AAIN - Mortgage REITs: High Yield Opportunity And Risk

2023-03-17 09:00:00 ET

Summary

- Mortgage REITs have been slammed by the fallout of the ongoing regional banking crisis amid a resurgence of interest rate volatility and credit concerns, erasing their once-robust gains for 2023.

- Commercial mREITs' exposure to the troubled office sector has come into focus following a wave of mega-sized loan defaults from over-levered private owners. We examine these REITs' sector-by-sector exposure.

- For Residential mREITs, Book Values remain in decent-shape as MBS spread-widening has been more-than-offset by a decline in benchmark rates, but sharp changes in rates heighten unknown hedge-related risks.

- Despite paying average dividend yields in the low-teens, the majority of mREITs are still able to cover their dividends, but a half-dozen mREITs have trimmed payouts and we flag several more with looming cuts.

- Everything in Moderation: While most mREITs stand on relatively decent footing with enough earnings power to maintain their hearty dividend yields, sharp changes in rates in either direction can wreak havoc on mREITs that are caught over-levered or improperly hedged.

REIT Rankings: Mortgage REITs

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on March 15th.

{kind=link}

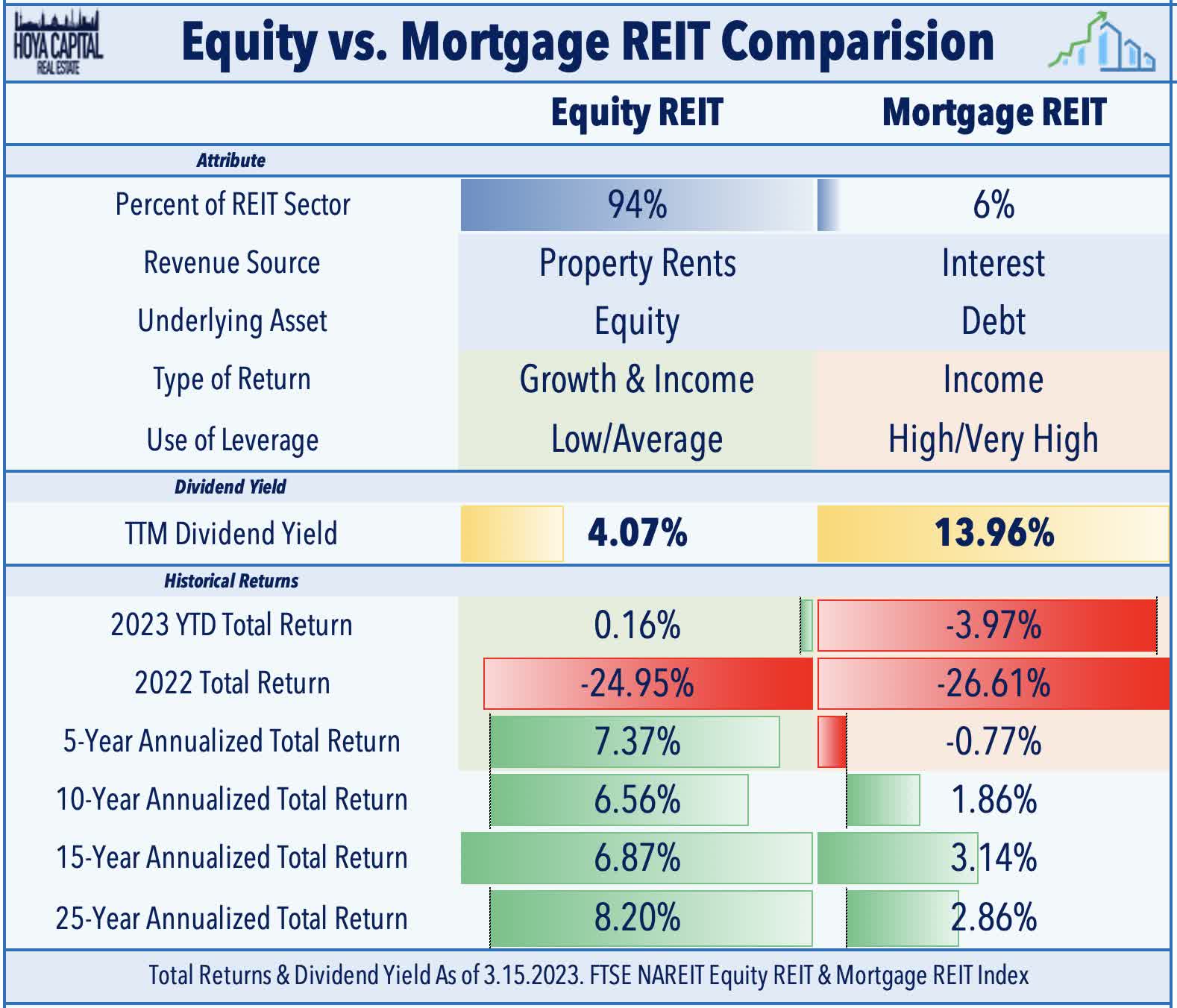

Best known for their hearty dividend yields that often breach double digits, Mortgage REITs - also called "mREITs" - comprise roughly 5% of the total REIT universe. Often viewed as a distinct asset class from equity REITs which own, operate, and collect rent on real estate properties, mortgage REITs function more like a lending bank by originating and investing in interest-bearing real estate debt instruments. mREITs have been slammed particularly by the fallout of the ongoing regional banking crisis amid a resurgence of interest rate volatility and credit concerns - erasing their once-robust gains for 2023. Everything in Moderation: While most mREITs stand on relatively decent footing with enough earnings power to maintain their hearty dividend yields, sharp changes in rates in either direction - along with sector-specific credit risk - can spell trouble for mREITs that are over-levered or improperly hedged.

{kind=link}

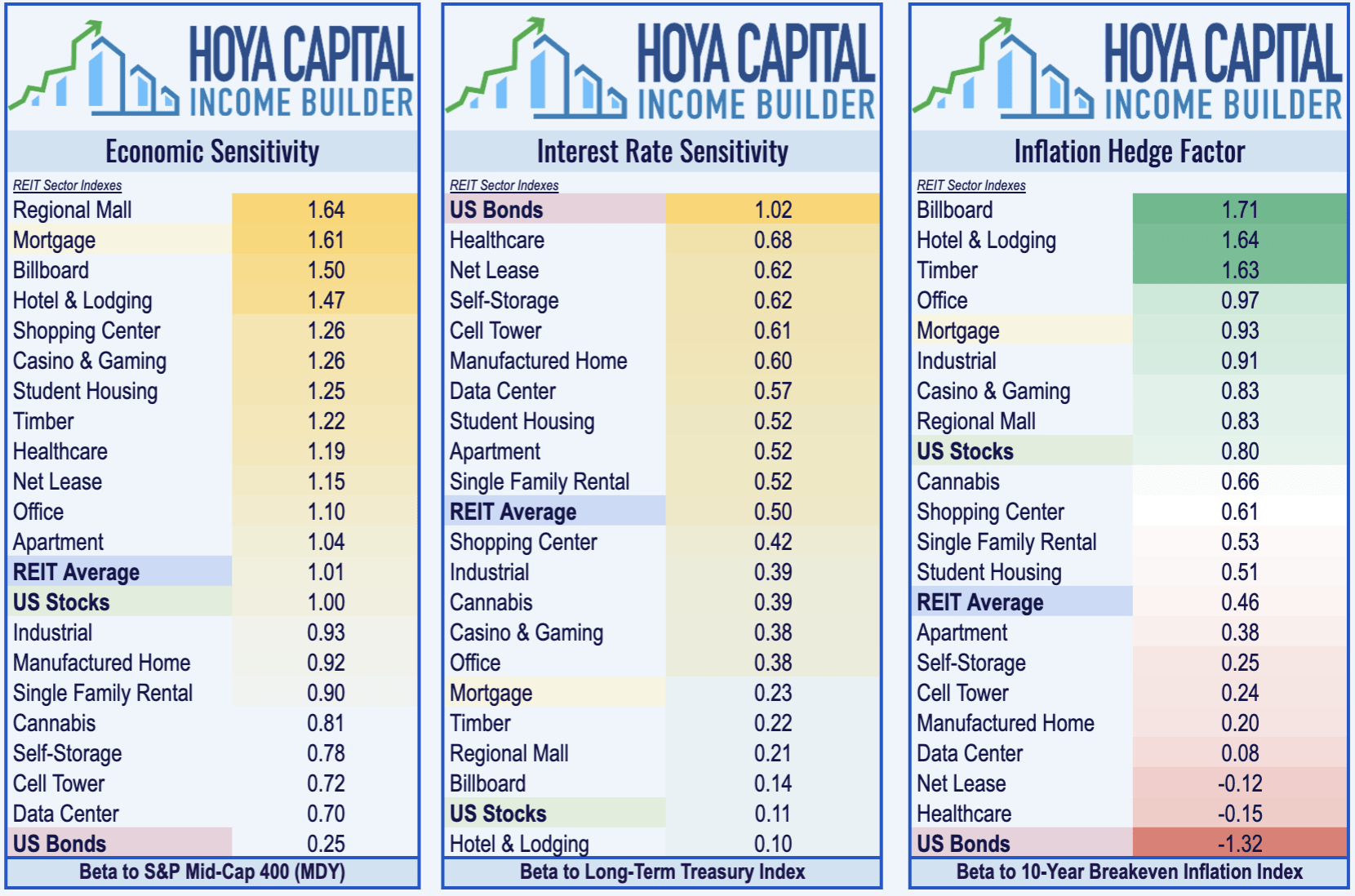

Despite their volatility over the past several years, mortgage REITs don't necessarily deserve their "ugly duckling" status within the REIT sector and we reiterate our view that maintaining a modest mREIT allocation to a balanced income-focused real estate portfolio can be a prudent strategy to hedge interest rate and inflation risk while adding immediate income. As illustrated through our Inflation Hedge Factor model, mortgage REITs provide some of the better inflation-hedging characteristics within the REIT sector and exhibit more muted interest rate sensitivity compared to their equity REIT peers.

