MOV - Movado: Scrutinizing Threats To Its Position In The Watch Market

2023-08-18 18:51:52 ET

Summary

- Movado's core brands have struggled with maintaining and improving reach, leading to a sustained decline in interest and low growth.

- The company's revenue and margins have declined in the most recent quarter, with no immediate improvement in sight.

- We do see attractive qualities with its licensing of brands, as its deep expertise positions the business as an attractive partner to brands.

- Movado is trading at a cheap valuation, but its lack of commercial strength suggests it may be a value trap.

Investment thesis

Our current investment thesis is:

- 2 of Movado's core brands have struggled with remaining culturally relevant, contributing to a sustained decline in interest for over a decade. The business has achieved low growth, supported by the acquisition of MVMT and its portfolio of licensed products.

- We do not believe the company is positioned to improve its growth trajectory, with the risk that the business continues to struggle. In the most recent quarter, both revenue and margins have declined, with no immediate end in sight.

- Movado is incredibly cheap, trading at a 10% free cash flow ("FCF") yield. Although this is attractive, we believe the lack of commercial strength implies a value trap.

Company description

Movado Group, Inc. ( MOV ) is a renowned luxury watch company with a rich heritage in watchmaking. The company is known for its iconic designs and high-quality timepieces.

Share price

Movado's share price performance has been poor in the last decade, losing over 25% of its value while the market has generated strong returns. This is a reflection of underwhelming financial development and changing industry dynamics.

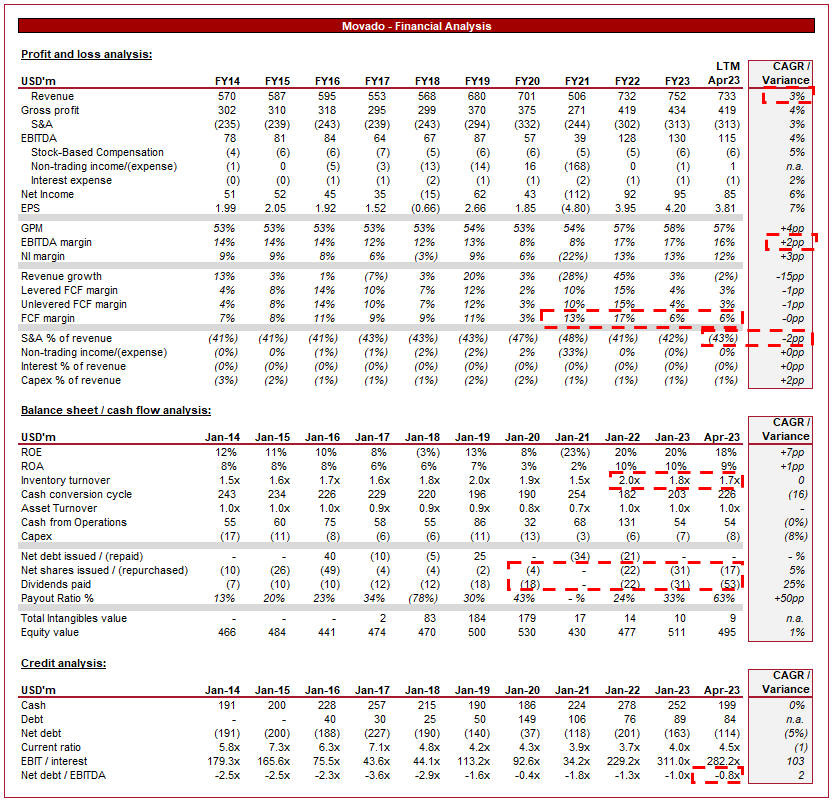

Financial analysis

Movado financials (Capital IQ)

{kind=link}

Presented above is Movado's financial performance in the last decade.

Revenue & Commercial Factors

Movado's revenue has grown at a CAGR of 3% in the last 10 years, with generally consistent growth, experiencing only a single period of negative growth (excl. the pandemic impact). Movado has supported revenue with acquisitions, such as that of MVMT in late 2018 .

Business Model

Movado is primarily known for its expertise in designing and manufacturing luxury and fashion watches. The company creates a wide range of watch styles, for differing consumer demographics.

