MNHVF - Mowi: Norwegian Salmon Still Has Upside

2023-11-26 22:37:29 ET

Summary

- Mowi's 2Q23 was a record-breaking quarter with high revenue and stable expenses, indicating upside potential.

- The company's valuation is primarily influenced by salmon pricing trends, and it has maintained strong pricing and contract discipline.

- Mowi's 3Q23 report shows good EBIT, record-high consumer product sales, and a strong position as the world's most sustainable animal protein producer.

Dear readers,

Mowi's (MNHVF) 2Q23 was a record-breaking quarter with high revenue and stable expenses, indicating plenty of upside potential. Like other salmon companies, the company's valuation is primarily influenced by salmon pricing trends, and the company has maintained strong pricing and contract discipline over time here. In this article, I'm going to look at if the same sort of discipline has been applied for the latest period, and where the company may go from here.

I've invested in Mowi in a few different ways this year - mostly, I've been using put options to gain exposure to the company at very attractive prices, without any of these options going through, resulting in double-digit annualized premium yields. However, I've also been open to actually adding shares at the market price if the company were to drop low enough to make this interesting.

A few weeks ago, this was relatively close to happening, but then the company did reverse.

Let's look at what upside we can see in Norwegian salmon here and what to expect from the company.

3Q23 is the latest report, which is less than 2 weeks old at this point. This is an updated piece to my last Mowi piece, which you can find here .

Mowi - Continued long-term upside from fundamentals and consumption of salmon

Mowi reports, for the 3Q23 period, a good EBIT of over €200M although farming costs due to inflation and macro were up slightly. The overall weakening of the NOK, which has been dropping over the past few months, means a €35M hit for the company versus its peers given the ties to the Norwegian crown.

