MHGVY - Mowi ASA: The Future Of Fish Farming

2023-12-23 02:28:15 ET

Summary

- Mowi is the largest farmer of Atlantic salmon and holds a 20% market share in the global farmed salmon industry.

- The market for salmon is expected to grow by 8% annually, driven by increasing demand and limited supply.

- Mowi has a strong market position with solid returns and above-average growth.

- There is an undervaluation of Mowi of around 30%.

Introduction - Mowi who?!

In terms of value, salmon is the largest single fish product in the world and is an important part of the diet in many regions of the world. In 2022, the salmon farming industry accounted for around 55% of total salmon consumption. Salmon farming has played an increasingly important role in recent years and will be needed in the future to meet the ever-increasing demand. In this analysis, we take a look at by far the largest farmer of Atlantic salmon and consider whether the share could be a worthwhile long-term investment.

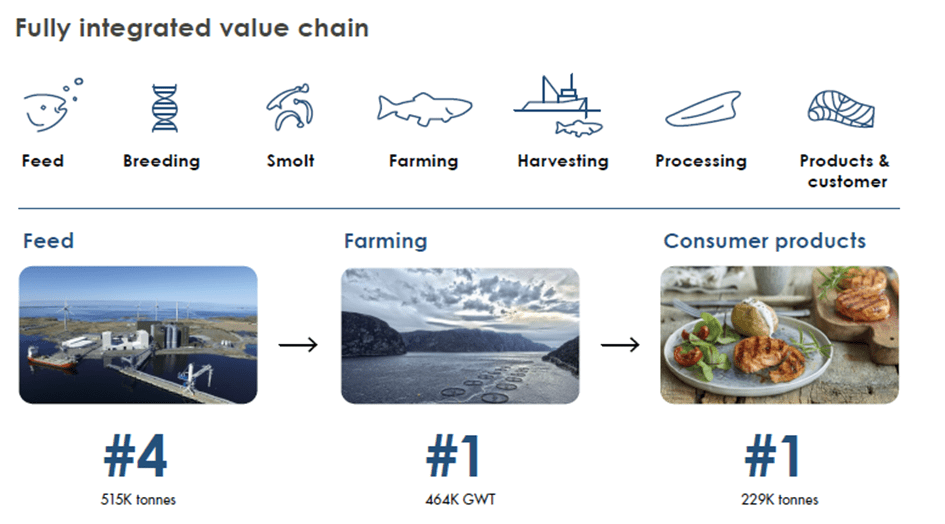

Mowi ( MHGVY ) is a Norwegian company active in the farming of wild salmon, covering the entire value chain from feed to farming and processing. In addition, Mowi is now even represented on the market as its own brand. Mowi‘s most important fish species is wild Atlantic salmon. After harvesting, it is either sold directly as a raw product or first filleted, smoked or marinated.

Mowi's value chain (Mowi Annual Report 2022)

{kind=link}

The wild Atlantic salmon is heavily dependent on environmental aspects such as temperature and water quality during its farming. It can therefore only be farmed in certain regions of the world. Mowi has grown steadily over the last few years through its own expansion and acquisitions and is now active in practically all regions of the world where wild salmon can be farmed. The most important farming areas are Norway, Scotland, Chile and Canada. Norway is by far the most important location. At around 293,720 GWT (Guttet Wight Tonnes), 63% of the total of 464 GWT harvested by Mowi in 2022 was harvested there. This enormously high volume of harvested salmon means that Mowi is the global market leader in farmed salmon with a 20% market share.

Salmon is sold both via direct contracts with traders and via the freely accessible futures and spot markets. As salmon is a premium product in the high-price segment, it is mainly sold to the wealthier regions of the world. Europe (71%) and America (20%) play a particularly important role.

Mowi's sales by region (Company presentation Q3 2023)

Growth - How high does it go?

Sales and profit growth play a decisive role in the long-term view of Mowi. Let's take a look at the market first.

According to studies, the market for salmon is expected to grow from its current level of around 31 billion USD to 45.7 billion USD in 2028 . This represents annual market growth of around 8%. This growth is achieved because, on the one hand, harvest volumes on the market are expected to increase by 2-3% per year and, at the same time, demand will exceed supply, meaning that the price is also likely to rise in the long term. This assumption seems plausible, as demand growth has amounted to around 11% in recent years. At the same time, the quantities of harvested salmon are strictly limited by regulatory and environmental conditions, meaning that it would not be possible to increase the harvest.

