MONDF - Mondi: Expect A 15% Special Dividend Upon The Sale Of The Russian Operations

2023-03-06 11:30:00 ET

Summary

- Mondi is a UK-based leader in the paper and cardboard packaging industry.

- Unfortunately, the company is selling its Russian subsidiary at just 2.5 times EBITDA.

- The proceeds - if and when approved - will be distributed among the shareholders.

- Mondi is investing in growth, and this should pay off in the next few years.

Introduction

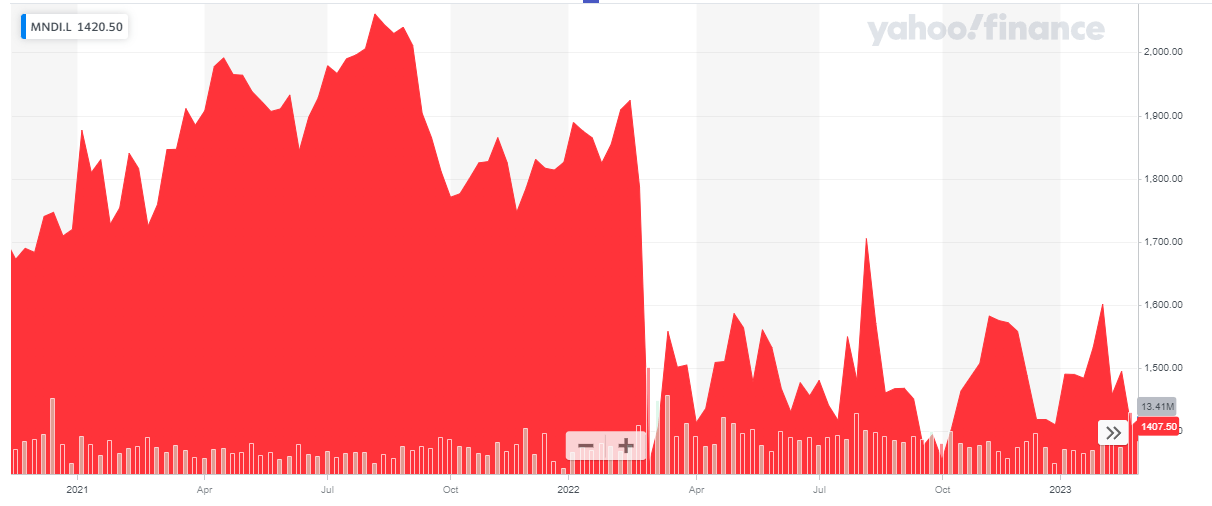

It has been less than two years since I published an article on Mondi ( OTCPK:MONDF ) ( OTCPK:MONDY ) and unfortunately the company’s share price is now trading about 25% lower. While 2022 hasn’t been the easiest year, I think Mondi deserves to be trading at a higher price and once the sale of the Russian operations has been completed, shareholders can likely look forward to a very substantial one-time dividend which could hopefully renew the interest in the story.

{kind=link}

Mondi has primary listings in South Africa and in London, and I will refer to its London listing, where Mondi is trading with MNDI as its ticker symbol with an average daily volume of almost 1.5M shares. An additional complication is that although Mondi trades in GBP, it reports its financial results in EUR and I will use the Euro as base currency throughout this article.

