MONDF - Mondi: Strong Financial Performance To Price In

Summary

- Mondi delivered a solid set of numbers in Q4 and FY 2022. The company managed excellent operational performances in a challenging business environment.

- Lower debt and higher FCF generation.

- DPS was increased by 8%. Again, Mondi is a clear buy at today's value.

Here at the Lab, we do have a good grip on paper companies. Within our universe coverage, we closely follow International Paper and WestRock and monitor Smurfit Kappa Group plc. In 2020, during the COVID-19 crisis, our internal team published a detailed analysis of how Mondi ( OTCPK:MONDY ) was very Well Positioned to navigate short-term turbulences, and we also emphasized how Ecommerce growth And headwind from Infrastructure were positive key catalysts to our long-term thesis. Despite that, at the stock price level, the company did not perform in line with our expectations, and today, taking into consideration the results just released, we are revising our buy rating.

{kind=link}

Given the fact that our last analysis was published almost two years ago, we can clearly say that Mondi is now a better and safer company. Why?

- In August 2022, Mondi signed an agreement to dispose of its most significant Russian facility to Augment Investments. The transaction is still waiting for regulatory approval; however, the total market value is approximately €1.2 billion (RUB 95 billion). More important to note is the fact that the implied EV/EBITDA was almost a 10x multiple and there was no balance sheet impairment. In detail, the Russian net asset was valued at €1.2 billion. In addition, in December 2022, the company also confirmed an agreement to sell its 3 Russian packaging converting facilities to the Gotek Group for a value of approximately €20 million (RUB 1.6 billion);

