IFGL - Mortgage REITs: High-Yield Risk And Opportunity

2023-06-27 10:00:00 ET

Summary

- Recovering from a sharp sell-off in the wake of the Silicon Valley and First Republic Bank collapses, Mortgage REITs have rebounded as turmoil across interest rate markets has calmed.

- Distress in the commercial and residential real estate markets has been more isolated than the 'scary' magazine covers would suggest. Outside of urban office properties, default rates remain near pre-pandemic lows.

- Dividend cuts have come as a 'ripple' rather than a 'wave.' 10 of 40 mREITs have reduced their dividends this year, but industry-wide payouts are only-down about 5% year-to-date.

- The squeeze on highly-levered private market portfolios is still in the early innings, but an orderly unwind remains the base case. Public equity REITs with balance sheet firepower should eventually scoop up many debt-burdened privately-held assets.

- 'Boring' Is Good: Like high-yield corporate credit, mortgage REITs are highly sensitive to macroeconomic shocks, but several higher-quality mREITs appear overly discounted and poised to deliver attractive income-heavy total returns as COVID-era shocks dissipate.

REIT Rankings: Mortgage REITs

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on June 24th.

{kind=link}

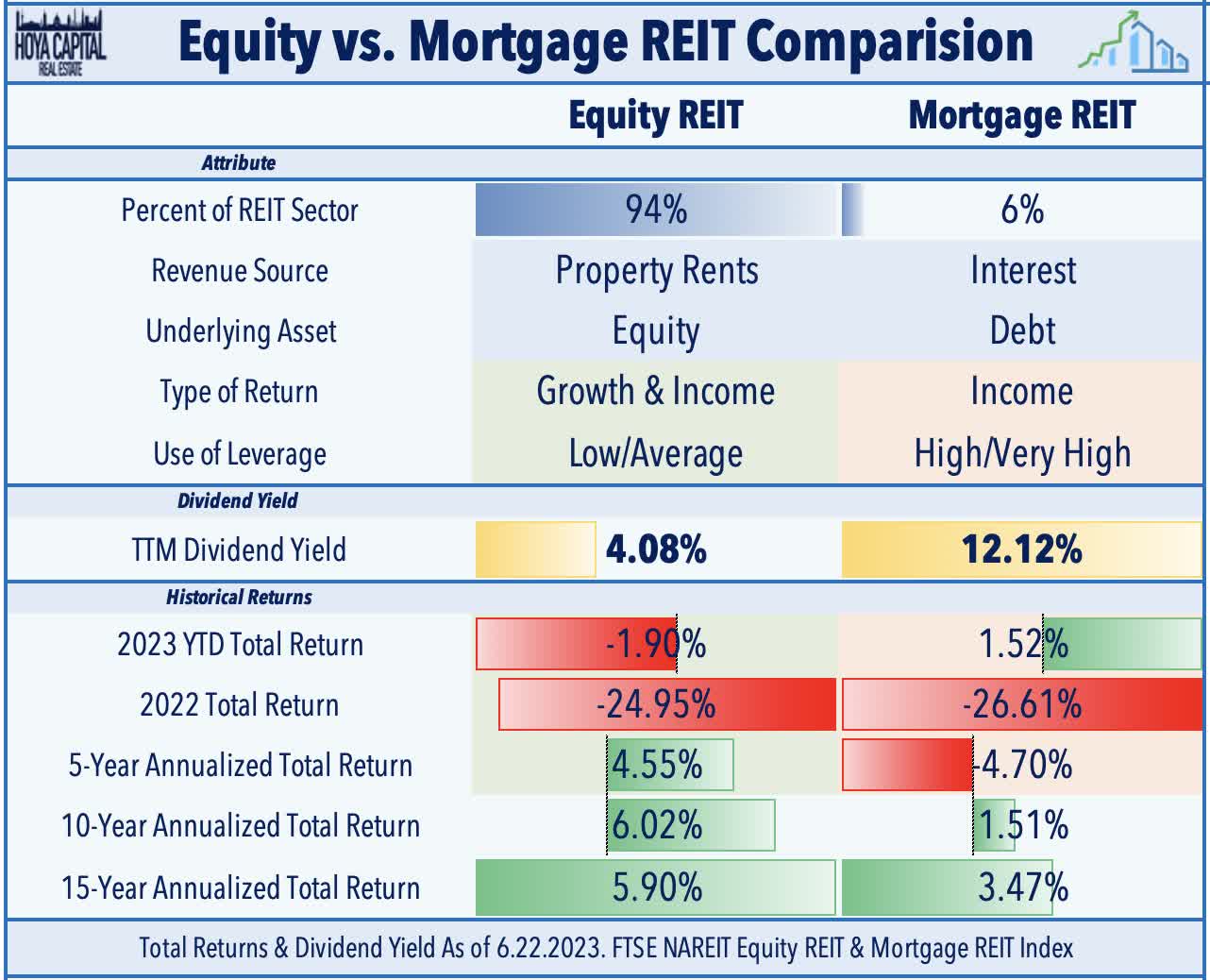

Best known for their hearty dividend yields that often breach double digits, Mortgage REITs - also called "mREITs" - comprise roughly 5% of the total REIT universe. Often viewed as a distinct asset class from equity REITs which own, operate, and collect rent on real estate properties, mortgage REITs function more like a lending bank by originating and investing in interest-bearing real estate debt instruments. mREITs were slammed by the fallout of the regional banking crisis in March amid a resurgence of interest rate volatility and credit concerns - erasing their once-robust gains for 2023 - but have rebounded by roughly 15% since bottoming in April and are now again outpacing their equity REIT peers on the year. Like high-yield corporate credit, mortgage REITs are highly sensitive to macroeconomic shocks, but several higher-quality mREITs appear overly discounted and poised to deliver attractive income-heavy total returns as COVID-era shocks dissipate.

{kind=link}

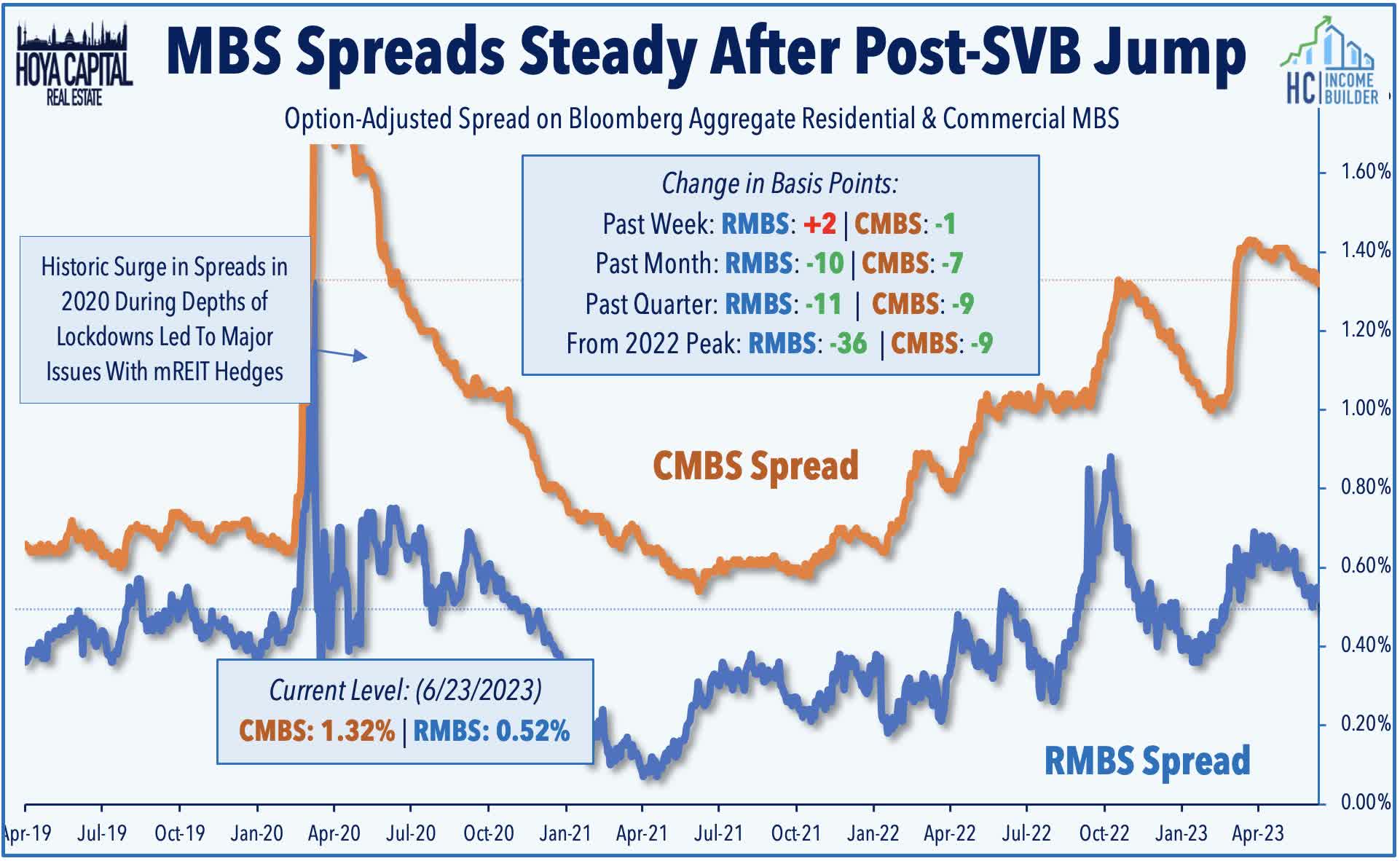

As discussed in our State of the REIT Nation report earlier this month, commercial real estate credit quality has remained quite stable across all of the major property sectors outside of the office segment. Notably, the iShares MBS ETF ( MBB ) and the iShares CMBS ETF ( CMBS ) - the benchmarks tracking the un-levered performance of residential and commercial mortgage-backed bonds - have responded favorably to recent market developments as headwinds from modestly higher benchmark interest rates have been more-than-offset by a modest tightening of MBS spreads since the end of March. Since the end of the first quarter, the benchmark 10-Year Treasury Yield, has increased by 18 basis points to 3.73%, but RMBS spreads have narrowed by 7 basis points to 0.52%, while CMBS spreads have narrowed by 11 basis points to 1.32%. The Merrill Lynch Option Volatility ("MOVE") Index - a measure of interest rate volatility - has declined about 20% since the end of Q1. Together, these three factors - benchmark rates, credit spreads, and rate volatility - suggest that mREIT Book Values will be flat-to-slightly positive in Q1.

