MNTK - Montauk Renewables: New Reactors Announced Production Increases And Cheap

2023-12-25 07:30:07 ET

Summary

- Montauk Renewables is a renewable energy company specializing in the recovery and processing of biogas from landfills and other non-fossil sources.

- The company has a strong operating portfolio with 12 RNG projects and three Renewable Electricity projects across six states.

- Recent earnings were in line with expectations, and the company's balance sheet appears stable, with sufficient resources for future opportunities.

Montauk Renewables, Inc. (MNTK) recently delivered EPS in line with expectations, and management continues to report quarterly net income growth. In my view, the recent announcement about new reactors and production increase from 2026 make MNTK a buy. Yes, I did find several risks coming from changes in energy prices, new regulatory standards for renewable energy, and rapid technical changes. However, even considering the risks, MNTK does look quite undervalued.

Montauk Renewables

Montauk Renewables is a renewable energy company specializing in the recovery and processing of biogas from landfills and other non-fossil sources for beneficial use as a substitute for fossil fuels. It develops, owns, and operates Renewable Natural Gas or RNG projects, using proven technologies that supply renewable fuel to the transportation and electric power sectors.

It is one of the largest RNG producers in the United States, with more than 30 years of experience in the industry. It has established an operating portfolio with 12 RNG projects and three Renewable Electricity projects through self-development, partnerships, and acquisitions, spanning six states.

The company's primary customers for RNG sales include large owners or long-term operators of landfills and livestock farms as well as local utilities and large refineries in the natural gas sector. In relation to Renewable Electricity, its typical customers are municipal electricity utilities or privately owned utilities.

The revenue Montauk receives from the sale of renewable energy consists of two main components. The first component is revenue derived from the commodity value of natural gas or electricity generated, which it sells through a variety of fixed-term agreements. The second component comes from the incentive programs granted to the production of Renewable Natural Gas and Renewable Electricity provided by the United States.

The company identifies stable sources of biogas feedstocks and secures long-term supply rights. It designs, builds, owns, and operates facilities that convert biogas to RNG or use the processed biogas to produce Renewable Electricity. The company establishes agreements with transportation companies and other types of companies that prioritize the consumption of renewable energy. Electricity sales agreements are established on a long-term basis with reputable counterparties, typically through a fixed price with scales.

Recent Earnings Were In Line With Expectations, With Less Operating Expenses

With the company delivering EPS in line with expectations, close to $0.09, and quarterly revenue of about $55.69 million, I do not think the market is paying a lot of attention to Montauk Renewables. The company is trading at multi-year lows.

Source: SA

Source: SA

With that about the recent changes in the stock price, I believe that the numbers recently delivered by Montauk Renewables were very beneficial. The company noted decreasing quarterly operating expenses y/y as well as increasing quarterly net income growth.

Source: 10-Q

Balance Sheet

Montauk Renewables reports a balance sheet with little working capital needs, a significant amount of cash, and some debt that is used to finance new property and equipment. Given the recent increase in book value, increases in property and equipment, and the total amount of debt, it seems that there are a few shareholders that are investing a meaningful amount of dollars to increase the company's capacity.

Source: Ycharts

More in particular, as of September 30, 2023, Montauk Renewables reported cash and cash equivalents of about $73 million, accounts and other receivables worth $18 million, and total current assets worth $107 million. The current ratio is larger than 3x, so I am not really concerned about the total amount of liquidity.

Property, plant, and equipment stands at close to $205 million, with goodwill and intangible assets worth $15 million, deferred tax assets of $2 million, and total assets worth $345 million. The asset/liability ratio is close to 3x, so I would say that the balance sheet appears quite stable.

Source: 10-Q

With accounts payable close to $6 million and accrued liabilities of about $15 million, current portion of long-term debt stands at about $7 million, with long-term debt worth $57 million. The company also reported asset retirement obligations worth $5 million, which I did not include for the calculation of the net debt and total liabilities of $102 million. Given the FCF projections by other investors and the current EBITDA levels, I am not concerned about the total amount of debt.

Source: 10-Q

Debt Agreements, Interest Rate, And Cost Of Capital Assumed

I am not concerned about the total amount of debt, however I will be running a discounted cash flow model. I believe that studying the cost of debt and cost of capital would help in the assessment of the WACC.