{kind=link}

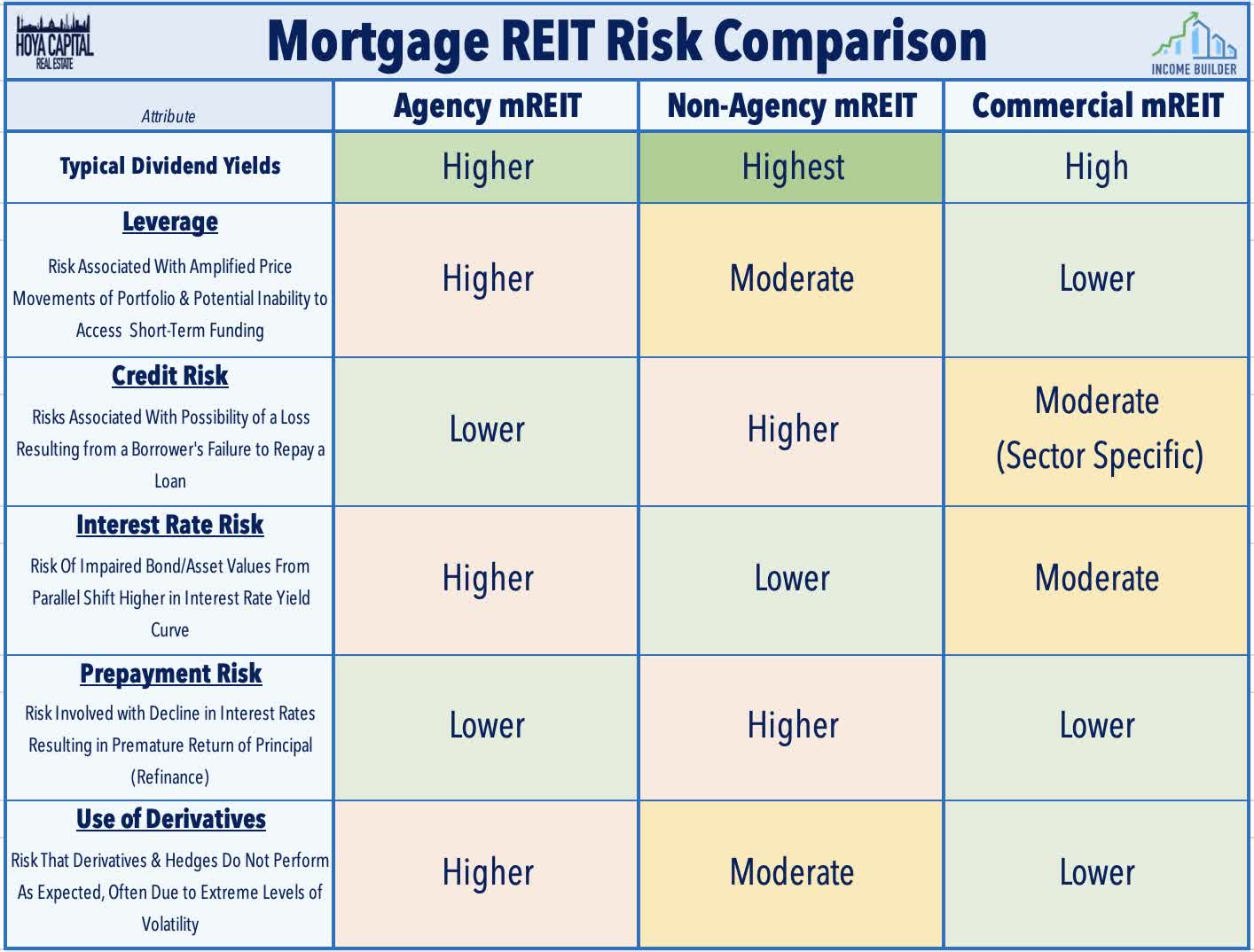

That said, it's important to keep in mind that mortgage REITs are not monolithic in their risk exposures. Mortgage REITs typically operate with a high degree of leverage to amplify investment spreads and often use short-term hedging instruments to manage interest rate and credit exposure, which makes each REIT rather unique in its end-exposure to certain macroeconomic environments. In general, similar to high-yield corporate credit, mortgage REITs tend to perform their best in "boring markets" - periods of lower interest rate and stock market volatility. Below, we define the five primary risk exposures faced by these different types of mortgage REITs: leverage risk, credit risk, interest rate risk, prepayment risk, and derivative risk.

