CHTR - Motiwala Capital - 2022 Letter: US Capital Appreciation

Summary

- Motiwala Capital is an independent, fee-only Registered Investment Advisor based in Texas. We provide equity portfolio management services to individuals.

- We discuss portfolio performance, top 10 positions and new investments.

- Our portfolio exhibits diversification via Peter Lynch categories.

2022 Letter: US Capital Appreciation

Dear Investors,

2022 was another year of unusual global events with the war in Ukraine. Globally most equity markets declined including the US stock market, bonds also lost value and interest rates increased sharply with raging inflation. Our core US capital appreciation strategy returned -11.9% net of fees. US markets had a losing year after a long time with the S&P 500 index total returns (including dividend) of -18.1%. The portfolio diversification across sectors/industries as well as the defensiveness of the stalwarts and slow grower Lynch categories helped in the relative performance of the portfolio v/s the indices in 2022.

2022 Performance

Detractors: The two positions that mainly detracted from performance were Facebook ( META , -6%), and Google ( GOOG , GOOGL , -4.3%). Other positions that hurt performance include Charter Comm ( CHTR , -1.5%), SSNC (-1%) and Microsoft ( MSFT , -1%). The outsized loss in Meta and Google were due to the large position sizes and large drops experienced in their share prices.

Winners: Positions that contributed positively to performance included Cigna ( CI , +1.9%), Swedish Match ( SWMAY ,+0.8%), All State (0.6%), Omnicom ( OMC , 0.6%), HDFC Bank ( HDB , +0.6%). Even though there were more winners than losers, the winners as a group could not make up for the outsized declines in the largest two positions.

Cash: Given we do not take short positions, in times when the risk reward is not favorable and doing nothing is a reasonable option, we can maintain a larger than normal cash position. As we sold several positions in 2022, most of the proceeds were left as cash. This provided the portfolio some cushion and helped in the relative performance compared to major US indices.

Portfolio Composition

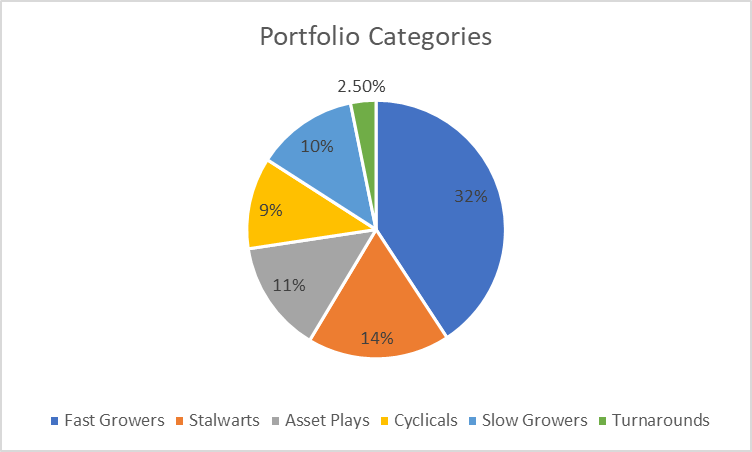

Since Q3 2020, we made changes to the Portfolio composition to follow the approach outlined by Peter Lynch in his wonderful book One Up on Wall Street. He placed the companies into 6 categories based on the maturity stage of the company, its steadiness or underlying nature. See Appendix for an explanation of Fast Growers, Stalwarts, Cyclicals, Turnarounds, Asset Plays and Slow Growers. This framework helps us place the companies in the correct construct and assists in thinking about risk/reward. The % of portfolio in each Lynch category will vary based on the attractiveness of the opportunity set. At year end, the portfolio had 27 positions and 22% cash.

{kind=link}

| ||||||||||||||||||||||||||||||||||||

|

When do we sell?