In the past, I saw management signing debt agreements with interest rates ranging from 4% to 2%. However, more recently, the company noted interest rates close to 6%. With this in mind, I assume that a cost of capital close to 2% and 7% would make sense.

The term loan amortizes in quarterly installments of $2,000 through December 2024, quarterly installments of $3,000 from 2025 through the maturity, with a final payment of $32,000, of December 21, 2026 with an interest rate of 4.12% and 2.91% at December 31, 2022 and 2021, respectively. The revolving and term loans under the Amended Credit Agreement bear interest at the BSBY Margin or Base Rate Margin based on our Total Leverage Ratio (in each case, as those terms are defined in the Amended Credit Agreement). Source: 10-k

Borrowings of the term loans and revolving credit facility bear interest at the Bloomberg Short-Term Bank Yield Index Rate plus an applicable margin. Interest rates as of September 30, 2023 and December 31, 2022 were 6.38% and 4.12%, respectively. Source: 10-Q

Under My Financial Model, I Assumed That New RNG Demand, New Value-added Services, And Further Diversification Of Activities Could Bring FCF Growth

In my view, the business strategy is centered on three priority areas. The first is to continue diversification in the range of agricultural raw materials used for RNG production. In this sense, investment in third-party technology is also considered to increase productive performance.

On the other hand, Montauk considers the need to optimize assets and its portfolio of existing projects as well as to develop new projects as appropriate. In particular, it is proposed to detect cases in which it is possible to convert renewable electricity demand into RNG demand.

Ultimately, it is considered beneficial to offer value-added services. This is what the company has done throughout its history as it has always focused on the comprehensive development of the production process considering engineering, construction, management, operation, and supervision of human resources.

Montauk Renewables Promised New Revenue Generating Activities Beginning In 2025 And New Reactors In 2024.

I believe that the most minimal meaningful communication made recently is the new addition of seven new reactors which will take place in 2024. It is also worth considering that revenue generating activities are also expected to take place from 2025. With all this in mind, I believe that we could see an accelerating net sales from 2024 and 2025 and free cash flow growth in these years.

Source: Investors Presentation

{kind=link}

The company also made a significant number of promises with respect to increases in annual production to begin in 2026. In two years, management noted that production could reach 45 to 50 thousand MWh equivalents.

Source: Investors Presentation

{kind=link}

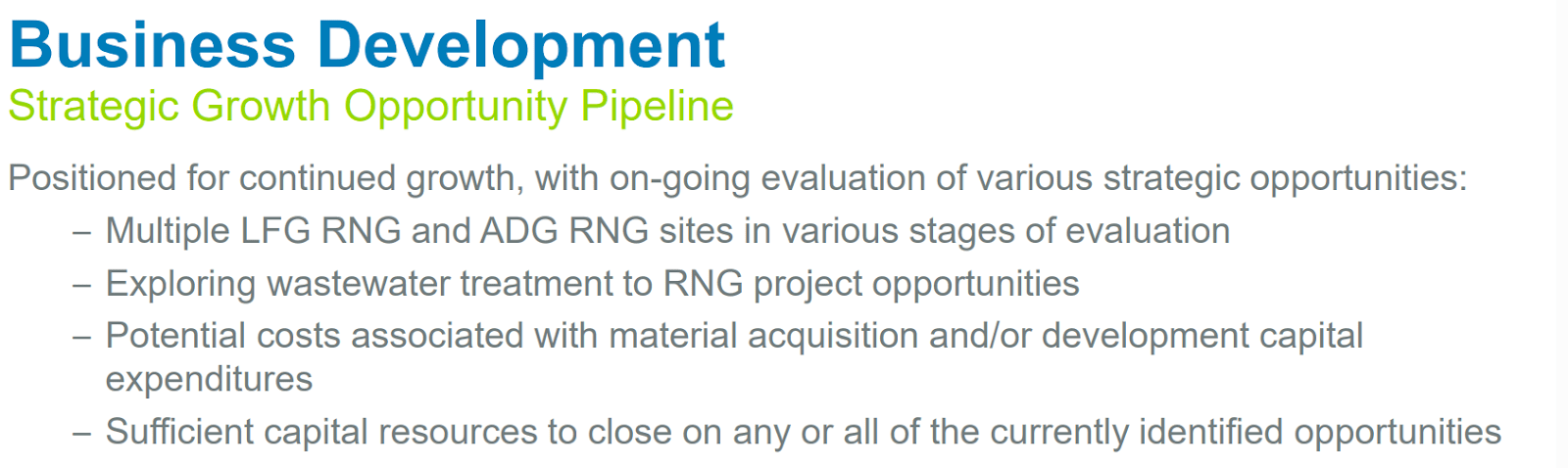

Montauk Renewables Appears To Have Sufficient Resources And Several Strategic Opportunities, Which May Be Announced In The Future.

