MHGVY - Mowi: Eventually This Will Stop Going Nowhere - I Say 'BUY'

2023-10-01 10:58:22 ET

Summary

- Mowi had a record-breaking quarter with high revenue and stable expenses, indicating plenty of upside potential.

- The company has a stable dividend yield of 4.2% and a resource rent tax of 25%, which is lower than feared.

- Mowi's valuation is primarily influenced by salmon pricing trends, and the company has maintained strong pricing and contract discipline.

Dear readers/followers,

As you can probably tell from my previous articles not only on Mowi ( OTCPK:MHGVY ) but other salmon plays like Bakkafrost ( OTCPK:BKFKF ), I remain a Salmon "Long" as long as the valuation is appealing. It is, in fact, an area that I love investing in. If and when Mowi drops below 170 NOK, I do a two-pronged buying approach. I buy both the common share, while also writing appealing options on the CSP side for even lower-priced shares if the company should fall below what I consider it's worth at the very least.

This should tell you something about how positive I am about this business.

Mowi doesn't have the best history in the business. That honor goes to Bakkafrost. That's why, despite a materially lower yield in the Faroe company, I'm longer Bakkafrost than Mowi. But Mowi is still a solid play here, and with the politics of everything slowly taking a backseat, I am updating my thesis on Mowi here.

Mowi - Plenty of Upside here

2Q23 is the latest report we have for Mowi - and the trends do not justify this latest quarter and period of no excitement that we're seeing for the company.

Why?

Because Mowi had a record-breaking quarter - yet another one. Mowi saw and all-time-high revenue of over €1.3B Euro, with an operational earnings before taxes (EBIT) of just north of €300M. The farming costs and overall opex side were stable despite this revenue increase , and cost-to-stock and feed prices are actually down for the sequential period. The same stable farming and expenses for the farming side of things are expected to continue going into 2H23.

We're seeing significantly appealing harvest volumes.

How?

Because they were even higher than the already-high guidance, due to efficient production and higher survival rates of fish. The weakening of the NOK continues to wreak havoc on the FX side, but just like Sweden with its currently super-weak currency, there is nothing that individual companies can do about this. It's a €42M hit for Mowi versus the pure Norwegian peer group in salmon farming.

EPS/results in key segments (Consumer Products) is at seasonal ATHs due to strong yields and good efficiency, and we have clarity on the political side of things. (Source: Mowi 2Q23)

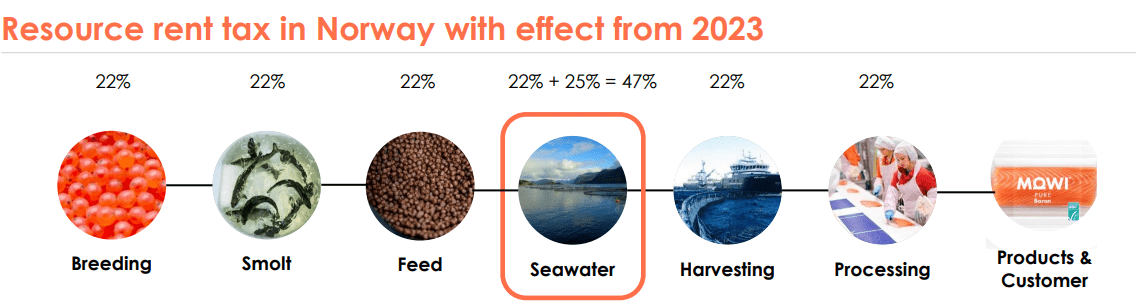

What we are looking at for Mowi is a resource rent tax of 25% which is now approved in Parliament. This is below, well below, the feared rate, and means that Mowi will be taxed at 47% including corporate tax. As of this update, Mowi provides a 2 NOK/share quarterly dividend, which based on the current share price comes to a not-at-all unattractive yield of 4.2%. It's well above the yield of Bakkafrost, even if it's nowhere near the levels that the company's predecessor-in-name offered, which at times was above 6%. Many dividend investors hoped for the company to maintain this sort of dividend approach, but I for one am happier with the more stable but more reliable dividend.

Unfortunately, with current estimated net earnings of around 14.3 NOK/share (Source: FactSet, Adjusted EPS forecast), it's still at a somewhat high payout ratio given the company had to lower it in 2020 from 2019.