{kind=link}

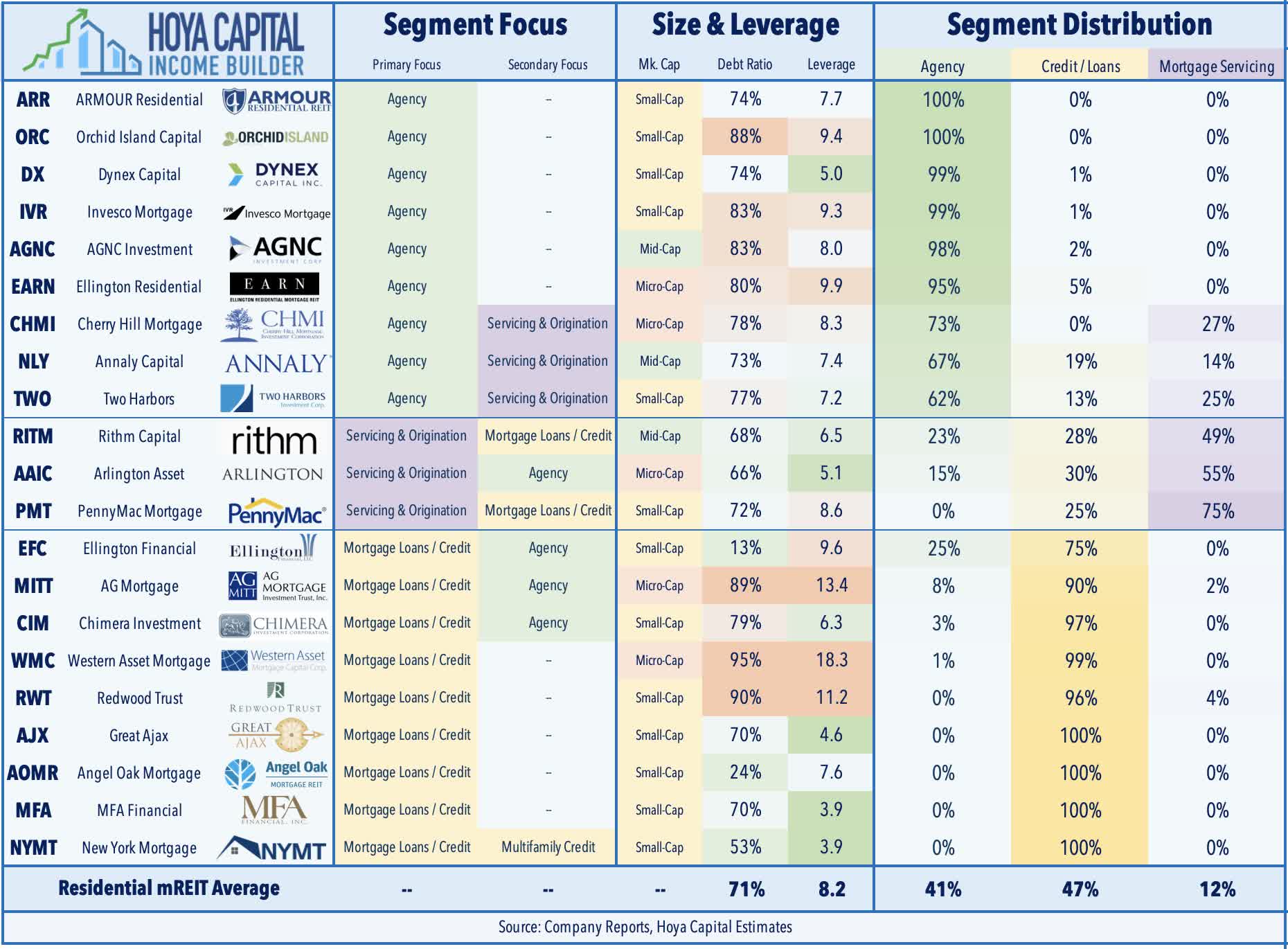

Residential Mortgage REIT Overview

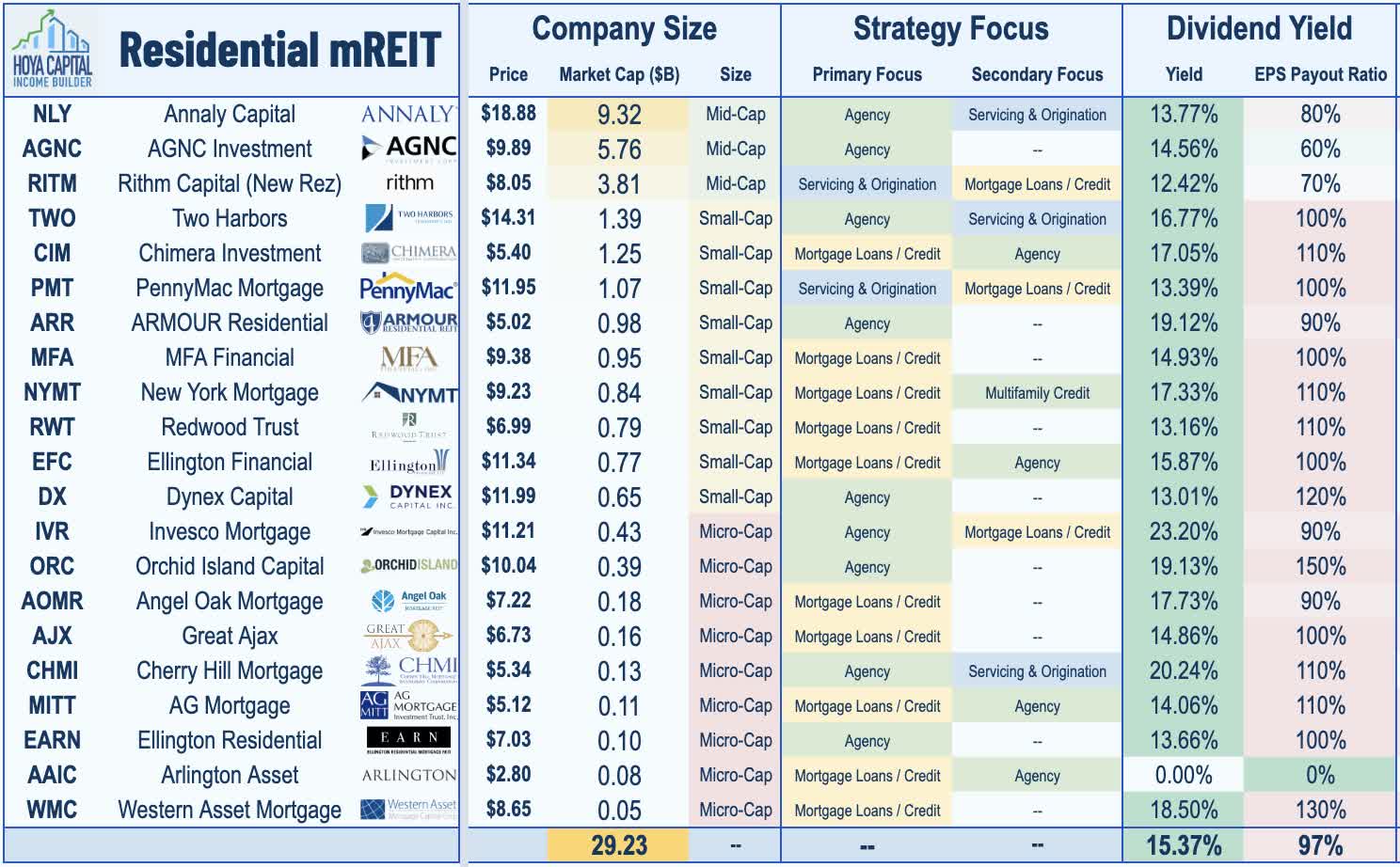

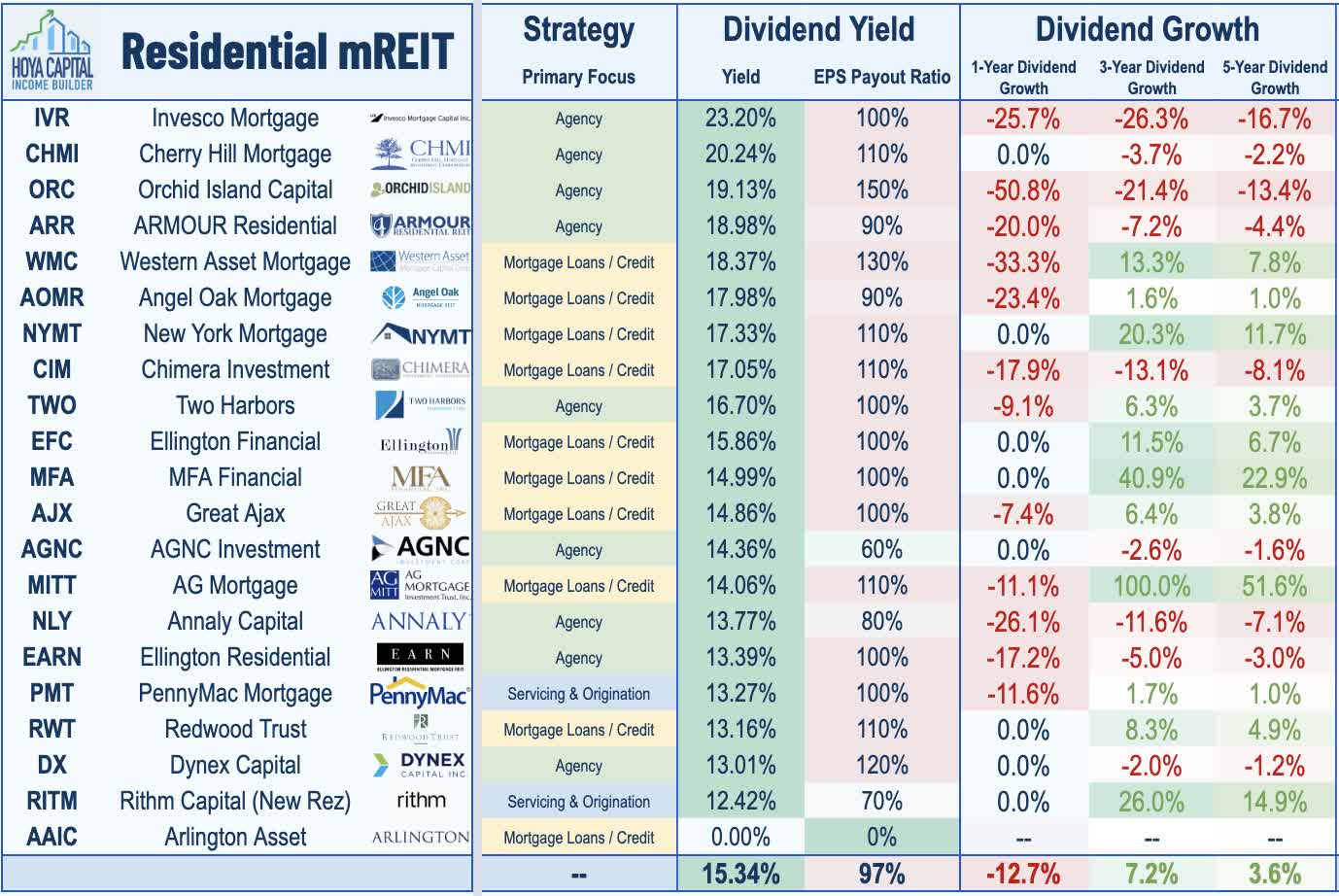

In the Hoya Capital Residential Mortgage REIT Index , we track the 21 exchange-listed residential mREITs, a sector that is comprised primarily of small and micro-cap REITs which pay dividend yields in the mid-to-high teens. Not unlike a traditional mortgage bank, Residential mREITs purchase or originate residential mortgages and mortgage-backed securities (“MBS”) and use leverage to enhance the investment spread between the effective lending rate and their cost of capital. As we'll discuss throughout this report, residential mREIT Book Values remain in decent shape amid the turmoil from the recent regional banking crisis as MBS spread-widening has been more-than-offset by a decline in benchmark rates, but sharp changes in interest rates heighten the hedge-related risk for some over-levered REITs.

{kind=link}

The sector can be further split into three sub-sectors: Agency mREITs - led by Annaly Capital ( NLY ) and AGNC Investment ( AGNC ) - invest primarily in agency mortgage-backed securities, or RMBS, which have their principal guaranteed by a Government-Sponsored Enterprise, or GSE, such as Fannie Mae, Freddie Mac, or Ginnie Mae, and thus bear minimal credit risk but tend to be more sensitive to changes in interest rates. Credit-Focused mREITs - led by Chimera ( CIM ), MFA Financial ( MFA ), and New York Mortgage ( NYMT ) - invest in RMBS and other types of residential credit that are not guaranteed by a GSE, including whole mortgage loans, which bear higher levels of credit risk but tend to be less sensitive to interest rates. Servicing/Origination mREITs - led by Rithm Capital ( RITM ) and PennyMac ( PMT ) - typically focus on non-traditional mortgage-related assets, including mortgage servicing rights (MSRs) and/or loan origination services.