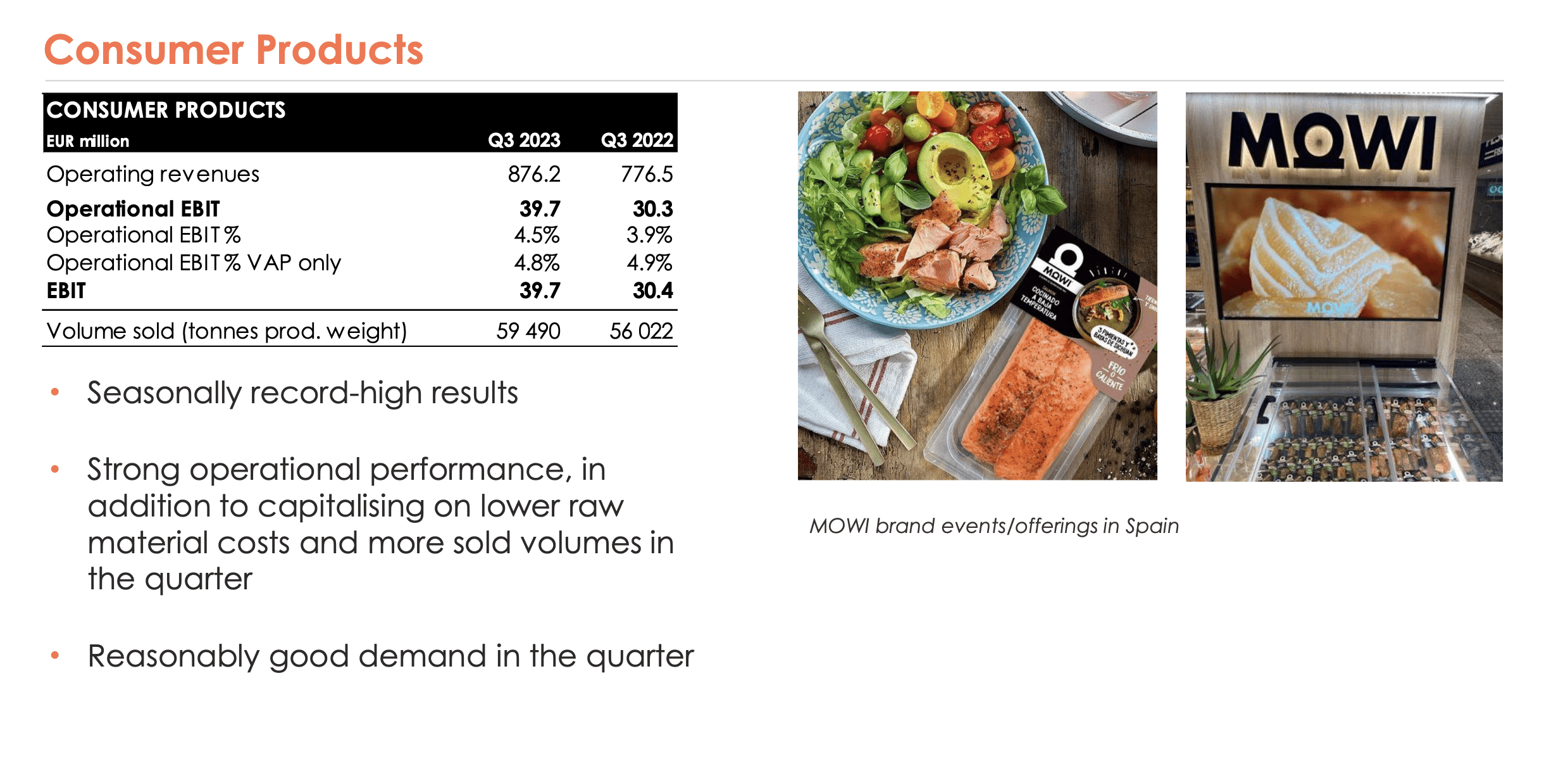

However, this was somewhat weighed up by seasonal record highs for consumer products, feed earnings, and feed volumes at record levels, implying that despite this, the company is still working well. The company continues to be ranked as the world's most sustainable animal protein producer - and this is the fifth year running the company has received this award. (Source: 3Q23 Results )

What's perhaps more important, given that this has been in the pipeline for a very long time, is the inclusion of an estimate for the effective resource rent tax - about 10% - for Mowi Norway across the value chain. This sort of tax and percentage is of course unwelcome news, but given how everything is looking and how high this could have been, it's still better than some of the scenarios showed this as being.

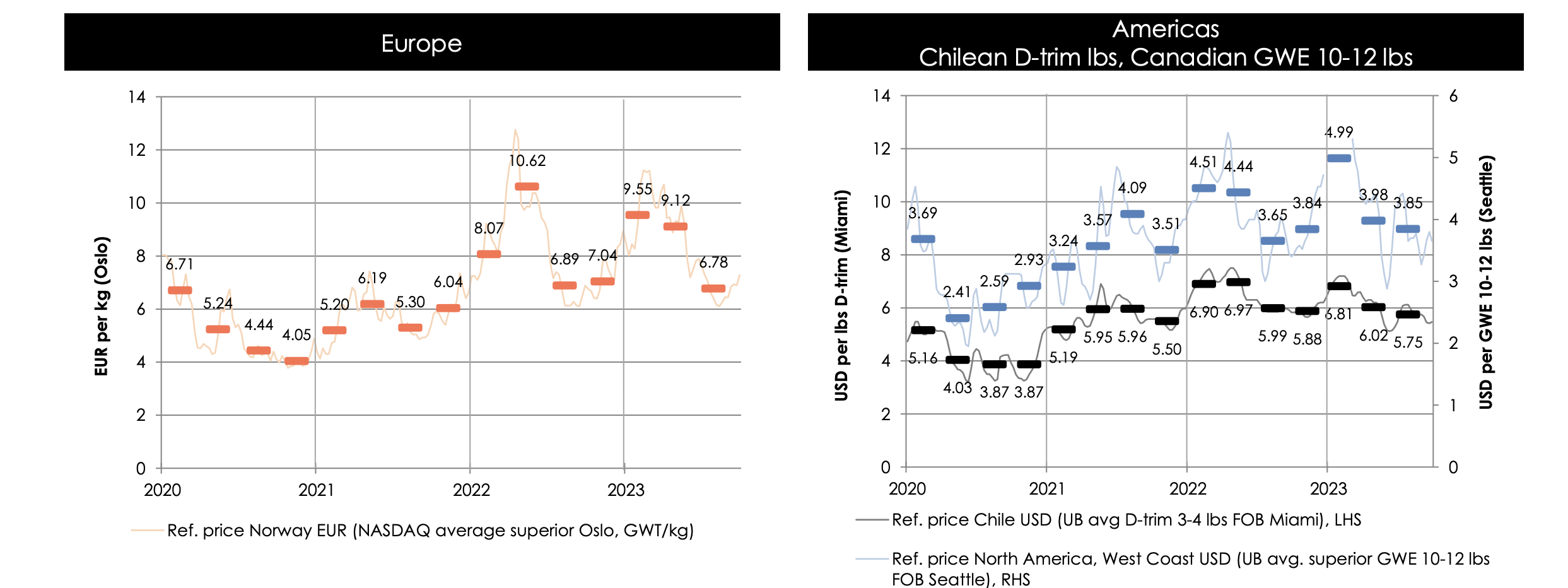

As I said initially, Mowi as with all salmon producers primarily plays on global salmon prices - you can almost follow the company's share price as it moves close to tandem with some of these trends here.