A quick word from the global salmon macro.

{kind=link}

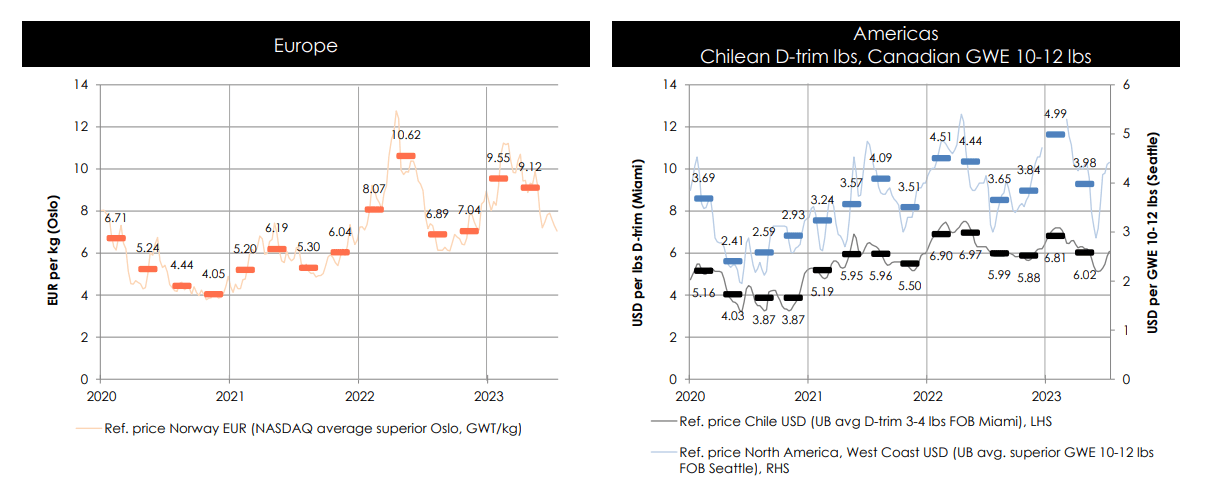

Just as with energy or other heavily correlated sectors, Mowi's valuation is primarily a product of the salmon pricing trends. That's why it pays to keep an eye on such trends. The current lower prices for American-origin salmon versus European salmon have to do with volume influx trends on the NA market. EU prices were strong - there's a qualitative upside to European salmon, which is why the best Salmon is fished/farmed here, even if it's down YoY due to ongoing supply contractions. All in all, I don't see a catalyst for another major downturn, but this is something you want to keep a close eye on.

Mowi meanwhile, has maintained a strong pricing and contract discipline, with everything except Canadian salmon.