{kind=link}

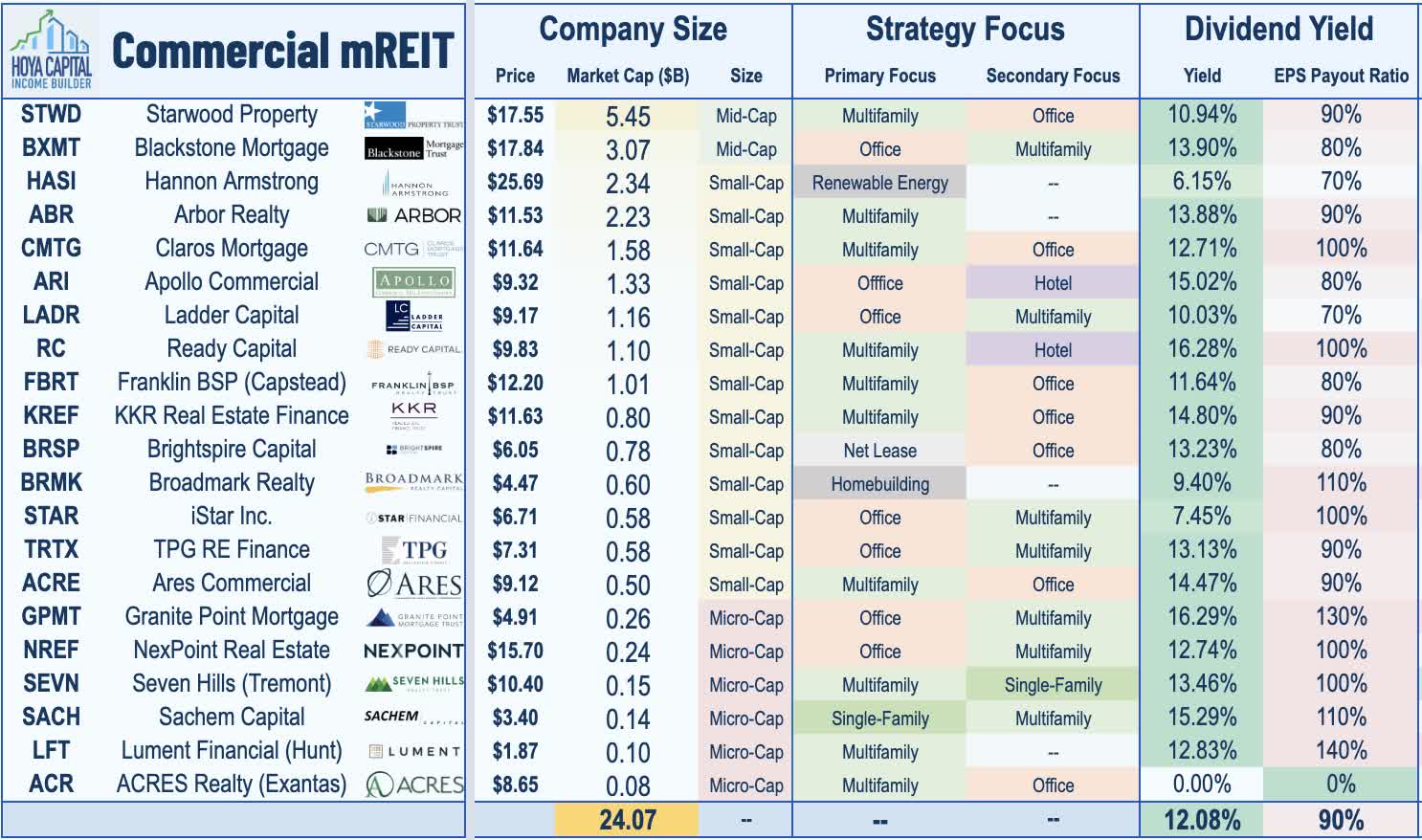

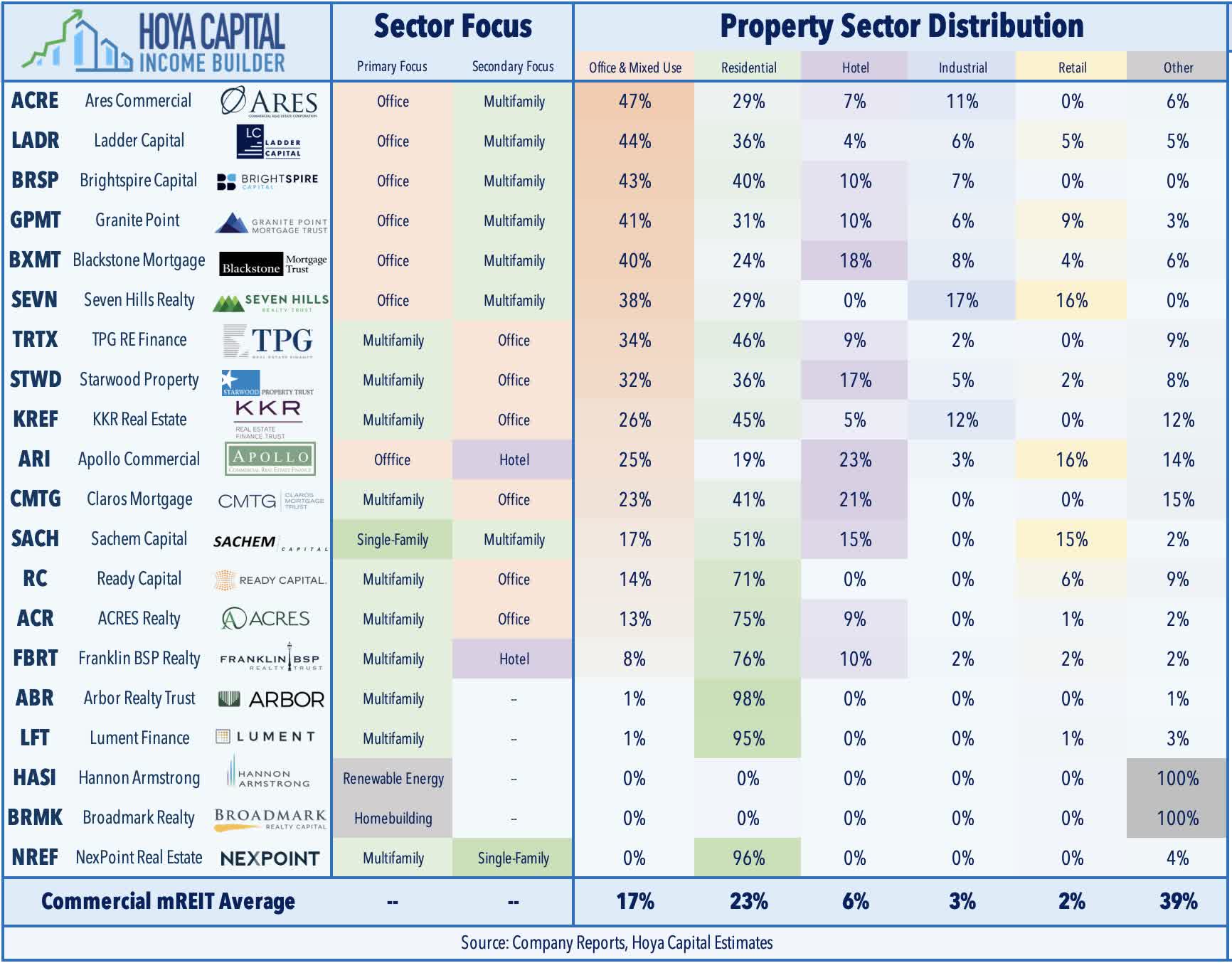

Commercial Mortgage REIT Overview

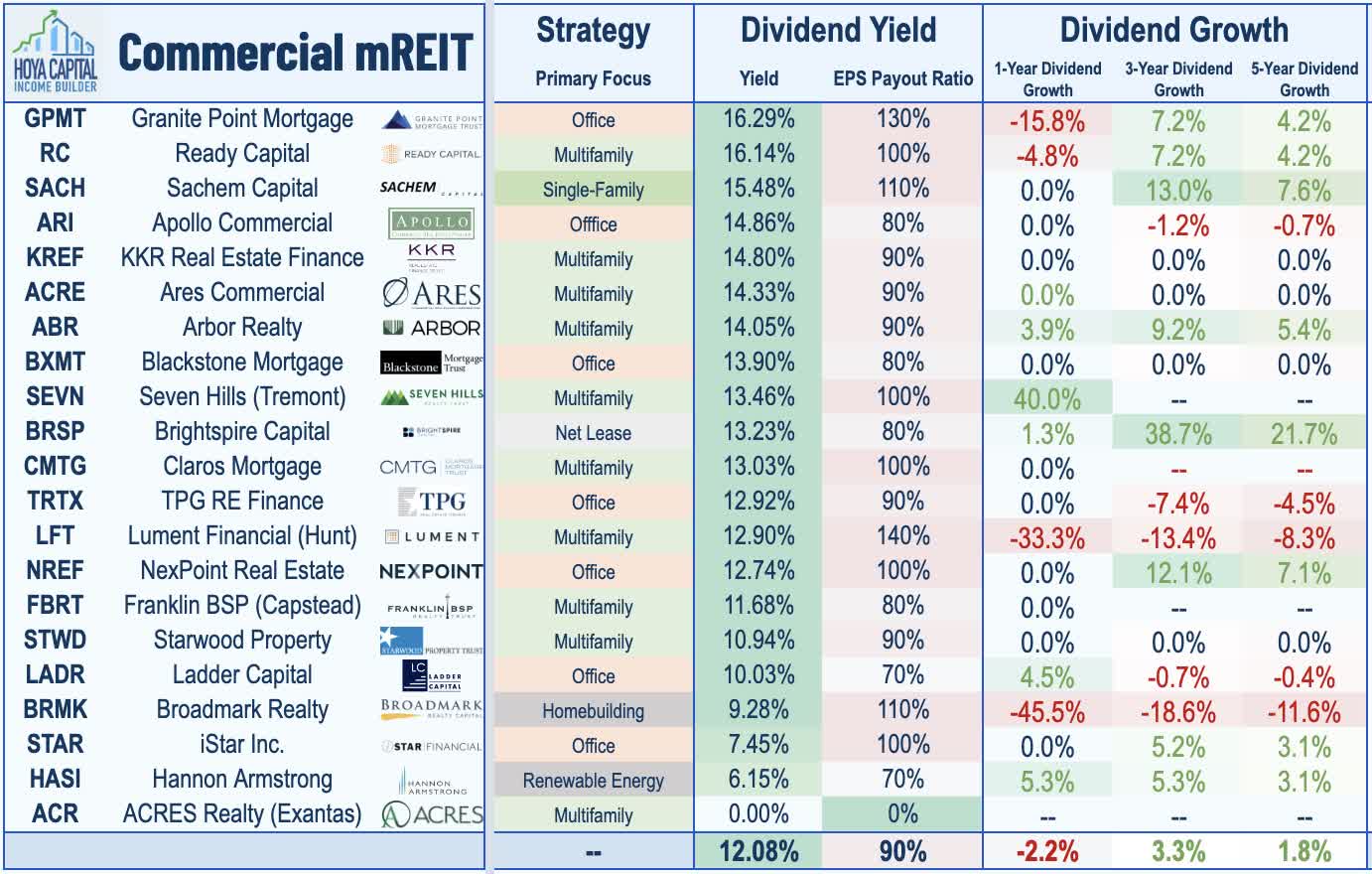

In the Hoya Capital Commercial Mortgage REIT Index , we track 21 exchange-listed commercial mREITs. Similar to equity REITs, commercial mREITs tend to focus on one or a small handful of property sectors, but tend to take on relatively lower levels of leverage compared to residential mREITs given the elevated credit risk compared to housing-backed loans. Like their counterparts on the residential side, the commercial mREIT is comprised primarily of small and micro-cap REITs, and pay dividend yields in the low-to-mid teens. The sector can be further segmented into two categories: pure Balance Sheet Lenders, which originate and purchase loans for their own balance sheet, and Conduit Lenders , which originate and purchase loans both to hold on their own balance sheet and also for the purposes of securitizing the loans into a CMBS or other vehicle. We track two additional mREITs AFC Gamma ( AFCG ) and Chicago Atlantic ( REFI ) in our Cannabis REIT report.