- When the share price appreciates closer to our estimated range of fair value

- When the company situation changed or we have made an analytical mistake or we lose conviction

- Better opportunities than a current investment present themselves

Portfolio Activity

Positions completely sold

We sold CVS , CBOE , CACI International and Prudential ( PRU ) as their share prices appreciated closer to our estimate of fair value.

The sell decision for Charter communications falls in the category "company situation changed and we lost conviction". Charter announced increased capital expenditures over the next three years to improve its broadband network and rural broadband initiatives. With uncertain payoff on the investment, potentially reduced free cash flow, increasing competition hurting subscriber growth and a high debt load, we decided to book the loss and move on.

Cardinal Health ( CAH ) was sold after five consecutive quarters of poor execution/results. It promptly went on a big run right after we sold. Maybe buying average quality companies requires more patience than we exhibited in this instance. (did you realize that was the 5th company starting with C)

Huntington Ingalls ( HII ) and Lockheed Martin ( LMT ) were sold prior to Russia's invasion of Ukraine as earnings trends were looking unexciting. We ignored the defensive characteristics of these companies (pun intended) and their share prices mounted an excellent offense. Our timing was unlucky.

Science Applications International ( SAIC ) was sold despite a low valuation as it began to match the profile of a slow grower without the attractive dividend payout. On balance, the steady sales and free cash flow profile is one of its attractive elements. We will keep an eye on this for future.

Positions reduced

The following positions were partially sold due to share price appreciation: Bank of New York ( BK ), Interpublic Group ( IPG ), Fidelity National Financial ( FNF ), Elevance Health ( ELV , formerly Anthem).

We sold 10% of the Meta position after disappointing Q4 2021 results and even considered selling it fully but decided to hold majority of the position. Financial results worsened each quarter in 2022 and it is possible this trend may continue in 2023 before we see improvements. Opex and capex spending has been high while revenue growth slowed and then Q3 saw a year over year revenue decline. The market punished the stock by 60% for these results and trimmed the position size for us.

The investment in Vistra Energy was halved with the realization that we may have over estimated the value of this company and the upside may not be as much as initially thought.

New Positions

Ebay operates its namesake online marketplace at ebay.com . Its platform enables users to list, buy, sell and pay for items. In 2022, ebay would generate about $9.7B in revenues and ~2 Billion in free cash flow and $4 in eps. While ebay's operating results have been uneven over the years, it generates solid free cash flow annually and has reduced shares outstanding by more than 50% over the last decade. Ebay trades at a below average multiple and has above average profitability.

S&P Global ( SPGI ) provides credit ratings, benchmarks, analytics and workflow solutions in the global capital, commodity markets. It merged with IHS Markit in the previous year which increases their product depth and end markets. With the expected 19% decline in global debt issuance in 2022, SPGI results were dragged down by the key credit ratings business. It should come back as issuances normalize in the coming couple of years. The merger will provide additional cost and revenue synergies.

Dollar General ( DG ) is a discount retailer with over 18,000 stores in the United States. The company is still opening 100s of stores annually which are self-funded and generate excellent returns on capital. DG uses the free cash flow to pay a growing dividend and repurchase shares. This business is very resilient and remains profitable in all economic conditions.

Adobe ( ADBE ) is a software company with well known products such as Photoshop, Acrobat, Illustrator and so on. Adobe has been valued richly in the past due to its superior operating results as seen in the increase in revenues, profits and free cash flow. We bought shares in the in Q1 2022 but we kept the position small. The stock continued its decline and we have room to add to the position.

Swedish Match (SWMA) is a Swedish company (since acquired by another portfolio holding Philip Morris PM) that we bought in the market drop post the Russian invasion of Ukraine. Swedish match had one of the fastest growing nicotine pouch business. The price drop made it attractive and the drop did not make sense given its lack of business in the war region. Luck is equally important in investing and this was proved again as PM made the acquisition offer a few months after our purchase. The upside is that we continue to have exposure to Swedish Match via PM.