Despite higher operating expenses, Mondi did well in 2022

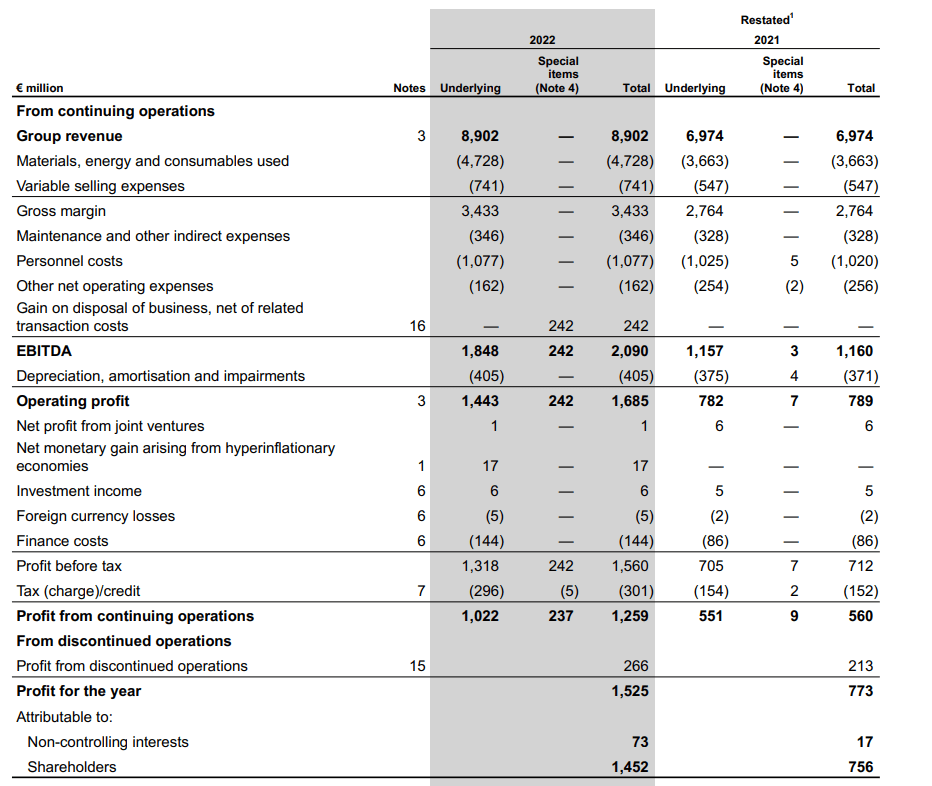

2022 wasn’t an easy year for anyone but I was pleasantly surprised to see how Mondi performed during the year. The total revenue increased to 8.9B EUR (which is almost 2B EUR higher than in 2021), but the gross margin also increased by approximately 24% to 3.43B EUR. While that’s a lower increase than the revenue jump, keep I mind Mondi is still working towards fully passing on the increased costs to the customers.

{kind=link}

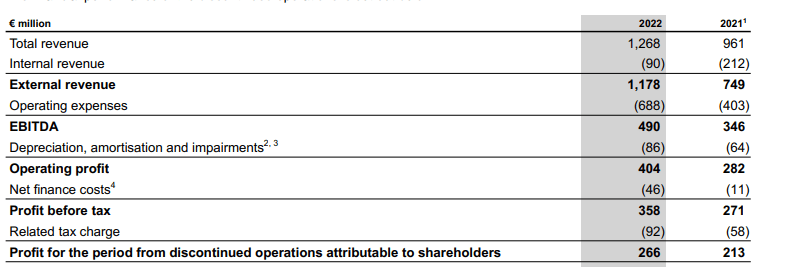

The other operating expense remained pretty stable resulting in an underlying EBITDA of 1.85B EUR. This was boosted by a 242M gain on the sale of a division so the reported EBITDA was almost 2.1B EUR, but I prefer to work with the underlying, normalized EBITDA. After deducting the depreciation and amortization expenses as well as the finance expenses, Mondi reported an underlying pre-tax income of 1.32B EUR resulting in a net income of 1.02B EUR. If you would use the non-recurring gain as well, the reported net income was 1.26B EUR with an additional 266M EUR coming in from discontinued operations. Of that amount, 1.45B EUR was attributable to the shareholders of Mondi. That represented an EPS of just under 3 EUR per share, while the underlying net income of 1.02B EUR would result in an underlying EPS of 2.10 EUR or approximately 185-186 pence per share. Which means that based on the current share price of approximately 1420 pence, Mondi is trading at less than 8 times earnings excluding the discontinued operations and excluding the non-recurring gain on the sale of a division.

