MHGVY - Mowi: Opportunities Remain In Salmon Farming

2023-04-10 10:49:13 ET

Summary

- When I last wrote about Mowi, I caught the company at an excellent valuation with a high yield - at least as I see current forecasts.

- I believe Mowi is worth significantly more than the company is currently being traded for on the market. The upside is still there, and the upside is worth investing in.

- While some underperformance has occurred, the long-term prospects for Mowi are intact - and here is my reasoning for that upside.

Dear readers,

People often ask me how I choose the companies that I invest in, and how, when these companies encounter instability or drawdowns, I can remain so calm in the face of what is perceived as adversity.

Well, a few things - and it really is about a combination of factors, not one specific factor. But something that definitely helps is picking companies that are already among the market-leading businesses in their specific sector.

When I worked through my last article on Mowi ASA ( MHGVY ), I made notice of the fact that I haven't been clear enough on just how far this company outperforms many of its peers. The salmon farming industry is a competitive place, and while Mowi has things to improve, as all companies do, there is an underlying stability and safety to the business that precludes true instability or decline - at least insofar as I see things here.

Let me clarify what I mean by updating my Mowi Thesis, and showing you why this company is actually undervalued here.

Updating on Mowi and the upside

So, straight to the point. Aside from being one of the most significant salmon farming companies on the planet, Mowi also happens to be one of the most profitable businesses in the entire sector - in the world. The company, whose previous name for which it is more known as Marine Harvest ASA, was a favorite for many income-oriented investors. I recall looking at the company many years ago, and the main argument people brought up was the high yield, which would sustain investors safely.

Of course, that's not exactly what happened - and I now believe their focus was somewhat misdirected.

Mowi's main argument, or what should be the main argument for the company, is the sheer profitability in context of the company. You can look at Mowi as a consumer packaged goods company, or as a salmon company, and in either of these contexts, Mowi is a company with good performance.

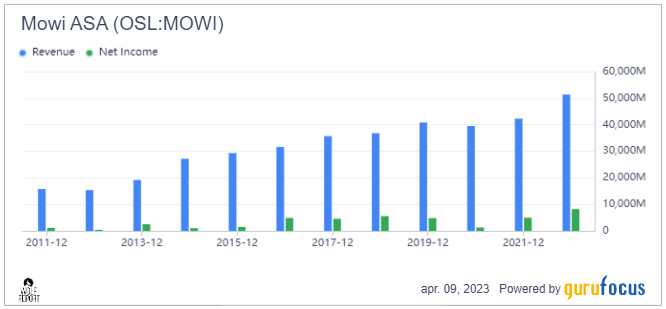

Revenue and net income, while having seen a decent amount of net income volatility, have remained solid and growing.

{kind=link}

The company is also a consistently profitable operation in terms of the returns on its investments. While Mowi has seen some downer years, and while the company has been mixing between issuing equity and growing, meaning shares outstanding is growing on a 10-year period, the company is nonetheless impressively profitable even under today's circumstances and the environment we're going into. The company's ROIC can "take" increased cost of debt and capital without going negative - as is evidenced by the latest set of company results.

The company is vertically integrated. This means aside from farming and providing fish, like other companies in the same segment, they also operate their own VAP segment through which it distributes a range of seafood products, as well as owning a number of small subsidiaries.

It's also one of few Norwegian companies that offers a quarterly dividend. Mowi is BBB rated, and isn't all that hard to comprehend, even for investment laymen, even if the underlying drivers of the company may be.

Mowi is among the top 80-90th percentile in the industry in every relevant profitability metric worth mentioning. This includes gross and net margins, operating margins, ROE, ROA, ROIC, and ROCE. We can also compare it to straight salmon farmers, a much smaller group, and Mowi still does well. It's dividend yield of 3.8% is nothing worth writing home about compared to what it once was under the form of Marine Harvest ASA, but that 3.8% yield comes at a dividend payout of less than 45%, making it a very safe dividend in the industry and in context.

{kind=link}

4Q22 is the latest set of results we have - and it was a highlight of the year. The company reached ATH revenues of almost €5B as well as an operational EBIT of over €1B, giving the company a full-year EBIT margin of 20%+.

Farming costs came in at relatively stable levels, and there is a continued combination of attractive, good demand and relatively low supply on the market. Mowi harvested more salmon in 4Q than they did in any previous quarter, and they're on track to break that record, on a full-year basis, once again in 2023.

{kind=link}

Improvements were broad-based and came in every single segment and business area. The company has managed organic growth over the past 5 years that has really outperformed, at a CAGR of nearly 7% in terms of harvesting. This is well above the industry norm.