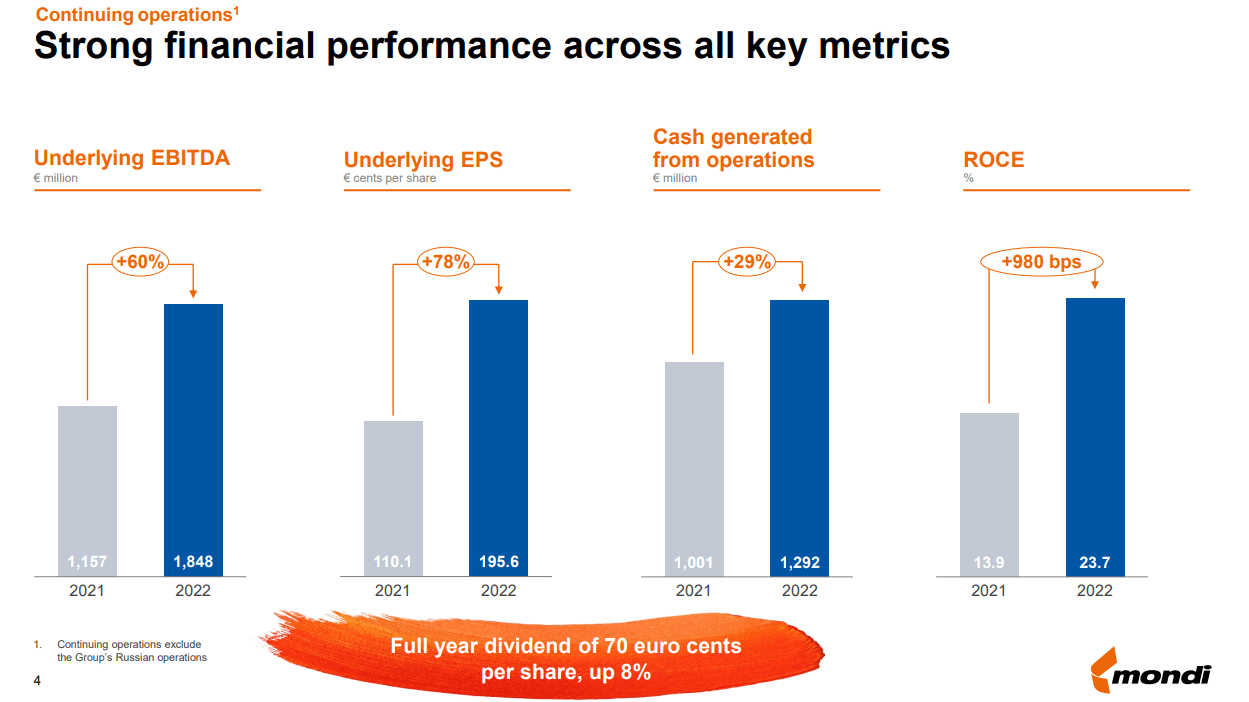

- Going to the P&L analysis, the company's EBITDA reached €1.8 billion and was up by 60% compared to the 2021 numbers at €1.1 billion). EBITDA margin reached 20.8% versus 2021 at 16.6%. Cross-checking Visible Alpha consensus, equity research analysts were forecasting an EBITDA of €1.8 billion so it ended up in line with Wall Street indications. However, looking at the specifics, the company's EBITDA was moderately in line with consensus but this number includes a positive €100 million non-cash forestry gain (Fig 1);

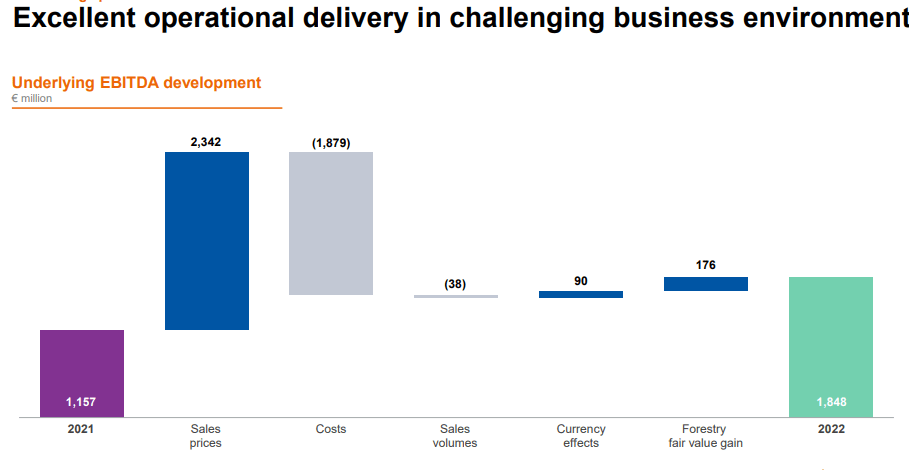

- The company was able to increase its selling price which more than compensates the higher yearly input costs recorded. Softer demand and inflationary cost pressures led to margin compression in 2022 second half. This was mainly due to energy cost evolution as well as slightly higher maintenance (€50 million vs. €40 million in H1) with a Fiscal Year EBITDA impact of €90 million compared to the €140 million reached in H2 (Fig 2);

- Still related to the margins, it is important to mention that the company generates most of its energy requirements thanks to biomass sources (almost 80%), thereby partially offsetting the energy cost impacts;

- Cash flow from operations reached €1.29 billion and was by 29% versus the 2021 account;