Let's take a brief look at the regulatory framework. A limited number of licenses are issued by the federal states, which can be acquired through bidding procedures. These licenses allow salmon to be farmed in certain areas. However, even in these areas, the quantity of salmon farmed is limited, as otherwise the risk of diseases such as salmon lice increases and the water quality decreases significantly. For this reason, a traffic light system has been introduced in countries such as Norway, which continuously evaluates salmon farming from an ecological point of view and thus imposes restrictions. This means that growth is restricted by the issuing of licenses by governments.

Furthermore, as already mentioned, environmental conditions mean that wild salmon cannot be farmed in every country, so there is also a natural limit to the growth of the market here.

Mowi's growth is largely organic. Harvest growth over the last 5 years has been 5.2%, while the market has only grown by 4.1%. This growth is expected to continue in the coming years and, at around 5%, is expected to exceed the market growth rate of 3%.

Mowi's harvest volumes 2018 - 2023E (Annual Report 2022)

In the past, these figures were also reflected in sales and profit growth. Turnover has increased by around 8% per year over the last 10 years. The decisive factor here will be whether Mowi succeeds in acquiring further licenses and thus naturally increasing the harvest volume.

Mowi's revenue 2013 - 2022 (Annual Report 2022)

In addition to organic growth, Mowi has repeatedly made smaller acquisitions, such as the takeover of the Icelandic salmon farm company "Arctic Fish" in 2022 . Here, Mowi has succeeded in integrating the acquired companies and leveraging further potential in the respective companies thanks to the fully covered value chain. A typical example of this is the supply of Arctic Fish with its own fish feed.

The growth in Mowi's profit is very difficult to quantify in the short to medium term, as it is subject to high fluctuations in individual years and is heavily dependent on the cyclical development of salmon prices on the market. However, it can be assumed that the price of salmon is likely to increase in the long term due to the gap between supply and demand and that Mowi's profit is therefore likely to develop accordingly. Based on the available information on harvest volumes, increases in profitability and the trend in salmon prices, average profit growth of around 7-8% can be assumed in the medium to long term.

Competition - Who else wants a piece of the cake?

The market for salmon is very fragmented and highly competitive. In addition to many smaller suppliers, Mowi competes with a number of larger salmon farmers such as SalMar ASA ( SALRF ), Grieg Seafood ASA ( GRGSF ), Leroy Seafood Group ASA ( LYSFF ) and Bakkafrost ( BKFKF ). It is therefore crucial to differentiate itself from its competitors.

In itself, salmon has no unique selling point. The price is determined by supply and demand, just like a commodity on the stock exchange. Mowi is trying to counteract this by selling products under its own brand via direct contracts. In particular, this should create pricing power in the future and make Mowi less dependent on stock market price developments.

The licenses granted by the state represent a toll bridge against the competition. These can be acquired by larger providers such as Mowi at higher prices and in greater numbers than the competition.

Furthermore, factors such as salinity, currents and water temperature represent a natural barrier that makes salmon farming possible in only a few regions in the world. Mowi has established itself in the largest regions for salmon farming through expansion or strategic acquisitions.

Another competitive advantage is Mowi's broad positioning along the entire value chain. This means that it always has greater control over the costs and quality of fish feed, egg farming and the type of processing, whereas its competitors are sometimes dependent on external suppliers and service providers.

Mowi also has an advantage of scale due to its diversification across various regional markets. This means that Mowi is less susceptible to regulatory restrictions, diseases or environmental influences.

Overall, Mowi's solid competitive position is also reflected in its key figures.

ROCE of Mowi and peer group (Created by author using data from annual reports)

As profit and sales growth is subject to major fluctuations due to many influencing factors, the market share of harvest volume is a useful indicator for assessing market position. Here, Mowi was able to increase its market share from 50.9% in 2018 to 54% in 2022. In addition, Mowi is expected to continue to grow above the market average in the coming years and thus gain further market share.

Profitability - Is it even worth it?

The profitability of Mowi depends on several influencing factors.

