SEVN - Mortgage REITs: High Yields Are Fine For Now

Summary

- Mortgage REITs - which were left for dead amid a historically brutal year across fixed-income markets - have rebounded in recent weeks as earnings results were not as catastrophic as feared.

- Mortgage REITs are now outperforming Equity REITs for the year, and we continue to see value in a modest allocation towards higher-quality mREITs in a balanced income-focused real estate portfolio.

- Despite paying average dividend yields in the mid-teens, the majority of mREITs were able to cover their dividends as improved earnings power from wider investment spreads offset book value declines.

- As expected, Book Value declines averaged double-digits for Agency-focused residential mREITs, but hybrid mREITs reported muted declines while most commercial mREITs reported BVPS accretion, benefiting from their focus on floating rate lending.

- Everything in Moderation: While most mREITs stand on relatively solid footing with enough earnings power to maintain their hearty dividend yields, sharp changes in rates in either direction can wreak havoc on mREITs that are caught over-levered or improperly hedged.

REIT Rankings: Mortgage REITs

This is an abridged version of the full report published on Hoya Capital Income Builder Marketplace on November 14th.

{kind=link}

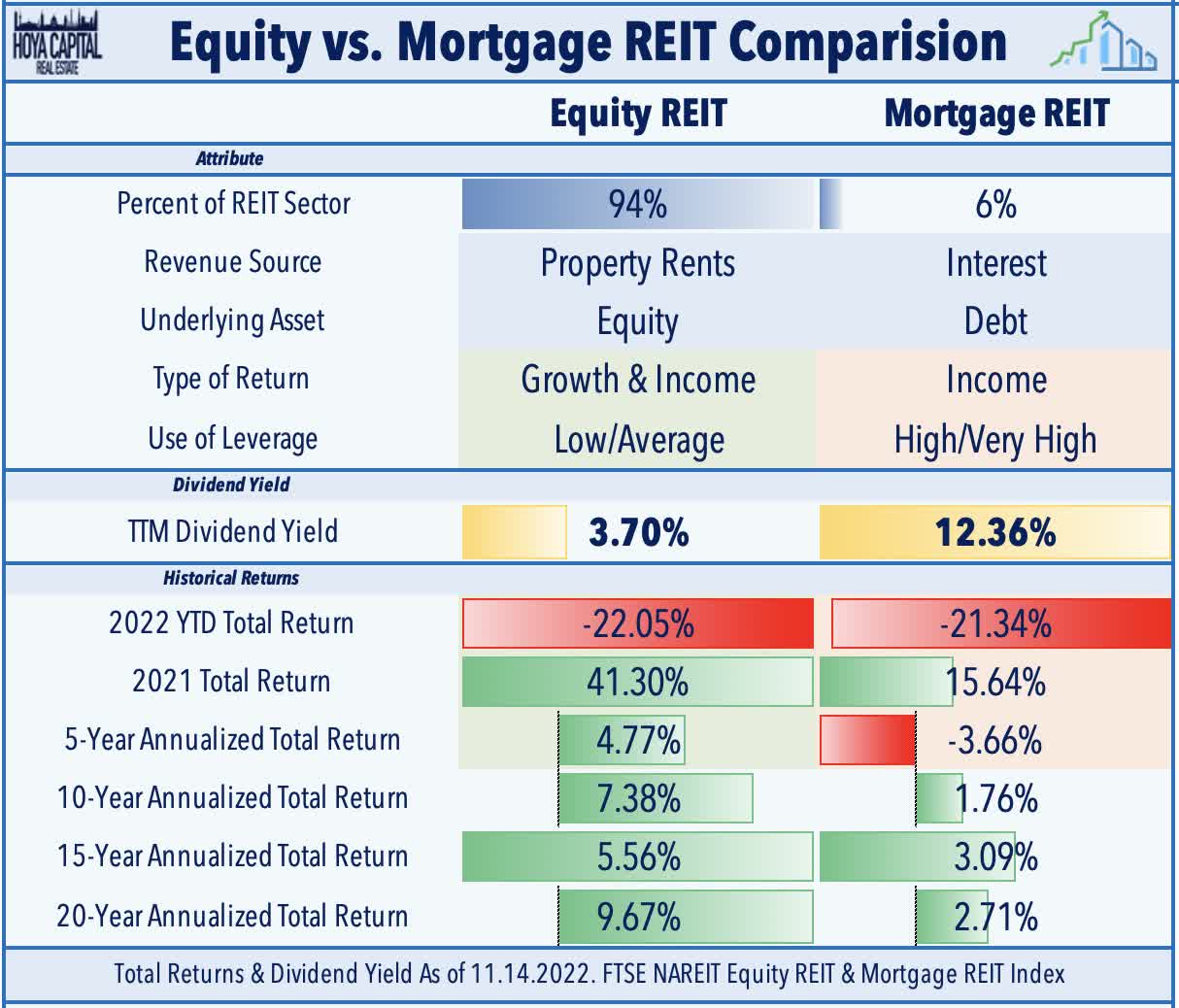

Best known for their hearty dividend yields that often breach double digits, Mortgage REITs - also called mREITs - comprise roughly 5% of the total REIT universe. Often viewed as a distinct asset class from equity REITs which own, operate, and collect rent on real estate properties, mortgage REITs function more like a lending bank by originating and investing in interest-bearing real estate debt instruments. After a wave of dividend cuts in early 2020, mortgage REITs have regained their footing over the past two years and despite the historically brutal year for fixed-income securities in 2022 - the dividend momentum has continued into 2022 with twice as many dividend hikes as dividend cuts this year. Mortgage REITs now pay an average yield of 12.4%, a hearty premium to the 3.7% dividend yield paid by the average Equity REIT.