{kind=link}

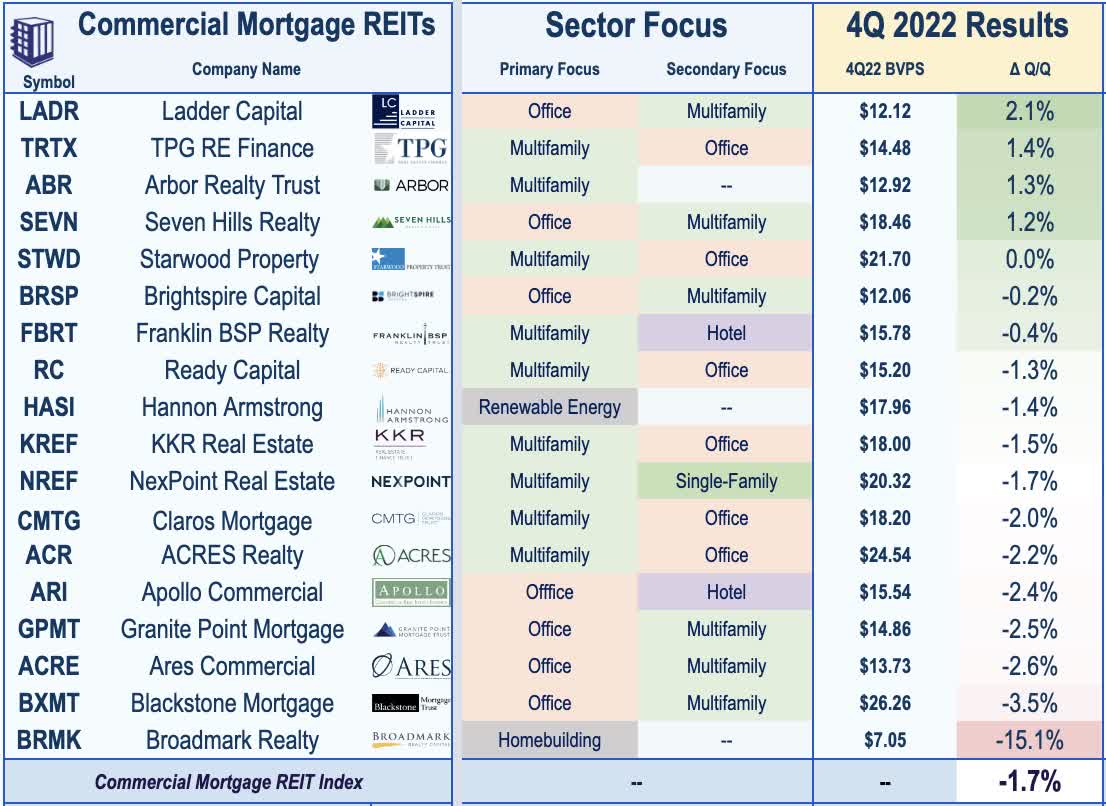

New to this report, we take a deeper dive into these commercial mREITs' property sector exposure in light of amplified credit concerns for the U.S. office sector, which has faced challenges from Work-From-Home headwinds. Over the past month, we've seen a handful of mega-sized loan defaults on office loans from PIMCO , Brookfield , and RXR . Last week, Fitch reported that 56% of new real estate delinquencies in February were in the office sector. As a whole, office assets represent less than 20% of commercial mREITs' property-level exposure, but a handful of names have outsized weight in the office sector, including Ares Commerical ( ACRE ), Ladder Capital ( LADR ), BrightSpire ( BRSP ) and Granite Point ( GPMT ) at more than 40% of their loan books.

{kind=link}

Mortgage REIT Performance & Earnings

Mortgage REITs endured punishing declines of 50-70% during the depths of the pandemic as the sharp plunge in interest rates wreaked havoc on mREITs that were caught over-levered and improperly hedged - triggering a cascading wave of forced selling that resulted in permanent Book Value declines for many mREITs - but similar signs of stress have been limited to a small number of highly-levered mREITs in the subsequent two years. Mortgage REIT performance was roughly even with their Equity REIT peers in 2022, with the iShares Mortgage REIT ETF ( REM ) and Vanguard Equity REIT ETF ( VNQ ) each lower by about 25% for the year. After jumping out to a strong start to 2023 with gains of nearly 20% that nearly closed the underperformance gap with their equity REIT peers, mREITs have fallen sharply over the past month and are now lower by about 5% so far in 2023.

Hoya Capital

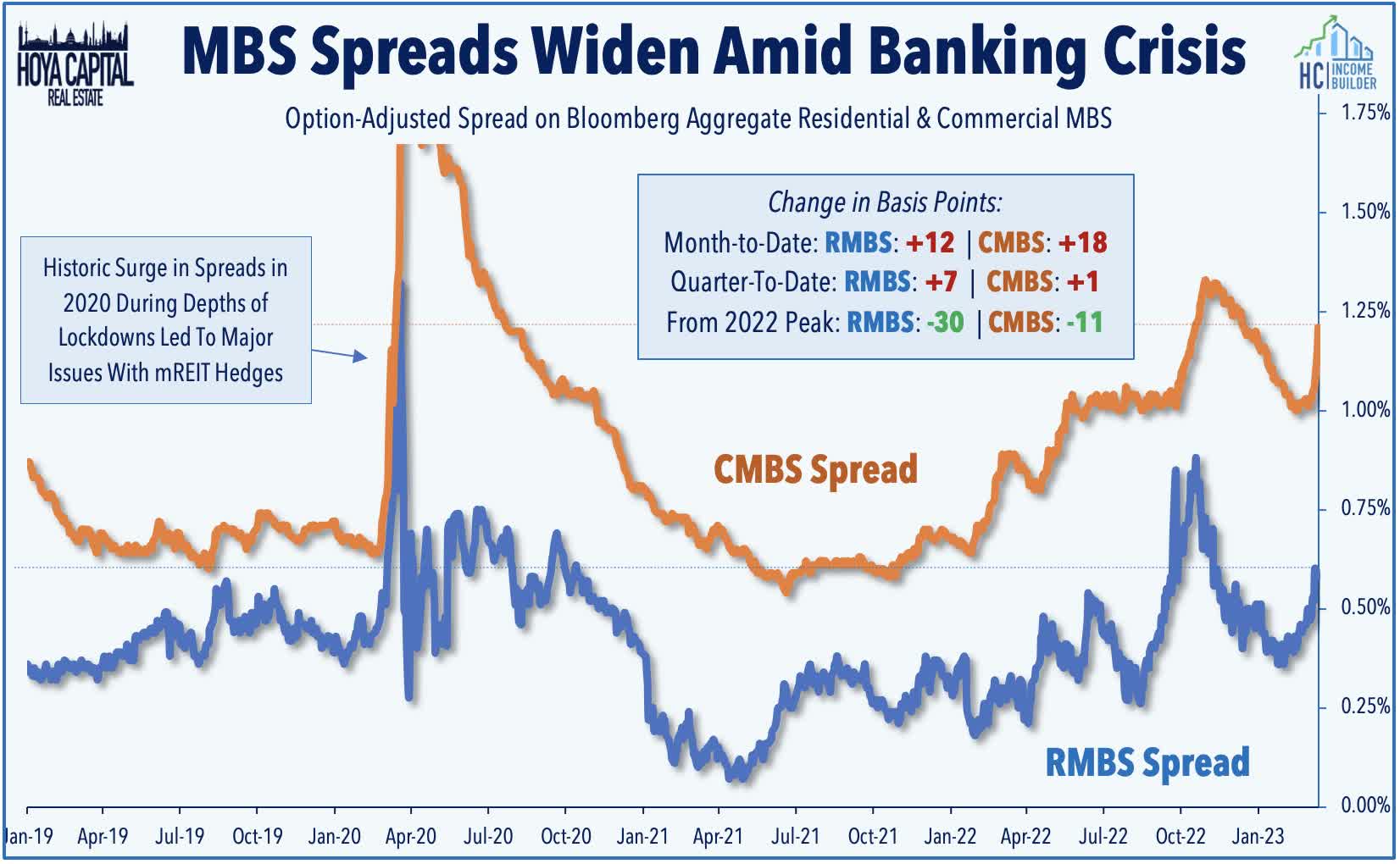

Renewed interest rate volatility sparked by the collapse of Silicon Valley Bank and Signature Bank - the second and third largest bank failures in U.S. history - has naturally revived concern that the mREIT sector could face a similar wave of distress as seen in the two prior financial crises - the Great Financial Crisis in 2008 and the COVID Crisis in 2020. These concerns appear overstated as underlying fundamentals in both the residential and commercial real estate industry remain on stable footing, albeit with some exceptions. Notably, the iShares MBS ETF ( MBB ) and the iShares CMBS ETF ( CMBS ) - the benchmarks tracking the un-levered performance of residential and commercial mortgage-backed bonds - have actually responded favorably to recent market developments as tailwinds from lower benchmark interest rates have more-than-offset the widening of MBS spreads while underlying delinquency rates entered this turmoil at historically-low levels.

{kind=link}

The compression of MBS spreads in late 2022 was a driving force behind a generally solid slate of fourth-quarter earnings results for residential mREITs, and while spreads have widened over the past month, the RMBS benchmark is only marginally (7 basis points) higher than the end of Q4. Ten residential mREITs reported an increase in Book Value Per Share ("BVPS") in Q4 led by the agency-focused mREITs, including AGNC Investment ( AGNC ), which reported an 8.4% bounce in its BVPS followed by Ellington Residential ( EARN ) and Two Harbors ( TWO ) at 8%. Results from credit-focused and servicing-oriented mREITs Rithm Capital ( RITM ) and PennyMac ( PMT ) were also solid, recording muted changes in its BVPS for a second-straight quarter. Most credit-focused mREITs reported a decline in BVPS following a strong rebound in Q3 amid a broader cooldown in the U.S. housing market.