{kind=link}

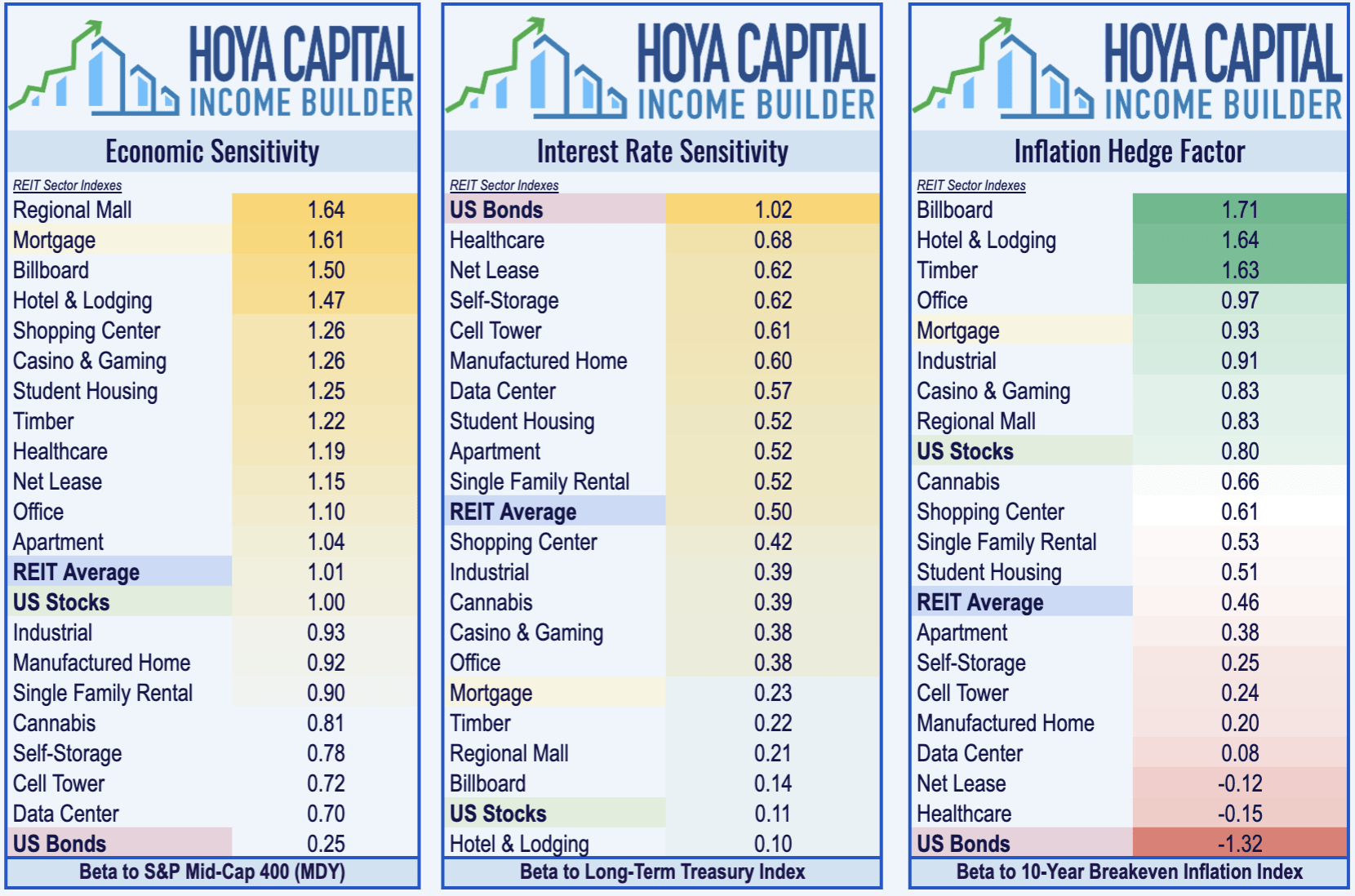

Mortgage REIT performance has historically been driven more directly by the velocity of interest rate movements rather than the absolute direction, and mREITs notably outperformed their Equity REIT peers in the pre-COVID era from 2015-2019, a macroeconomic environment characterized by a slow-but-steady increase in the Federal Funds rate and relatively muted interest rate volatility. Despite their volatility over the past several years, mortgage REITs don't necessarily deserve their "ugly duckling" status within the real estate sector and we reiterate our view that maintaining a modest mREIT allocation to a balanced income-focused real estate portfolio can be a prudent strategy to hedge interest rate and inflation risk while adding immediate income. As illustrated through our Inflation Hedge Factor , mortgage REITs provide some of the better inflation-hedging characteristics within the REIT sector and exhibit more muted interest rate sensitivity compared to their equity REIT peers.

{kind=link}

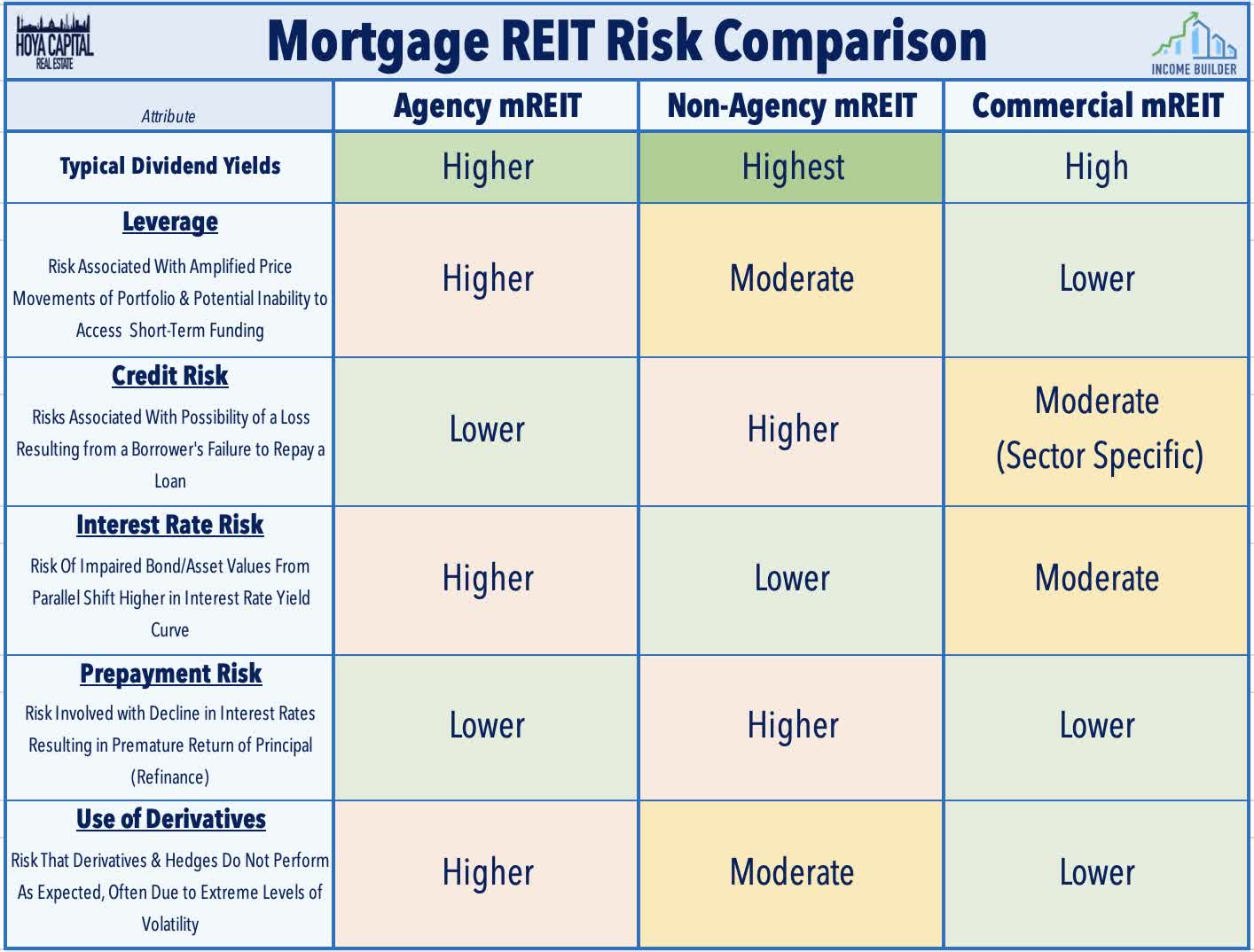

That said, it's important to keep in mind that mortgage REITs are not monolithic in their risk exposures. Mortgage REITs typically operate with a high degree of leverage to amplify investment spreads and often use short-term hedging instruments to manage interest rate and credit exposure, which makes each REIT rather unique in its end-exposure to certain macroeconomic environments. In general, similar to high-yield corporate credit, mortgage REITs tend to perform their best in "boring markets" - periods of lower interest rate and stock market volatility. Below, we define the five primary risk exposures faced by these different types of mortgage REITs: leverage risk, credit risk, interest rate risk, prepayment risk, and derivative risk.

