SWGNF - Movado: Attractive Valuations Don't Make Up For Weak Performance

2023-10-27 15:23:30 ET

Summary

- Movado's share price is down 10.7% YTD, underperforming the luxury sector.

- Weak financial performance, including a decline in sales and operating margin, is a key factor. Its big US presence and small Asia market have particularly impacted it.

- A focus on premium and affordable brands is reflected in its operating margins. While its market multiples are attractive, there isn't a convincing enough Buy case here.

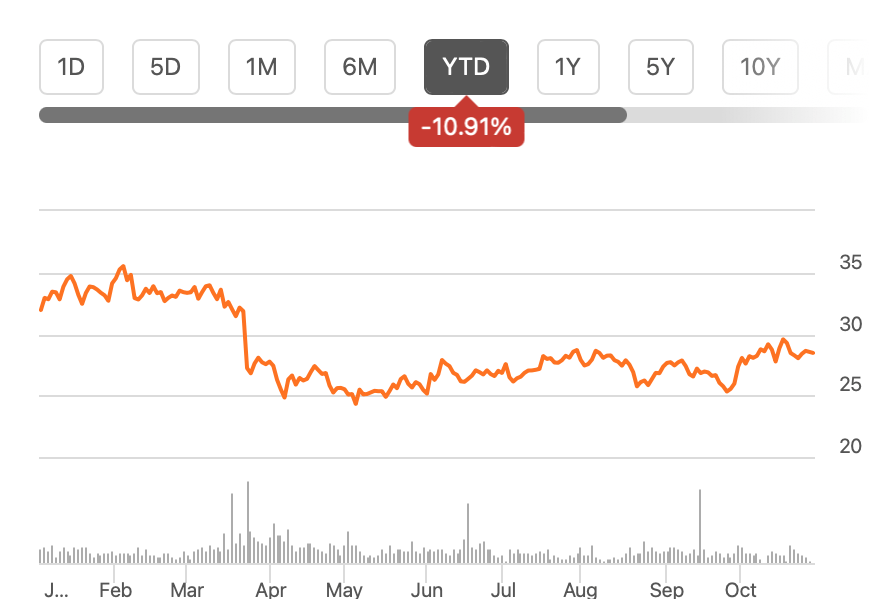

The luxury and affordable watch company Movado ( MOV ) hasn’t had much of a year on the stock market. Its share price is down by 10.7% year-to-date [YTD]. To be fair, this hasn't been a good year for the luxury sector as such. This is evident in the fact that the S&P Global Luxury Index has seen only a negligible rise YTD compared to an 8.6% increase in the S&P 500 ( SP500 ) index.

But it's clear that Movado has underperformed the sector. The reasons aren't hard to find. It has seen weak financial performance in the first half of its current financial year (H1 FY24, ending July 31, 2023). While signs of weakness are visible across luxury companies, Movado's softening stands out. Here I assess why this is so and if the stock might have overcorrected.

{kind=link}

Price Chart (Source: Seeking Alpha)

Why has performance weakened?

In H1 FY24 , the company’s sales fell by 12.3% year-on-year (YoY) on a reported basis and by 13.8% on a constant currency basis. This compares poorly to other luxury companies like the Swiss Swatch Group ( OTCPK:SWGAY ), as an example, which also specialises in watches. Swatch has seen an 11.3% increase in reported net sales for the first half of 2023 and an 18% rise in constant currency terms.

Poor sales figures have also impacted its operating margin, which has also declined drastically to 6.7% (H1 FY23: 16.2%) even as the cost of revenues shrank. In contrast, Swatch's operating margin in the first half of 2023 was at 17.1%, a rise from the corresponding period of the previous year.

Movado has been uncompetitive at this time for two reasons, which are as follows.