{kind=link}

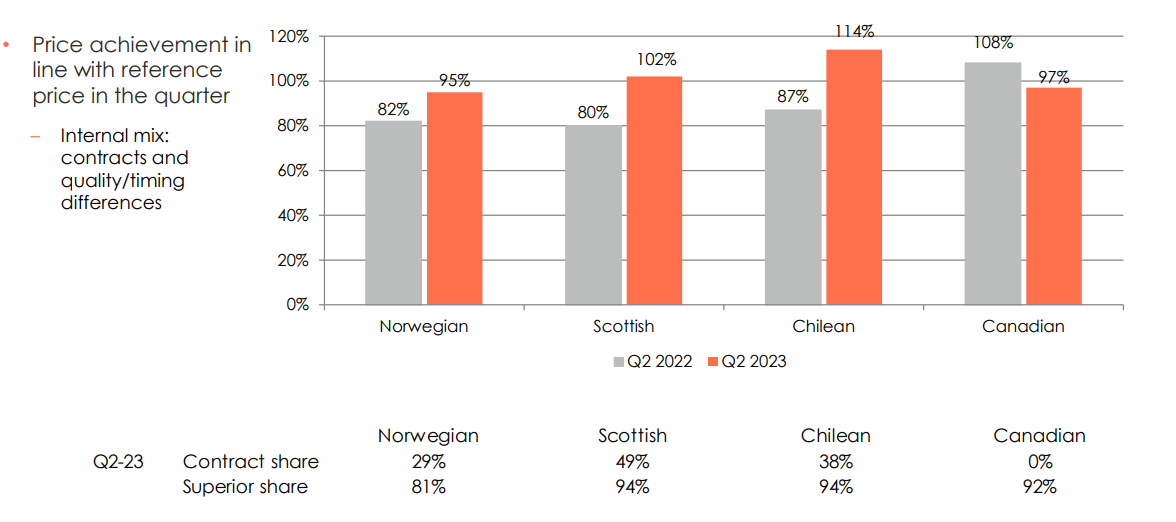

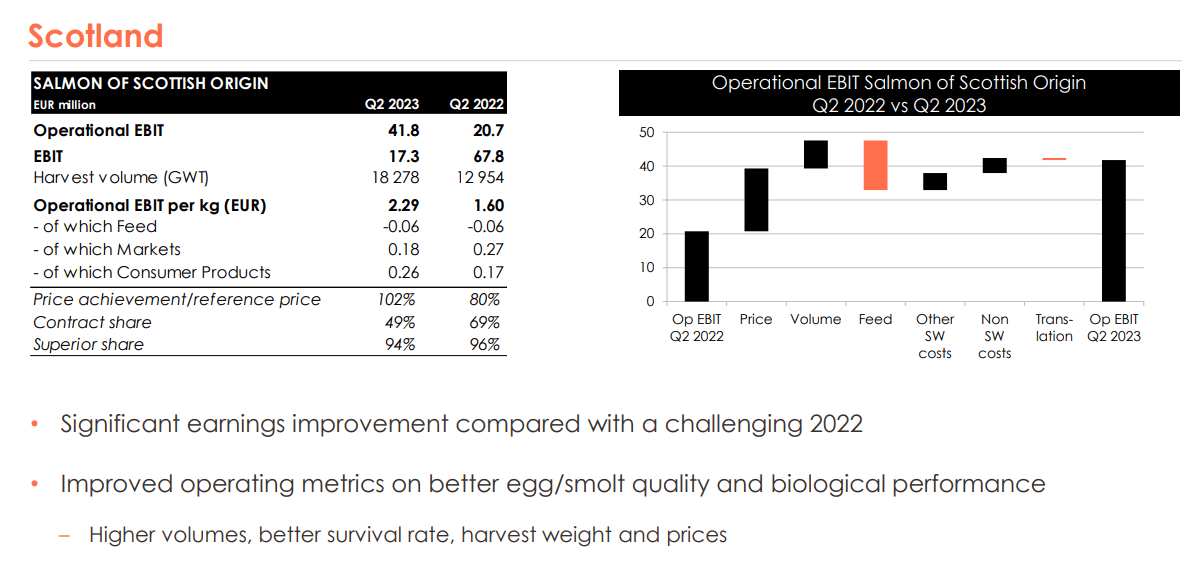

The main negative for this quarter, and there are negatives, are the operational EBIT drops - significant ones, in the mid-region. The volumes in Canadian salmon were down by significantly due to both low harvesting and problems at the production/farming sites, with turnarounds already initiated. Yet despite this, the company expects the second half of the year, where we're likely to get indicators in a month or so, to remain stable. And most of the companies' regions, such as Scotland, actually saw significant improvements.

{kind=link}

Canada was the "black sheep" of the quarter here, and I don't foresee an easy solution to this either. However, with Mowi's size and scale, they can afford to have 1-2 segments that don't operate at the same superbly high level as others, while trying to improve them. We'll revisit the segment in 2H23 and see if anything needs changing.

The company's quarterly P&Ls were superb, as indicated. I don't see any material issues or worries that are worth lifting here. 2Q22 was a superb quarter in terms of profitability - and so earnings did not match those, even if sales revenues came in at record levels - but we need to consider the negative impacts of both Canada and FX.

Here is a good summary of how the recent political changes and the resource rent tax impact the industry.

{kind=link}

The lack of clarity has long been a significant drag for the company here. But the advantage is, as of right now, only the seawater phase is in scope for the tax - and there is current work ongoing to establish the correct pricing method. The impacts of these changes are not yet included in the quarterly P&L in the forecast, but the company is applying a conservative approach for the underlying EPS and ROCE - and the one-offs are currently included.