Movado owns and manages a diverse portfolio of watch brands, including Movado, Ebel, Concord, MVMT, Coach, Tommy Hilfiger, Hugo Boss, and more. The company's deep expertise allows it to initiate strategic partnerships and licensing agreements with well-known fashion and lifestyle brands, diversifying its revenue by supporting its in-house brands.

Movado sells its products through a combination of its own retail stores, department stores, specialty retailers, and e-commerce platforms. This multi-channel distribution approach ensures wide market coverage.

Competitive Positioning

Movado's portfolio includes well-established brands with a legacy of quality and design excellence. This has allowed the business to achieve consistent growth, particularly with the brands it licenses.

The demand for watches has improved considerably in recent years, particularly in the luxury segment, driven by word-of-mouth marketing and hype. This is encouraging new consumers into the market and the discovery of new brands. We see this as a "rising tide lifts all boats" situation, potentially continuing an improvement in growth trajectory.

We are disappointed by the development of the Ebel and Movado brands, however. Both had been incredibly popular within mainstream/horological culture, but an inability to successfully innovate their designs with changing consumer trends has left both brands significantly less compelling to consumers. Likely compounding this poor innovation is a lack of effective marketing, as Management likely relied on popularity to maintain its trajectory.

Luxury watches are often associated with status, style, and personal expression. The issue with the Movado brand is that it relied far too heavily on a single design rather than developing the brand association with these 3 factors. Ebel, on the other hand, struggled with identity, likely due to the brand being outspent on marketing relative to its Swiss peers such as TAG ( LVMHF ), Raymond Weil, Rado, Longines ( SWGAY ), and Frederique Constant.

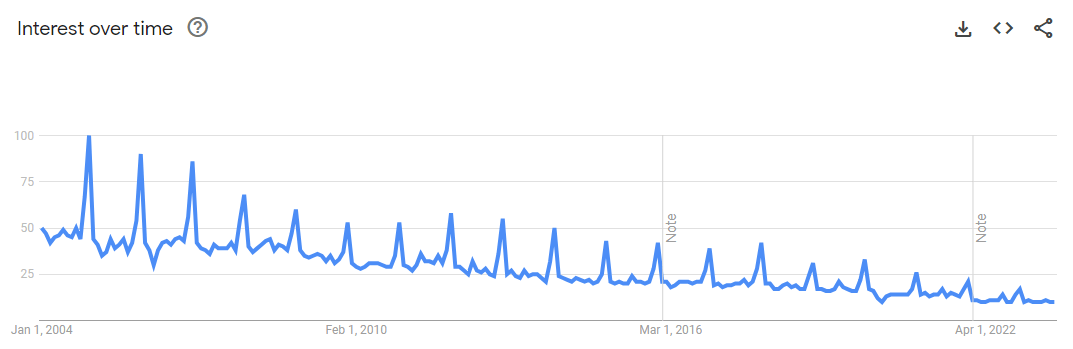

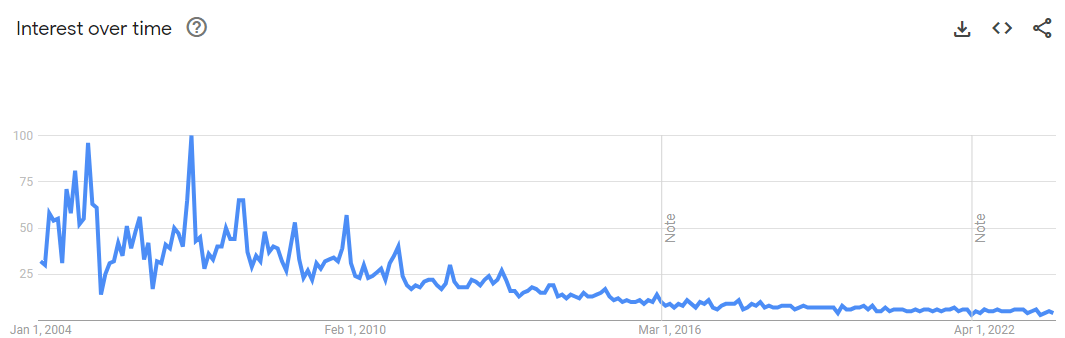

As the following illustrates, the interest in both Movado and Ebel has consistently declined, with no improvement in over 10 years.