{kind=link}

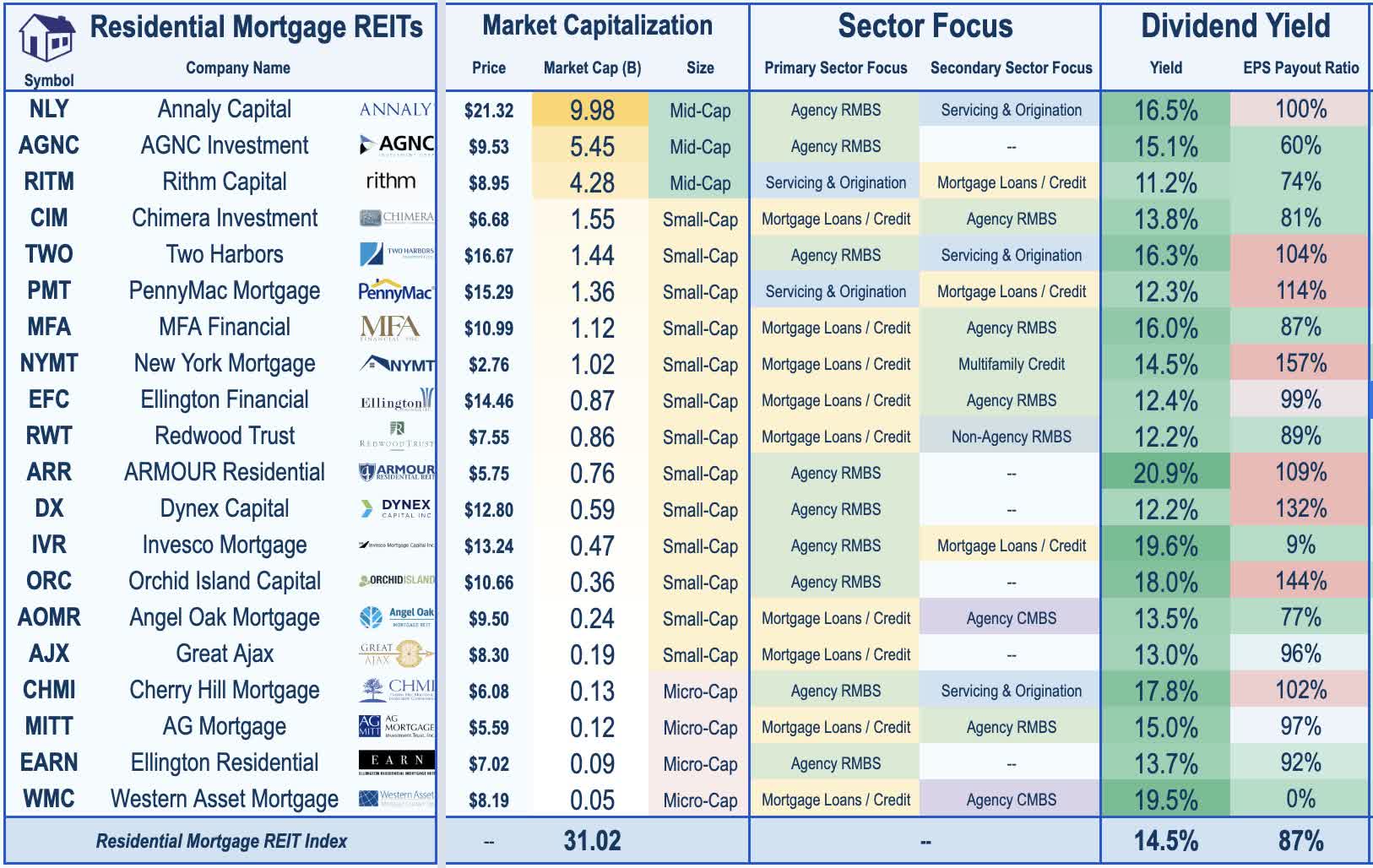

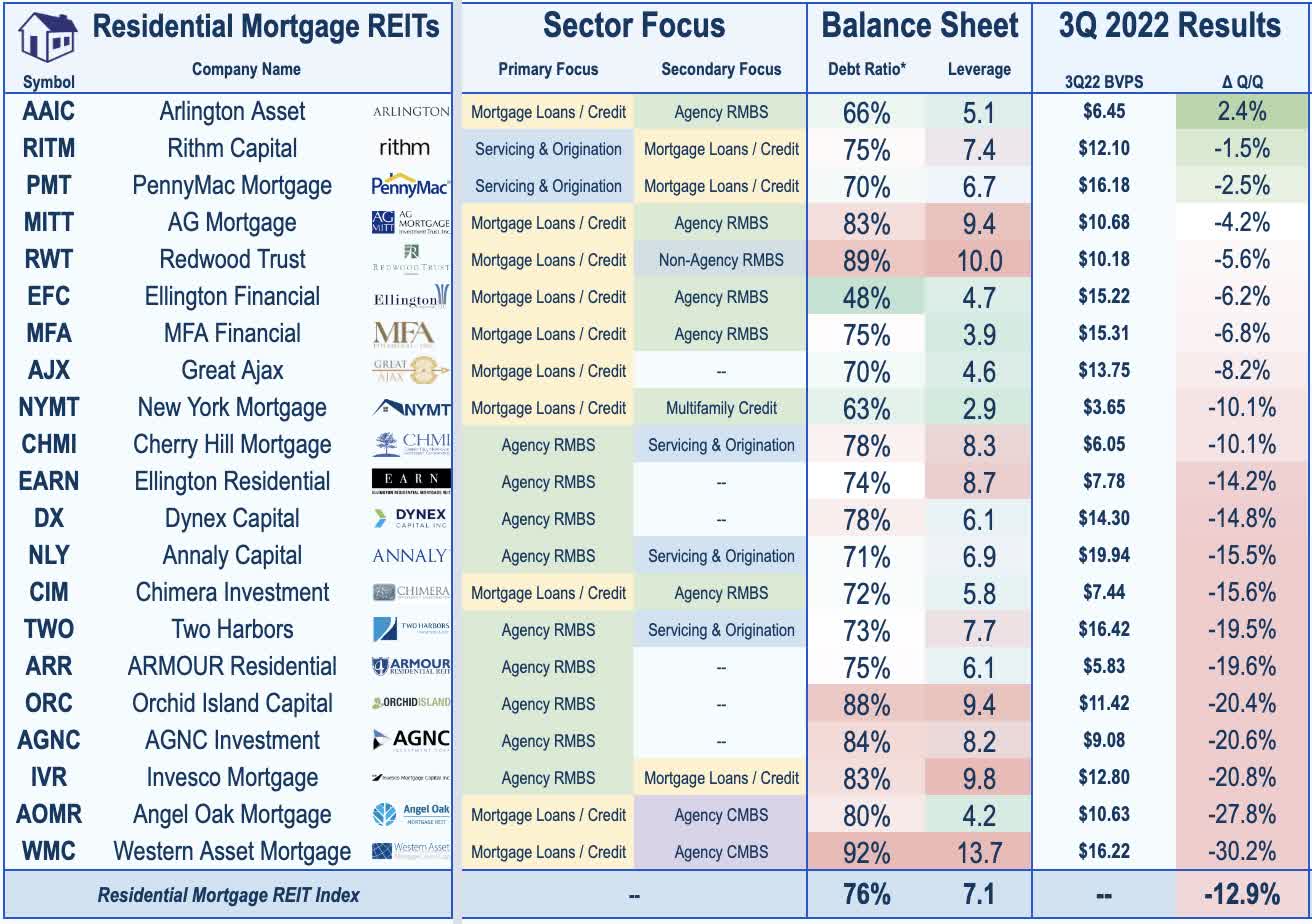

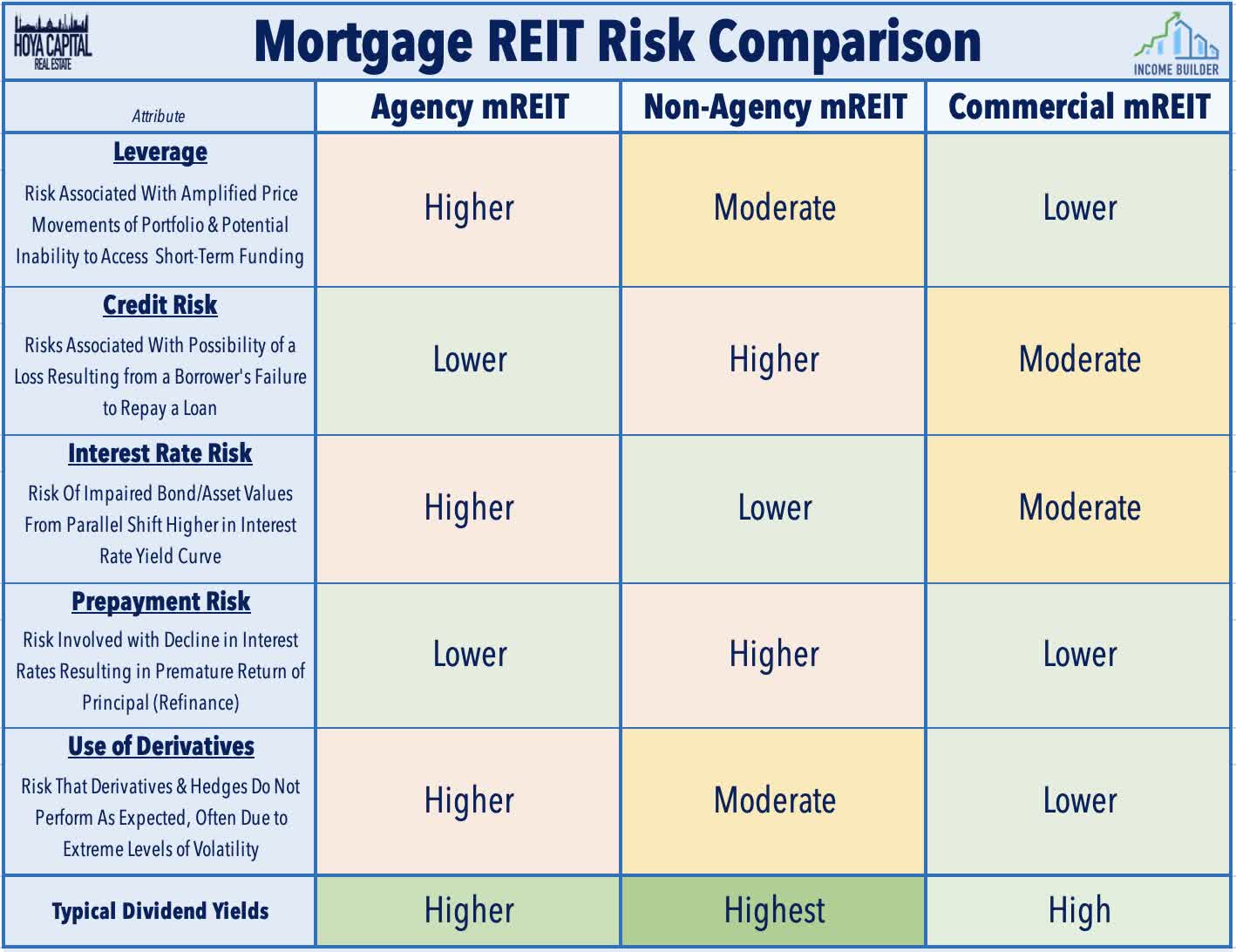

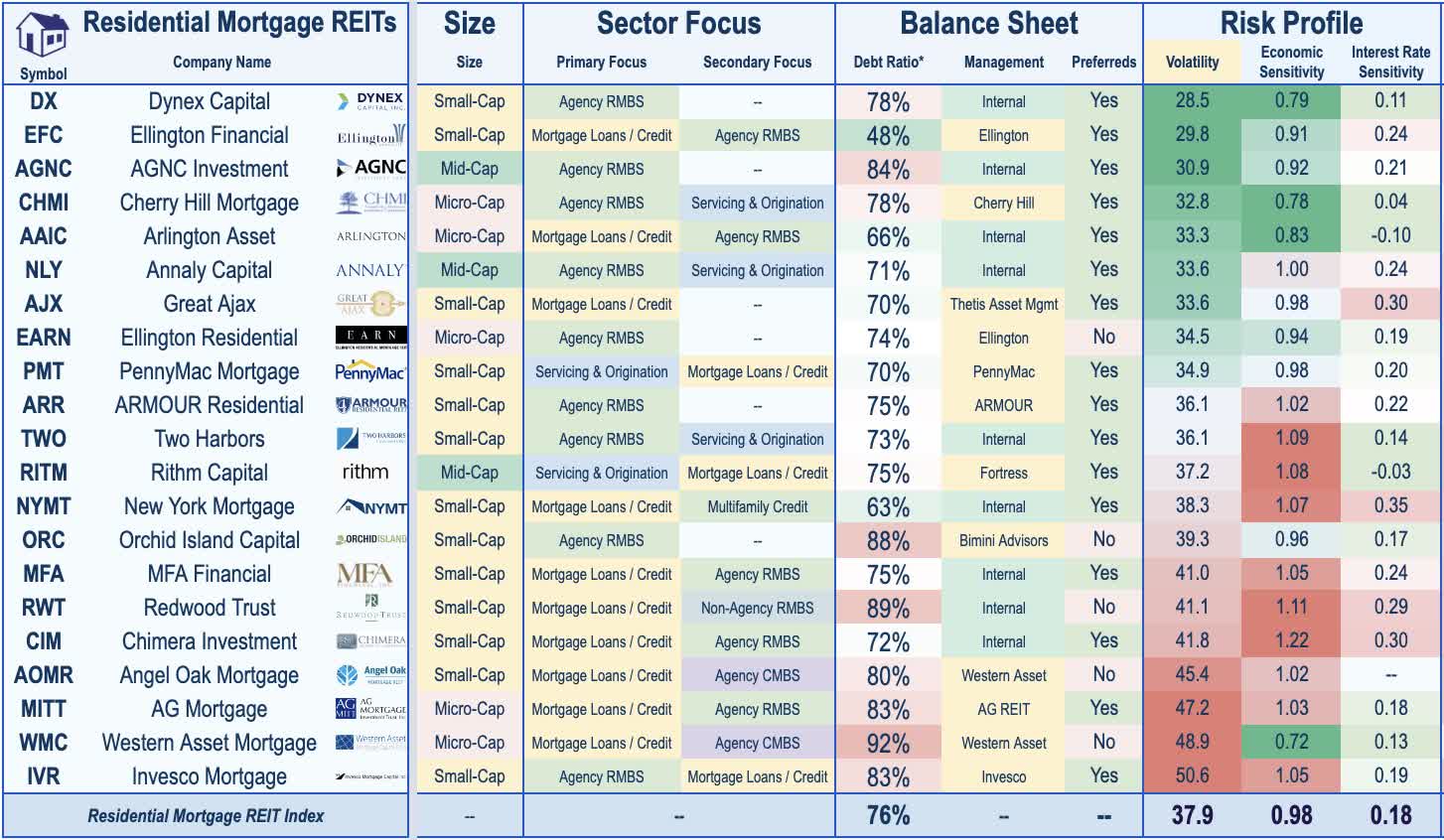

In the Hoya Capital Residential Mortgage REIT Index , we track the 21 exchange-listed residential mREITs that currently pay dividend yields averaging 14.5%. Agency mREITs invest primarily in agency mortgage-backed securities, or RMBS, which have their principal guaranteed by a Government-Sponsored Enterprise, or GSE, such as Fannie Mae, Freddie Mac, or Ginnie Mae, and thus bear minimal credit risk but tend to be more sensitive to changes in interest rates. Non-agency mREITs invest in RMBS and other types of residential credit that are not guaranteed by a GSE, including mortgage servicing rights (MSRs) and whole mortgage loans, which bear higher levels of credit risk but tend to be less sensitive to interest rates.