{kind=link}

Residential Mortgage REIT Overview

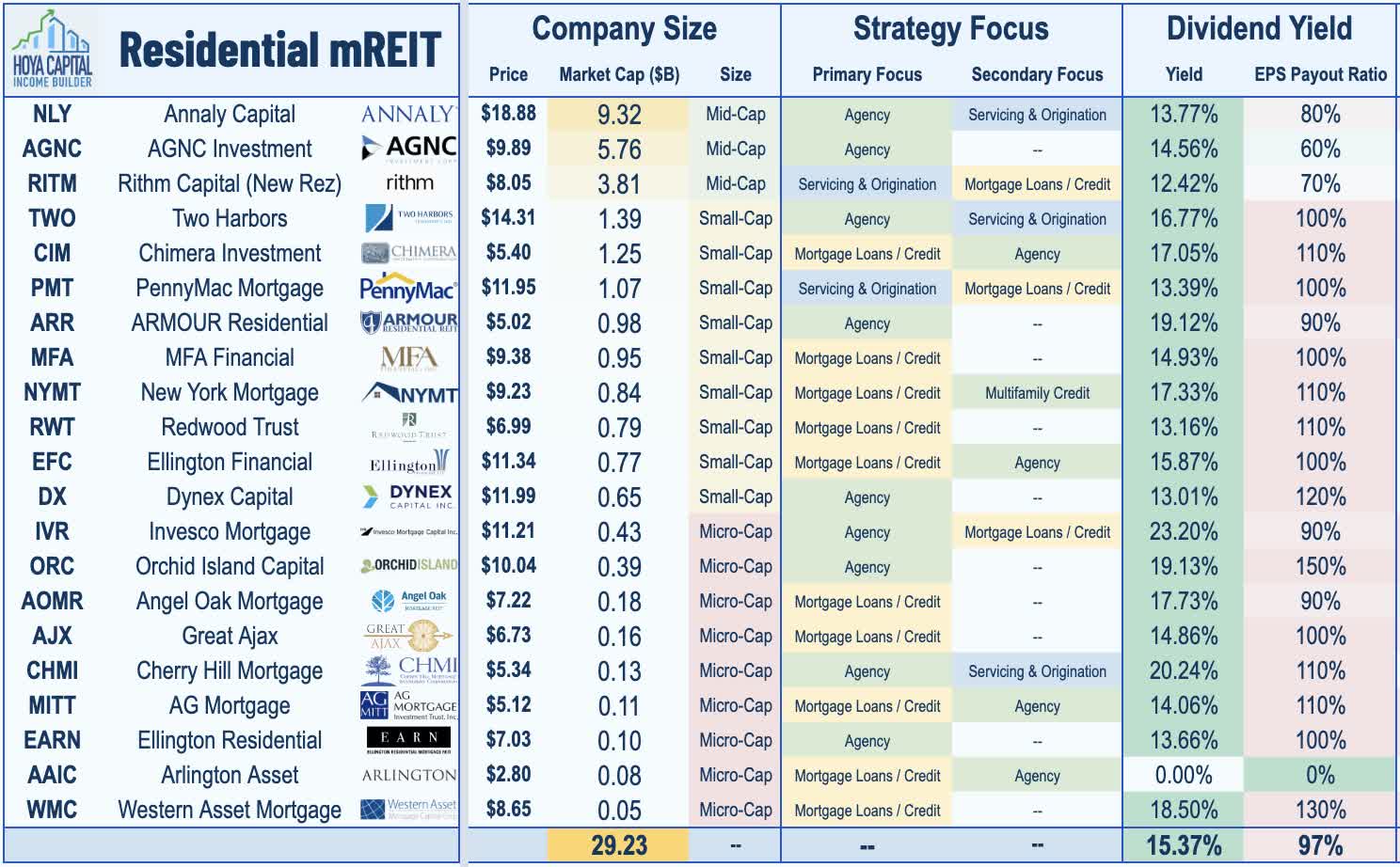

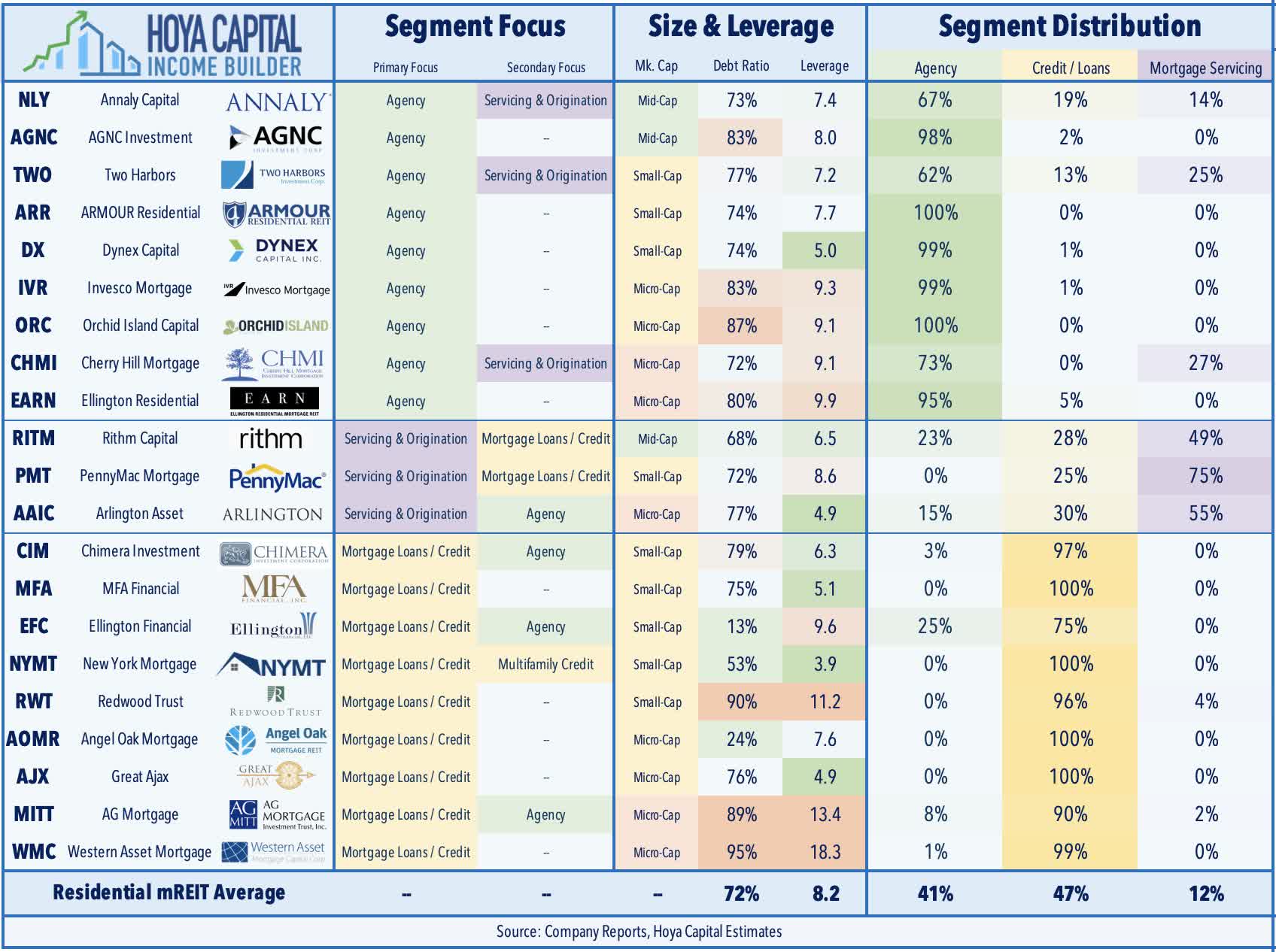

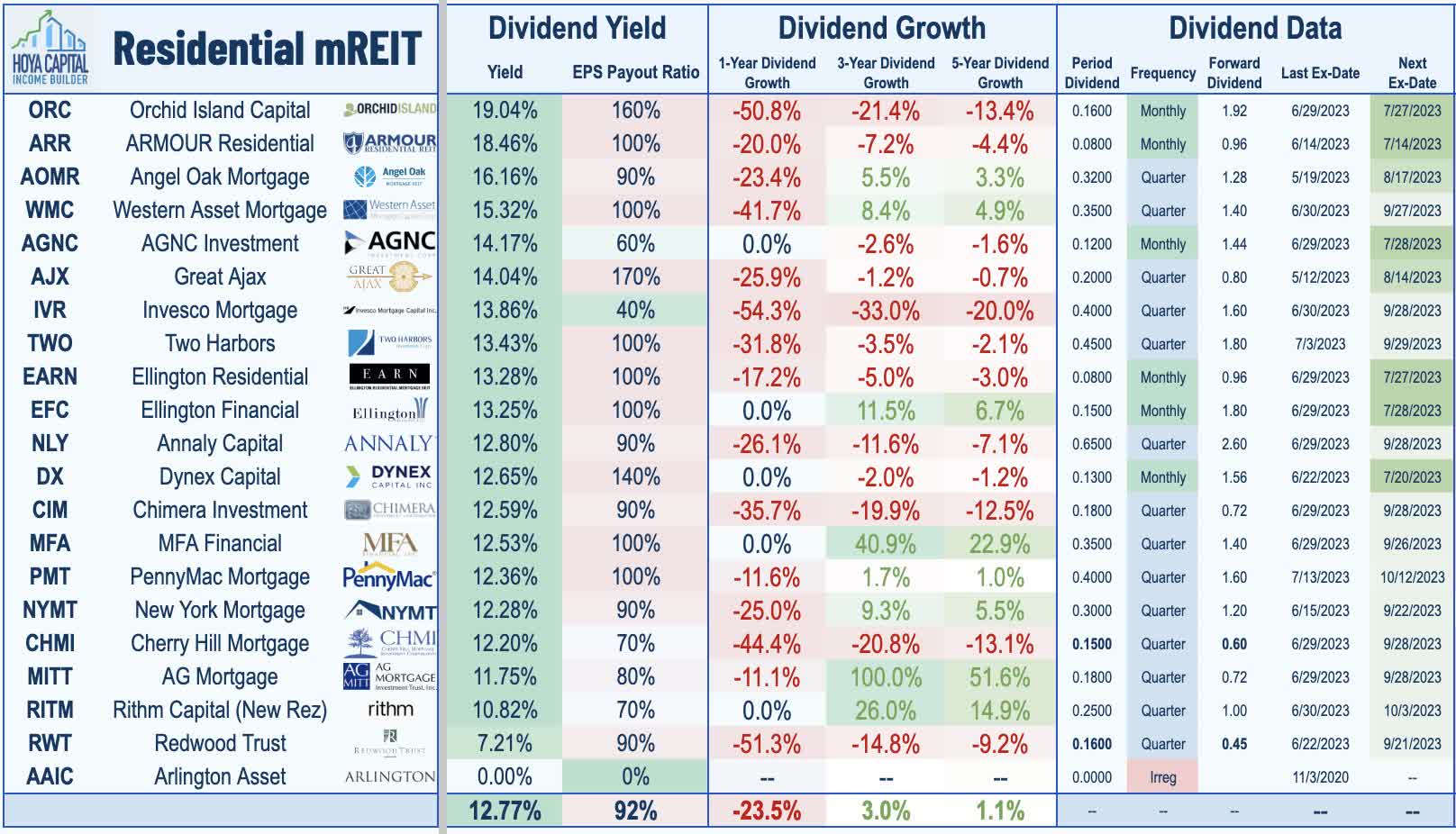

In the Hoya Capital Residential Mortgage REIT Index , we track the 21 exchange-listed residential mREITs, a sector that is comprised primarily of small and micro-cap REITs which pay dividend yields in the mid-to-high teens. Not unlike a traditional mortgage bank, Residential mREITs purchase and originate residential mortgages and mortgage-backed securities ("MBS"), and use leverage to enhance the investment spread between the effective lending rate and their cost of capital. As we'll discuss throughout this report, residential mREIT Book Values remain in decent shape as concerns over a looming housing market crisis have thus far proven to be misguided, and RMBS spreads have again narrowed after a surge in the wake of the Silicon Valley Bank collapse. While residential credit remains healthy, heightened interest rate volatility has taken a toll on several more-highly-levered mREITs, prompting a ripple of dividend reductions across the sector this year.

{kind=link}

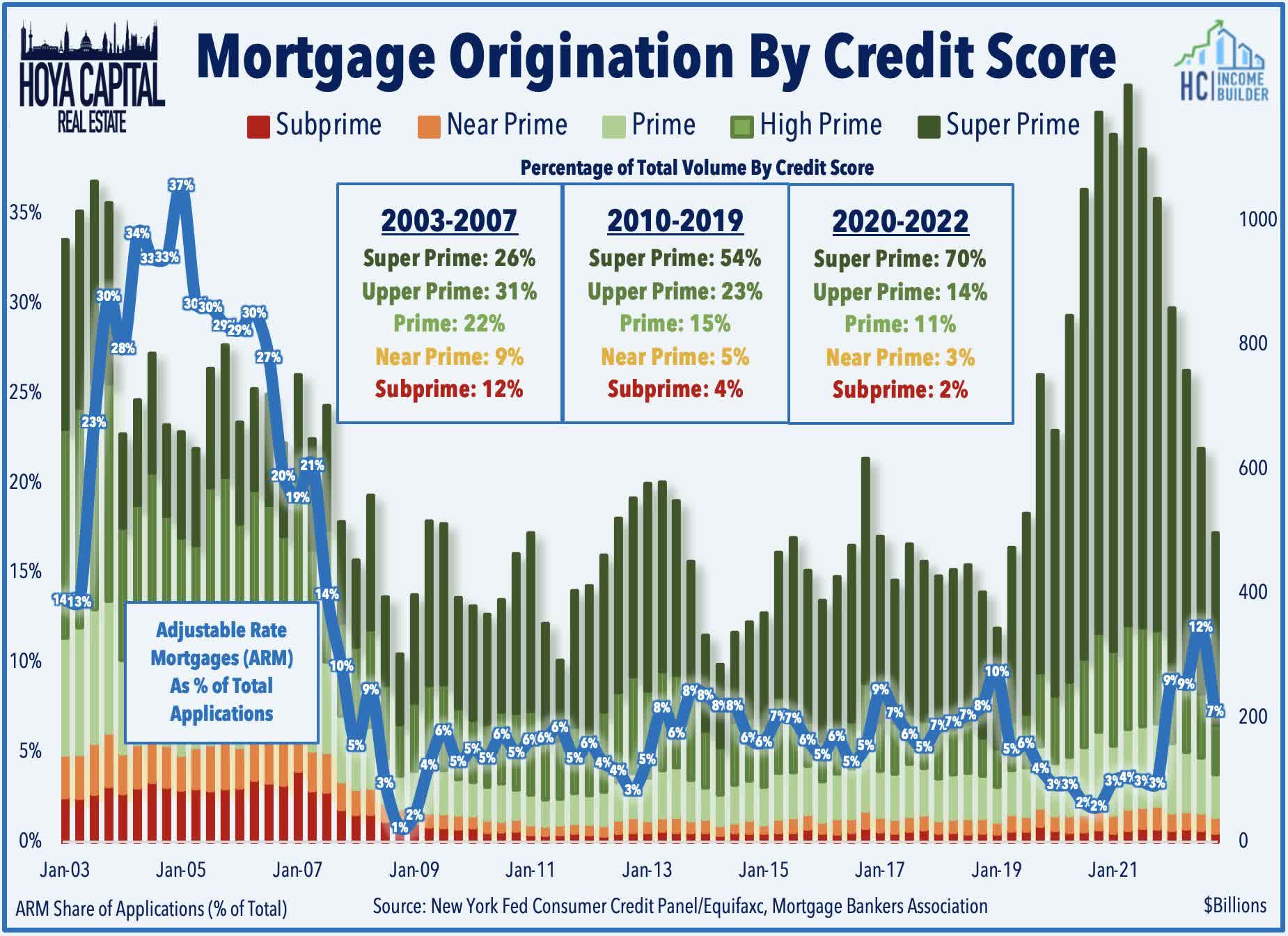

The cooldown in housing market activity in 2022 and into early 2023 sparked by surging mortgage rates renewed the perennial "Bubble" calls from pundits , but recent fundamentals suggest that national housing markets are instead more likely to see a somewhat "boring" return to normalcy ahead, a macro environment similar to 2016-2019 when rising mortgage rates