MPSYF - MorphoSys: Still Positive Moving Into Pelabresib Data (Maintaining Buy Rating)

2023-11-19 18:59:11 ET

Summary

- MorphoSys reported Q3 2023 earnings with underperformance in Monjuvi sales due to competition and market saturation.

- There is optimism surrounding the upcoming data readout for Pelabresib, a promising myelofibrosis treatment.

- The company has a healthy cash runway and potential for market expansion with Pelabresib's success.

- We maintain a non-consensus buy rating.

Summary of Q3 2023 Earnings and Thesis update

We previously upgraded MorphoSys to a buy rating due to our enthusiasm around the company's late-stage candidate Pelabresib; this article is a follow-up article to update readers on the new information released after the recent Q3 2023 earnings call and the timeline around the clinical data readout (that can have a meaningful impact on the stock price).

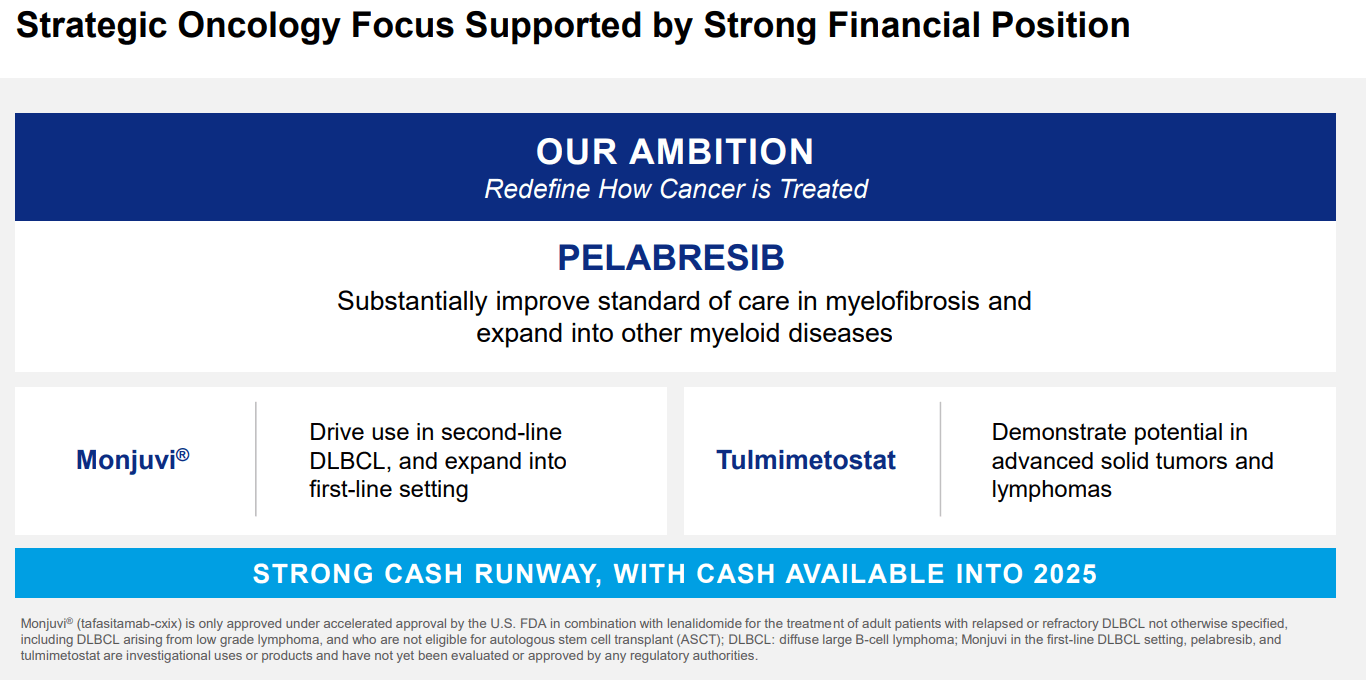

MorphoSys reported Q3 2023 results , revealing a slight underperformance in Monjuvi sales, which failed to meet the optimistic market consensus. Despite being in line with the company's guidance, sales remained subdued, attributed to intensified competition and market saturation. The gross margin for Monjuvi also saw a decline to approximately 75%, reflecting one-time write-offs. On the upside, R&D and SG&A expenses were consistent with forecasts, showcasing efficient cost management. Notably, MorphoSys has maintained a healthy cash runway (described in more detail below), vital for its ongoing research and upcoming trial milestones.