{kind=link}

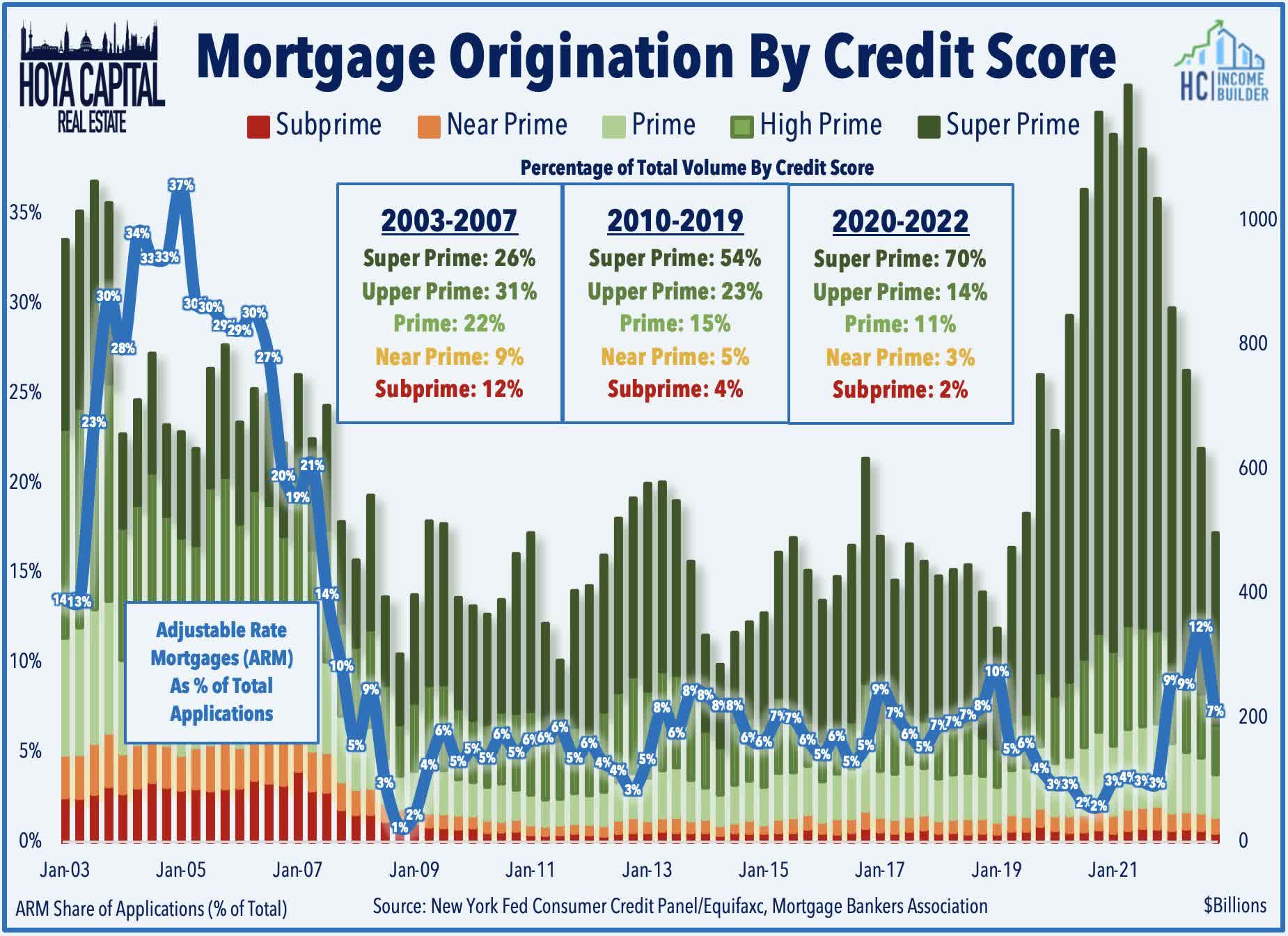

Looking more broadly at the macro environment, as the Federal Reserve intended , rising mortgage rates have indeed poured icy-cold water over the previously red-hot housing market in recent months. The recent cooldown has renewed the perennial "Bubble" calls from pundits , but fundamentals suggest that national housing markets are instead more likely to see a somewhat "boring" return to normalcy ahead, similar to 2018-2019 when rising mortgage rates resulted in a notable near-term slowdown in buying activity. Importantly, subprime loans and adjustable-rate mortgages - the dynamite that led to a cascading financial market collapse in 2008 - have been essentially non-existent throughout this cycle. Adjustable-rate mortgages - which would be most "at-risk" from the surge in rates have accounted for less than 5% of mortgages originated since 2009, down from nearly 30% at the peak in 2005.

{kind=link}

On the commercial mREIT side, the movement in BVPS has been more muted throughout the pandemic, but increased loan loss reserves - particularly in the office sector - offset tailwinds from these REITs' floating-rate loans. Commercial mREITs reported just a 6.5% decline in BVPS at the depths of the pandemic and most of the larger REITs have now recovered all of these declines. Commercial mREITs weren't facing the same "existential crisis" as their residential mREIT peers, but the sector's exposure to the hotel, office, and retail sectors dragged on performance early in the pandemic. Five REITs reported a sequential increase in BVPS in Q4, including Arbor Realty ( ABR ) and Starwood Property ( STWD ). Downside laggards this earnings season included many of the office-focused mREITs, including Granite Point ( GPMT ), Ares Commercial ( ACRE ), and Blackstone Mortgage ( BXMT ).

{kind=link}

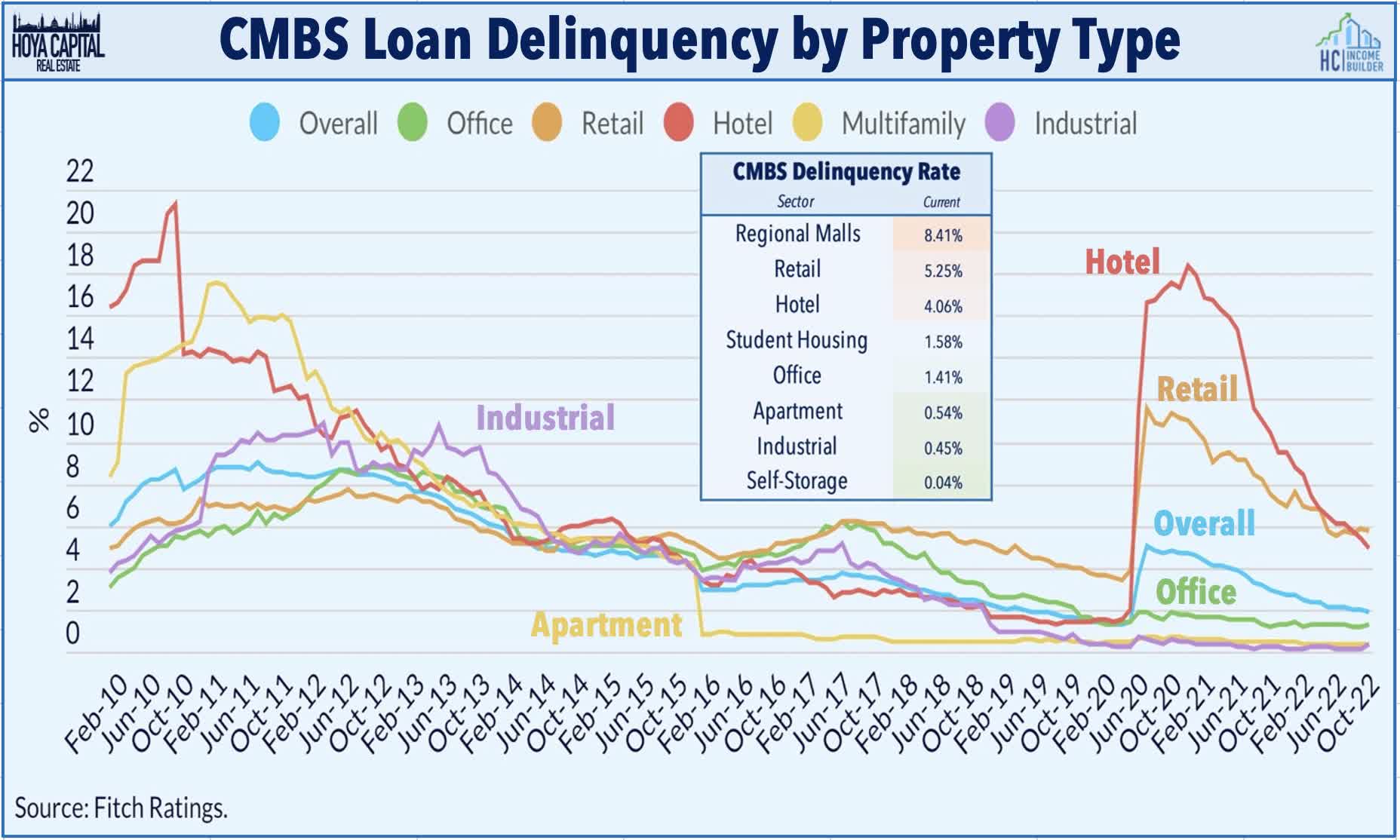

As discussed in our State of the REIT Nation report earlier this week, commercial real estate credit quality remains quite stable - and even strong - across all of the major property sectors outside of office and regional malls. Fitch reported last week that the overall U.S. CMBS delinquency rate decreased to 1.83% in February - well below the roughly 3% average from 2015-2018 and the 9% peak in 2011. Notably, over 90% of the new delinquencies in February were office (56%) and retail (35%). Even with the uptick, however, office delinquency rates stood at just 1.4% in February. Delinquency rates in the apartment sector have remained near all-time lows at roughly 0.5%, which roughly matches the industrial delinquency rate.