Given the current state of the balance sheet and the total amount of cash accumulated, it is fair to say that the company is well equipped to consider new opportunities. In the last presentation to investors, the company provided a list of potential projects that included new LFG RNG and ADG RNG sites, water treatments projects, and other related acquisitions. In my view, any increase in new capacity will most likely lead to increases in FCF expectations. As a result, we may see new investors interested in the company's stock.

Source: Investors Presentation

{kind=link}

My Expectations Include Conservative Net Income Growth And FCF Growth

My financial expectations are mainly based on the expectations of other analysts, who recently delivered beneficial EPS revisions and my own assumptions. I believe that my figures are very conservative.

Source: SA

2031 net income stands at close to $156 million, with 2031 depreciation and amortization of $12 million, provision for deferred income taxes worth $57 million, and 2031 stock-based compensation close to $25 million.

Besides, with gain on property insurance proceeds close to $4 million, derivative mark-to-market adjustments and settlements of about -$5 million, and changes in accounts payable and other accrued expenses of about $41 million, 2031 CFO would be close to $281 million. Also, with 2031 capex of -$58 million, 2031 FCF would be about $224 million.

Source: Author's Work

Considering a FCF of about $74 million and $224 million from 2023 to 2031, a WACC between 2% and 7%, and EV/FCF of 5x-10x, I obtained an implied valuation without debt of $1.5-$3 billion. With a WACC of 4%-5% and EV/FCF of 7x, the implied valuation would be close to $2.2-$2.4 billion.

Note that my exit multiple appears to be close to median Price/Cash Flow reported in the sector of 7x. As mentioned earlier, I believe that my assumptions are quite conservative.

Source: Author's Work

Dividing by the share count, I obtained a valuation of close to $10-$18 per share, but the median valuation resulted in close to $12-$14 per share.

Source: Author's Work

Finally, the internal rate of return would include a maximum valuation of 12% and a median IRR of 4.7%-7%. With these figures, I would say that there is a certain undervaluation.

Source: Author's Work

Competition

Competition in the renewable energy business ranges from other project developers to service or equipment providers, but the main competition comes from other companies or solutions seeking to access biogas from waste.

The biogas market is highly fragmented, but Montauk maintains that its size compared to many other similar companies as well as its capital structure put it in a strong position to compete for new project development opportunities or acquisitions of existing projects.

The company's main competitors are Archaea Energy, Morrow Renewables, OPAL Fuels (OPAL), U.S. Gain, Brightmark, and AMP Energy as well as companies with biogas-to-energy facilities as a segment or subsidiary of their operations, including DTE and Ameresco. Additionally, certain landfill operators, such as Waste Management (WM), have also chosen to selectively pursue biogas conversion projects at their sites. Finally, Republic has partnered with Archaea Energy to develop certain of its locations.

Risks

The concentration of revenues in a few major customers and the geographic concentration of its projects expose the company to greater production risks. It is also possible that several landfill owners may seek to install their own biogas production projects on their sites, which would reduce the number of opportunities for new project development.

Furthermore, the achievement of financial objectives is tied to the projected demand for renewable energy. On the other hand, the possibility of a reduction or elimination of government economic incentives for the renewable energy market must be considered.

The company is also exposed to commodity prices, regulatory standards for renewable energy, and the rapid technical changes that occur in relation to the renewable energy production process.

My Takeaway

With growing quarterly net income y/y and beneficial EPS revisions for the new quarter, Montauk Renewables also announced new reactors, capacity increases, and production increase from 2026. I do not think that market participants had a look at the expectations of management and potential FCF generation in the coming years. All put together, in my view, makes Montauk Renewables a buy. Yes, there are obvious risks from changes in the price of energy and natural gas, lower capacity expansion than expected, or changes in environmental laws and regulations. With that, I think that Montauk Renewables remains undervalued.

For further details see:

Montauk Renewables: New Reactors Announced, Production Increases, And Cheap