BURBY - Moncler: Limited Upside With Volumes And Stone Island

Summary

- Moncler's shares have underperformed its luxury fashion peer group YTD.

- Q3 FY12/2022 results highlighted signs of volume weakness, with time and investment required at Stone Island to establish a retail business.

- The shares appear fairly valued on consensus PER FY12/2024 23.3x. We are neutral on the shares.

Investment thesis

Moncler ( OTCPK:MONRF ) has underperformed its peers YTD, but we see no reason to invest. Valuations appear fair in our view, given signs of volume weakness and Stone Island's business transition to a retail model expected to take time and investment. We rate the shares as neutral.

Quick primer

Founded in 1952, Moncler S.p.A. designs, manufactures, and sells clothing and accessories through the Moncler and Stone Island brands, with the former making up approximately 80% of H1 FY12/2022 sales. The Moncler brand operates a direct-to-consumer retail model, whilst Stone Island (fully acquired in February 2021 ) operates a wholesale model relying on distributors although this is undergoing a transition. Its largest geographic market is Asia, followed by EMEA.

As a luxury fashion brand, a typical Moncler down jacket retails around USD1,000 to USD2,000. During FY12/2022 the company raised average prices by 10% YoY.

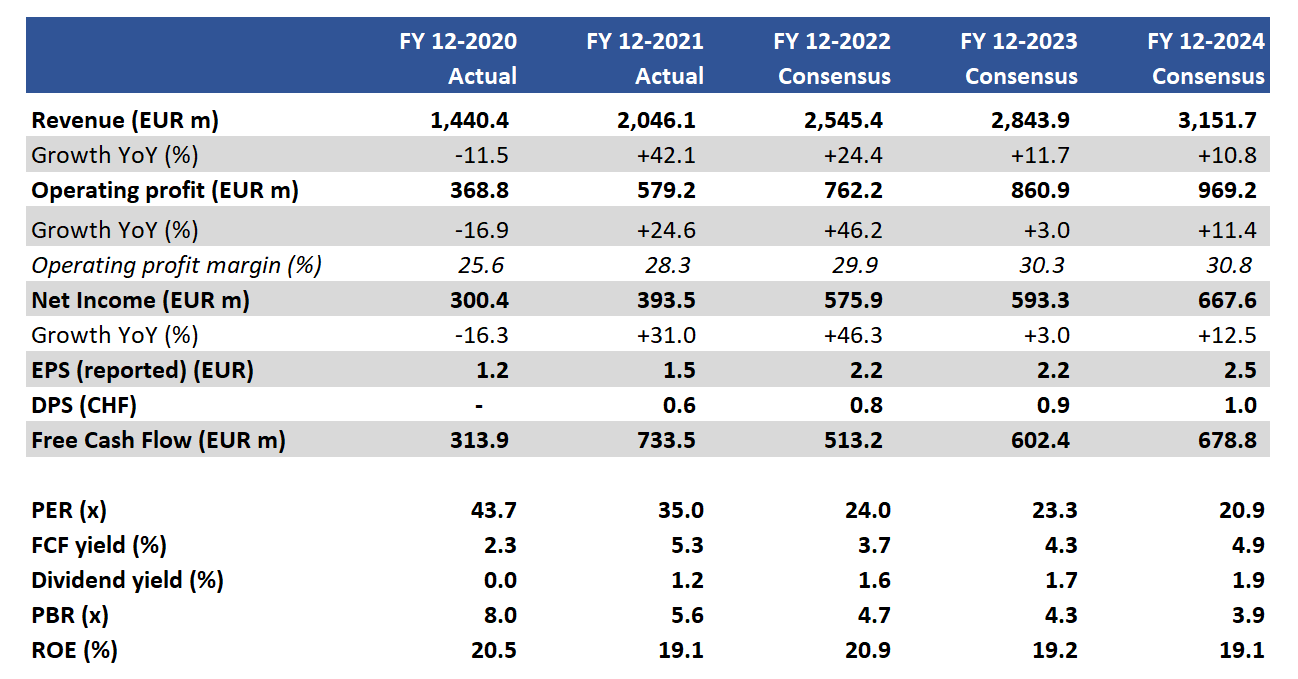

Key financials including consensus forecasts

Key financials including consensus forecasts (Company, Refinitiv)

{kind=link}

Our objectives

Moncler has a solid track record of high double-digit operating margins (a 10-year average of 28%) and is sustainably free cash flow generative. It has also notably underperformed its peers such as Burberry Group ( OTCPK:BURBY ) and LVMH ( OTCPK:LVMHF ) although the latter has a much more diversified business model.