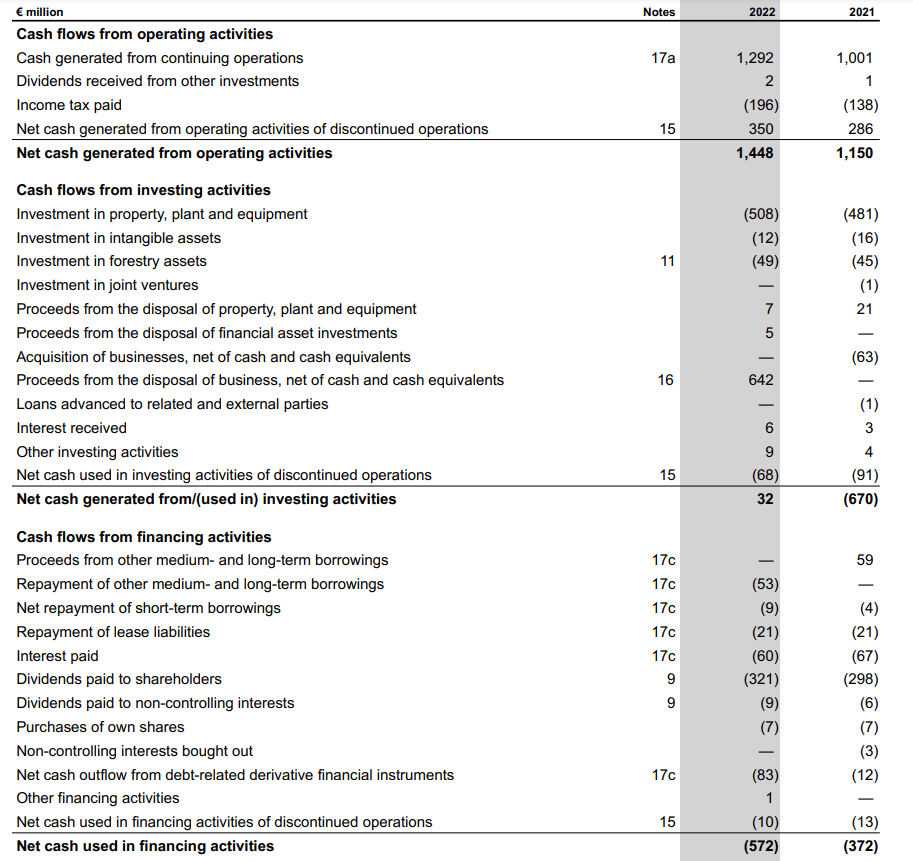

This also resulted in a strong cash flow performance. The total operating cash flow was 1.45B EUR (which includes just 196M EUR in cash taxes versus the 301M EUR owed and 350M EUR In operating cash flow from the discontinued operations).

{kind=link}

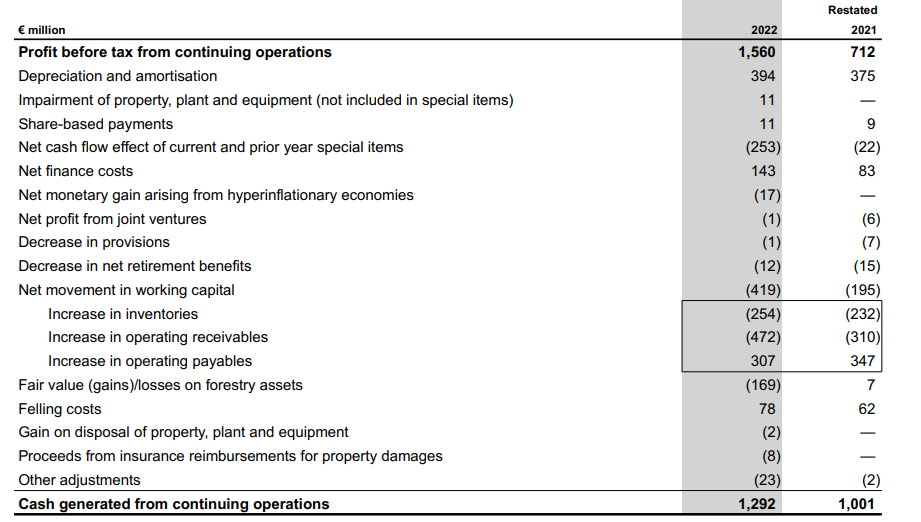

That being said, the reported operating cash flow also includes a 419M EUR investment in the working capital position, as you can see below.

