MDV - Mouse Traps: 8 High-Yielding REITs Risking Dividend Cuts

2023-12-05 07:00:00 ET

Summary

- Overall, this is a good time to invest in REITs.

- The expected surge in REIT share prices will not benefit all REITs equally. There are always mousetrap REITs, even in the best of times.

- Dividend safety is crucial for REIT value as a dividend cut can lead to a significant loss in share value.

- This article provides a list of REITs yielding over 5.25% but with poor dividend safety grades, according to Seeking Alpha Premium's Quant Ratings system.

Overall, this is a good time to invest in REITs. Right now, there are lots of quality REITs whose yields are at or near their all-time highs. Inflation appears to be under control , and nearly down to the Fed target of 2%. It is likely that interest rates will hold steady or drop in the foreseeable future. After the brutal sell-off of the last two years, REITs appear to be poised for a surge .

But there are always mousetrap REITs, even in the best of times. These companies offer temptingly high dividend yields, but in reality, those yields may turn out to be an illusion. That's because any company that wants to lower its dividend can do so at any time. Management usually avoids cutting the dividend if at all possible, but some are forced to do so, because of reversals in the company's fortunes, or unexpected crises in the macro environment (remember COVID?).

Dividend Safety: Why it's important

Dividend safety is crucial to the value of a REIT, for one simple reason. When a REIT cuts its dividend, COWhand investors dump shares like yesterday's garbage, and the share price sinks like a stone. The hapless investor is left with the worst of both worlds: reduced income and a dramatic loss in share value, often leaving little recourse but to sell at a loss, or hold for a very long time in hopes of a recovery. Thus, it is vitally important to avoid mousetrap REITs, and if you are holding one, it is prudent to sell it before management cuts the dividend.

Dividend Safety: How to read the scores

You might think that of course the best dividend safety score would be A+, and the worst F. From the standpoint of safety alone, that would be true.

However, it is more complex than that. Every company has a choice of what to do with their excess funds from operations. They can plow the money into investments to expand, or they can pay it out to shareholders as dividends. So a company with an extraordinarily safe dividend may be failing to reward shareholders with as much cash income as the company could afford to pay.

Some companies operate in an environment that more or less requires them to retain more earnings for expansion and reinvestment. However, for all other companies, a Dividend Safety of A+ generally means they could safely pay out quite a bit more cash income to their shareholders.

Thus, the graphic below portrays the way I view the meaning of the Dividend Safety grade, in most cases.