{kind=link}

Still, prices in Europe are actually good for the overall period, with only Chilean prices really showing over 3% year-over-year declines. Also, Mowi's products continue to demand a premium, close to double digits compared to the reference price due to good contracts and contributions from other segments. Only Canadian salmon here are seeing reference, or slightly below reference pricing trends. (Source: 3Q23 Results)

Comparing the 2Q and 3Q results, Mowi's results are down about 15% in EUR, which is mostly due to FX. In NOK terms, the company's results were far less impacted, less than 5%. Farming as a segment was a mixed bag due to the impacts of El Nino but weighed up by strong operational performance in Feed and Consumer products. While not growing as much as expected, the company still increased guidance on GWT to almost 300k due to strong growth in the sea segment.

The share of contract volume is growing, with around 22% contract share for 3Q, and almost 30% for 4Q due to relatively stable pricing trends - that's for Norway. The Scottish and Chilean geographical segments were a bit more mixed from higher biological costs, and weather effects, but even with these, the segments managed strong pricing and fundamental trends. Canada was impacted meanwhile by algae mortality at the facilities in British Columbia, but Canada East managed good performance. (Source: 3Q23 Results)

Also, Mowi remains one of the few players that's allowed to farm both in Iceland and the Faroes, which still remains an advantage to the company compared to many of its peers here.

Consumer products deserve highlighting, managing seasonally high results - and the company's offerings are receiving more traction across Europe.

{kind=link}

Another thing that deserves if not highlighting, at least some space in the article is the final effects on an estimated basis for the resource rent tax and how this will be calculated. Even with this calculation though, it's still a preliminary estimate, but one that is perhaps more potentially accurate than the previous estimates and forecasts here.

Overall, the cost of the company's farming for the entire year is actually down, due to stabilizing feed prices - and volumes for harvest in South America could mitigate the record-high prices for marine ingredients that are crucial to the company's value chain, in particular fish oil. (Source: 3Q23 Results)

For the 2023E period, the company is now expecting a CapEx of slightly below €350M, which is a reduction compared to the previous, and an ongoing quarterly dividend of 1.5 NOK/share per quarter, coming to 6 NOK/year, which comes to a current yield of around 3.2-3.7% depending on FX. The material weakening of the NOK also has an impact on the dividend of course, and it means that Mowi, at this particular price and dividend yield compared to what else is available on the market, isn't all that attractive given how much of a yield you can "easily" get.

The upside is combined here. I believe Mowi to be worth at least 15x P/E, and for the 2023 period, the company is expected to manage a native EPS of 15.5 NOK/share, growing by around 5-8% on average both in 2024 and 2025E, given increased consumption and positive trends from both production and consumption growth, likely hampered slightly by pricing increases. (Source: 3Q23 Results)

Salmon pricing trends continue to make this company - or any company like it - difficult to forecast here. As before, I don't see any fundamental dangers in terms of either the balance sheet or the next 3 years of result forecasts. While downturns in a volatile commodity like salmon are possible, the longer-term impact on the company's earnings or its business model is, once again, estimated to be limited.

Valuation continues to show a very strong price disconnect here - and in the next section, I'll remind you of this.