{kind=link}

Mortgage REIT Dividends Safer Than Feared

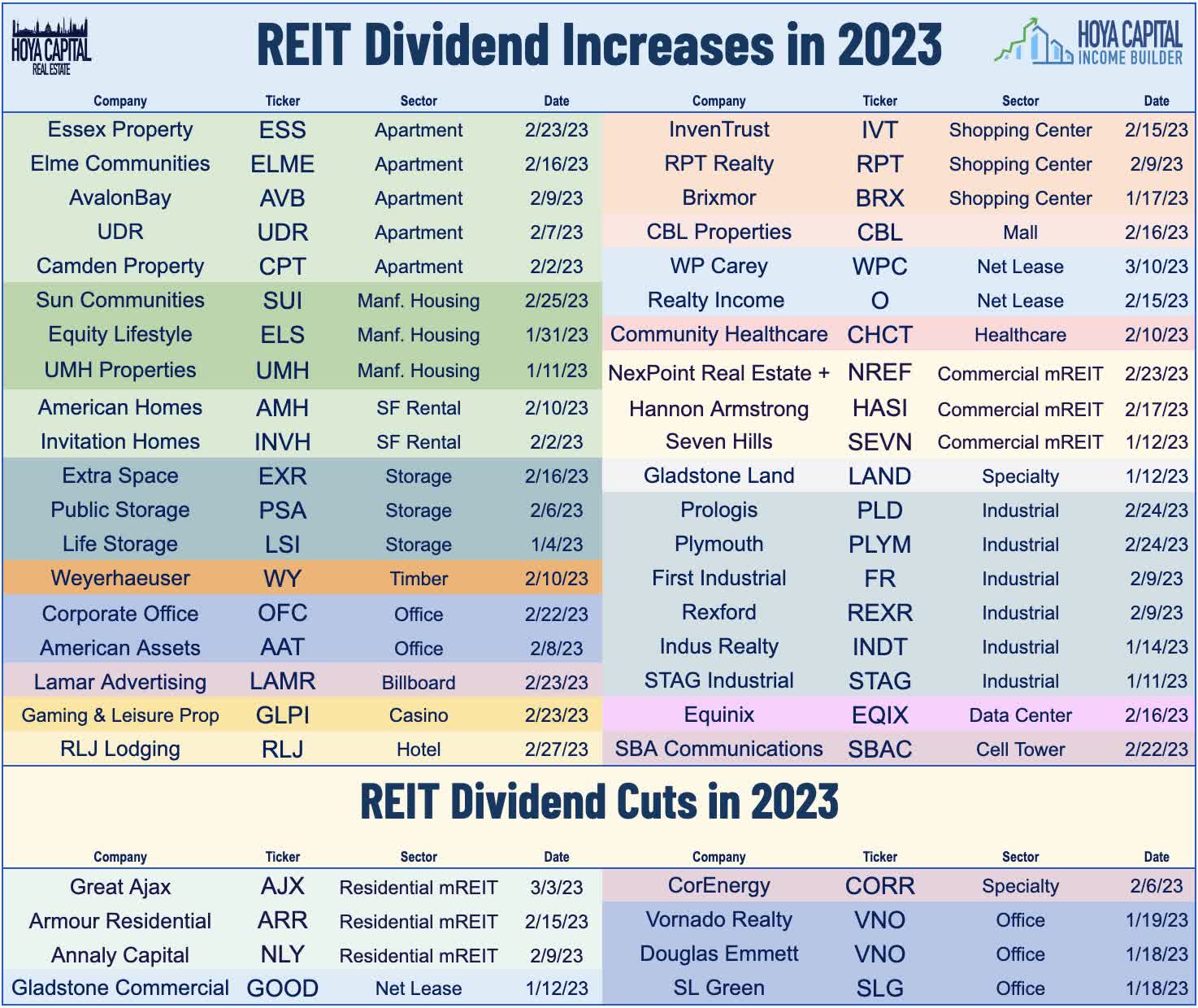

Recall that the mREIT sector faced a "dividend cut bloodbath" in 2020 as 30 mREITs reduced or suspended their dividend, including all-but-one residential mREITs and half of the commercial mREITs. The pandemic-driven wave of dividend cuts gave way to a similar power wave of dividend hikes in 2021 and into 2022 with the vast majority of the sector raising their dividend over those two years. That momentum has slowed since mid-2022, however, as dividend cuts in the mREIT space have outpaced dividend hikes over the past nine months. With many mREITs' payout ratios pushing their upper limits, we focused on earnings analysis on dividend-related commentary. Among the mREITs that are currently not covering their dividend, there was a mix of strategies expressed, with some REITs hinting at a likely dividend cut while others committed to holding steady at current levels.

{kind=link}

Residential mortgage REITs now pay an average dividend yield of 15.3% at an average payout ratio of 97% based on the Bloomberg consensus for full-year 2023 EPS, but 8 of the 21 mREITs are paying dividends above their expected 2023 EPS. This year, we've seen dividend reductions from three residential mREITs: Annaly Capital , Armour Residential , and Great Ajax . This follows reductions last year from eight names: Orchid Island , Invesco , AG Mortgage , PennyMac , Ready Capital , Chimera , and Western Asset . Earnings call commentary indicated that, with some exceptions, most residential mREITs still see their current distribution levels as sustainable given the improved earnings potential in the wider-spread environment and from hedge-related income that is not included in EPS metrics. We compiled relevant commentary below from earnings calls below.

{kind=link}

| TWO |

| "We believe the current dividend is sustainable at this level." |

| ORC |

| " We see it as sustainable . We were a little short in the fourth quarter, but that's just purely on an income basis. The portfolio's total return was much higher than the dividend because we had the price appreciation." |

| ARR |

| "Our aim is to pay an attractive dividend that is appropriate in context and stable over the medium-term. We keep a keen eye on economic conditions and the Board believes that this dividend rate achieves those objectives ." |

| EFC |

| "We have no plans to cut the dividend ." |

| RWT |

| "We are currently estimating book value to be of 2% through February 7th, and EAD earnings to re-approach our dividend level for the first quarter." |

| DX |

| "Our portfolio and liquidity is currently structured to support the economic return necessary to pay the current level of the dividend ." |

| NLY |

| "While we generated EAD that covered our dividend this quarter, we anticipate further pressure on EAD. We expect to reduce our dividend in Q1 to a level closer to our historical yield on book value of 11% to 12% vs. 16% today." |

| WMC |

| "Our distributable earnings in the quarter fell short of our dividend of $0.40 per share. We will continue to evaluate the level of the dividend ." |

On the other side of the sector, Commercial Mortgage REITs now pay an average dividend yield of 12.1% at a more modest average EPS payout ratio of 90% while just four mREITs above 100%. Two commercial mREITs have raised their dividend this year: Hannon Armstrong and Seven Hills, while a handful of names raised their payouts in late 2022, including Arbor Realty , Ladder Capital , and BrightSpire Capital . We've seen four commercial mREITs reduce their dividends over the last year; however, including Granite Point , Lument Finance , Ready Capital , and Broadmark Realty . Our review of earnings call commentary found a high degree of confidence in covering dividends among the larger and mid-sized commercial mREITs. We compiled relevant commentary below from earnings calls below.

{kind=link}

| BXMT |

| " The dividend is well protected , 140% coverage this quarter, creating meaningful cushion against non-accruals." |

| STWD |

| "We project we will continue to earn our dividend each quarter this year in our core businesses alone. Our ability to earn our dividend also doesn’t depend on raising incremental capital" |

| ABR |

| On maintaining the dividend in the quarter: "[The Board felt] that there is really no upside in the market to raising the dividend and [we wouldn't get] credit after raising it 3 times last year and in 10 of the last 11 quarters." |

| ACRE |

| "We fully covered our regular and supplemental dividends from distributable earnings at 110%." |

| ARI |

| "ARI's portfolio remains well-positioned to continue generating distributable earnings in excess of the common stock dividend." |