| Grade |

| B+ |

| B |

| B- |

| C+ |

| C |

| C- |

| D+ |

| D |

| D- |

| F |

| Apartment Income |

| ( AIRC ) |

| Apartment |

| 5.60% |

| D- |

| BRT Apartments |

| ( BRT ) |

| Apartment |

| 5.30% |

| F |

| Clipper Realty |

| ( CLPR ) |

| Apartment |

| 7.32% |

| F |

| UMH Properties |

| ( UMH ) |

| Apartment |

| 5.64% |

| D- |

| Service Properties Trust |

| ( SVC ) |

| Apartment |

| 10.77% |

| D |

| Healthcare Realty |

| ( HR ) |

| Medical |

| 7.87% |

| D- |

| Global Medical |

| ( GMRE ) |

| Medical |

| 8.12% |

| F |

| Omega Healthcare Investors |

| ( OHI ) |

| Medical |

| 8.34% |

| D- |

| Sabra Health Care |

| ( SBRA ) |

| Medical |

| 8.18% |

| D |

| CTO Realty Growth |

| ( CTO ) |

| Strip Center |

| 8.84% |

| D |

| CBL & Associates Properties |

| ( CBL ) |

| Regional Mall |

| 6.36% |

| D- |

| Global Net Lease |

| ( GNL ) |

| Net Lease |

| 5.280% |

| F |

| Gladstone Commercial |

| ( GOOD ) |

| Net Lease |

| 9.23% |

| D- |

| One Liberty Properties |

| ( OLP ) |

| Net Lease |

| 8.55% |

| D |

| Postal Realty Trust |

| ( PSTL ) |

| Net Lease |

| 6.65% |

| D- |

| Modiv Industrial |

| ( MDV ) |

| Net Lease |

| 7.53% |

| D |

| Generation Income Properties |

| ( GIPR ) |

| Net Lease |

| 11.70% |

| F |

| Alexander's, Inc. |

| ( ALX ) |

| Office |

| 9.71% |

| D- |

| Creative Media & Community Trust |

| ( CMCT ) |

| Office |

| 8.90% |

| D- |

| Easterly Government Properties |

| ( DEA ) |

| Office |

| 8.65% |

| D- |

| Uniti Group Inc. |

| ( UNIT ) |

| Cell Tower |

| 10.27% |

| F |

| Crown Castle Inc. |

| ( CCI ) |

| Cell Tower |

| 5.28% |

| D |

| Outfront Media Inc. |

| ( OUT ) |

| Billboard |

| 9.24% |

| F |

| Presidio Property Trust Inc. |

| ( SQFT ) |

| Specialty |

| 9.68% |

| F |

Source: Hoya Capital Income Builder and Seeking Alpha Premium

The remainder of this article will zero in on the 8 REITs with Dividend Safety grades of F, to take just a quick look at why the Seeking Alpha Quant Ratings system considers the risk of an imminent dividend cut so high.

BRT Apartments

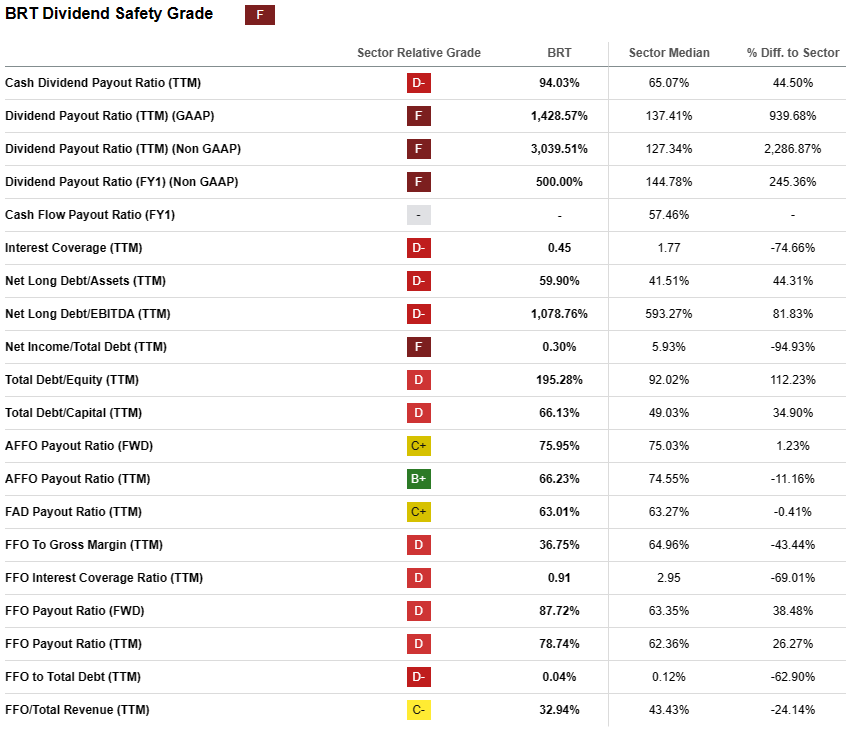

The table below shows how BRT Apartments scored on each of the factors that the Seeking Alpha Quant Ratings system considers when arriving at the Dividend Safety grade. As you can see, of the 20 data points considered, 16 are rated D or F, with the payout ratios and net income/total debt being the worst culprits. BRT relies heavily on lucrative redevelopment of its Class B apartment units, and usually carries more debt than most apartment REITs as a result, so a healthy grain of salt goes a long way here. The company's Debt/EBITDA is currently a lofty 12.3.

