MONRY - Moncler: Stand Out Luxury Company But Market Valuations Unattractive

2023-10-03 15:25:02 ET

Summary

- Moncler's stock is up 7% this year, outperforming other luxury stocks like LVMH.

- Moncler's healthy revenue growth and sustained performance in the EMEA market, set it apart from its peers. While its margins have softened, the second half of 2023 holds promise.

- However, its market multiples are ahead of peers at a time of relative weakness in the sector, making it hard to justify buying it right now.

It's been a challenging year for luxury stocks, with shrinking sales in the US and uncertainty about future performance from China, despite the market's strong performance in the year. However, not all stocks in the segment have performed poorly.

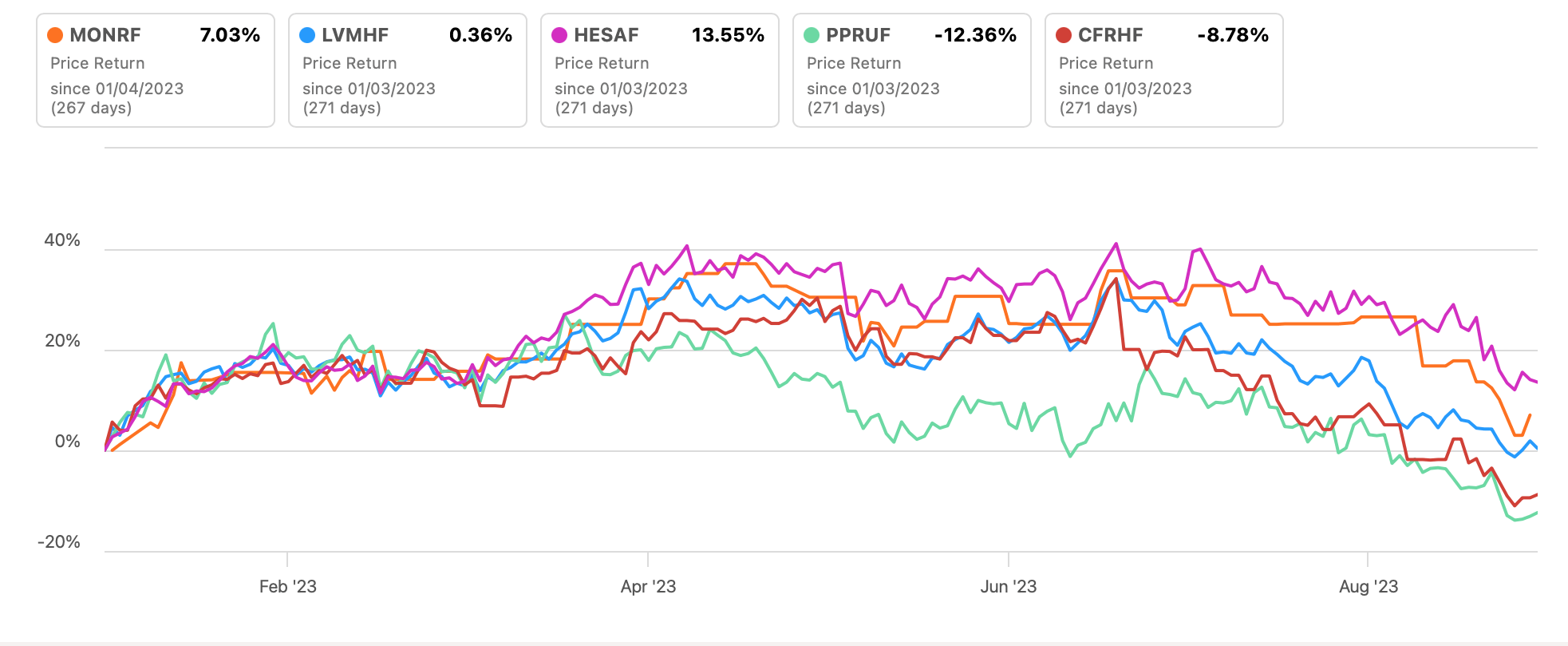

One of them is the Italian Moncler ( MONRF ), known for its outerwear, which is up by 7%. Its performance is second only to the French Birkin maker Hermès ( HESAF ), which is saying something. Hermès is in a league of its own , as both its market multiples and financials stand out from the rest of the sector. Notably, Moncler is also ahead of the big luxury company LVMH ( LVMHF ), which has made no gains this year, while the other big ones have dipped (see chart below).

{kind=link}

This raises the question, what sets the company and its stock apart? Also, in a time of reduced outlook for the sector can it continue to rise?