Movado (Google Trends) Ebel (Google Trends)

{kind=link}

{kind=link}

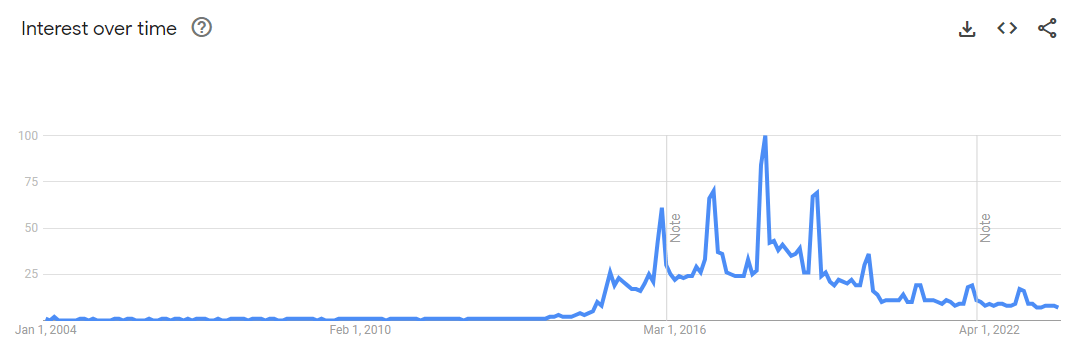

This does raise the question of whether management will ever generate improvement in these brands. Compounding this is the development of MVMT post-acquisition. The hype MVMT generated in the 2016-2018 period has evaporated, with a steep subsequent decline. This implies the brand will be unable to support continued weakness in Movado/Ebel, increasing reliance on licensed brands to maintain healthy revenue growth

{kind=link}

Another factor contributing to this is globalization. We have seen an increase in affordable watch brands with supply chains in the Far East (MVMT began as one such brand), contributing to the market being flooded by a number of new entrants who are priced aggressively relative to the traditional brands. This has given consumers significantly more choices and means more competition for Movado, which has pricing restrictions due to marketing investment.

This has been accelerated by the rise of e-commerce, with companies embracing digital platforms. This has further increased competition, as consumers have greater choice and ease of comparability.

Movado Group operates in the luxury watch and accessories sector and competes with companies like Fossil Group ( FOSL ), Citizen Watch Co, Swatch Group, and Seiko.

Economic & External Consideration

Current economic conditions represent near-term headwinds. With heightened interest rates and a significant period of high inflation, consumers have experienced an attack on finances, contributing to reduced spending and increased borrowing.

This is naturally expected to disproportionately impact discretionary retail spending, particularly because consumer spending has been reasonably robust thus far.

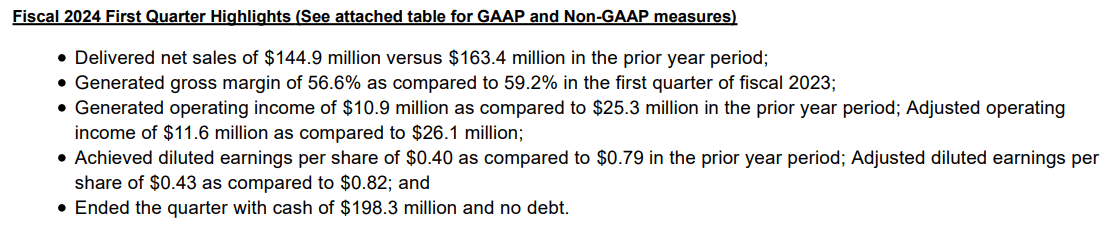

Movado is feeling the impact of this, with revenue declining (11.3)% YoY in Q1 and GPM declining (2.6)ppts. The decline in net sales was felt across all channels, cementing the challenges faced by macro conditions. Sales in the U.S. saw a significant decrease of (15.7)%. Similarly, international sales also declined by (8.1)%. Our expectation is for this trend to continue in FY24, although potentially to a reduced degree as wholesale demand normalizes.

{kind=link}

Margins

Movado's margins have surprisingly improved over the historical period, with EBITDA-M reaching 16% and NIM reaching 12%. This is a rare sight for a business struggling with growth, as the classic response has always been to increase S&A spending (which did occur for a short period). Movado's Management on the other hand has maintained similar spending (2ppts. increase in S&A spending, primarily wage related), allowing for operating cost leverage despite the mediocre growth.