Clipper Realty

{kind=link}

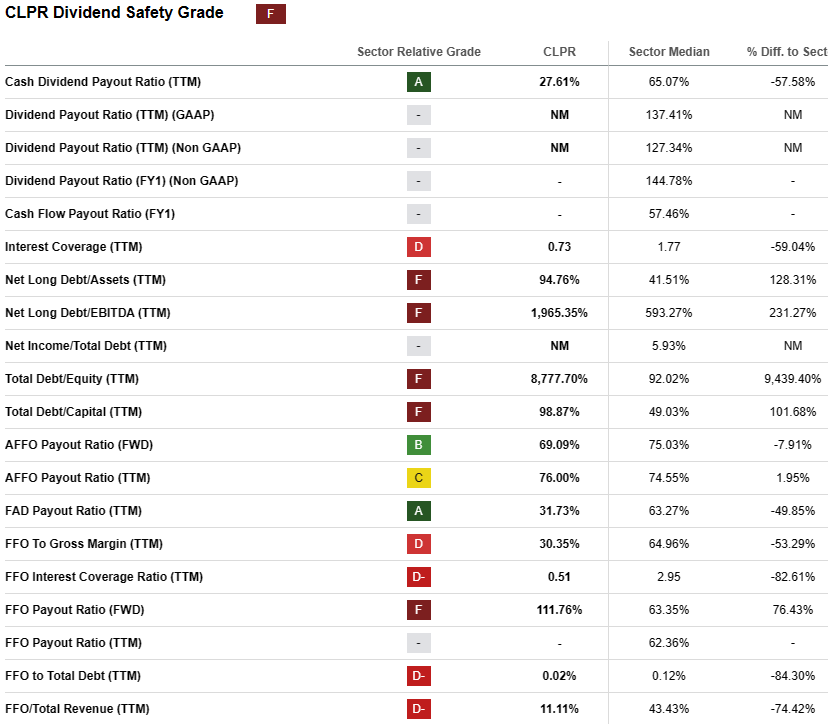

Here are the relevant Seeking Alpha Quant Ratings data points for CLPR. Of the 14 data points, 11 grade out at a D or worse, with the various debt ratios showing up worst. The company currently sports a very heavy 92% debt ratio and Debt/EBITDA of a whopping 19.9. However, the forward FFO payout ratio of 111.76% is also troubling.

Global Medical REIT

{kind=link}

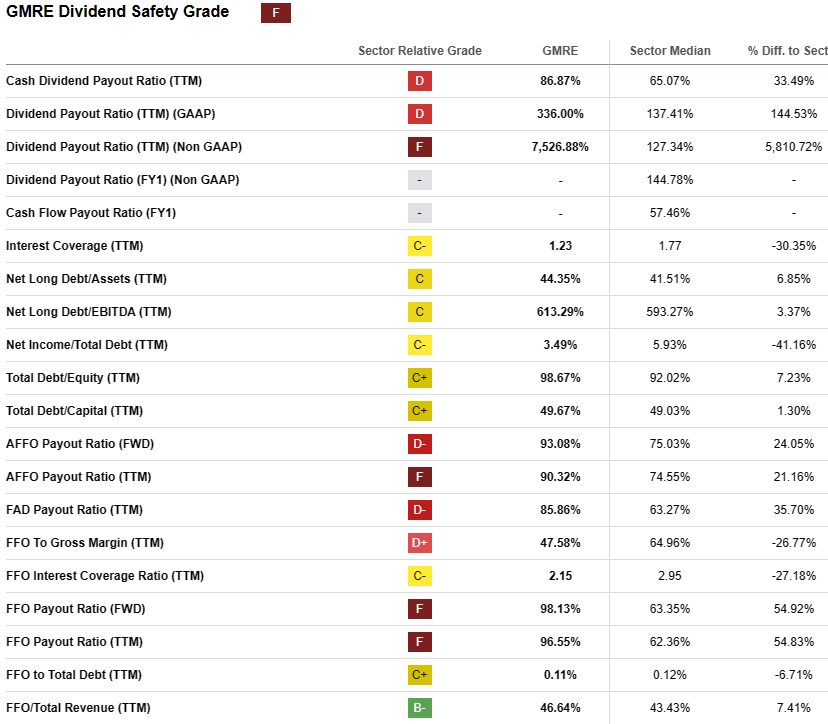

Here is the Quant Ratings picture for GMRE. Of the 18 data points, 9 grade out at D or lower. This company has historically deployed an aggressive payout ratio but has never cut its dividend, not even during COVID. Instead, GMRE has successfully relied on increasing FFO to maintain the dividend. However, this year, the company's FFO dipped by (-6.5)%, and without a strong rebound, the divvy could indeed be in danger of a cut.