Global Payments ( GPN ) provides payment technology and software solutions for card, electronic, check payments in Americas, Europe and Asia Pacific. There has been a lot of competition entering this space over the last few years. The legacy payment tech companies beefed up with acquisitions. GPN should generate over $8B in revenue and $2.5B in FCF in 2022. While the debt is slightly on the higher side ($10B net debt), the company can reduce it using the ample free cash flow and the valuation is attractive.

Mind CTI ( MNDO ) is an Israeli company that provides end-to-end billing and customer care product-based solutions for telecom service providers as well as telecom expense management solutions. MNDO is making a comeback to the portfolio having first owned in 2012. Sales are about $18-$20 million annually with $4-$5m in free cash flow. The balance sheet is rock solid with $15 million in cash while the market cap at the time of purchase was $40 million. Management is very shareholder friendly with 100% of FCF being paid out in the form of dividends for more than a decade. The dividend yield based on last years' payout was 12%. The founder CEO owns 15%+ of the shares outstanding.

Positions added to

Through the year, we added to several holdings such as Facebook, Microsoft, Cigna, DXC, Bank of New York and SSNC.

Outlook for 2023

There are interesting factors in the markets currently with high inflation globally and rising interest rates. It would be interesting to see how well company earnings hold up this year. This year we may look to add some investments outside the US as well as smaller market capitalization companies depending on the overall opportunities available.

Thank you for the opportunity to manage a portion of your assets. We will continue to work hard to protect and grow your entrusted capital in 2023 and beyond.

Sincerely,

Adib Motiwala, Portfolio Manager

Appendix

Fast Growers (9 positions, 32%) - Earnings per share growth in the double digits. As long as they can grow, this category produces the big winners. The challenge is here to figure out when a company will stop growing and how much to pay for the growth. Portfolio has nine fast growers that make up 32%. Largest positions are Google, Cigna and Visa.

Stalwarts (4 positions, 14%) - Steady earnings per share growth and offer good protection during recessions and hard times. Four companies make up 14% of the portfolio. HDFC Bank and All State are the largest Stalwart positions.

Cyclicals (4 positions, 9%) - These companies' sales and profits rise and fall in a regular but not completely predictable fashion. Four companies make up 9% of the portfolio. Omnicom is the largest cyclical by weight.

Asset Plays (6 positions, 11%) - These companies have some kind of valuable asset that makes them attractive. The asset could be as simple as cash on the balance sheet, valuable real estate, tax assets, patents etc. We also use this bucket to group companies that are attractive on the basis of the free cash flow they generate. Six companies make up 11% of the portfolio. SSNC is the largest position.

Slow Growers (3 positions, 10%) -These companies grow modestly at best. They are primarily purchased for their generous dividend. Three tobacco companies make up 10% of the portfolio with British Tobacco being the largest position.

Turnarounds (1 position, 2.5%)- These are companies that have fallen on hard times and are being revived by management. The best thing about investing in successful turnarounds is that their ups and downs are least related to the general market. DXC that is in the late stage of turnaround and is 2.5% of the portfolio.

| Motiwala Capital LLC is a Registered Investment Advisor. This commentary candidly discusses a number of individual companies. These opinions are current as of the date of this commentary but are subject to change. All information provided is for information purposes only and should not be considered as investment advice or a recommendation to purchase or sell any specific security. While the information presented herein is believed to be reliable, no representations or warranty is made concerning the accuracy of any data presented. This communication may not be reproduced without prior written permission from us. Past performance is no guarantee of future results. Motiwala Capital performance is computed on a before-tax time weighted return (TWR) basis and is net of all paid management fees and brokerage costs. Performance figures are unaudited and generated using our custodian's reporting functionality. Performance of individual accounts may vary depending on the timing of their investment, the effects of additions, and the impact of withdrawals from their account. |

For further details see:

Motiwala Capital - 2022 Letter: US Capital Appreciation