The reduction in GM% in the LTM is primarily from unfavorable shifts in both channel and product mix, as well as the negative influence of FX. However, this decrease was partially mitigated by lower shipping costs, implying inflationary pressures are subsiding.

Our expectation is for continued margin erosion due to competition, moving toward the prior normalized level of 12-14% level.

Balance sheet & Cash Flows

Movado's inventory turnover has been gradually declining, falling to 1.7x in Apr-23. This suggests demand remains below Management's expectations, contributing to a strain on cash flows.

Movado is conservatively financed, with a ND/EBITDA ratio of (0.8)x. This ensures no downside risk if growth continues to be a challenge.

Industry analysis

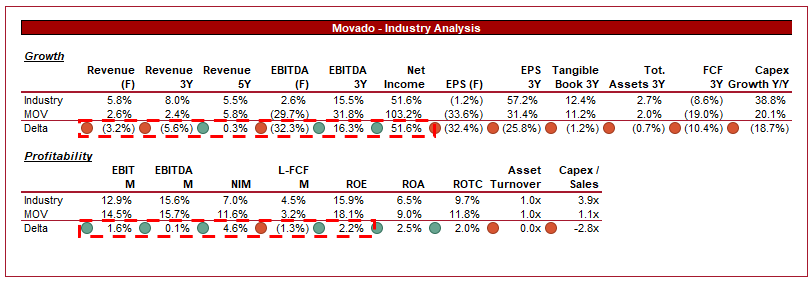

Apparel, Accessories and Luxury Goods Stocks (Seeking Alpha)

{kind=link}

Presented above is a comparison of Movado's growth and profitability to the average of its industry, as defined by Seeking Alpha (26 companies).

Movado performs well, implying potential. The company is lacking in organic revenue growth, with the expectation for this to continue. The growth delta is a reflection of heightened post-pandemic spending by consumers, with Movado being restricted by the weakness in its two core brands.

The company performs far better in profitability, boasting superior average margins and efficiency metrics. This is likely a reflection of the segment it operates within, as fashion watches generally have extremely low production costs while boasting good MSRPs. The only concern with this is the risk of further margin contraction taking the business below average.

Valuation

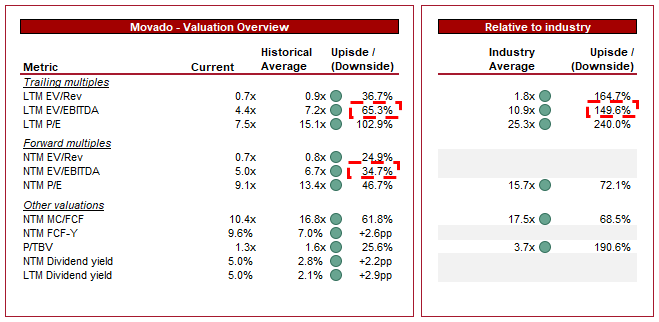

{kind=link}

Movado is currently trading at 4x LTM EBITDA and 5x NTM EBITDA. This is a discount to its historical average.

A discount to its historical average is reasonable in our view, as growth continues to be a struggle for the business while competition has increased and its brands have degraded in value.

Further, the company is trading at a 149% discount to its peers on an EBITDA basis, and 69% on a FCF basis. A discount is warranted in our view, primarily due to commercial weakness rather than a clear financial metric. This will translate to financial weakness going forward and is likely to restrict cash flow potential.

For higher-risk investors, there is clearly a good proposition here. The business is extremely cheap and at a FCF yield of 10%, the business is generating strong returns.

At its current share price, however, the business could be a good takeover target. Its expertise are key, which could allow for an expansion of its portfolio of brands. Further, there could be a situation where the business is combined with Fossil, which operates as similar business model.

Final thoughts

Fashion retail is notoriously highly competitive due to changing consumer trends and the difficulties with maintaining trajectory. Movado Group, Inc. has been a victim of this, with 2 of its core-owned brands (Movado and Ebel) having experienced a sustained decline in interest for over a decade. Despite the acquisition of MVMT and the strengths of its licensed brands, we believe the company's trajectory has not materially changed.

This is a business that could be considered cheap, but we like this to be underpinned by some commercial strength. In this case, the business is sorely lacking.

For further details see:

Movado: Scrutinizing Threats To Its Position In The Watch Market