Global Net Lease

{kind=link}

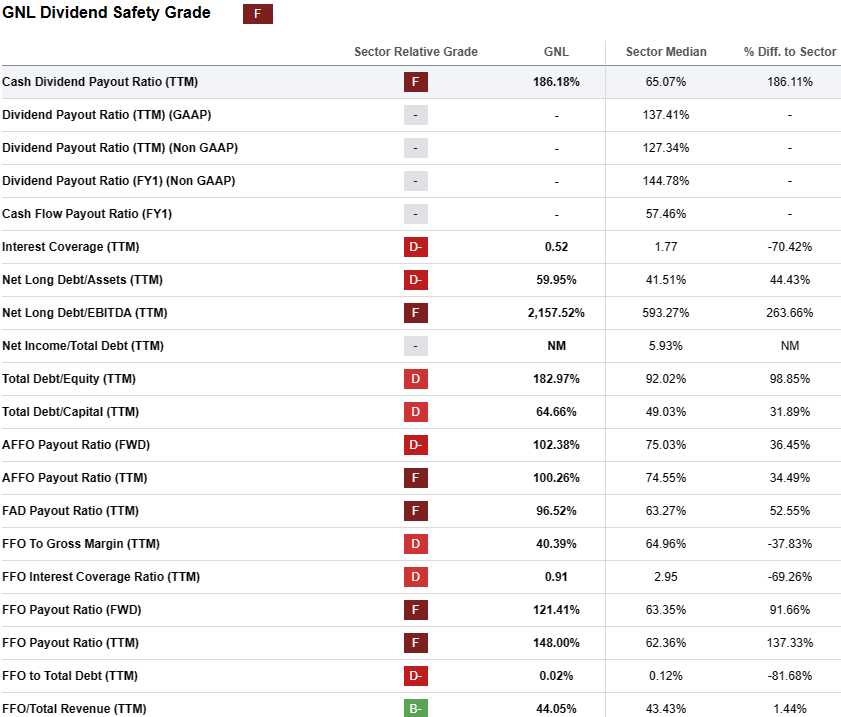

Here is the Quant ratings picture for GNL. Of the 15 data points, 14 grade out at D or worse. In September, GNL closed on acquisition of Necessity Retail and has since trimmed the dividend once already. However, with a 62% Debt Ratio, an absurd Debt/EBITDA of 281.9, elevated interest rates on the 18.7% of its debt held at variable rates, and an expected (-26.4)% decline in FFO/share this year, the sky-high yield of 15%+ seemingly can only be maintained with an immediate and substantial surge in revenues.

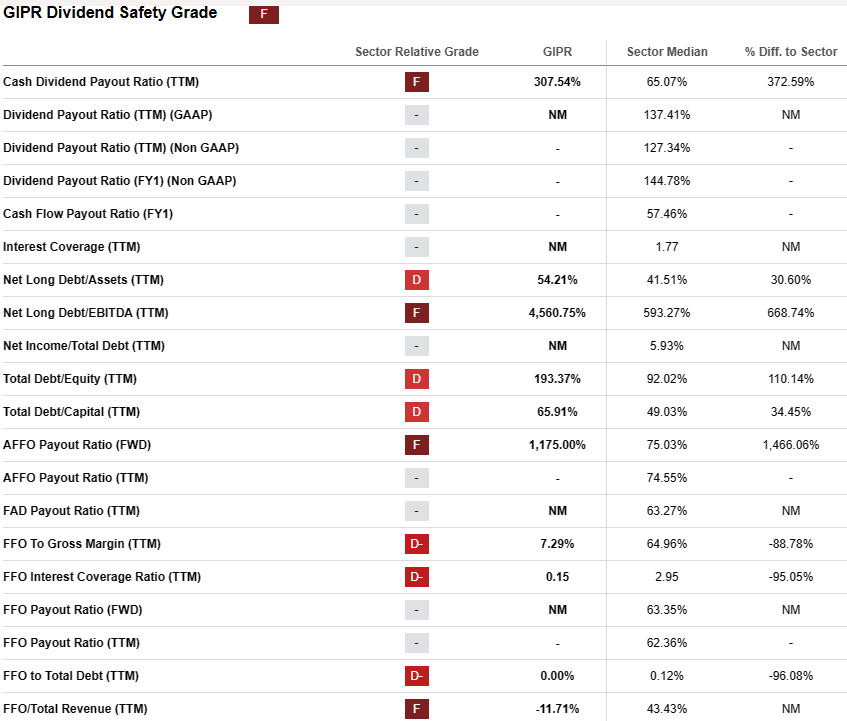

Generation Income Properties

{kind=link}

Below is a snapshot of the Quant ratings data points for micro-cap GIPR. All 10 of the data points grade out at D or worse. The Quant ratings system sees problems with the company's payout ratio, long debt, FFO to gross margin (trailing 12 months), and FFO interest coverage ratio. The company's debt ratio is a challenging 75% and Debt/EBITDA stands at 10.0. Like GNL, tiny GIPR likely will need an immediate surge in revenue to avoid a dividend cut.