Big US and small Asia market

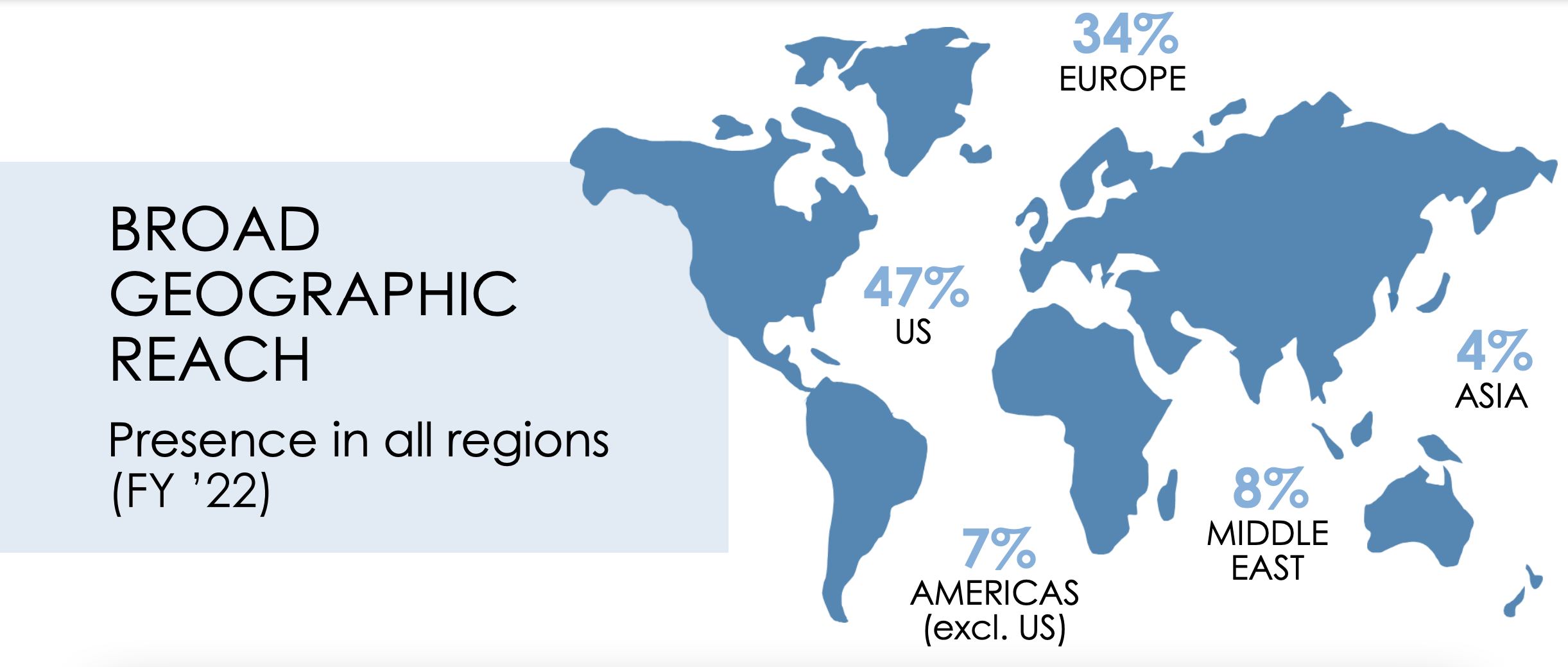

First, compared to other luxury companies, which have a strong Asia-Pacific market, Movado is US-focused. For the financial year ending January 31, 2023 (FY23), 44.4% of its sales were from the US market. Europe came next, with a 32.8% share in sales, while Asia contributed just 4.7% of revenues.

{kind=link}

Sales by Geography (Source: Movado)

{kind=link}

Source: Movado

The share of the US market has declined to 42.6% in H1 FY24, but it remains substantial. As a result, the trend of a weakening US market across the luxury segment has had a higher proportional impact on it. While other luxury companies have been cushioned by a surge in Asia sales following China's post-lockdown spending spree, Movado hasn't been able to benefit from this trend either.

Not all luxury

Second, it doesn't entirely cater to luxury demand, which is best explained with a closer look at its brands. The company divides its watch brands under two heads, owned brands and licensed brands (see chart below). Its own brands like Olivia Burton, a popular UK women's brand for watches and accessories acquired in 2017 and MVMT, founded in 2013 and bought by Movado in 2018, sell watches at relatively affordable prices.

{kind=link}

Movado Brands (Source: Movado)

Similarly, its licensed brands can best be called affordable luxury, while others like Tommy Hilfiger and Calvin Klein, otherwise owned by PVH Corporation ( PVH ) are relatively lower-margin businesses.

For such categories, it's harder for a company to grow revenues by raising prices. The fact that its licensed brands accounted for 63% of sales reflects the size of their impact on the company's margins. Sustained fixed costs and higher payroll expenses were an additional challenge, as operating costs rose to 49.3% of net sales (H1 FY23: 41.3%). As a result, Movado got squeezed on both ends, resulting in a lower operating margin.

{kind=link}

Sales by Category, H1 FY24 (Source: Movado)

Fundamental issues

Movado's challenges go beyond just the current context, however. Consider its international sales. These to have been affected, by 12.1% in reported numbers and 14.9% on a constant currency basis, a trend distinct from that witnessed by other luxury companies.

The likes of Swatch have reported rising demand for lower-priced watch segments at this time, indicating that there's a growing market for exactly the kind of price points that Movado caters to. But the company hasn't been able to benefit from the trend. Speculatively, this suggests a possible lack of brand strength at par with others.

Further, a big issue with Movado is its small Asia presence. It's hard to see it becoming competitive with other luxury brands until there's a strategic shift towards more emphasis on the fast-growing market.

Reduced outlook

In line with a weak financial performance, Movado has unsurprisingly downgraded its outlook for FY24. It now expects net sales to come in at USD 690-700 million, which is a 7.6% decline from FY23 at the midpoint of the range. Even earlier, it had expected a decline at the midpoint, but it was far smaller at under 2%.

It has also downgraded its operating profit outlook to USD 62.5-65 million from the earlier USD 80-85 million. Despite this, however, a better operating margin from H1 FY24 is likely though, at 9.2%. It’s not as high as the 11.2% expected earlier, and a significant decline from the 16.1% seen in FY23, though.

It also sees a lower diluted earnings per share [EPS] at USD 2.15-2.25 compared to the earlier USD 2.70-2.90.

What the market multiples say

At this EPS, though, Movado’s forward P/E for FY24 is rather competitive at 12.1x. The consumer discretionary sector’s average forward P/E is at a higher 14x. And if we add some luxury premium to the stock, it should be even higher than that. Its GAAP TTM P/E is also low at 9.4x compared to the 14.8x for the sector.

What next?

Normally, a low P/E would be a good indication of a stock’s value. I don’t think that’s the case here, though. Even with strong brands in its portfolio, Movado’s performance is sorely lacking. And the US economy might not be out of the woods until we are well into next year. Further, despite declining inflation, its margins have fallen. The overall picture isn’t inspiring as a result. It’s not a stock to Sell, considering that it could see a pickup as the macroeconomic cycle turns. But there’s no real reason to Buy it either. I’m going with a Hold.

For further details see:

Movado: Attractive Valuations Don't Make Up For Weak Performance