What sets Moncler apart

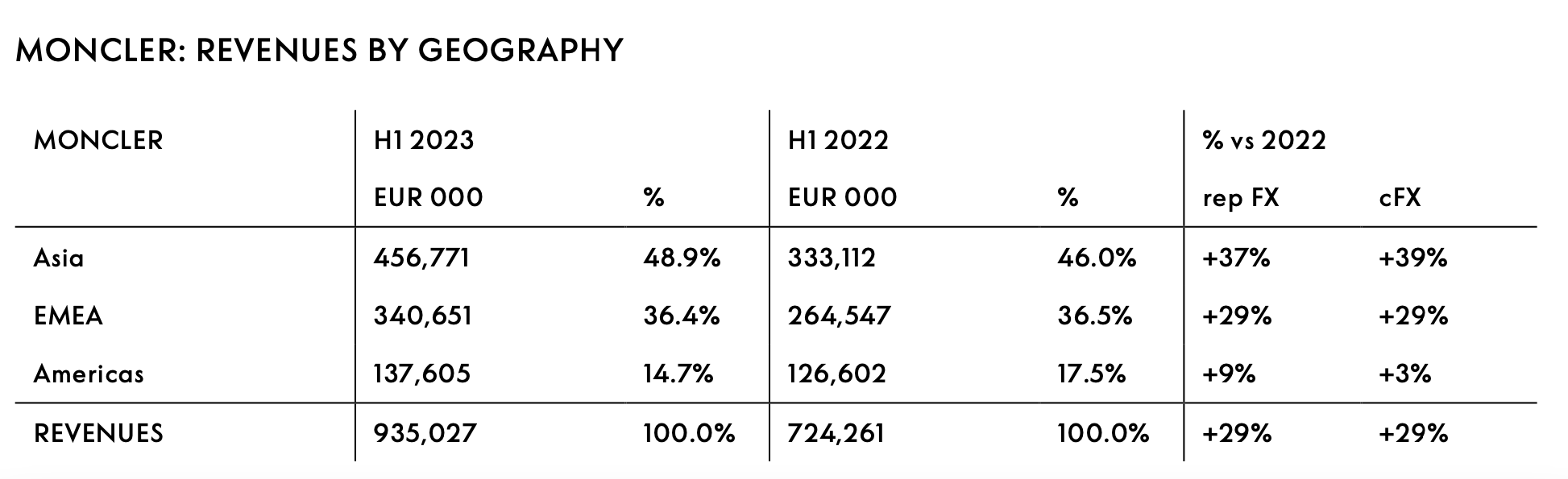

A look at its first half (H1 2023) update does indeed set it apart for multiple reasons. The first is that, unlike other luxury companies, it has actually seen an improvement in revenue growth to 29% year-on-year (YoY) from 25% in the full year 2022, though it has come off from the high 48% growth seen in H1 2022.

Besides the expected rise in Asia revenues, it has also seen sustained performance from the EMEA market at 29%, the same as that in 2022. By comparison, the region has been softening for other companies. For instance, LVMH reported a 22% growth from its Europe market in H1 2023, down from 35% in 2022.

The region, which brought in 36.4% of Moncler's revenues in H1 2023, has recently come into the spotlight after Richemont ( CFRHF ) warned of slowing demand from affluent customers in the region. That Moncler's demand in the market has stayed strong so far, then, clearly sets it apart.

{kind=link}

Further, while its Americas' growth has softened in line with the trend seen across luxury companies, it's also less concerning than for its peers. First, it has a relatively low share in the company's total revenues, at under 15% in H1 2023.

Second, Americas' demand has been affected because of the company's strategic decisions. It's personalising its sales processes at the retailer Nordstrom to build on brand perception. This is expected to have a negative impact for three to four quarters. The region clocked a 5% fall in Q2 2023, which would actually have been positive if it weren't for the strategy change.

Why margins are relatively low

Despite the robust revenue trends, however, Moncler's margins don't stand out as much. All its margins have declined from the full year 2022 (see chart below). But the decline in net margin to 12.8% from 23.3% in 2022 looks particularly disappointing as it impacts the company's EPS directly.

Source: Seeking Alpha, Moncler

In the case of margins, however, a comparison with the last full year doesn't give an accurate picture since the H1 of a year typically shows a lower operating margin compared to H2 (see chart below).

Source: Seeking Alpha, Moncler

Also, the latest net margin looks particularly bad in comparison to H1 2022, which was at a high of 23% on a positive tax impact from the brand value realignment for Stone Island, the Italian men's luxury brand acquired by Moncler in 2021. This actually resulted in a higher net income margin compared to the operating margin during H1 2022. And, of course, impacted the full-year net margin positively too.

Estimating forward EPS and multiples

In estimating the EPS for 2023, I have taken this difference between H1 and H2 margins into account, since an assumption of the same net margin as seen in H1 2023 can skew estimates to the downside. I have assumed that the net margin in H2 2023 comes in at the same level as in H2 2022 of 23.5%.

For revenues, I've gone with analysts' estimates of a 13.7% growth, down from 19.7% in 2022 in USD terms, in line with expectations of a broad-based softening in the sector. This results in a 19.3% margin for 2023 and an EPS of USD 2.30, which is a 5% decline from last year, after the year saw a one-off rise in earnings.