{kind=link}

So if I would adjust the operating cash flow for those elements while also deducting the 81M EUR in lease payments and interest payments, the adjusted operating cash flow from continuing operations was roughly 1.34B EUR and approximately 1.3B EUR (rounded) if you take payments to non-controlling interests into account).

We see the total capex was 570M EUR, so the underlying free cash flow was approximately 730M EUR or 133 pence per share. Keep in mind this includes growth initiatives: the total depreciation and amortization expenses during FY 2022 came in at 394M EUR while the company spent about 590M EUR on capex and lease payments.

{kind=link}

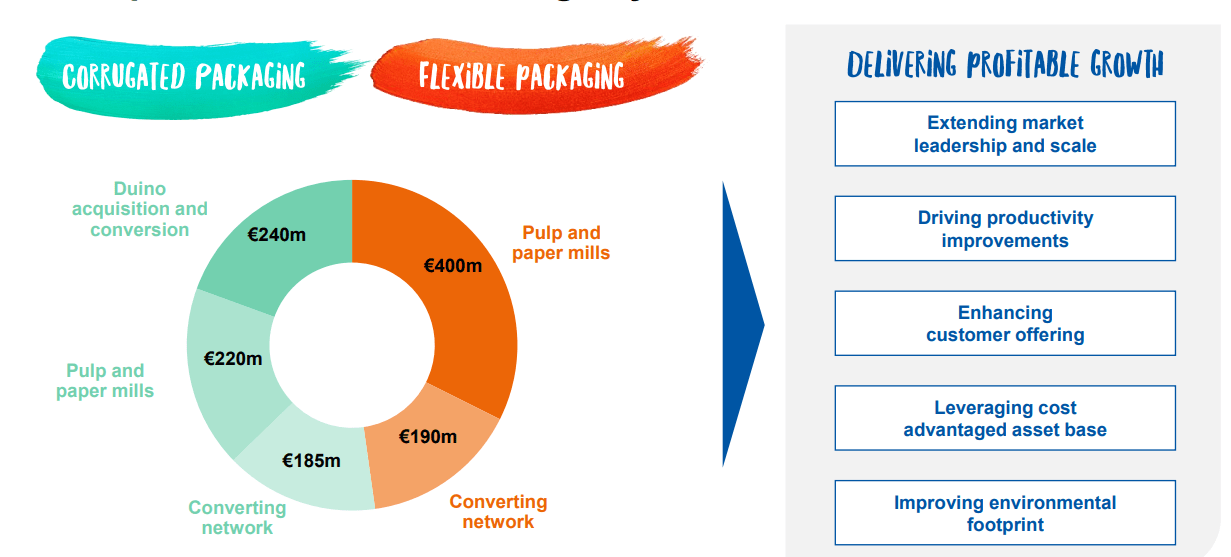

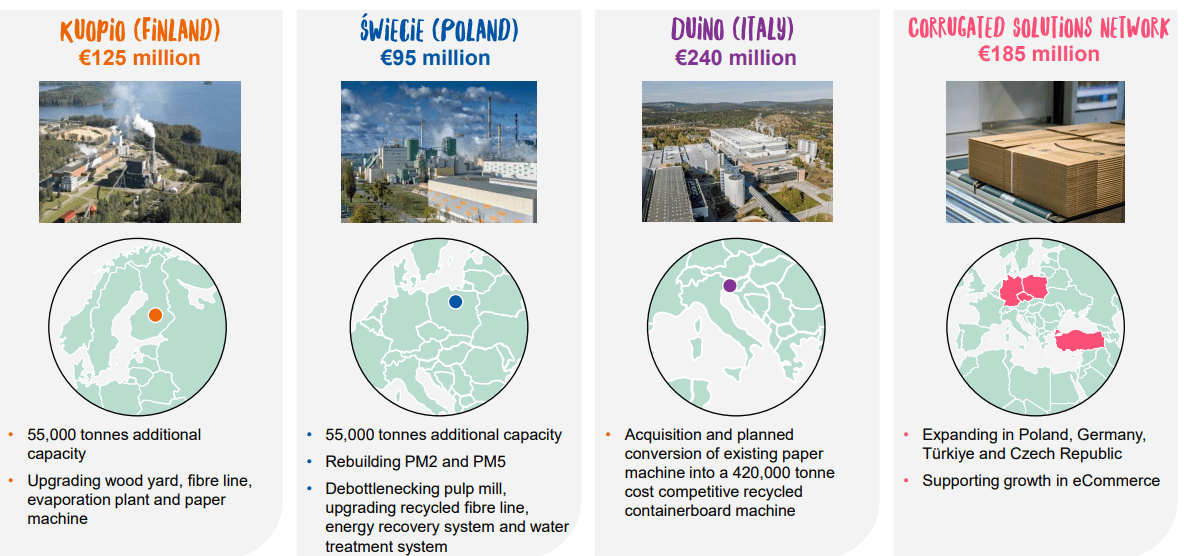

Mondi is smart when it comes to its capital allocation plans and growth investments as the ROCE exceeded 20% last year (and the company is guiding for returns in the mid-teens on the expansion capex). We should see the new or expanded assets starting to contribute pretty soon. A 125M EUR investment in a Finnish mill will be completed this year with the asset starting up in Q4 2023 while a 95M EUR debottleneck project in Poland will be effective from next year on. The 400M EUR investment in flexible packaging will result in the construction of a 210,000 tonnes capacity kraft paper production in Czechia which will start in 2025 with full production anticipated by 2027.

{kind=link}

So yes, Mondi is investing heavily (and the reported free cash flow will likely decrease this year despite pricing initiatives as demand will likely be a bit weaker which will subsequent again put pressure on prices), but there is a plan and the capacity increases will pay off within the next few years. Mondi will pay a final dividend of 0.4833 EUR with a record date of March 31 and a payment date of May 12. This brings the full-year dividend at 0.70 EUR per share.

Shareholders may receive a bonus later this year

Mondi had a sizeable amount of activities in Russia but the company decided to sell its Russian operations. In August last year, it announced the sale of its main Russian subsidiary for 95B RUB (1.18B EUR) while in December, three packaging converting operations were sold for 24M EUR . An interesting additional feature to the larger sale is that the 95B RUB sales price is on an enterprise value basis, and the Russian entity will wire 16B RUB in cash back to Mondi before the deal closes. Based on the current exchange rate, that’s an additional 200M EUR.