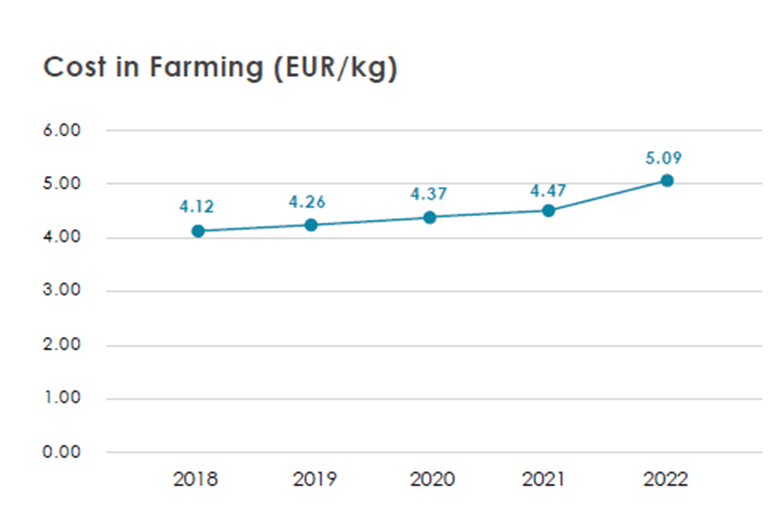

One important factor is the cost of farming salmon. In particular, feed for the animals is the largest cost factor at around 40%. Mowi has recognized this aspect and set up its own feed production. This means that the quality and availability of the feed can be better monitored. In addition, lower prices for feed can be set within the company, which increases the company's profitability. Overall, Mowi's strategy of covering the entire salmon farming value chain has shown great benefits in recent years. Major investments have been made in recent years in the area of feed production and for the optimization of land tanks for breeding the small fish.

Mowi's cost of farming (Annual Report 2022)

{kind=link}

The graph clearly shows that the cost side is relatively stable and is hardly subject to any major fluctuations. Adjusted for inflation, the farming costs per kg of salmon have remained constant. However, the prices for feed have risen very sharply, particularly in 2022. In future, the costs of farming and processing salmon are to be reduced with the help of optimization, digitalization and automation. The Mowi 4.0 program was launched for this purpose. At the same time, the potential for optimization at this point is limited, so it is much more interesting to take a look at the sales side in terms of profitability.

Mowi sells salmon partly through long-term direct contracts with traders, which serve to protect the salmon price from market fluctuations. Another and much more common option is to sell on the spot and futures markets . Here, salmon is traded like a commodity, so the price achieved depends on supply and demand.

Salmon price development 1998 - 2023 (indexmundi.com)

{kind=link}

This graph clearly shows that the price of salmon on the market is subject to strong fluctuations. This can be attributed in particular to the fluctuating supply of salmon on the market. In years with large salmon harvests, the price can fall significantly. In other years, when the harvest is significantly lower, for example due to disease, the price can rise sharply in the short term.

All market participants are subject to these fluctuations and cannot simply sit out low market prices because all harvested salmon must be processed and consumed within a short period of time. Mowi tries to counteract this trend through direct contracts with wholesalers, retail chains and the use of forward contracts. However, the significant fluctuations in profits and margins make it clear that Mowi cannot escape the price fluctuations on the market. Looking at the above chart and the market trend, however, it is clear that higher salmon prices can be achieved on the market in the long term and that the company's profitability will therefore increase.

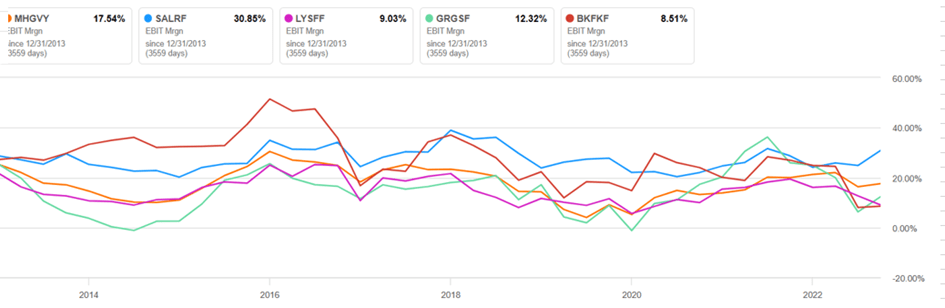

An important key figure for measuring profitability is the EBIT margin. This has also been subject to major fluctuations in recent years, reaching an average of around 18% over the last 10 years. In the same period, competitors such as Salmar (26%) and Bakkafrost (28%) achieved significantly higher margins, while Leroy Seafood (15%) and Grieg Seafood (14.5%) only achieved lower EBIT margins.

Development of 10-year EBIT margin of Mowi and competitors (Seekingalpha.com)

{kind=link}

The different margins can be attributed in particular to local differences. For each region, profitability is always expressed in terms of EBIT/kg. This key figure shows how much EBIT was achieved by Mowi per kg of salmon sold in the particular region.

