-term yields have continued to rise.

Distribution & Yield

One attractive feature of the MMD fund is its distribution yield. The MMD fund is currently paying a $0.07 / month distribution which works out to a 5.3% forward yield (Figure 7).

Figure 7 - MMD is paying a 5.3% forward yield (Seeking Alpha)

{kind=link}

While some investors may be concerned that MMD fund has cut its distribution rate by 18% in recent months from $0.085 / month to $0.07 / month, I actually applaud the move, since the decline in the fund's NAV means there are less assets to support the old distribution rate. In fact, if investment performance continues to be poor in 2023, I believe the MMD fund should continue to cut its distribution.

Ultimately, a fund should only pay out a distribution yield that is supported by its earnings potential. Otherwise, the fund will become an amortizing 'return of principal' fund, as detailed in an Eaton Vance whitepaper .

If the municipal bond asset class only earns 5-6% long-term returns (MMD has a 10Yr average annual return of 5.2%), then the distribution yield should not materially exceed that return rate.

This is precisely the reason why I was recently cautious on the GBAB fund. Despite an earnings shortfall, the GBAB fund continued to maintain its historical distribution rate, using return of capital ("ROC") to fund the difference between returns and distribution (Figure 8).

Figure 8 - GBAB has been funding shortfall with ROC (GBAB annual report)

In contrast, the MMD fund's manager has enough awareness to understand that the municipal bond asset class cannot pay distribution yields materially higher than ~6%, and thus chose to cut its distribution. Kudos to the team for making the hard decisions.

Risk To MMD

The biggest risk to the MMD fund is rising interest rates. Historically, the MMD fund has performed poorly when long-term interest rates are rising due to the fund's long duration exposure (Figure 9). If long-term interest rates continue to rise, the MMD fund will continue to struggle on an absolute basis.

Figure 9 - MMD has struggled in rising interest rate environments (Author created with data from Stockcharts.com and Morningstar)

{kind=link}

Conclusion

The MMD fund is a CEF that actively invests in the investment-grade municipal bond markets to deliver current income. Although the MMD fund has only delivered modest historical returns, that is a function of the asset class and rising interest rates. Historically, the MMD fund has delivered first quartile performance across multiple time frames, outperforming peer municipal bond funds.

The MMD fund is currently paying a 5.3% distribution yield that has been cut by 18% in the past year. While painful, I believe this is the right decision by management as the fund's NAV has declined.

I am currently cautious on long-duration bonds, hence I rate the MMD fund a hold . However, I am adding the MMD fund to my watchlist for when my macro-view on interest rate changes.

For further details see:

MMD: A Solid Muni Fund That Is Worth Putting On A Watchlist