resulted in a notable near-term slowdown in buying activity before activity began to level-off and accelerate as the Fed took its foot off the gas in mid 2019. Importantly, subprime loans and adjustable-rate mortgages - the dynamite that led to a cascading financial market collapse in 2008 - have been essentially non-existent throughout this cycle. Adjustable-rate mortgages - which would be most "at-risk" from the surge in rates have accounted for less than 5% of mortgages originated since 2009, down from nearly 30% at the peak in 2005.

{kind=link}

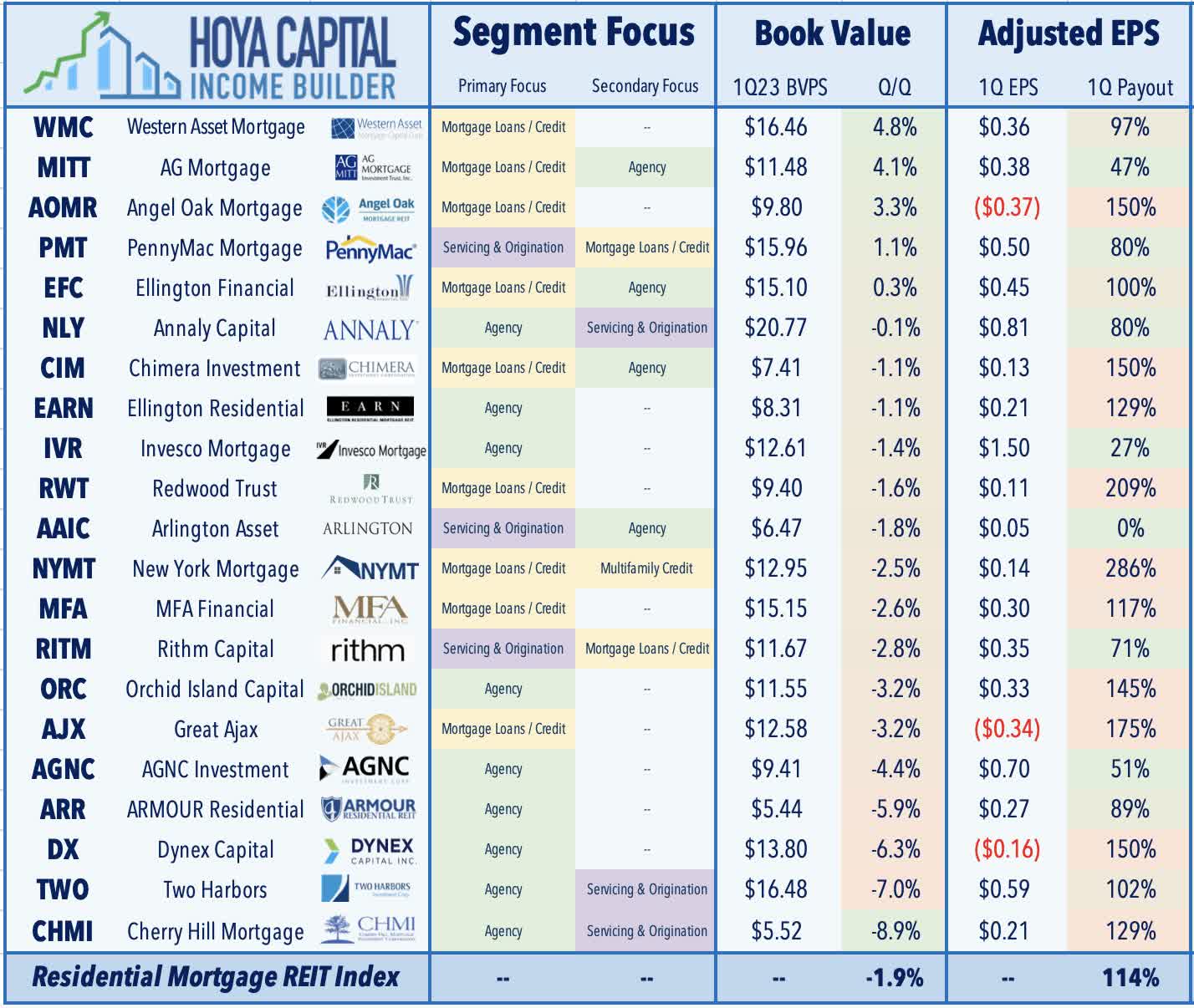

The sector can be further split into three sub-sectors: Agency mREITs - led by Annaly Capital ( NLY ) and AGNC Investment ( AGNC ) - invest primarily in agency mortgage-backed securities, or RMBS, which have their principal guaranteed by a Government-Sponsored Enterprise, or GSE, such as Fannie Mae, Freddie Mac, or Ginnie Mae, and thus bear minimal credit risk but tend to be more sensitive to changes in interest rates. Servicing/Origination mREITs - led by Rithm Capital ( RITM ) and PennyMac ( PMT ) - typically focus on non-traditional mortgage-related assets, including mortgage servicing rights (MSRs) and/or loan origination services. Credit-Focused mREITs - led by Chimera ( CIM ), MFA Financial ( MFA ), and New York Mortgage ( NYMT ) - invest in RMBS and other types of residential credit that are not guaranteed by a GSE, including whole mortgage loans, which bear higher levels of credit risk but tend to be less sensitive to changes in interest rates.