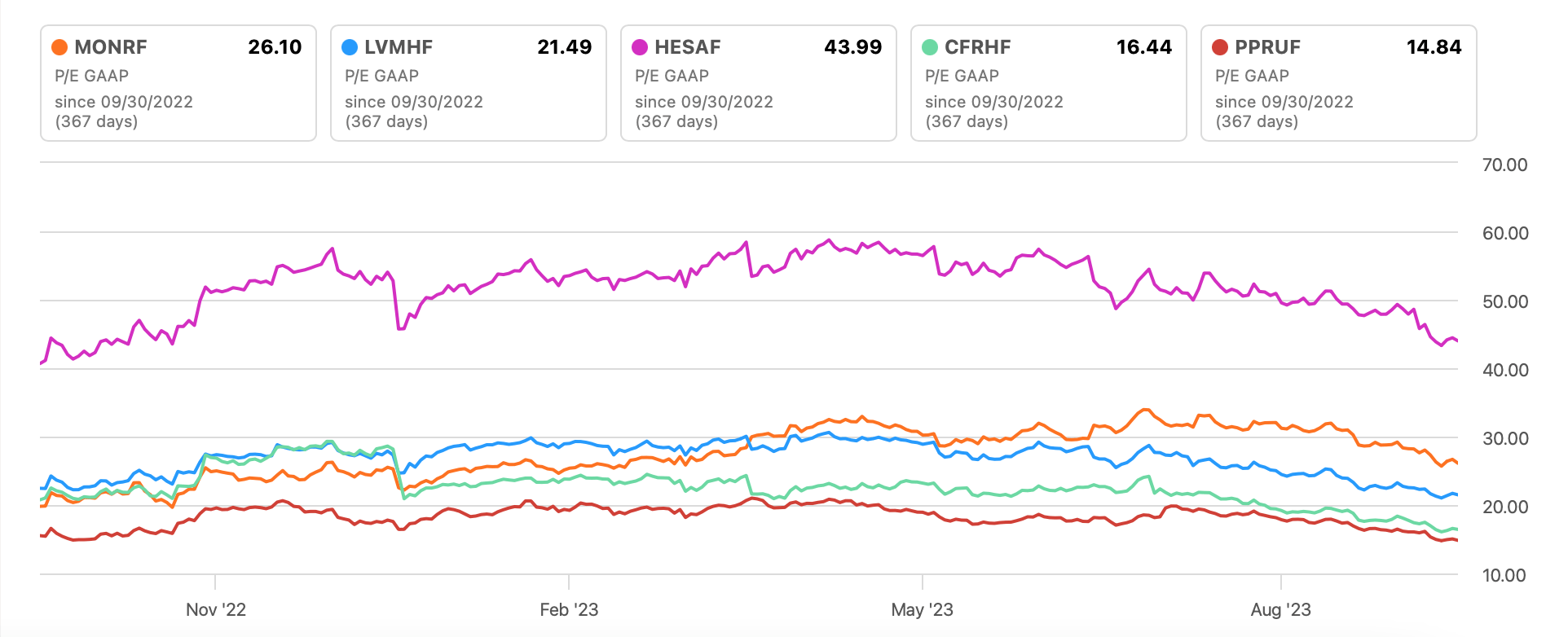

This in turn gives a forward price-to-earnings (P/E) of 25.4x, which is high compared to its peers, save Hermès, which is at 42.6x. Even LVMH is trading at a forward P/E of 21.9x. The trailing twelve months [TTM] GAAP P/E ratio shows the same trend (see chart below).

{kind=link}

What next?

The valuation discussion isn't complete without mentioning that Moncler's average P/E over the past 10 years is actually a higher 29.5x. In regular times, this would imply an upside to the stock. However, these aren't regular times. Global luxury markets are seen as weakening, and if the biggest players in the sector aren't being exempt from it, it's hard to see Moncler come out completely unscathed either. The revenue projections for 2023 certainly indicate softening ahead.

However, it does have advantages over others. For one, its relatively limited presence in the Americas market means it can be less affected by the drag from the market. Its sustained EMEA growth also goes in its favour, as it indicates continued demand in a region where it has softened for peers. And finally, with the second half of the year typically being better for its earnings than the first half, the best for 2023 may well be yet to come for Moncler.

At the same time, its attractiveness relative to peers is dulled by its relatively higher forward and TTM market multiples. It's hard to justify buying it right now when stocks like LVMH look more attractive. On its own, it's still good, but I believe the 15.4% correction seen in the past month can continue until its multiples appear in line with the sector or if its upcoming results reflect that it indeed can buck the weakening market trend. Until then, I'm going with a Hold on Moncler.

For further details see:

Moncler: Stand Out Luxury Company, But Market Valuations Unattractive