Positive Outlook on Pelabresib

Despite the lackluster performance of Monjuvi, there's a palpable optimism surrounding the imminent data readout for Pelabresib, MorphoSys's promising myelofibrosis treatment. The robust Phase 2 data and favorable feedback from physicians underscore the high likelihood of a successful Phase 3 outcome. However, concerns linger over the trial's endpoint design, with the total symptom score (TSS50) being a pivotal factor. The anticipation is building for the trial results, expected to be published at the ASH conference on December 10. We are cautiously optimistic and believe it is worth to keep an optioned size position moving into the data readout.

Company IR deck (Company IR Deck)

{kind=link}

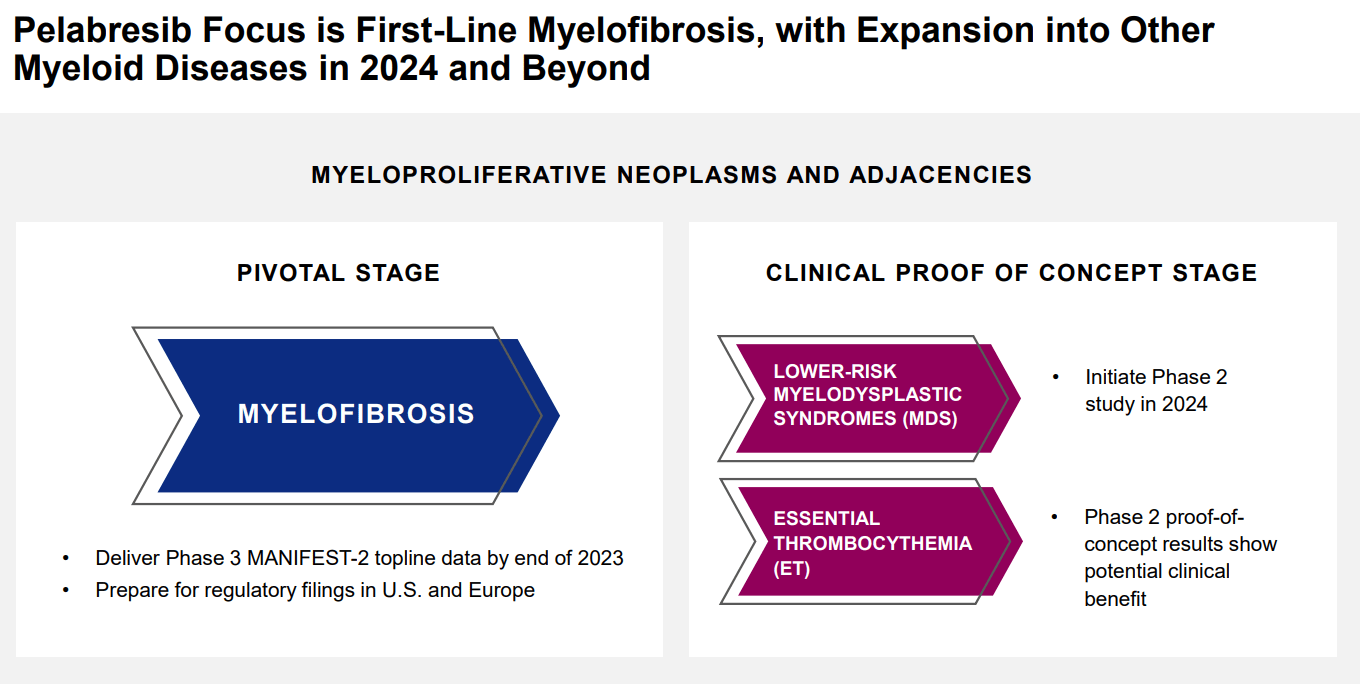

Pelabresib, known by its investigational code CPI-0610, is a small-molecule bromodomain and extraterminal ((BET)) domain inhibitor. As a targeted therapy, it aims to interfere with the reading of certain acetylation marks on histone proteins, thereby impacting gene expression. This mechanism of action is particularly relevant in myelofibrosis, where aberrant gene expression plays a role in disease pathology.