{kind=link}

Commercial Mortgage REIT Overview

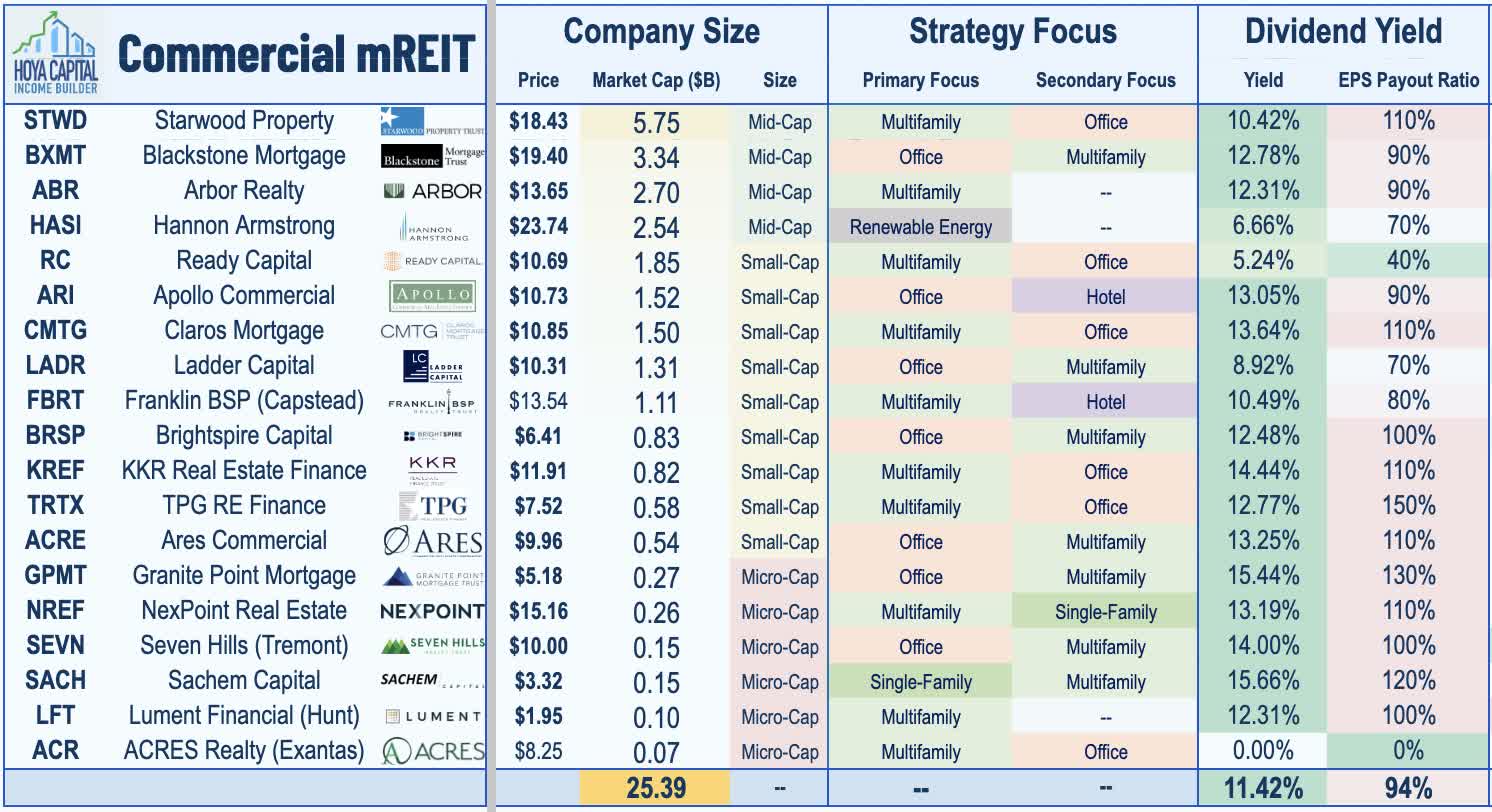

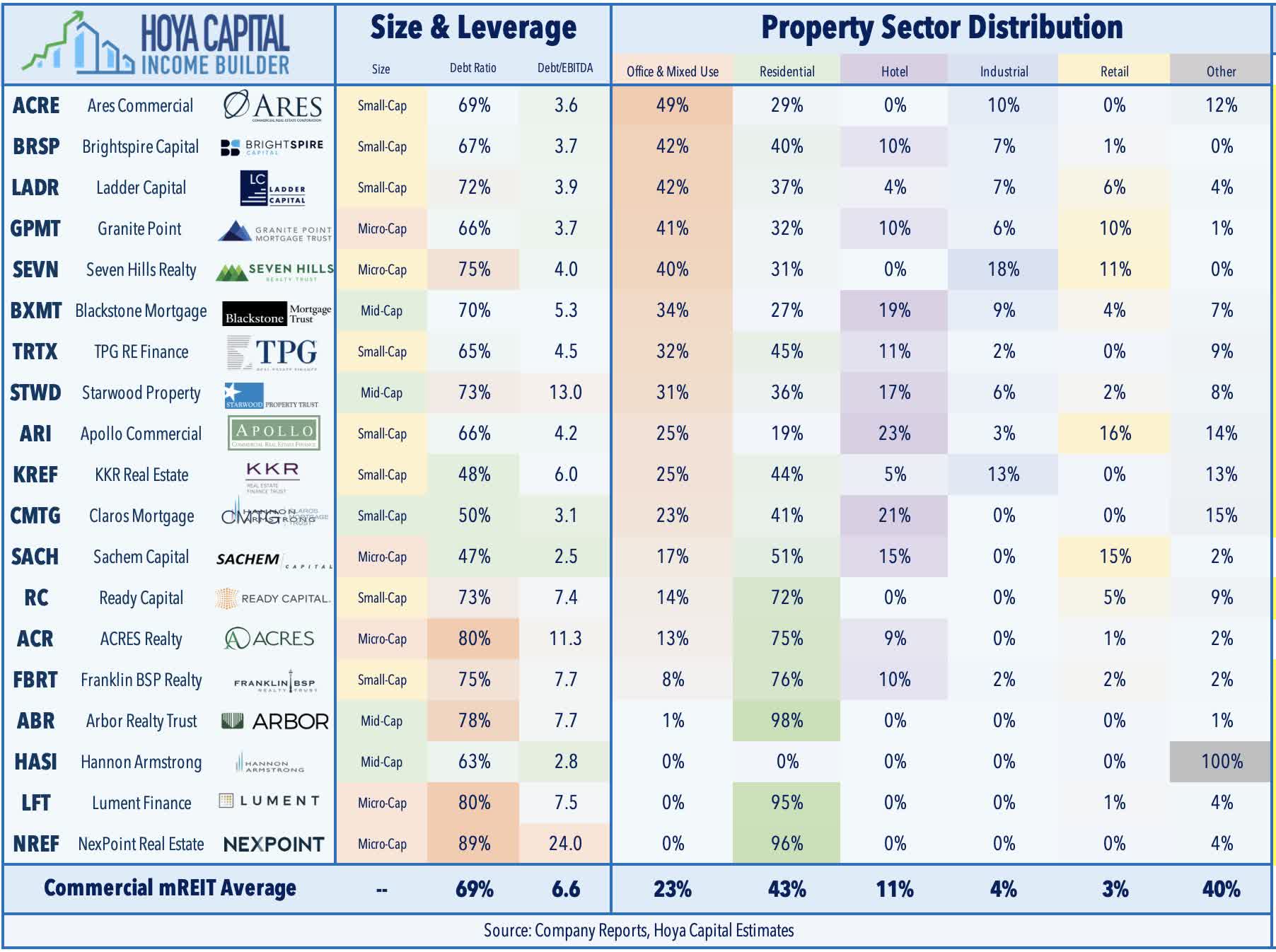

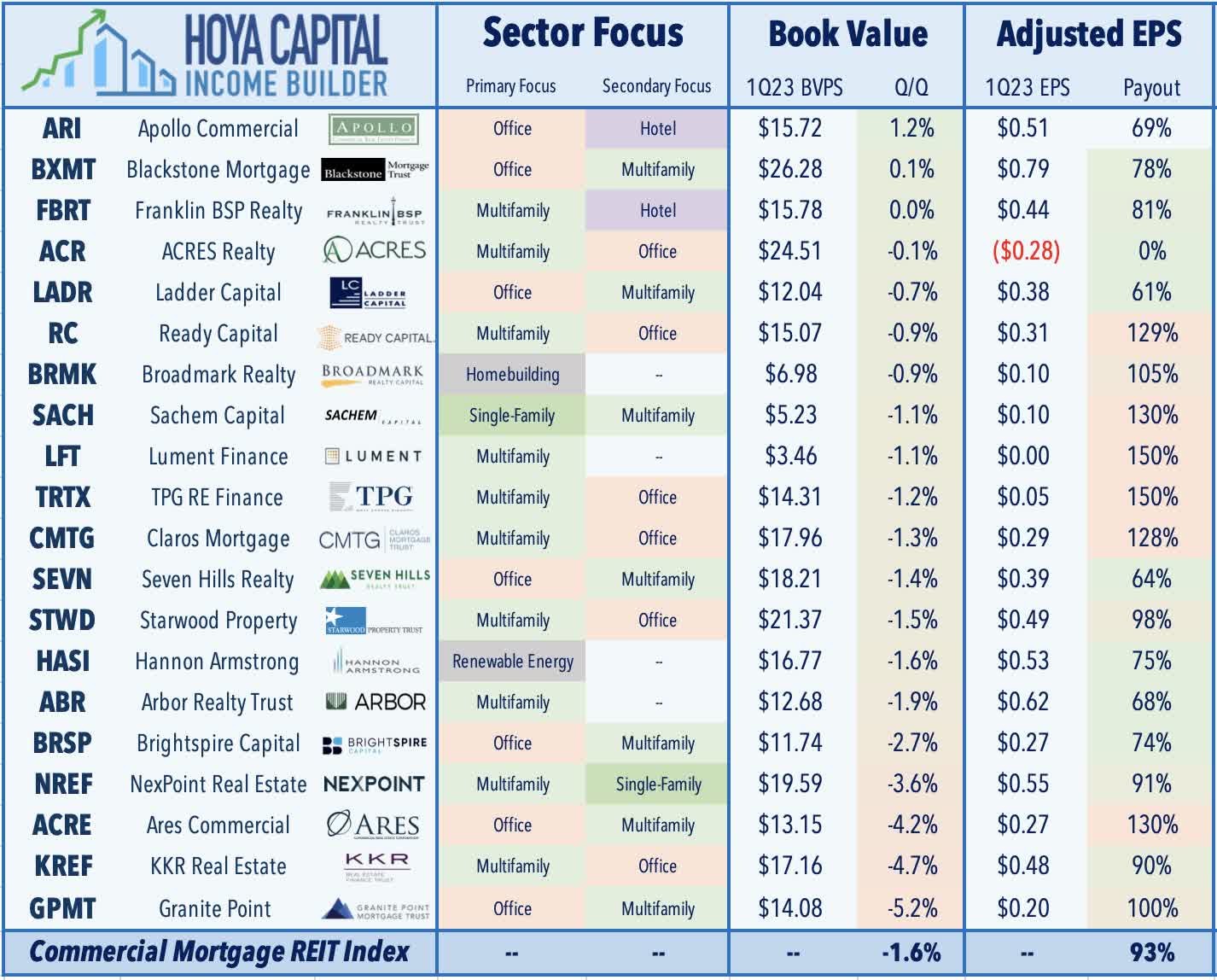

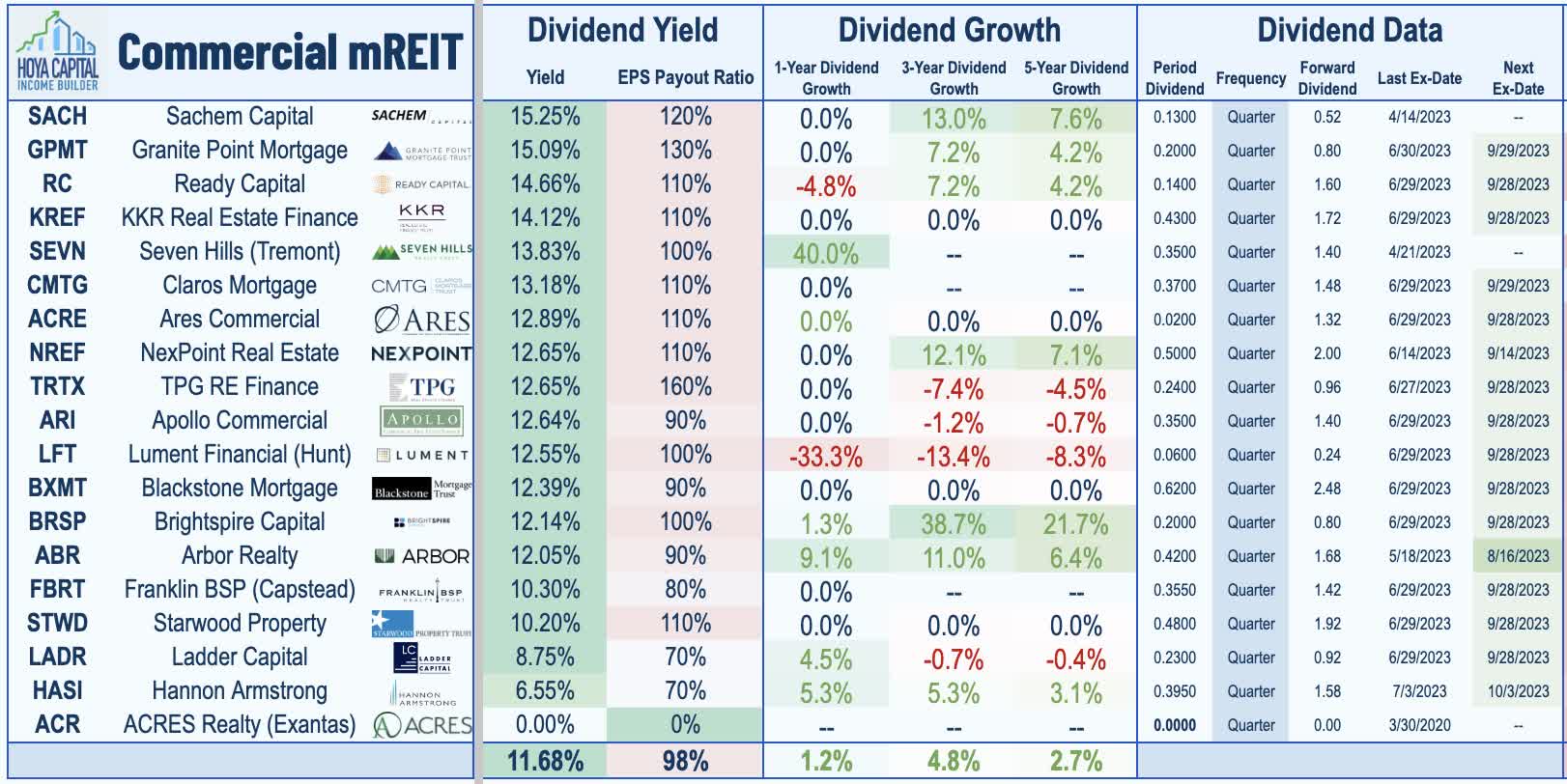

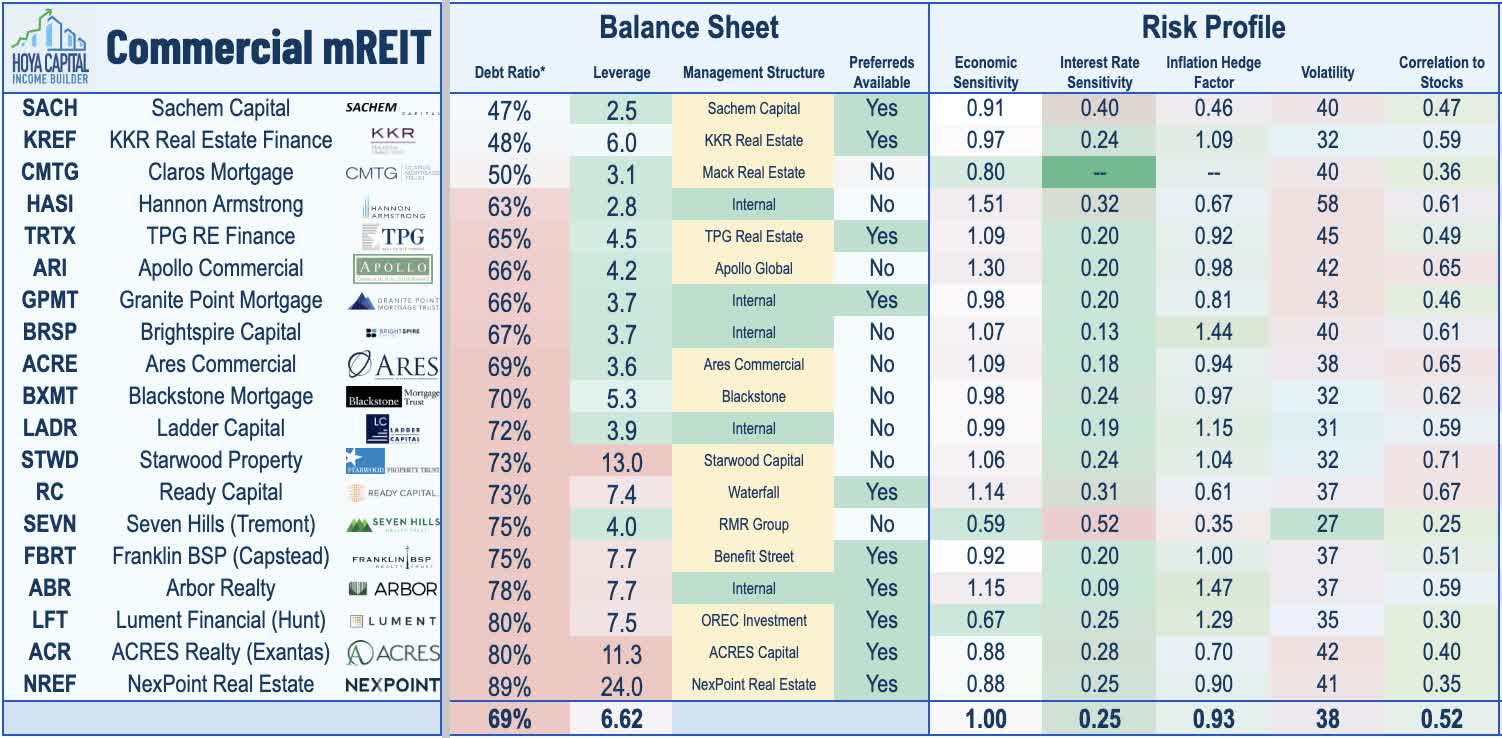

In the Hoya Capital Commercial Mortgage REIT Index , we track 19 exchange-listed commercial mREITs. Commercial mREITs tend to focus on one or a small handful of property sectors and generally provide floating-rate lending facilities with terms of 2-5 years collateralized by commercial real estate assets, often 'competing' with regional banks for deal flow. Like their counterparts on the residential side, the commercial mREIT sector is comprised primarily of small and micro-cap REITs, and pay dividend yields in the low teens. The sector can be further segmented into two categories: pure Balance Sheet Lenders, which originate and purchase loans for their own balance sheet, and Conduit Lenders , which originate and purchase loans both to hold on their own balance sheet and also for the purposes of securitizing the loans into a CMBS or other vehicles. We track two additional mREITs AFC Gamma ( AFCG ) and Chicago Atlantic ( REFI ) in our Cannabis REIT report.