Mortgage REIT Preferreds

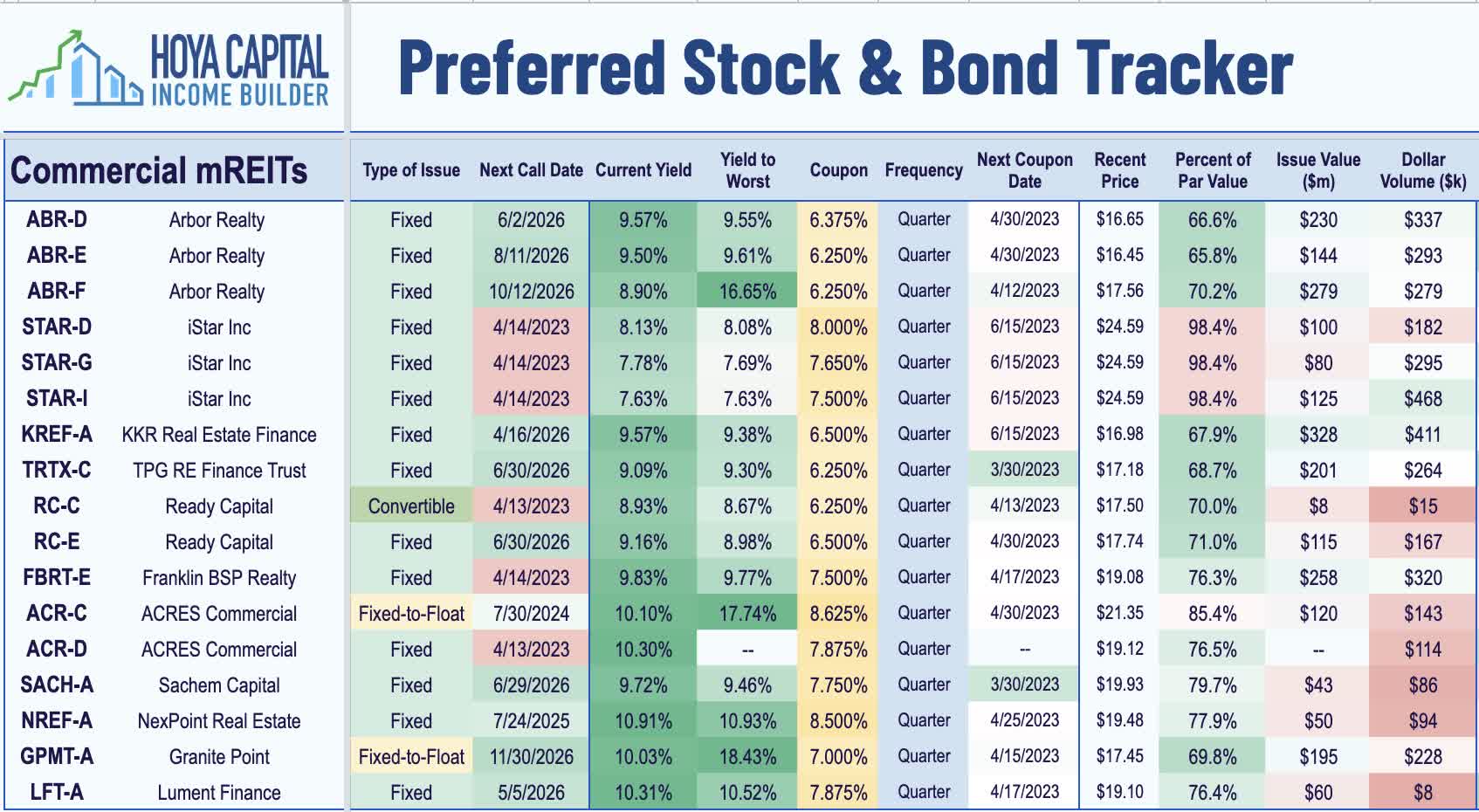

Investors seeking more fixed-income-like exposure can also take the "preferred route" as mortgage REITs make far heavier use of preferred stock within their capital stack as compared to equity REITs. Preferred stocks generally offer more downside protection, but in exchange, these securities offer more limited upside potential than common stock. Ten of the 20 commercial mREITs currently have outstanding preferred stocks or "baby bonds": Arbor Realty ( ABR ) has a suite of relatively new issues, while Ready Capital ( RC ) and Ares Commercial ( ACRE ) each have two actively-listed preferreds. Six others each have one preferred issue - KKR Real Estate ( KREF ), TPG Real Estate ( TRTX ), Franklin BSP Realty ( FBRT ), Sachem Capital ( SACH ), NexPoint Real Estate ( NREF ), and Lument Finance ( LFT ).

{kind=link}

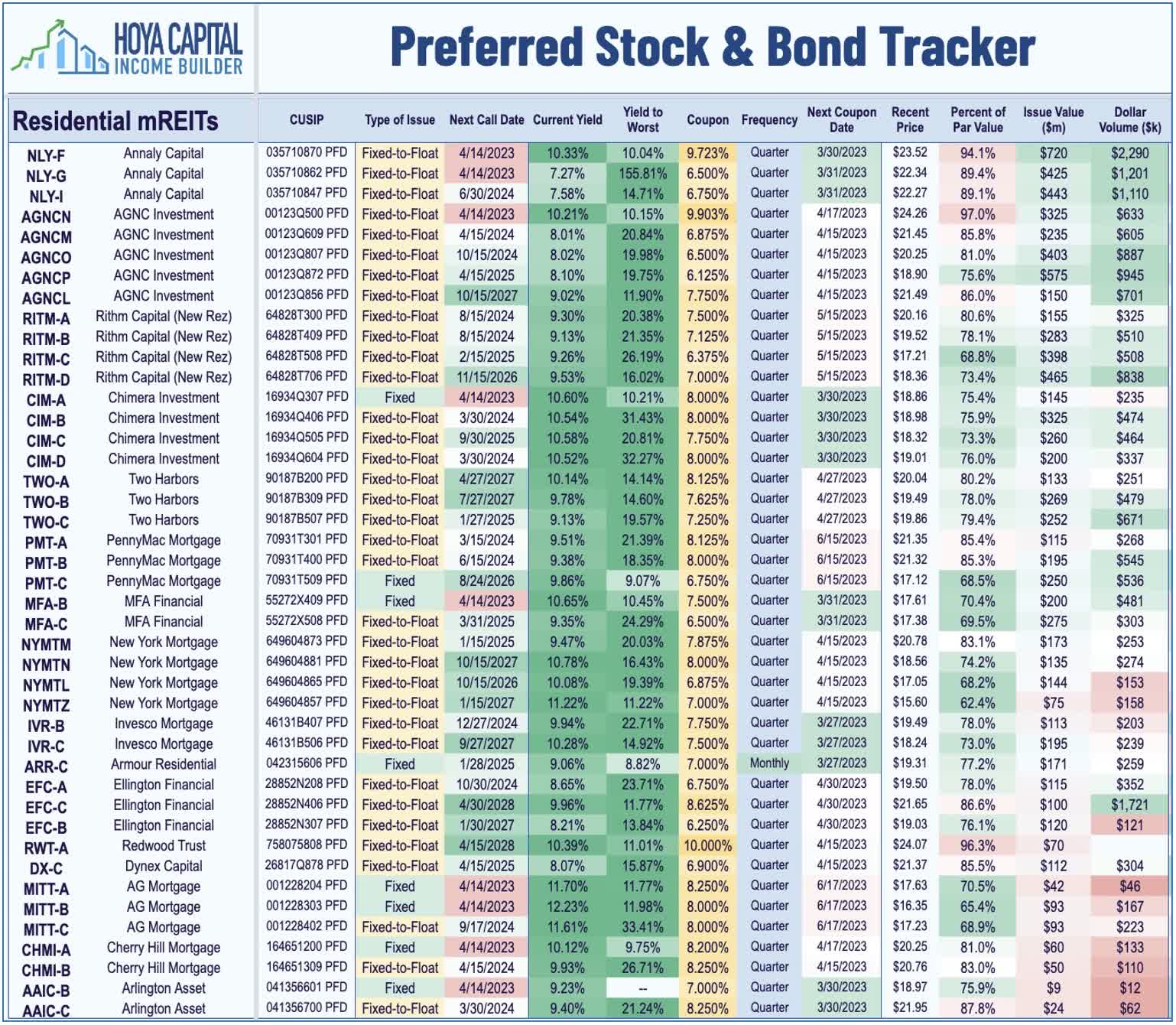

Residential mREITs make even higher use of preferred securities with 16 of the 21 REITs offering preferred issues and/or exchange-traded "baby bonds". All 43 currently outstanding preferred securities from these REITs are cumulative, which entitles investors to "missed" dividend payments before any distributions can be paid to common shareholders. While a half-dozen mREITs had initially suspended their preferred distribution, all have since resumed distributions. On average, the 49 residential mortgage REIT preferred issues pay a current yield of 9.68% while commercial mortgage REIT preferred issues pay an average current yield of 9.38%. On average, residential and commercial mREIT preferreds trade at roughly 20% discounts to par value.

{kind=link}

Takeaways: Everything in Moderation

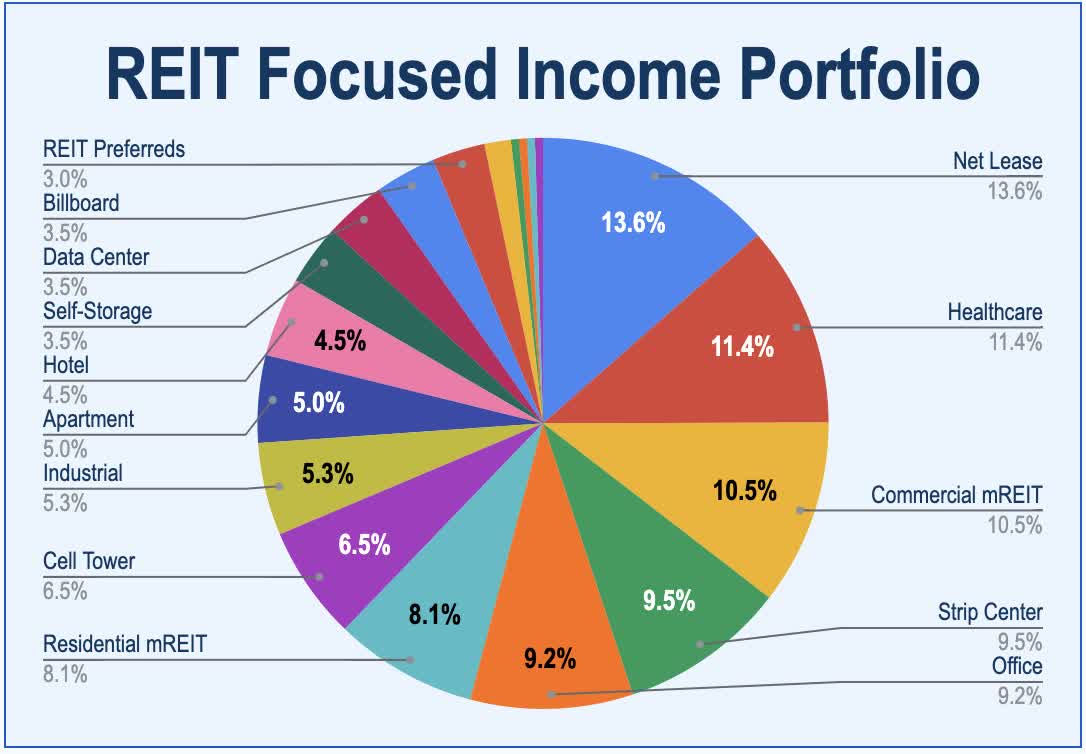

Mortgage REITs don't deserve their 'ugly duckling' status within the REIT sector, but we continue to emphasize that when buying individual mREITs, quality and an extra level of diligence is absolutely essential as BVPS declines can be "temporary" for well-managed portfolios with reasonable leverage and effective hedges, but BVPS declines can become "permanent" for less-prepared mREITs. A philosophy that we employ in the RIET ETF as well, the Focused Income Portfolio is able to achieve a premium dividend yield with an aggregate balance sheet and asset quality - and dividend coverage - that is at least on par with the broader REIT benchmarks. We also reiterate our philosophy of using mortgage REITs diversified across various property types and risk sensitivities to complement a diversified equity REIT portfolio to reduce the interest rate sensitivity and improve the inflation-hedging potential.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Mortgage REITs: High Yield Opportunity And Risk