{kind=link}

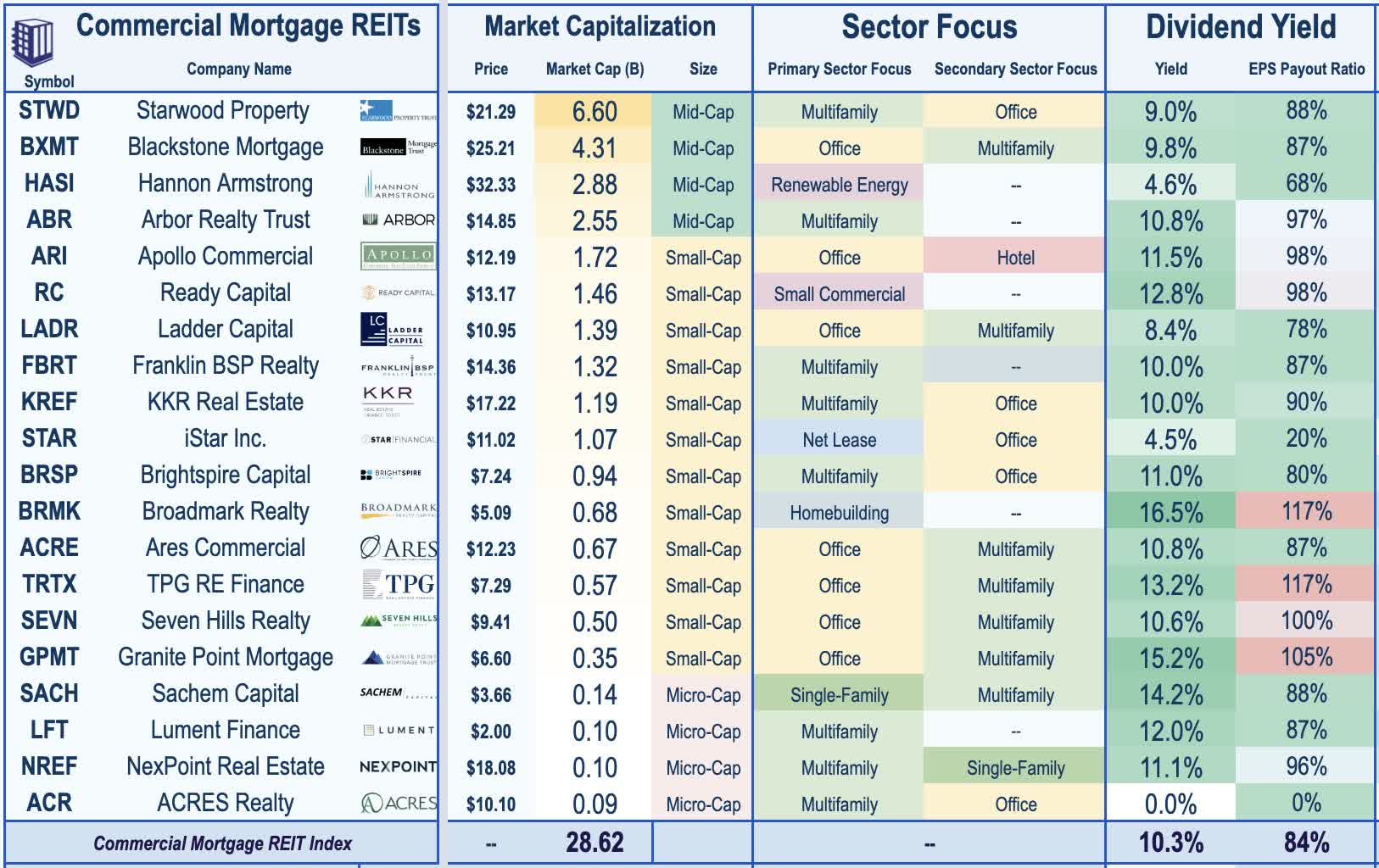

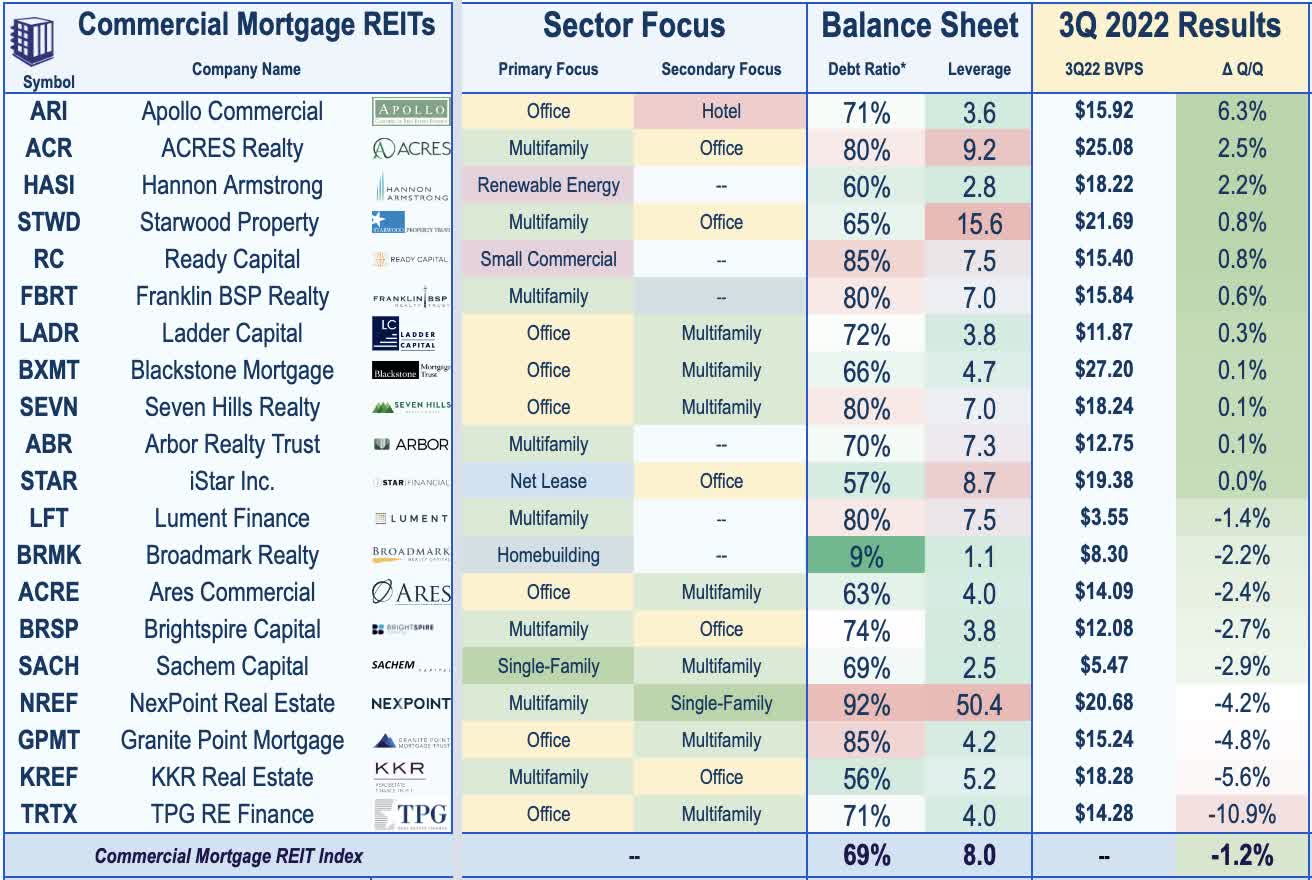

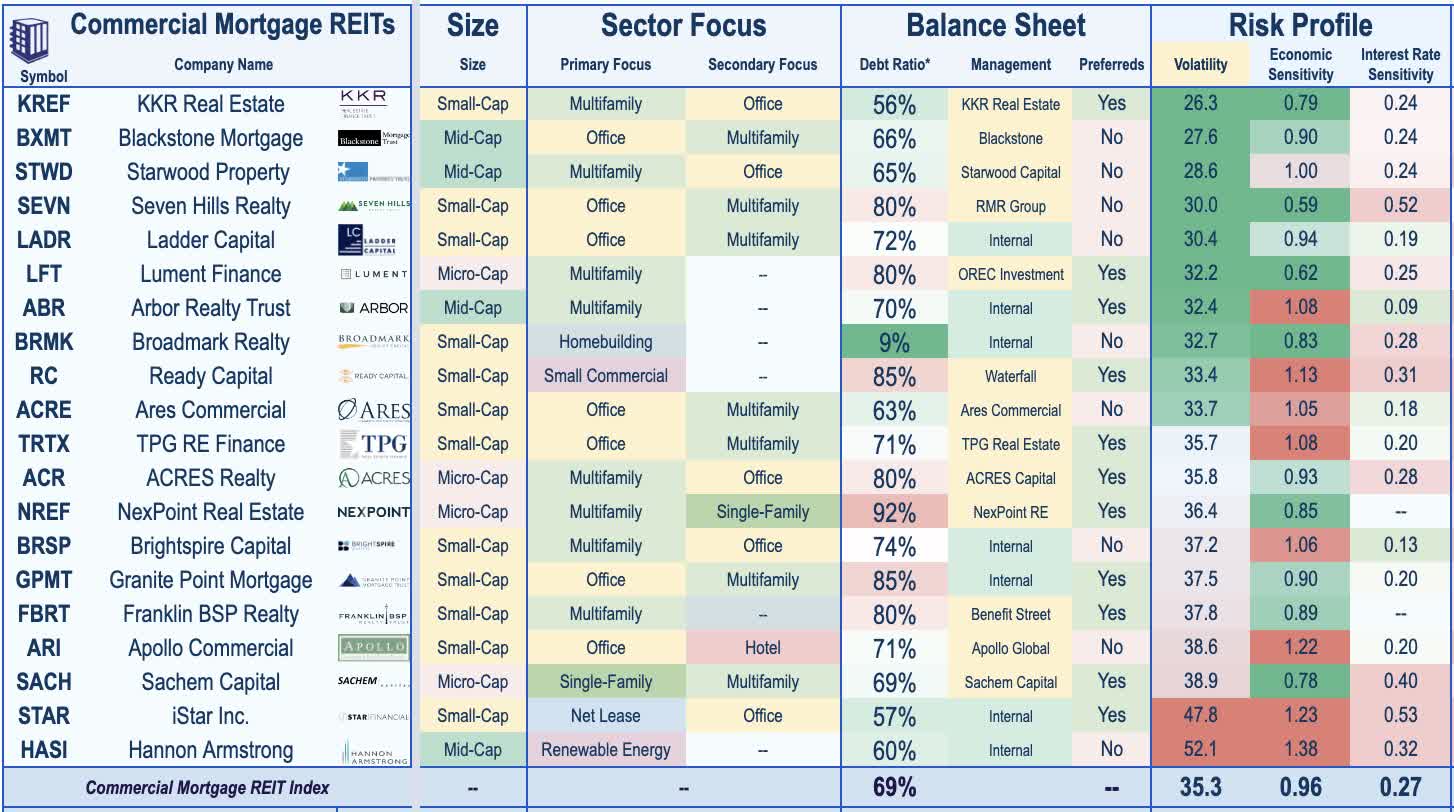

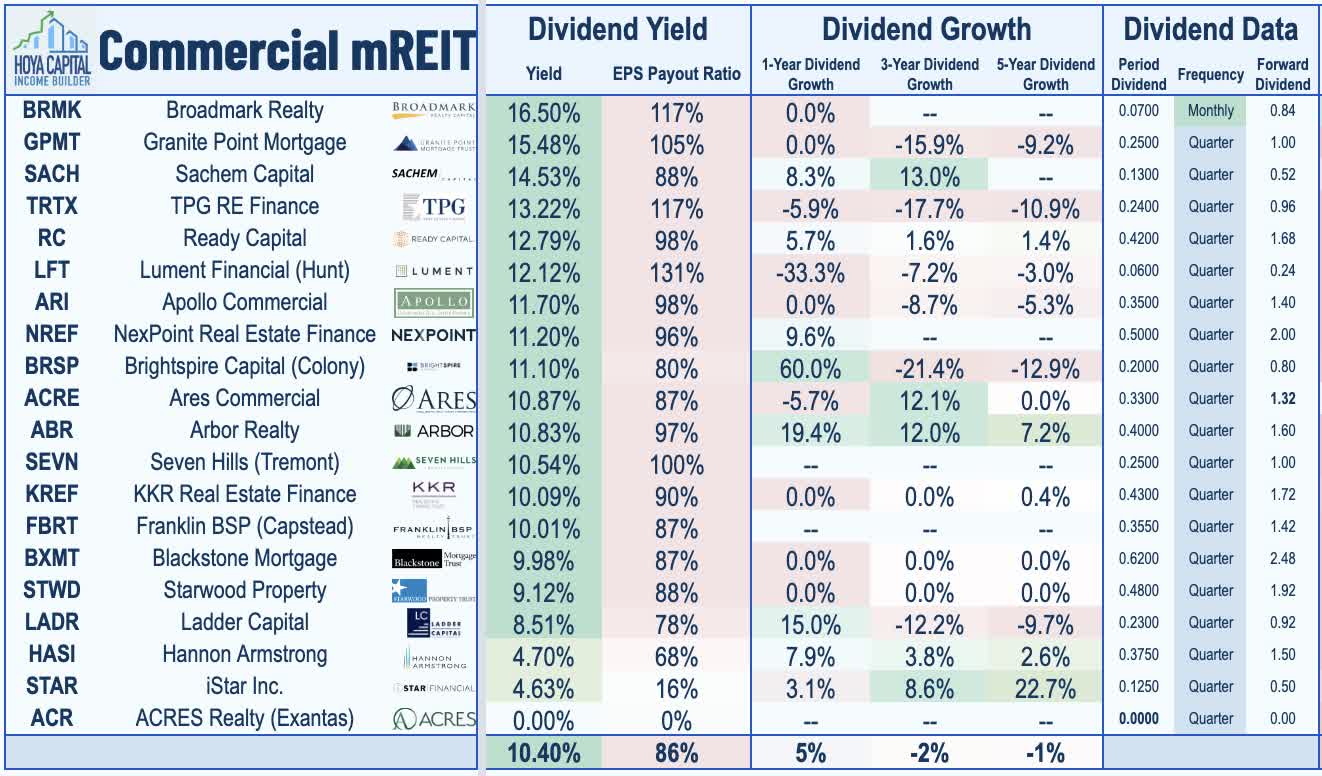

In the Hoya Capital Commercial Mortgage REIT Index , we track 20 exchange-listed commercial mREITs that currently pay dividend yields averaging 10.3%. Similar to equity REITs, commercial mREITs tend to focus on one or a small handful of property sectors and tend to take on relatively lower levels of leverage compared to residential mREITs. Commercial mREITs can also be further segmented into two categories: pure Balance Sheet Lenders, which originate and purchase loans for their own balance sheet, and Conduit Lenders , which originate and purchase loans both to hold on their own balance sheet and also for the purposes of securitizing the loans into a CMBS or other vehicle. We track two additional mREITs AFC Gamma ( AFCG ) and Chicago Atlantic ( REFI ) in our Cannabis REIT report.