{kind=link}

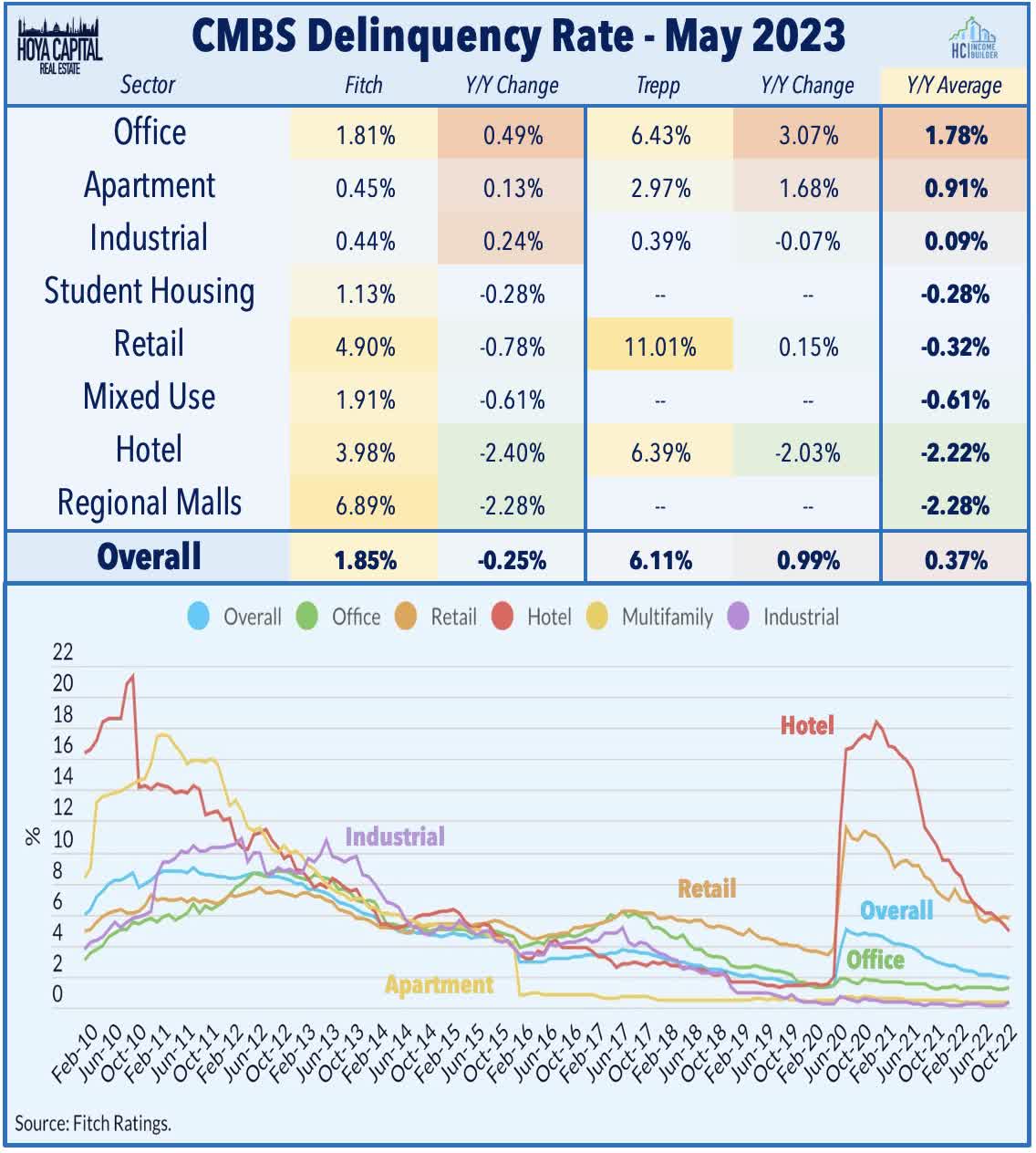

Renewed interest rate volatility sparked by the collapse of Silicon Valley Bank and Signature Bank - the second and third largest bank failures in U.S. history naturally revived concern that the mREIT sector could face a similar wave of distress as seen in the two prior financial crises - the Great Financial Crisis in 2008 and the COVID Crisis in 2020. These concerns have thus far proven to be overstated as underlying fundamentals in both the residential and commercial real estate industry remain on stable footing, albeit with the notable exception of urban office assets. MSCI Real Assets reported last week that there is roughly $43B of office properties that are in "potential distress" - which is the most of any property sector - as maturities come due over the coming years. MSCI defines "distressed" as properties in bankruptcy, default, court administration, liquidation, or that have CMBS loans that have been transferred to a special servicer. Trepp reports that the percentage of office loans in distress has nearly doubled over the past year to 6.4%, while Fitch data showed that delinquency rates on office loans increased to 1.8% in May, a year-over-year increase that is twice as large as the next property sector.

{kind=link}

Historically, office loans were generally viewed as "low risk" with default rates that were a fraction of hotel and retail-backed loans, but this dynamic has, of course, shifted rather dramatically in the post-pandemic era. We take a deeper dive into these commercial mREITs' property sector exposure in light of amplified credit concerns for the U.S. office sector, which has faced challenges from Work-From-Home headwinds and fears of cascading distress. Over the past quarter, we've seen a handful of large-sized loan defaults on office loans from Pimco , Brookfield , and RXR - defaults sparked primarily by soaring debt service expense rather than property-level cash flows. As a whole, office assets represent about a fifth of commercial mREITs' property-level exposure, but a handful of names have outsized weight in the office sector, including Ares Commercial ( ACRE ), BrightSpire ( BRSP ), Ladder Capital ( LADR ), and Granite Point ( GPMT ) at more than 40% of their loan books.

{kind=link}

Mortgage REIT Performance & Earnings

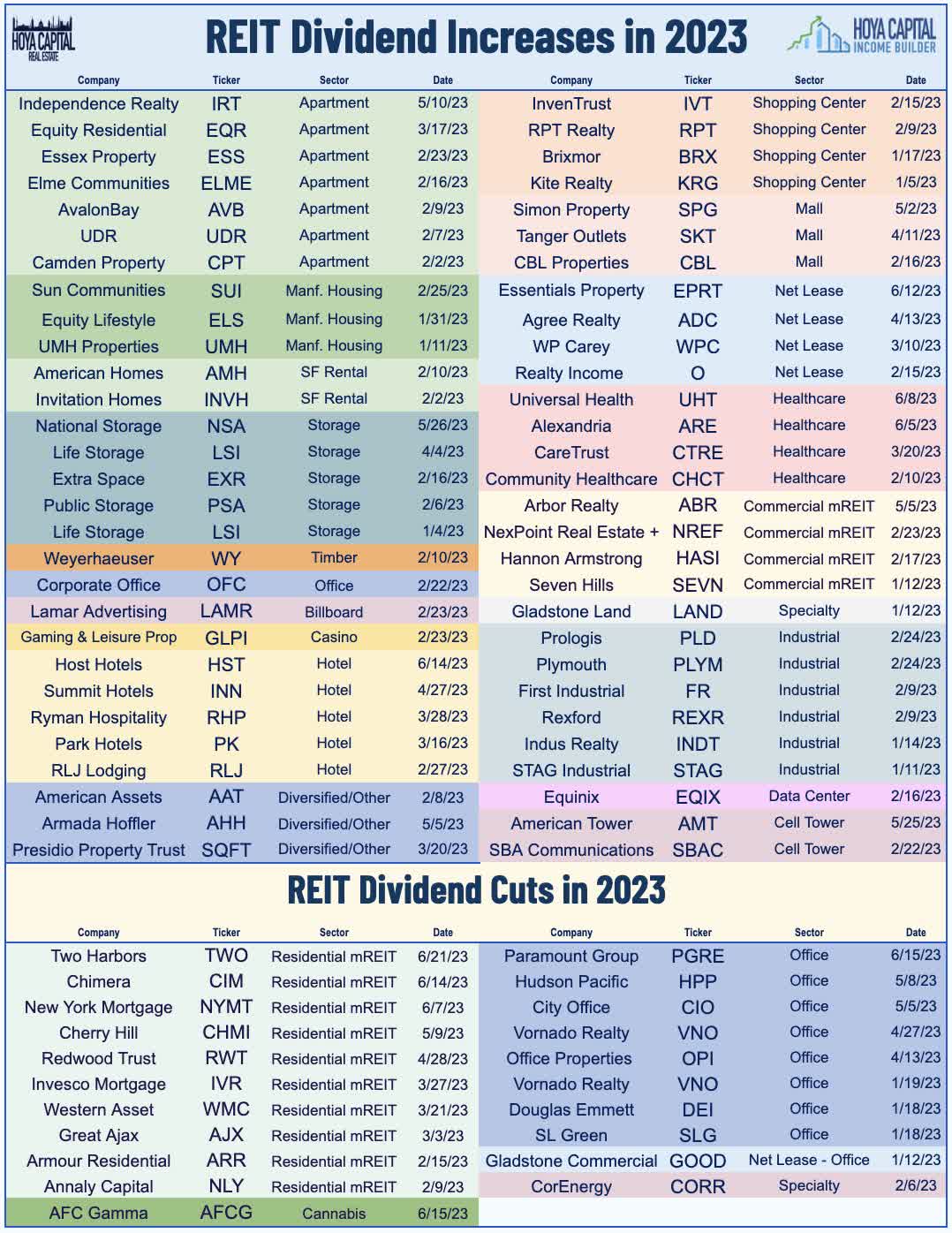

The mortgage REIT sector faced a "dividend cut bloodbath" in 2020 as 30 of 40 mREITs reduced or suspended their dividend, including all-but-one residential mREITs and half of the commercial mREITs. The pandemic-driven wave of dividend cuts gave way to a similar power wave of dividend hikes in 2021 and into 2022 with the vast majority of the sector raising their dividend over those two years. That pendulum has swung back in the negative direction since mid-2022, however, as dividend cuts in the mREIT space have outpaced dividend hikes by about 2:1 over the past twelve months. That said, these recent dividend cuts have come as a 'ripple' rather than a 'wave.' While 10 of 40 mREITs have reduced their dividends this year, industry-wide payouts are down only about 5% since the start of the year compared to the 60% decline in dividends seen during the "bloodbath" of 2020.