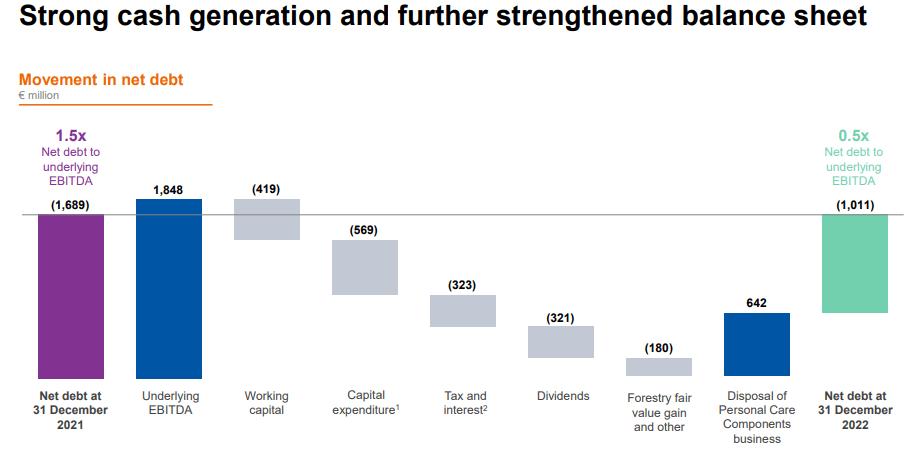

- For the above points, Mondi is now safer thanks to a solid balance sheet with leverage Net debt/EBITDA at 0.5x (it was 1.5x in 2021). Net debt declined by more than €650 million (Fig 3);

- If approved, Mondi will record another dividend hike at plus 8% compared to the consensus estimate of +7%. In number, the board has recommended a final DPS of €70 cents versus the €65 cents paid in 2021 (Fig 1).

{kind=link}

(Fig 1)

{kind=link}

(Fig 2)

{kind=link}

(Fig 3)

Risks

There are many risks including 1) Euro to GBP exchange rate evolution, 2) lower economic growth, 3) lower demand for Mondi's packaging products, especially in construction, and 4) office paper division which is linked to white-collar job evolution.

Conclusion and Valuation

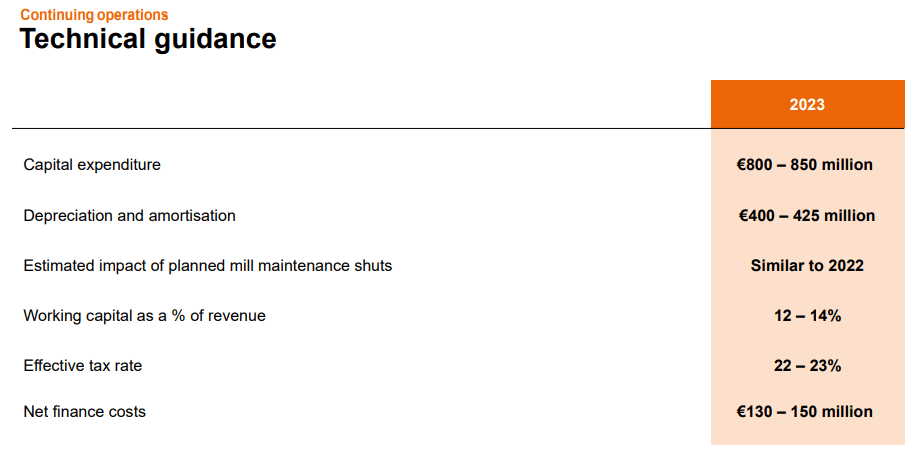

Lower debt, higher FCF generation, and a return on capital employed of more than 20%. As usual, there were not many details about the 2023 outlook and the regulatory process for the Russian sale assets is still ongoing. Aside from the MICRO risks components, we expect geopolitical and macro uncertainties. In particular, we are assuming near-term price pressure and a slowdown in volumes. The latter is likely due to an element of inventory destocking. Even if some costs have eased, others such as the wood costs remain at a high level. Our 2023 assumption of planned maintenance will be a €90 million deduction at the EBITDA level. As usual for paper companies, we derive the company's valuation using the average of the two following methodologies:

- A 7.0x EV/EBITDA on our 12-month forward estimates;

- A DCF valuation with a 9.6% discount rate and a terminal growth rate of 1.5%.

For the above reason, our Mondi target price is set at 1900p per share (versus the current trading at 1400p per share). This is derived from Mondi continuing operations and includes the distribution of Russian disposal proceeds. Mare Evidence Lab's target price is based on a € to GBP exchange rate of 1.15.

{kind=link}

For further details see:

Mondi: Strong Financial Performance To Price In