{kind=link}

Mortgage REIT Performance & Earnings

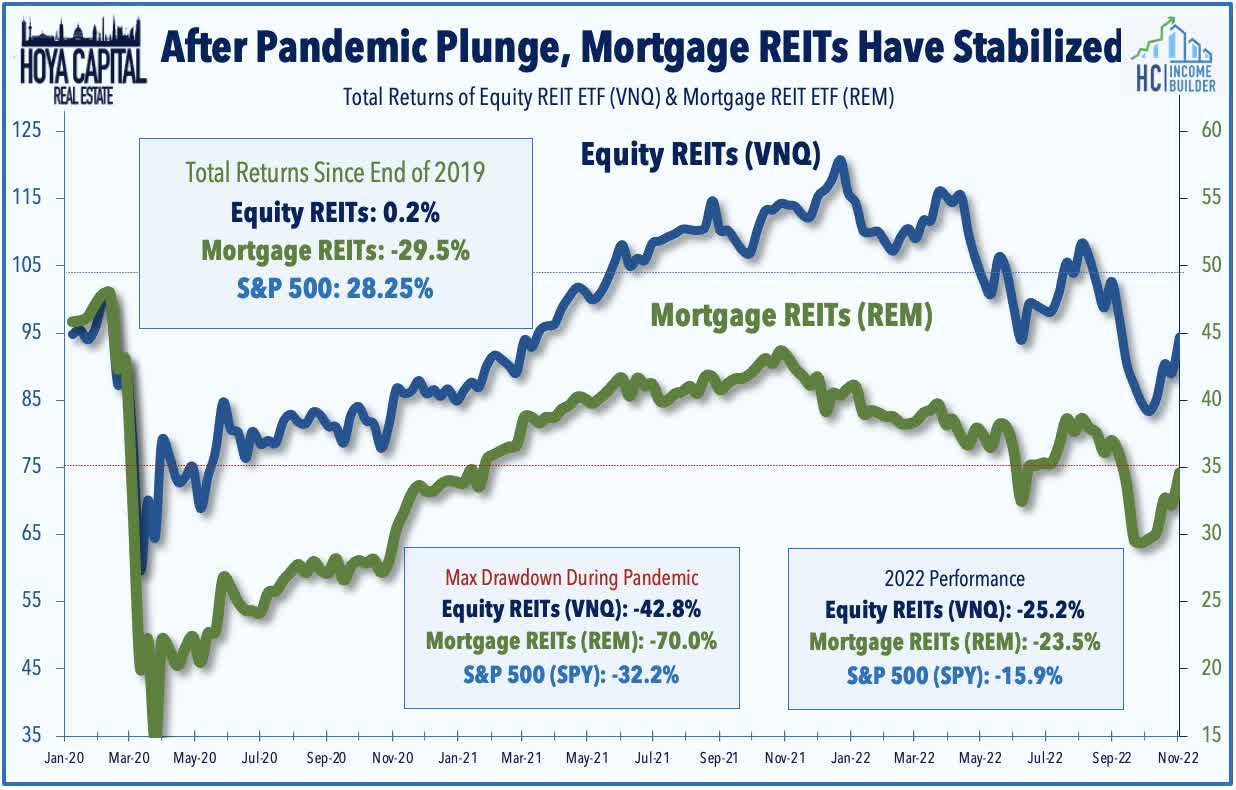

After dipping as much as 40% on a year-to-date basis at their lows in October, Mortgage REITs have rebounded in recent weeks amid early signs of peaking inflationary pressure and after earnings results were not as catastrophic as many feared amid an otherwise brutal year across fixed income markets. Mortgage REITs endured punishing declines of 50-70% during the depths of the pandemic as the sharp plunge in interest rates wreaked havoc on mREITs that were caught over-levered and improperly hedged - triggering a cascading wave of forced selling that resulted in permanent Book Value declines for many mortgage REITs - but similar signs of stress have been limited to a small number of highly-levered mREITs. For the year, the iShares Mortgage REIT ETF ( REM ) is lower by 23.5% on a total return basis compared to the 25.2% decline on Vanguard Equity REIT ETF ( VNQ ).

{kind=link}

Through early October, many investors feared that mortgage REITs were on a similarly troubled trajectory as the pandemic-era turmoil amid the historically brutal year for bond markets with the Bloomberg US Aggregate Bond Index on its way to its worst year on record. The iShares MBS ETF ( MBB ) and the iShares CMBS ETF ( CMBS ) - the benchmarks tracking the un-levered performance of residential and commercial mortgage-backed bonds - had recorded similarly-historically-large drawdowns of 15% in mid-October, but both have rebounded over the past month amid signs of slowing economic activity and waning inflationary pressures. Despite the rebound, the roughly 12% decline would be the worst full-year performance for MBB and CMBS since their inception in 2007 and 2012, respectively.

Hoya Capital

Consensus expectations called for Book Value Per Share ("BVPS") declines of up to 20% in Q3 during a particularly rough quarter for mortgage-backed securities - but mREITs have rebounded sharply since the start of earnings season. BV declines were more muted for credit-focused mREITs compared to pure-play agency-focused mREITs with particularly solid results from PennyMac ( PMT ) and Rithm Capital ( RITM ). Among the agency-focused mREITs, BVPS declines ranged from 10%-30%, but EPS metrics were generally "less ugly" than BV metrics with most agency mREITs still able to cover their dividends, including a strong report from Annaly ( NLY ), which noted that its Earnings Available for Distribution (“EAD”) of $1.06/share still comfortably covers its dividend yield of nearly 20%. The average residential mREIT now trades at a 15.6% discount to its last reported BVPS.