One notable event has been Moncler's acquisition of Stone Island, a luxury men's brand initially for a 70% stake in December 2020 , followed by the remaining balance in February 2021 . The consideration totaled EUR1,150 million/USD1,480 million, based on an estimated 13.5x price/EBITDA multiple.

In this piece, we assess the outlook for the Moncler brand business, and how the acquisition of Stone Island is progressing.

Moncler dependent on price hikes

Q3 FY12/2022 YTD results were strong with revenues growing 30% YoY under constant currencies, driven primarily by the Moncler brand that grew sales by 21% YoY. Key drivers were Asia and EMEA markets, especially in Japan and Korea as well as local and US tourist demand in Europe (particularly in France, Germany, and Italy).

Demand looks robust, but there are some signs which suggest underlying growth was weaker than reported. Firstly, during Q3 the impact of price increases represented over 50% of sales growth seen in the retail business, compared to the usual contribution of 1/3. This implies that there is some concern over volumes and weakening end demand. Secondly, the strong US dollar is enabling North American tourists to enjoy a shopping spree in Europe - whilst a strong US dollar is likely for the short to medium term, this positive trend does feel temporary.

Whilst Moncler is a price maker, we note that gross margins fell to 73.8% in H1 FY12/2022 (no disclosure for Q3 FY12/2022), which is a marked decline from 75.2% in H1 FY12/2021 and 76.6% for FY12/2021. Cost inflation is having a negative impact in terms of input costs for yarn, and for labor costs in Romania where production is focused.

The question is whether volumes will start to recover as price hikes are a given in this trade and if cost inflation can be sufficiently offset. The big positive could be China's road to recovery post lockdowns, but there are mixed signals here as Guangzhou has become the latest epicenter, whilst Shanghai begins to see more loose restrictions. Management has commented that trading in China weakened in August 2022 despite better conditions earlier in Q3 FY12/2022, and we do not expect recent trading to have improved significantly.

Stone Island Impact

Whilst there is no segmental disclosure over the profitability of Moncler brand and Stone Island. With Stone Island becoming consolidated in April 2021, there is a limited track record to show if margins have been enhanced or not. However, in FY2020 the company had an EBITDA margin of 28% versus 39.6% for Moncler, so this acquisition has likely been margin dilutive. This may not be a huge surprise considering its predominantly wholesale business model.

The strategy to transition Stone Island to a direct-to-consumer retail model makes sense long term, as profitability should increase with scale. However, this period of transition means no quick fixes, and significantly higher operating expenses as well as new store openings. We believe management is playing a long game, focusing on the Asian market where there is scope for near-term results, as opposed to completely changing the model in the core European market.

Whilst there is scope for Stone Island to become a key growth driver for the business, some limitations remain. Its current model is for men's fashion only, and competes more generally with numerous high-end apparel brands. Quarterly Q3 FY12/2022 Stone Island sales only grew 1% YoY, which was explained as due to shipment timings. However, as the European market is experiencing negative consumer sentiment , we believe seasonal trading into Q4 FY12/2022 will be relatively subdued.

Valuation

On consensus forecasts, the shares are trading on PER FY12/2024 23.3x on low single-digit earnings growth YoY. We believe price hikes of around 10% YoY will naturally push up revenues YoY, but cost inflation and investment into Stone Island will mean limited scope to improve operating margins YoY. Free cash flow yield of 4.3% is respectable but does not look overly undervalued. We note cash burn in H1 FY12/2022 so FY12/2022 consensus forecasts look too bullish.

Risks

Upside risk comes from Chinese demand ramping up significantly YoY into FY12/2024, as lockdown restrictions come to an end. Continued strength in the US dollar may sustain demand from US tourists coming to Europe and buying high-end goods.

Downside risk comes from volume weakness as end demand recovery remains muted in Asia and Europe, particularly due to cost of living pressures as well and more expensive access to credit. A marked weakness in the US dollar will push down US tourist activity, although this could be a symptom of the Federal Reserve halting its tightening policy which would be positive for equities.

Conclusion

The positive case for Moncler is its ability to raise prices to offset volume weakness, and relatively high demand in Korea, Japan, and US tourist activity. The negative factors which may explain the relative underperformance of the shares are limited volume growth, dependency on China, and Stone Island a margin-dilutive acquisition that will need investment to transition to a retail model. Current valuations do not look overvalued, but we see limited attractions to invest in the shares and give a neutral rating.

For further details see:

Moncler: Limited Upside With Volumes And Stone Island