The Phase 2 clinical trial, known as the MANIFEST trial, explored the efficacy and safety of pelabresib in patients with myelofibrosis, particularly in combination with ruxolitinib, which is a standard treatment for myelofibrosis. This trial was designed to address the significant unmet medical need in this patient population, characterized by symptoms such as splenomegaly, cytopenias, and bone marrow fibrosis, all contributing to a reduced life expectancy??.

In the MANIFEST trial, a notable proportion of JAK inhibitor-naïve patients treated with the combination of pelabresib and ruxolitinib demonstrated a durable improvement in spleen volume, as evidenced by a 35% reduction from baseline (SVR35) sustained beyond 24 weeks. Additionally, this treatment regimen led to a significant reduction in symptom burden, with a considerable percentage of patients achieving at least a 50% reduction in their total symptom score (TSS50) from baseline. These clinical benefits were also accompanied by an improvement in bone marrow fibrosis in some patients, suggesting a potential disease-modifying effect??.

However, the treatment was not without side effects. Hematologic treatment-emergent adverse events were common, with thrombocytopenia and anemia being the most notable. Nonhematologic treatment-emergent adverse events included gastrointestinal symptoms like diarrhea, musculoskeletal pain, and respiratory tract infections, among others??.

Building upon the Phase 2 results, the Phase 3 MANIFEST-2 study is a global, double-blind, placebo-controlled trial evaluating the efficacy and safety of pelabresib in combination with ruxolitinib versus placebo and ruxolitinib in JAK inhibitor treatment-naïve myelofibrosis patients. This study aims to provide further evidence on the drug's impact on disease symptoms and progression, with a focus on long-term outcomes and a larger patient population to validate the Phase 2 findings

Financials

The company ended Q3 2023 with cash of $733M, considering that the OPEX burn of the company is ~$55M (in Q3 23) and considering that the R&D expense decline after the completion of Pelabresib's late-stage trial, we see at least 2 years of cash runway even if Monjuvi's revenue stays flat. This aligns with the company's guidance.

{kind=link}

Valuation

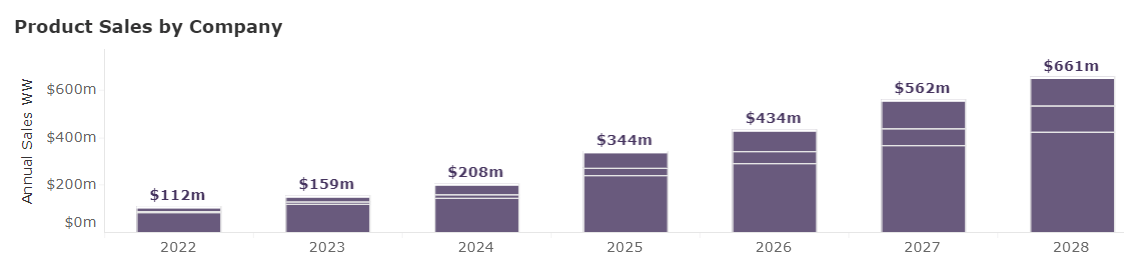

Considering that the street consensus (below) for Morphosys's 2028 peak sales is ~$660M, using a conservative peak sales multiple of x3, we get around $1.8Bn of enterprise value. Considering that the current enterprise value is $640m, we see ~x3 additional upside from the current valuation.

EVP street consensus (EVP consensus)

{kind=link}

Risk

MorphoSys, while pioneering in its field, is not without its risks. The company's heavy reliance on the success of Monjuvi and Pelabresib trials means any negative outcome could significantly impact its financial stability. Additionally, the looming maturity of the company's EUR 260 million convertible bonds in 2025 could strain its cash reserves in the event of an acquisition or if further research funding is required.

Conclusion

Our buy rating on MorphoSys remains steadfast, underpinned by the company's solid clinical advancements and the strategic significance of its pipeline. While the Q3 sales of Monjuvi were not as robust as hoped, the company's disciplined cost structure and cash management lay a strong foundation for its future endeavors. The potential market expansion with Pelabresib's success in myelofibrosis—a domain with a high unmet medical need—could significantly bolster MorphoSys's valuation and market position.

For further details see:

MorphoSys: Still Positive Moving Into Pelabresib Data (Maintaining Buy Rating)