Mowi Valuation - At this price, we have a significant upside

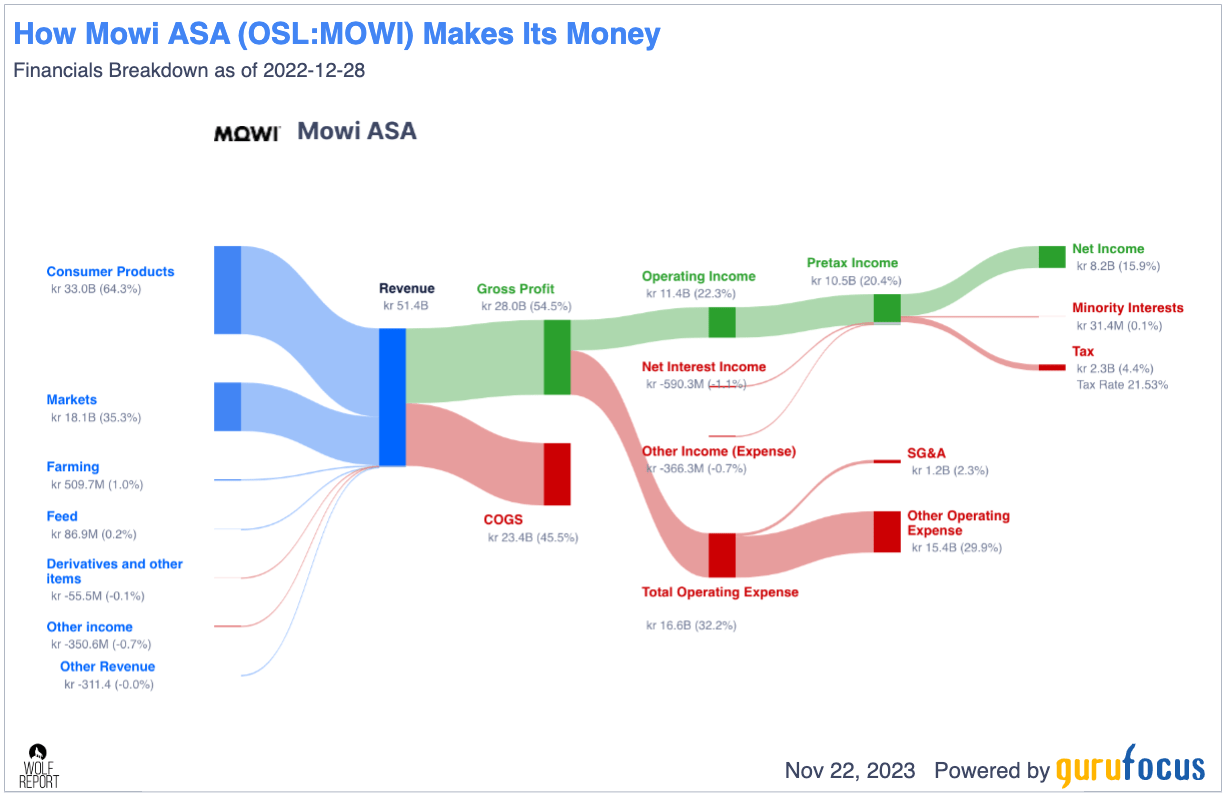

It's important to understand how solid Mowi's business model actually is, and how well the company performs in comparison to other Salmon companies and even other consumer goods companies. Mowi manages 48%+ gross margins and 18.5%+ EBIT margins with over 7.5% margins on the net profit side. They combine this with a debt/EBITDA of less than 1.7x. They also combine this with a very solid revenue growth trend. Even the slight pressure on EBIT margin, which is completely understandable given cost trends, and the increases in debt can't do much to impact what I believe to be the company's long-term appeal here.

And that 7.5% net margin - that's actually a low point for the company. Take a look at how good the company's results were during the last fiscal, and where I believe the company is going.

{kind=link}

It's important, I believe, to point out just how undervalued based on peer metrics things are here. Based on a simple DCF-based forecast with a basis of EPS, the company is, if the company manages this level with an EPS growth of about 5-8%, worth at least 250-280, depending if you look at FCF or EPS, and how you discount the company. A 250 NOK share price would, by the way, imply a 15x P/E for the company, which for this business is more than a "fair" estimate in my opinion.

Analyst fair value estimates range between 195 NOK to 280 NOK, also well above the current level, with a most recent fair-value price estimate of around 260 NOK/share (Source: S&P Global, TIKR). Out of 10 analysts, 7 have the company at a "BUY" here.

The reason why I've used put options to gain exposure to this company is simply that the relative yield of below 4%, even with a potential upside to P/E 15x, is better "played" using conservative options.

The upside for Mowi to that P/E 15x is no less than 22.4% per year until 2025E, with an implied FV of 263 NOK at an exact P/E 15x. The company has typically traded as high as 19-20x P/E, which would imply something close to 350 NOK, and an upside almost in the triple digits for the forecasted period here - but I view this as being far too rich in valuation at this particular time.

If you recall my previous pieces, I forecast the company to around 12-13x P/E to remain really conservative here, and despite this low level, the company still manages a 15%+ annualized upside from this. It's not the highest one I consider available on the market, and you can see in the company's share price just how volatile these trends and this company can be - but fundamentally speaking , I do not believe there to be anything wrong with investing here at this time.

The company remains a very good bet on Salmon. But Salmon is also notoriously fickle and volatile at times, so planning accordingly is a fundamental requirement here - and that is why my main avenue of investment for this particular play remains options. I currently do not have any options "running" for the company, but may add some if things decline again.

Here is my updated 3Q23 thesis for Mowi.

Thesis

- Mowi is a market leader in the global industry of Salmon and fish farming. The company has good fundamentals, and competitive yield, and more importantly, is quite undervalued despite a recent climb back to higher valuation levels.

- With the proposed legislation essentially canceled in its original form at this point due to protests, I believe one of the more essential risks has been removed, which increases the appeal of the company.

- For that reason, I give Mowi a PT of 235 NOK and call it a "BUY". This rating remains as of November of 2023.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansions/reversions.

I believe the company fulfills all of my fundamentals and criteria here - it's a "BUY".

This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

Mowi: Norwegian Salmon Still Has Upside