This means that if/when the two deals close, Mondi will receive approximately 1.2B EUR in cash and the company has pledged to distribute the cash to its own shareholders. Based on the current EUR/GBP exchange rate, this represents approximately 1.06B GBP. And considering there are currently approximately 485M shares outstanding, the special dividend upon the closing of the sale of the Russian assets will come in close to 220 pence per share, or about 15% of the current share price. As Mondi is domiciled in the UK , there should be no foreign dividend withholding tax.

It's a waiting game now. The buyers need the approval from the Russian administration and Mondi shareholders will also have to vote on the deal (but considering there is no real viable plan-B, I assume shareholders will vote in favor of the agreement). The agreement has a long stop date of May 12 th , and after this date both parties can just terminate the agreement without repercussions. I don’t think this will happen as the buyer is acquiring the asset at just 2.5 times EBITDA and less than 5 times earnings (as the Russian operations generated about 490M EUR in EBITDA in 2022 and 266M EUR in net income) so there’s plenty of incentive for the buyer to push forward with this transaction. And from Mondi’s perspective, it could try to find another buyer but then the process just starts again from day 1.

{kind=link}

Both parties are probably quite committed to the deal, but the Russian buyer is getting a steal at 2.5 times the 2022 EBITDA and just 3.5 times the 2021 EBITDA.

Investment thesis

It is a pity Mondi is selling its Russian operations as that division has been very profitable but unless the war ends next month I’m afraid keeping the asset isn’t an option Mondi is considering.

I’m not expecting much from Mondi this year but it is clear the company is positioning itself for 2025 and beyond as that’s the year several new growth initiatives will come online. The current yield of approximately 4.4% is attractive and if the Russian deal closes, Mondi has made it very clear all of the proceeds will be returned to the shareholders with a special dividend being the most straightforward option.

I have waited long before going long on Mondi, but I will likely initiate a long position in the next few weeks with an anticipated investment horizon of 3-5 years.

For further details see:

Mondi: Expect A 15% Special Dividend Upon The Sale Of The Russian Operations