{kind=link}

As discussed in our Earnings Recap , residential mREIT results in the first quarter were "hit-and-miss" given the volatile interest rate environment combined with these REITs' typically high leverage and uncertain hedge exposure. On average, residential mortgage REITs reported a 1.9% decline in their Book Value Per Share in Q1 compared to the prior quarter. Credit-focused mREITs fared better in Q1 - reporting a slight increase in their Book Value Per Share ("BVPS") - led by PennyMac ( PMT ) along with a trio of small-cap mREITs - Angel Oak ( AOMR ), Western Asset ( WMC ), and AG Mortgage ( MITT ). Agency-focused REITs, however, reported an average decline in their BVPS of about 5% in Q1, with Dynex Capital ( DX ), Two Harbors ( TWO ), Cherry Hill ( CHMI ) reporting the steepest declines.

{kind=link}

Only about half of the residential mREITs reported distributable EPS that covered their Q1 dividend, leading to dividend reductions from another six mREITs since the end of the quarter - reductions that averaged around 20% - bringing the full-year total across the sub-sector to ten. Nearly all of the reductions were foretold either directly or indirectly in earnings call commentary. After incorporating these dividend reductions, and using the analyst consensus EPS estimate for full-year 2023, the sector payout ratio has returned to around 90%, down from 115% before these reductions. The average residential mortgage REIT now pays a dividend yield of 12.8%.

{kind=link}

On the commercial mREIT side, the movement in BVPS has been more muted throughout the pandemic, but increased loan loss reserves - particularly in the office sector - offset tailwinds from these REITs' floating-rate loans. Commercial mREITs reported just a 6.5% decline in BVPS at the depths of the pandemic and most of the larger REITs have now recovered all of these declines. Commercial mREITs weren't facing the same "existential crisis" as their residential mREIT peers, but the sector's exposure to the hotel, office, and retail sectors dragged on performance early in the pandemic. Arbor Realty ( ABR ) was the upside leader in Q1 earnings season after reporting strong results and raising its dividend by 5%, one of four commercial mortgage REIT to raise its dividend this year. Results from a handful of office-focused lenders showed that the grave concern over a wave of office loan defaults might be a bit premature. Blackstone Mortgage ( BXMT ) has been among the better-performers after reporting adjusted EPS of $0.79/share - covering its $0.62/share dividend - and noting that it collected 100% of interest payments in Q1 with no defaults despite its office-heavy loan portfolio.

{kind=link}

Commercial Mortgage REITs now pay an average dividend yield of 11.7% with a similar EPS payout ratio of around 95%. Three commercial mREITs have raised their dividend this year: Abor Realty , Hannon Armstrong , and Seven Hills, while a handful of names raised their payouts in late 2022, including Ladder Capital , and BrightSpire Capital . While we haven't yet seen any commercial mREIT lower its payout in 2023 aside from cannabis mREIT AFC Gamma ( AFCG ), we did see three commercial mREITs reduce their dividends in late 2022 including Granite Point , Lument Finance , and Ready Capital . Our review of earnings call commentary found a high degree of confidence in covering dividends among the larger and mid-sized commercial mREITs, but one commercial mREITs - Sachem Capital ( SACH ) - indicated that a dividend reduction was likely for this coming quarter.

{kind=link}

Mortgage REIT Risks & Balance Sheets

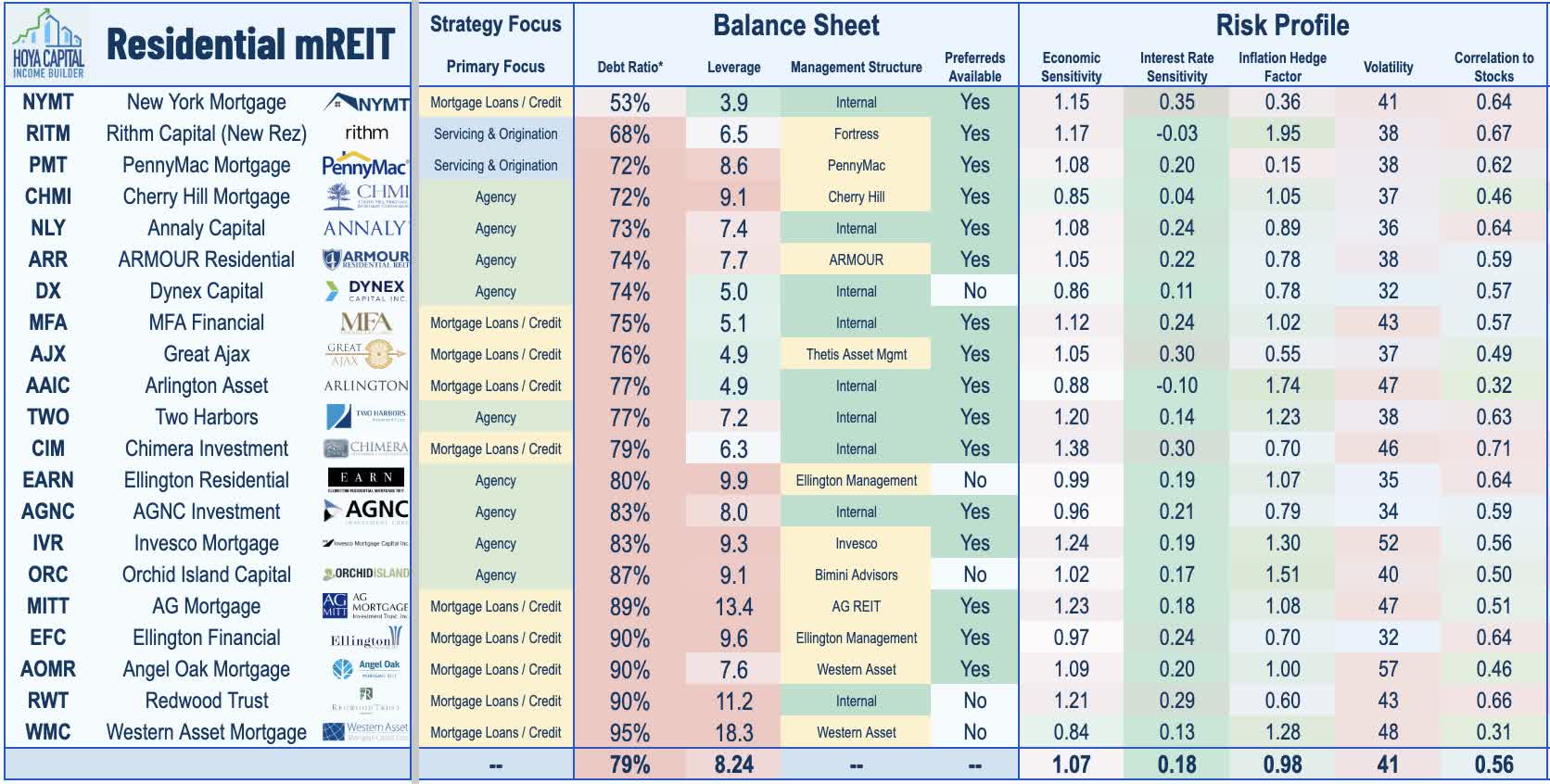

Using our REIT Risk Profile for every mREIT in our coverage universe, we note the leverage ratios and variations in risk exposures faced by these 21 residential mortgage REITs - sorted by volatility. Of note, the larger Agency-focused mREITs, including Annaly Capital ( NLY ) and AGNC Investment ( AGNC ) tend to exhibit lower levels of volatility and economic sensitivity but tend to be more interest rate sensitive while non-Agency mREITs including New Residential (RITM) tend to exhibit higher volatility but also tend to be less interest rate sensitive. Smaller-cap mREITs and those that employ a higher degree of balance sheet leverage tend to exhibit very high volatility while also exhibiting a high degree of economic and interest rate sensitivity.

{kind=link}

Looking at the commercial mREIT side, we see similar levels of variation within the sector, which generally reflects the property focus of these REITs. Larger commercial mREITs that focus primarily on residential lending - including Starwood Property ( STWD ), KKR Real Estate ( KREF ) - tend to exhibit more "defensive" investment attributes while mREITs with more office and hotel exposure like Apollo Commercial ( ARI ) - and those that use higher leverage than their peers like ACRES Realty ( ACR ) - tend to be more pro-cyclical in their investment characteristics. While real estate-backed loans are strong and stable collateral that allow higher levels of leverage, we urge caution with REITs with Debt Ratios above 80%.

{kind=link}

Takeaway: Less 'Scary' Than Headlines Suggest

Recovering from a sharp sell-off in the wake of the Silicon Valley and First Republic Bank collapses, Mortgage REITs have rebounded as turmoil in interest rate markets has calmed. Distress in the commercial and residential real estate markets has been more isolated than the 'scary' magazine covers would suggest. Outside of urban office properties, default rates remain near pre-pandemic lows. The squeeze on highly-levered private market portfolios is still in the early innings, but an orderly unwind remains the base case and public equity REITs with balance sheet firepower should eventually scoop up many debt-burdened privately-held assets. Like high-yield corporate credit, mortgage REITs are highly sensitive to macroeconomic shocks, but several higher-quality mREITs appear overly discounted and poised to deliver attractive income-heavy total returns as COVID-era shocks dissipate.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Mortgage REITs: High-Yield Risk And Opportunity