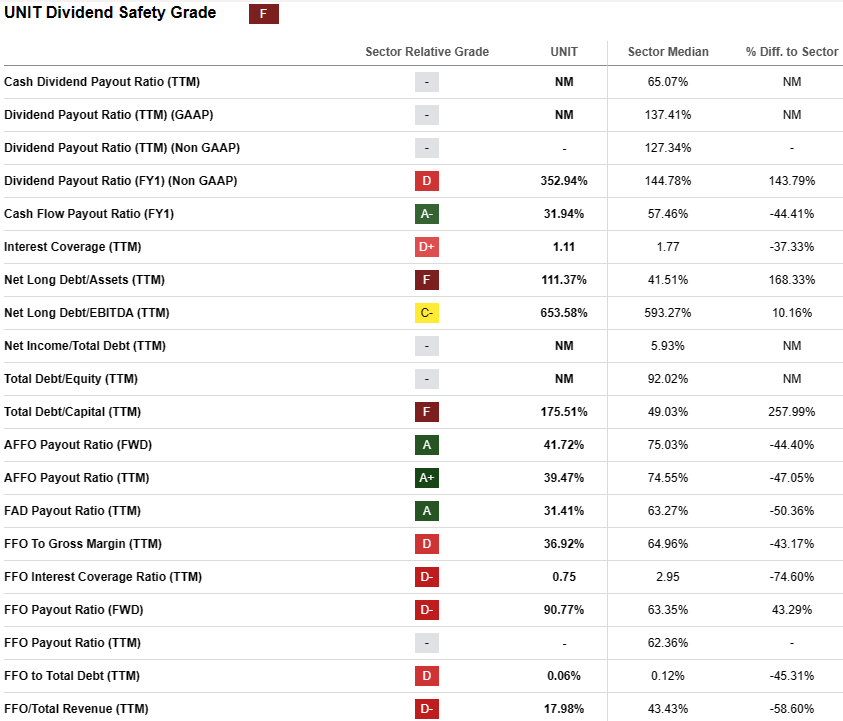

Uniti Group Inc.

{kind=link}

Here is the Quant snapshot of Uniti's dividend structure. Despite some areas of strength, 9 of the 14 data points grade at D or worse. UNIT's debt ratio is a formidable 81%, and the company's 78% surge in FFO/share in 2023 is likely to be followed by a significant (-18.7)% sag in 2024, from $1.39 this year to an estimated $1.13 next. Long debt and debt/capital are seen as especially worrisome by the Quant system.