{kind=link}

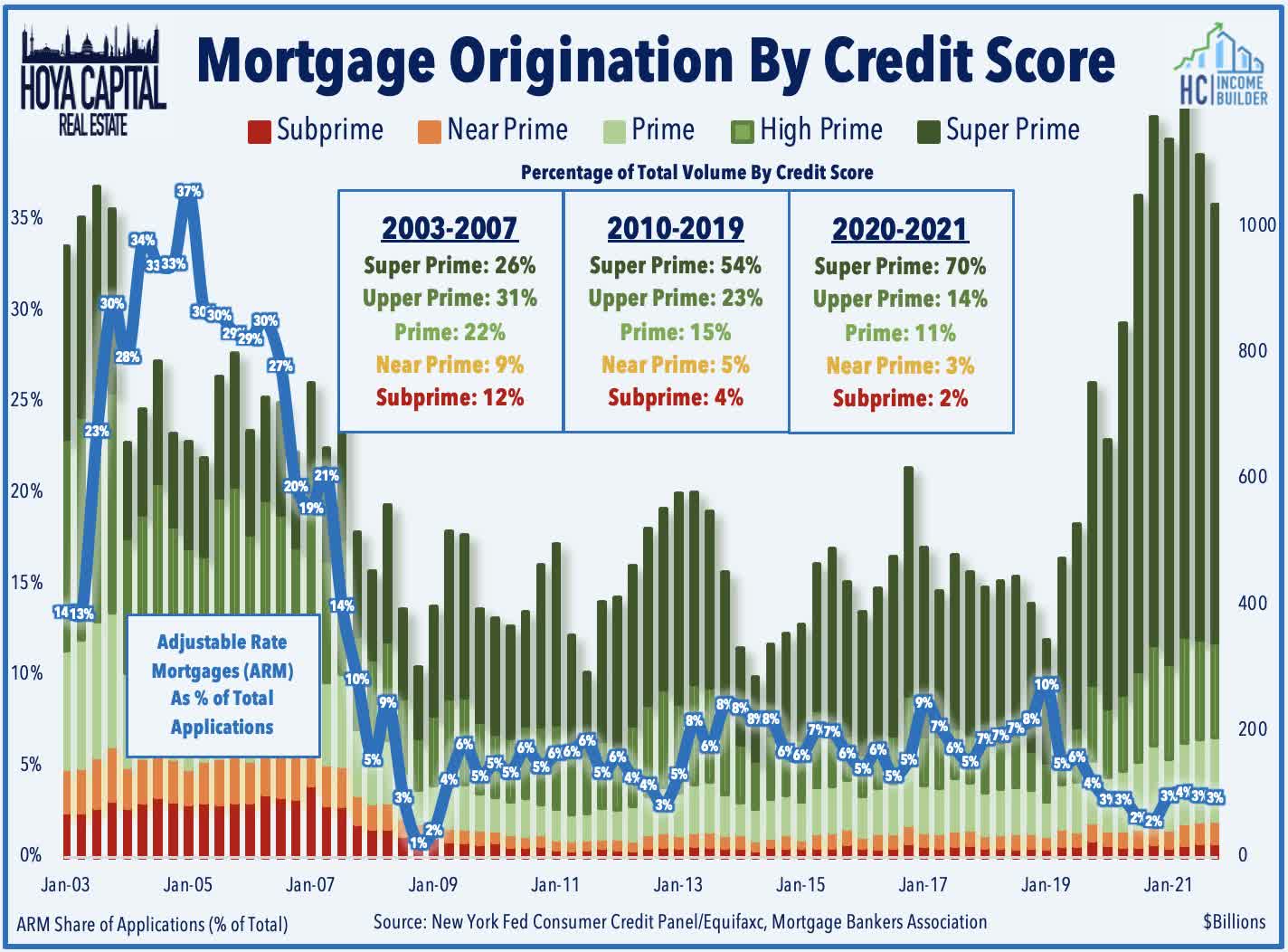

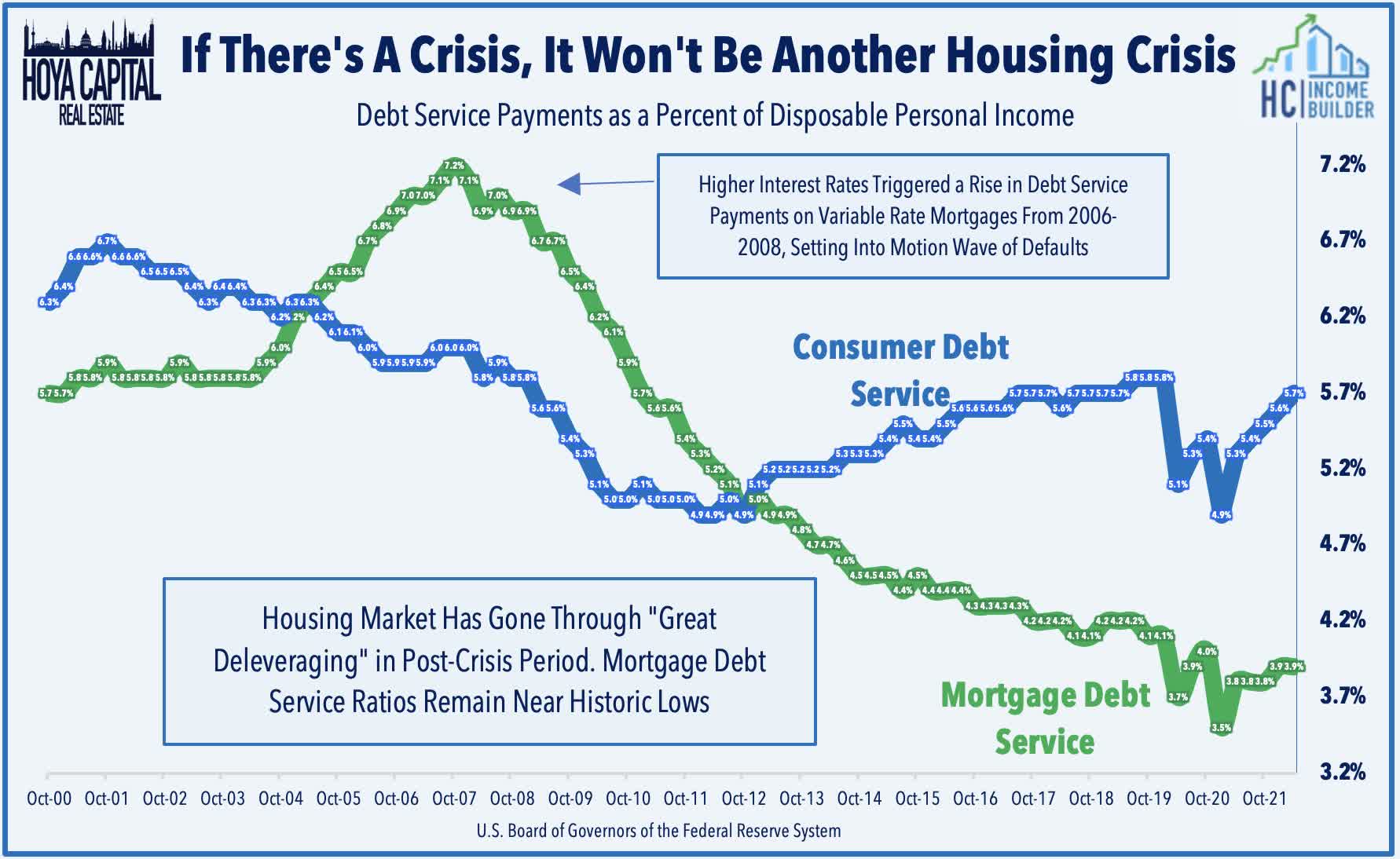

Looking more broadly at the macro environment, as the Federal Reserve intended , rising mortgage rates have indeed poured icy-cold water over the previously red-hot housing market in recent months. The recent cooldown has renewed the perennial "Bubble" calls from pundits , but fundamentals suggest that national housing markets are instead more likely to see a somewhat "boring" return to normalcy ahead similar to 2018-2019 when rising mortgage rates resulted in a notable near-term slowdown in buying activity. Importantly, subprime loans and adjustable-rate mortgages - the dynamite that led to a cascading financial market collapse in 2008 - have been essentially non-existent throughout this cycle. Adjustable-rate mortgages - which would be most "at-risk" from the surge in rates have accounted for less than 5% of mortgages originated since 2009, down from nearly 30% at the peak in 2005.

{kind=link}

On the commercial mREIT side, the movement in BVPS has been far more muted - and even positive from the REITs that focus primarily on floating rate lending. Apollo Commercial ( ARI ) soared after reporting better-than-expected results including a 6% rise in its BVPS to $16.12. Blackstone Mortgage ( BXMT ) - which owns a similar book of floating-rate loans - reported a 1% rise in its BVPS while noting that its average loan rates increased 100 basis points in Q3 alone while Starwood ( STWD ) also reported a modest BVPS increase during the quarter. Also of note, Arbor Realty ( ABR ) rallied after reporting strong Q3 results and raising its dividend for the fourth time this year. Downside laggards this quarter included KKR Real Estate ( KREF ) and TPG Real Estate ( TRTX ) which each reported BVPS declines of over 5% while Broadmark ( BRMK ) dipped after reporting disappointing results with an increase in loans under default. The average commercial mREIT now trades at a 26% discount to its last reported BVPS.

{kind=link}

Commercial mREITs reported just a 6.5% decline in BVPS at the depths of the pandemic and have recovered most of these declines over the subsequent five quarters. Commercial mREITs weren't facing the same "existential crisis" as their residential mREIT peers, but the sector's exposure to the hotel, office, and retail sectors dragged on performance early in the pandemic. Rent collection rates across these commercial sectors fully normalized by mid-2021 and the office, multifamily, and retail sectors have seen some of the strongest acceleration in same-store metrics over the past several quarters.

{kind=link}

Mortgage REIT Risks

Despite their volatility over the past several years, mortgage REITs don't necessarily deserve their "ugly duckling" status within the REIT sector, but it's important to keep in mind that mortgage REITs are not monolithic in their risk exposures. Mortgage REITs typically operate with a high degree of leverage to amplify investment spreads and often use short-term hedging instruments to manage interest rate and credit exposure, which makes each REIT rather unique in its end-exposure to certain macroeconomic environments. In general, similar to high-yield corporate credit, mortgage REITs tend to perform their best in "boring markets" - periods of lower interest rate and stock market volatility. Below, we define the five primary risk exposures faced by these different types of mortgage REITs: leverage risk, credit risk, interest rate risk, prepayment risk, and derivative risk.

{kind=link}

Using our REIT Risk Profile for every mREIT in our coverage universe, we note the leverage ratios and variations in risk exposures faced by these 21 residential mortgage REITs - sorted by volatility. Of note, the larger Agency-focused mREITs including Annaly Capital ( NLY ) and AGNC Investment ( AGNC ) tend to exhibit lower levels of volatility and economic sensitivity but tend to be more interest rate sensitive while non-Agency mREITs including New Residential ( NRZ ) tend to exhibit higher volatility but also tend to be less interest rate sensitive. Smaller-cap mREITs and those that employ a higher degree of balance sheet leverage tend to exhibit very high volatility while also exhibiting a high degree of economic and interest rate sensitivity.