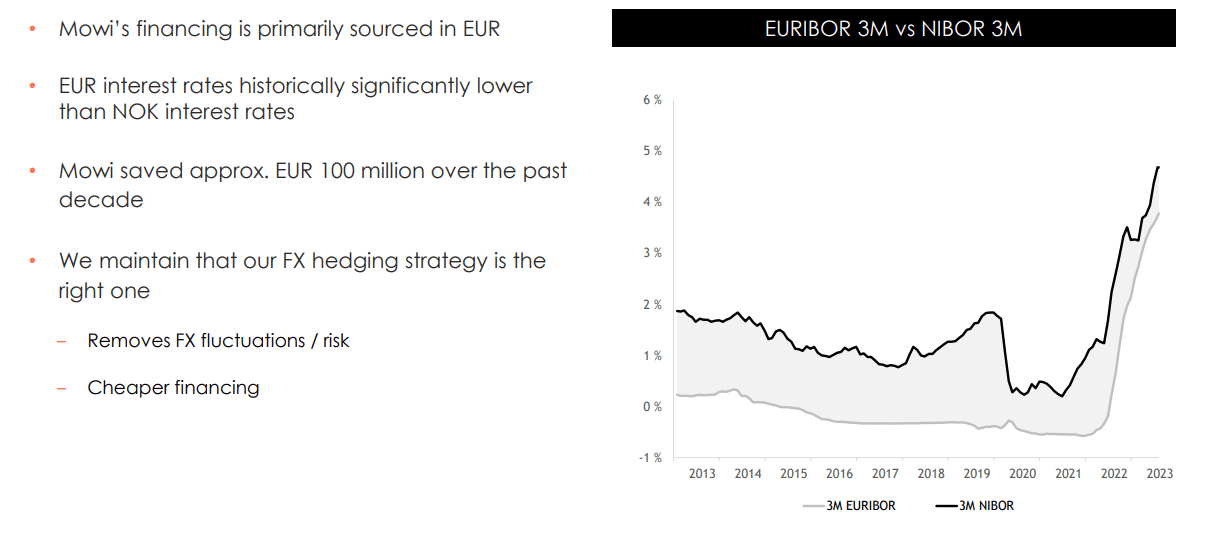

The FX is another thing worth mentioning. It's currently very negative. Historically, the company's EUR dependency has actually been a significant positive from a cost perspective. This has now been reversed and with a vengeance.

{kind=link}

I share the company's view here that moving to EUR or USD is the right choice. The NOK isn't the SEK and its weakness, but I believe in the future, these smaller currencies are going to see significant weaknesses and issues. That's why I am pro-EUR for Sweden - though I know that realistically this is not something we would be able to get for several years.

However, it's why I diversify heavily FX-wise, and only 34% of my portfolio is in my native currency.

The company has worked diligently to reduce working capital - but its work to lower NWC from non-marine feed input is currently offset by price increases in other inputs such as fish meal. CapEx for the company comes in at around €380M for this year (Source: Mowi 2Q23 Cash flow Guidance), and that's a significant amount of investments across the value chain - everything from freshwater to seawater investments.

On the fundamental side, with current financing, we're seeing repayment of bonds, we're seeing over €2B available in a new facility with an attractive covenant of 35% equity, and a €100M accordion, and we're seeing good new bonds with...so-so interest rates. We're talking mostly Euro, so we're working with EURIBOR rates, and those are at EURIBOR +1.6%. Not the best, but okay.

I don't see any fundamental issues on the balance sheet or operational side as things are now - with that, here is the upside and valuation after 2Q23.

Mowi - The updated valuation

So, Mowi really hasn't gone to a lot of good places (up) since I started investing in the company. My options for the company have obviously made sure that I'm at a significant positive for my investments here, but as to the common shares I own, those haven't gone much to the upside.

The future for the company is both good and bad. Good, because 2023E EPS is probably going to be stable. Bad, because from 2024E and forward, the resource tax could bite into profits, seeing at least a single-digit deterioration into 2025E. What this will do with the share price is something that will have to be seen.

However, this complex set of forecasts is why I maintain an option-heavy stance on Mowi.