Mowi’s EBIT/kg by region (Company presentation Q3 2023)

The chart clearly shows that Mowi's broad regional diversification means that, in addition to the very profitable Norway (EUR 2.15/kg), less profitable regions such as Chile (EUR 0.48/kg) also reduce the company's overall profitability. Companies such as Salmar, on the other hand, operate almost exclusively on the Norwegian market and can demonstrate higher profitability. Overall, however, Mowi's regional diversification should be seen as advantageous due to the resulting reduced risks and increased growth potential.

At this point, it should be mentioned that Mowi achieves an above-average EBIT/kg in each of its regional markets and that margins are set to increase further in the future through the development of its own brand.

Another aspect that I would like to mention at this point with regarding profitability is that Mowi has always managed to generate a free cash flow in recent years despite the expansion of its business activities and efficiency programs. This should increase significantly as soon as the Mowi 4.0 efficiency program, among other things, is completed.

Stability - Could tomorrow be the end?

When considering stability, a number of factors are important that are very sector-specific.

According to the annual report, the "Biological assets" item comprises around EUR 2 billion, which is around 26% of total assets. These assets are live salmon, which are subject to environmental risks. Difficulties could arise here in the event of disease, storms, etc. This means that 26% of the balance sheet is swimming around alive in pools and must always be valued differently depending on the market price on the stock exchange and environmental conditions. This is why write-ups or write-downs take place regularly. However, Mowi is well diversified in terms of regions, so that difficulties such as those currently experienced in Canada can be absorbed very well by the other regions.

Mowi measures and evaluates the debt ratio in net interest bearing debt (NIBD). In recent years, debt has increased significantly to EUR 1706 million, partly due to the acquisition of the Icelandic salmon farm company Arctic Fish. As a result, interest expenses have risen to EUR 30 million in Q3 2022. This is around 16% of the EBIT generated in the same period. According to the company's management, debt is to be reduced to 1400 million EUR in the medium term.

Looking at the dynamic gearing ratio of 5.1 and the gearing of 33%, it is clear that there is significant debt, but that this has not reached a critical level and that Mowi should be able to reduce its debt in the future.

Due to the low level of cash and cash equivalents and the limited scope for raising fresh debt capital, opportunities for growth through acquisitions are limited in the near future.

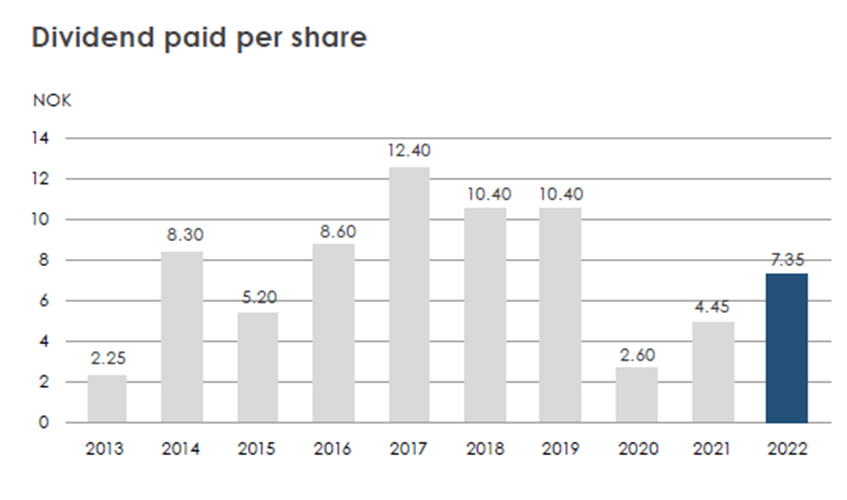

Dividend - Can I rely on it?

The company management pursues a clear strategy with regard to the dividend. In 2020, the Executive Board passed a forward-looking resolution to bring transparency and predictability to the dividend distribution. The dividend policy is clearly structured: At least 50% of earnings per share are paid out as a quarterly ordinary dividend. Any surplus capital is paid out to shareholders as an extraordinary dividend. The Board of Directors makes these decisions taking into account expected cash flow, investment plans and financial flexibility. A long-term target for interest-bearing net debt is regularly reviewed and updated.

A look at Mowi's dividend in recent years shows the fluctuating development of the company's profits. Determining a dividend yield or dividend growth is not expedient at this point, as the dividend, as shown above, merely follows the profit trend and therefore strong fluctuations are to be expected in the future.

Mowi's dividends 2013 - 2022 (Annual Report 2022)

{kind=link}

In addition, a look at the company's cash flow statement reveals that in recent years, the amount of dividend payments has exceeded the amount of free cash flow on several occasions, meaning that the dividend had to be financed in part with the help of debt capital or from the company's assets. This leaves no scope for consistent and sustainable dividend growth.