{kind=link}

Looking at the commercial mREIT side, we see similar levels of variation within the sector which generally reflects the property focus of these REITs. Larger commercial mREITs that focus primarily on residential lending - including Starwood Property ( STWD ), KKR Real Estate ( KREF ) - tend to exhibit more "defensive" investment attributes while mREITs with more office and hotel exposure like Apollo Commercial ( ARI ) - and those that use higher leverage than their peers like ACRES Commercial Realty ( ACR ) - tend to be more pro-cyclical in their investment characteristics. While real estate-backed loans are strong and stable collateral that allow higher levels of leverage, we urge caution with REITs with Debt Ratios above 80%.

{kind=link}

Mortgage REIT Dividends Likely Safer Than Feared

Recall that the mREIT sector faced a "dividend cut bloodbath" in 2020 as 30 mREITs reduced or suspended their dividend including all-but-one residential mREIT and half of the commercial mREITs. The pandemic-driven wave of dividend cuts gave way to a similar powerful wave of dividend hikes last year with more than two dozen mREIT dividend hikes. That momentum has continued into 2022 with another dozen dividend hikes - double the quantity of mREITs that have reduced their payouts. While many mREITs' payout ratios are pushing their upper limits, earnings call commentary indicated that most mREITs see their current distribution levels as sustainable given the improved earnings potential in the wider spread environment and from hedge-related income that is not included in GAAP EPS metrics.

{kind=link}

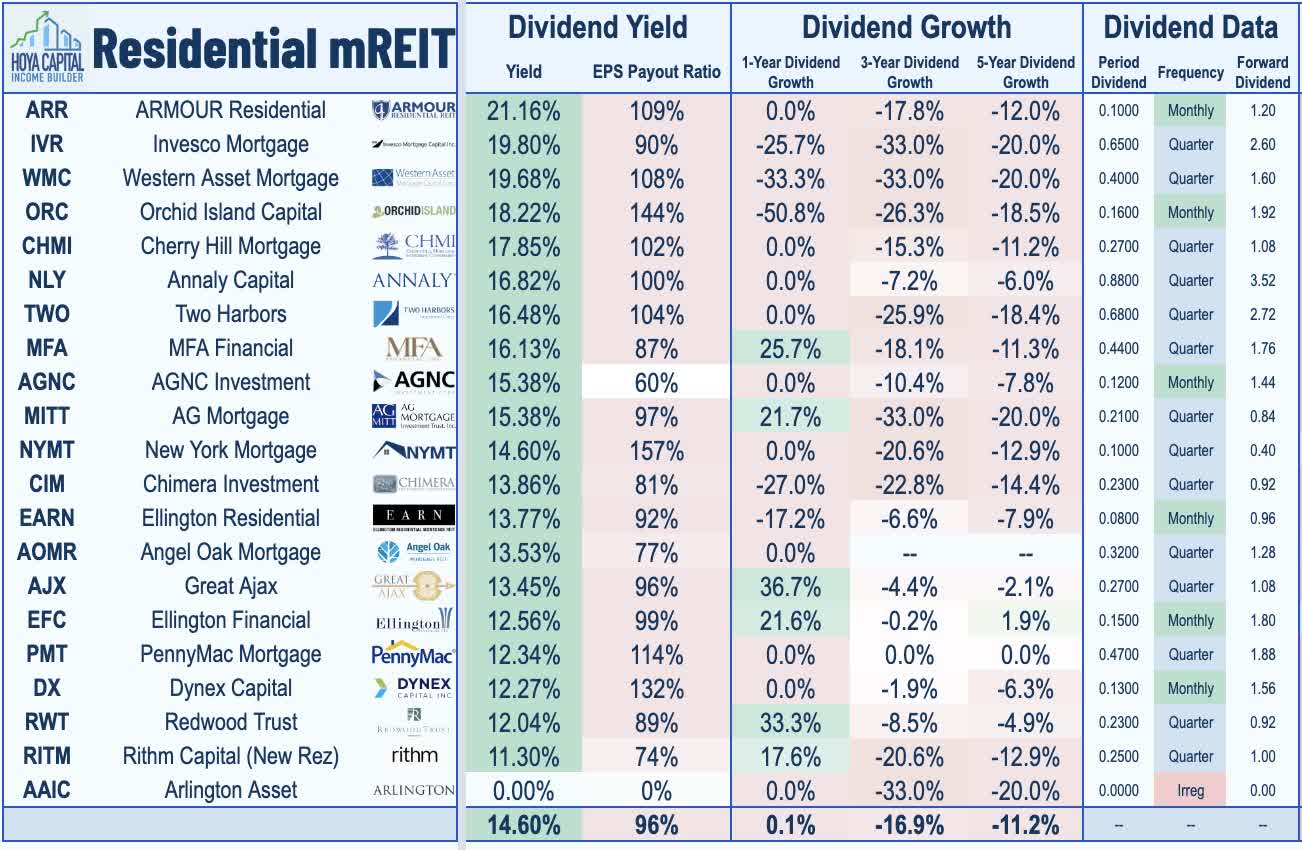

Residential mortgage REITs now pay an average dividend yield of 14.6% at an average EPS payout ratio of 96% with 14 of the 21 REITs currently covering their distribution. Among the mREITs that are currently not covering their dividend, there was a mix of strategies expressed with some REITs hinting at a likely dividend cut while others committed to holding steady at current levels. We compiled some relevant commentary below from earnings calls, focusing on 7 residential mREITs that are at or above 100% payout levels.

{kind=link}

| ARR |

| "The outlook for dividends appears to be stable based on current conditions." |

| NYMT |

| "We've already announced the $0.10 dividend and looking at the 18-month forecast, we feel that we can support that dividend over time." |

| DX |

| "Substantial hedge gains exist in the portfolio to support our forward dividend." |

| ORC |

| "[Including hedges], the economic net interest income was very much in line with the dividend ." |

| WMC |

| "We are well positioned to generate consistent distributable earnings with the objective of supporting our dividend in the quarters ahead." |

| TWO |

| "The outlook supports the current dividend, but we'll make those decisions based on market conditions." |

| PMT |

| "The dividend level [currently $0.47] will be driven primarily by projections of PMT's earnings potential, with a bias towards dividend stability. We expect the quarterly run rate to average $0.41 per share." |

On the other side of the sector, Commercial Mortgage REITs now pay an average dividend yield of 10.4% at a more modest average EPS payout ratio of 86% while just four mREITs at or above 100%. We compiled the relevant commentary from REITs at-or-above 100% payout levels below.

{kind=link}

| RC |

| "Our Board of Directors plans to realign the dividend in the fourth quarter to ensure our go-forward dividend is covered by normalized distributable earnings." |

| BRMK |

| "Our shareholders expect dividends. Our goal is to set a dividend that’s sustainable over time and covered by distributable EPS." |

| ARI |

| "The robust pace of originations over the past 18 months will enable the company to continue generating distributable earnings that support the common stock dividend" |

| TRTX |

| "Our mission is to prudently deploy capital for the benefit of our shareholders, and position ourselves to increase the quarterly dividend when appropriate. I believe we're well-positioned to do so." |

Takeaways: Everything in Moderation

Mortgage REITs - which were 'left for dead' amid a historically brutal year across fixed income markets - have rebounded over the last month as earnings results were not nearly as catastrophic as many feared. Despite paying average dividend yields in the mid-teens, the majority of mREITs were able to cover their dividends in Q3 as improved earnings power from wider investment spreads and hedging gains offset the immediate negative impact on loan book values. While most mREITs stand on relatively solid footing with loan default rates still near historic lows, sharp changes in rates in either direction can wreak havoc on mREITs that are caught over-levered or improperly hedged, and we continue to emphasize that an extra level of diligence is essential when investing in mREITs as BVPS declines can be "temporary" for well-managed portfolios with reasonable leverage and effective hedges, but BVPS declines can become "permanent" for less-prepared and over-extended mREITs.

{kind=link}

For an in-depth analysis of all real estate sectors, be sure to check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Mortgage REITs: High Yields Are Fine, For Now