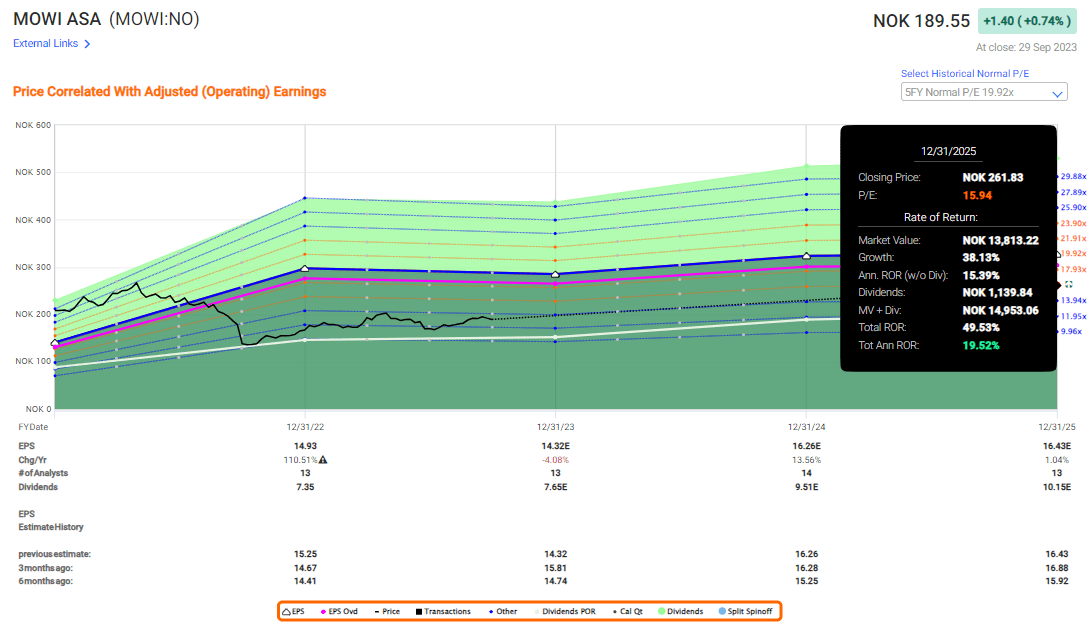

The current P/E for the native based on 2022A results is 12.69x, and for current estimates (depending on where one lands) is around 13.2x or 13.09x blended P/E. I still maintain that Mowi is worth at least 235 NOK. I maintain my "BUY" on this company, that's for certain sure. If we value the company at a 15x P/E, this company based on 2024E is valued at around 243 NOK/share for the native if trading at 15x P/E based on the current set of earnings estimates (Source: F.A.ST Graphs). This gives us a 3-year upside to 2025E of about 16.6% per year, even at a price of almost 190 NOK/share. It's good enough for me to maintain my "BUY" rating on the company.

As long as the company is below a 12.5x normalized level in terms of P/E, I would view this company as a very solid "BUY". But for those with the ability to trade native options, I say that this is a very appealing alternative you because the premiums are attractive and the annualized levels of yield during days it moves down (resulting in higher premiums) are also excellent.

You can easily, during down days, get annualized yields of around 10-13% on this company going 10-13% below the current share prices. It remains one of the few companies where CSP premiums haven't deteriorated completely. In other options, I'm having difficulty finding anything close to the yields of 10-15% that I was used to with conservative share prices during late 2022 and 2023 up until about summer.

The company remains a very good bet on Salmon. But Salmon is also notoriously fickle and volatile at times, so planning accordingly is a fundamental requirement here.

I give you, therefore, my current thesis on Mowi ASA. I would say the company has a continued upside of 18-19% per year in accordance with what you see here.

F.A.S.T Graphs (F.A.S.T Graphs)

{kind=link}

Thesis

- Mowi is a market leader in the global industry of Salmon and fish farming. The company has good fundamentals, and competitive yield, and more importantly, is quite undervalued despite a recent climb back to higher valuation levels.

- With the proposed legislation essentially canceled in its original form at this point due to protests, I believe one of the more essential risks has been removed, which increases the appeal of the company.

- For that reason, I give Mowi a PT of 235 NOK and call it a "BUY". This rating remains as of October of 2023.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

I believe the company fulfills all of my fundamentals and criteria here - it's a "BUY".

For further details see:

Mowi: Eventually, This Will Stop Going Nowhere - I Say 'BUY'