Risks - How risky is it actually?

Mowi is subject to a number of risks that are of central importance to the future development of the company.

One of these risks is environmental influences. For example, higher temperatures as a result of global warming can promote algae infestation in water systems, resulting in poorer water quality. Such a problem led to a negative result in Canada this year. Environmental influences such as the El Nino hurricane also resulted in poorer water quality, which in turn led to significantly lower profitability in the respective regions.

Another problem is the high susceptibility of salmon to diseases such as sea lice. These can lead to the death of salmon and often threaten a large part of the harvest of an entire region. Mowi has recognized this challenge and taken a number of precautions. Nevertheless, diseases still pose a risk to future salmon harvests.

Regulatory restrictions are another not insignificant factor for the company's profitability. For example, the Norwegian government's announcement of a 40% resource tax on aquaculture led to a sharp drop in the share price in 2022. Ultimately, this same tax of 25% was introduced in the middle of the year. However, this incident clearly shows how dependent Mowi is on the requirements of a few governments. This also applies to the same extent to the granting of licenses, which are a basic requirement for salmon farming.

In my view, Mowi has proactively addressed these risks in the past, for example through regional diversification, and has been able to significantly reduce them in recent years.

Valuation - What value am I getting for the price?

To calculate the valuation, a few factors must first be determined. The decisive factors here are the sales volume and the price of salmon. While the volume of salmon harvested will increase by around 5% annually, I assume an average medium to long-term conservative profit growth of 7-8%, which roughly corresponds to the growth of the market. This thesis is also supported by market studies that predict medium to long-term growth in the price of salmon, as supply on the market (3-4% p.a.) cannot keep pace with rapidly rising demand (11% p.a.). Furthermore, I assume that an average ROCE of around 12% can be achieved in the future, which is also in line with Mowi's management targets. Based on these assumptions, I currently consider the company to be fairly valued at USD 22.

Another aspect that I do not want to withhold is the valuation based on the price/book value. This seems reasonable, as I believe that Mowi's licenses are undervalued. These are acquired from the state and can be used for an unlimited period of time for salmon farming. Mowi has always reported the licenses on its balance sheet at the purchase price. In the meantime, many of the licenses have been held for a long time and have since increased in value due to the increasing demand for salmon and a very limited amount of licenses. At the last auction, prices were twice as high as at the previous auction. These are therefore hidden values within Mowi's balance sheet that would justify a higher valuation.

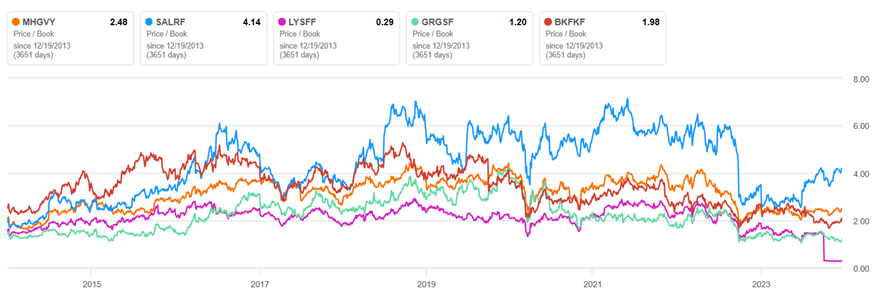

10-year Price/Book of Mowi and competitors (Seekingalpha.com)

{kind=link}

Another aspect for the valuation of Mowi was the already described taxation of Mowi by the Norwegian government. Following the announcement of the tax, the share price initially fell significantly, as Norway is Mowi's largest and most profitable market and the increase represented a risk for Mowi. Now, after eight months of discussions , the tax has been set at 25% in mid-2023. According to Mowi's statement, in cooperation with tax experts, the actual impact on the business has been analyzed and has come to the preliminary estimate that the effective increase in the tax rate for Mowi is around 10%, as a significant part of Mowi's value chain is not affected by the tax. This means that there is no longer any uncertainty for Mowi and the burden is significantly lower than initially assumed.

Taking the known figures into account, the fair value is USD 22. At the current share price of USD 17, this would represent an upside of around 30%. In addition, the undervalued licenses and the significant valuation discount in the context of the tax discussion represent a clear margin of safety. In my view, the current valuation level of Mowi makes it a clear buy and my high conviction pick for 2024.

Editor's Note : This article was submitted as part of Seeking Alpha's Top 2024 Long/Short Pick investment competition , which runs through December 31. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!”

For further details see:

Mowi ASA: The Future Of Fish Farming