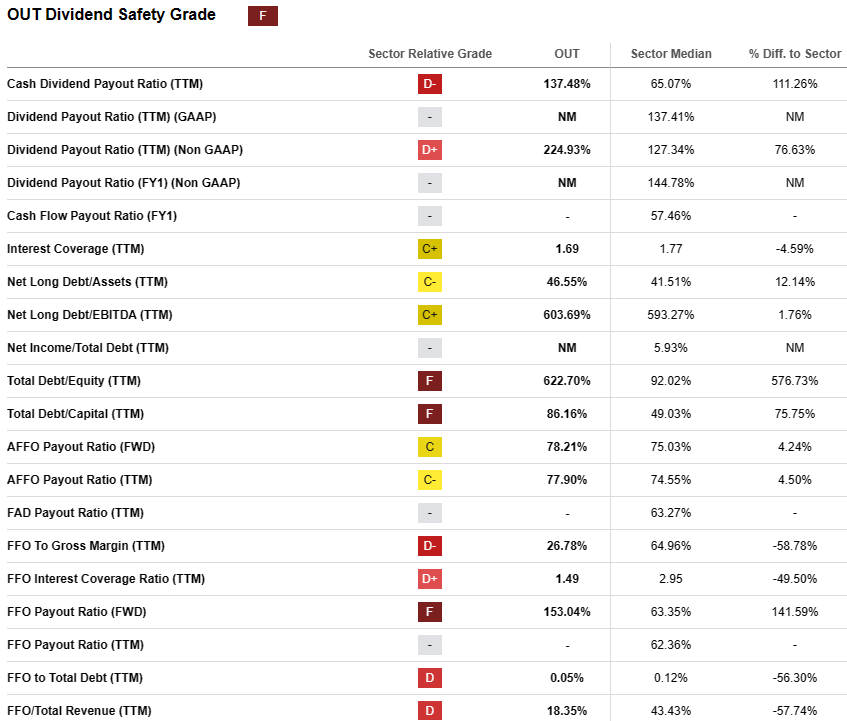

Outfront Media

{kind=link}

Of the 14 data points the Quant system shows for OUT, 9 come in at D or worse. The system sees debt/equity and debt/capital as particular problems, and the forward payout ratio of 153% is obviously very risky too. Debt/EBITDA is a miserable 23.0, and 14.4% of the company's debt is held at variable rates, thus at comparatively high interest. FFO/share has been extremely uneven over the past 4 years, vacillating between $2.06 in 2019 to $1.26 this year, with dips as low as $0.57 in 2020 and 2021.

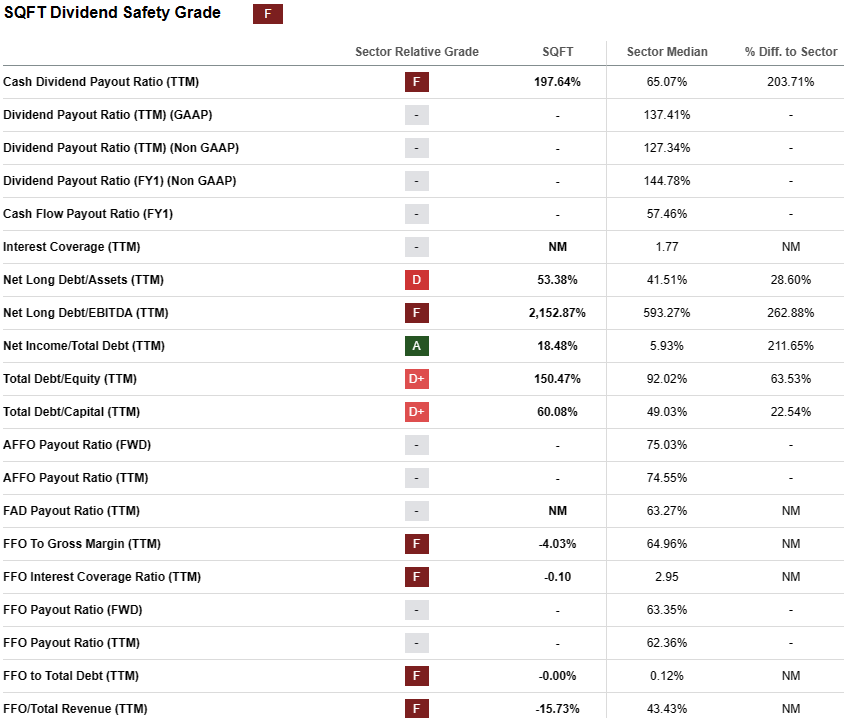

Presidio Property Trust

{kind=link}

Finally, here is the Quant snapshot of micro-cap Presidio's dividend structure. Of the 10 data points, 9 grade out at D or worse. The Quant system is especially dubious of Presidio's payout ratio, long debt, FFO to gross margin, and FFO interest coverage ratio. The company's debt/EBITDA is an atrocious 21.4.

{kind=link}

The Bottom Line

Just because a company receives an F grade on Dividend Safety does not mean a dividend cut will necessarily happen. A Hold case can be made for some of the companies mentioned in this article, including the 8 with the worst Dividend Safety ratings. A Buy case can even be made on a few.

The Seeking Alpha Quant system is not necessarily the final word on dividend safety, but the fact that these companies grade out so low in that system should give a sensible investor cause to pause before adding more shares, and good reason to seriously consider cutting any existing exposure and reallocating their capital.

For further details see:

Mouse Traps: 8 High-Yielding REITs Risking Dividend Cuts