{kind=link}

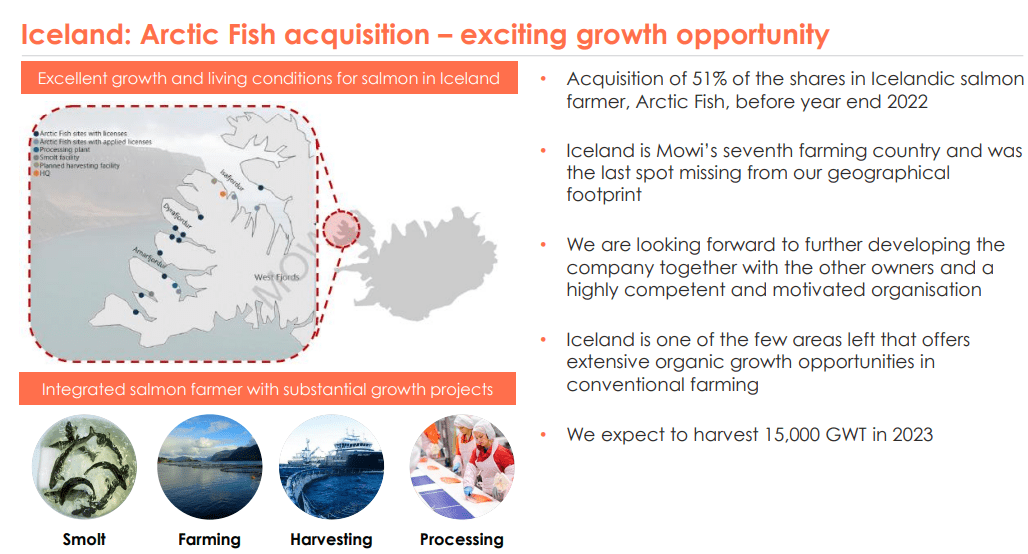

The company has also been active on the M&A side of things, recently finishing its M&A of over half of the Icelandic Company Arctic Fish, and it has guided for an appealing dividend on a quarterly basis in 2023.

Mowi is now ranked the world's most sustainable animal protein producer. This is not necessarily news, but it is news when it's done for the fourth year in a row.

Sales in the consumer goods section showcase just how attractive the company's products are viewed on the market - this is an easy one for me, because I myself actually buy and eat Mowi salmon on a weekly or bi-weekly basis. Not only is it one of the healthiest proteins out there, it also tastes amazing, and even more so when you prepare it with skill.

With the recently-suggested tax change in Norway that would have impacted companies such as Mowi significantly now ground to a halt, very few macro concerns remain for the long term for this company. We could look at some lock-up of Working capital, but there's going to be a €150M release we'll see due to the temporary build-up of last year - so know that on the cash flow front. CapEx for the coming year is guided below €400M, with investments across freshwater, seawater, and processing.

Any underlying cost pressures the company is experiencing are offset by cost initiatives - at least, until inflation from the post-COVID era started driving home. Things are still good, but inflation is picking up, especially due to feed prices. However, the company is still the #1 or #2 performer in its active regions.

Mowi IR (Mowi IR)

In short, the appeal for Mowi is based on broad-based fundamental outperformance. Mowi is one of the best-performing consumer packaged goods companies in the sector in terms of its profitability. While its asset growth has been picking up faster than revenues, this is understandable in the context of its growth strategy, and this also explains the new debt that's been consistently added. However, the company is growing revenues, and because it's one of the most profitable operators in the industry, this means it will grow earnings at or around the levels we've been seeing, at least for the foreseeable future.

That's one side. The second side is the fact that the company is being valued at really nothing close to its actual performance capabilities in my view.

Mowi Valuation - Appeal remains, for much the same reasons

My strategy for investing in Mowi over the past 8 months has been twofold. First off, I write 30-60 days cash-secured puts that usually net, if I do my job, between 8-16% annualized. I do these at very attractive prices, and so far, none of them has expired in the money. Secondly, when and if the company falls to prices I consider myself unable to ignore, I add shares as well.

This has resulted in a situation where I have several contracts running in Mowi at this time, but also have a long position in the company. My position in Mowi has done extremely well given my cost basis (below 155 NOK), and my options are set to expire worthless as well, given the climb the company has been doing here.

As I mentioned in my last article - the company does have local and close peers in the salmon farming industry itself. These include Bakkafrost ( OTCPK:BKFKF ), Leröy Seafood Group ( OTCPK:LYSFF ), Golden Ocean ( GOGL ) as well as SalMar ( OTCPK:SALRY ), meaning there is competition, but given the global state of the market, not as much as you think. What's more, given the negative move since my last article, Mowi is still considerably cheaper than other options here.

A simple EPS-based DCF with a growth rate of 4-6%, which is well below the company's estimated, as well as its historical EPS growth rate, gives us an FV estimate of 220 NOK, which implies a margin of safety of almost 15% even at this share price. According to services that track stocks, Mowi is also a very predictable company based on the consistency of its revenue per share and EBITDA - which in Mowi's case causes it to "score" more points as well.

Analysts following the company give us a mostly positive view on the business. We have 10 analysts, 6 of which are positive on the stock. Their average PT is around 250 NOK for the company, offering us an upside of over 35% from the current share price the company is trading at. That is from a range of 200 NOK on the low side and 280 NOK on the high side.

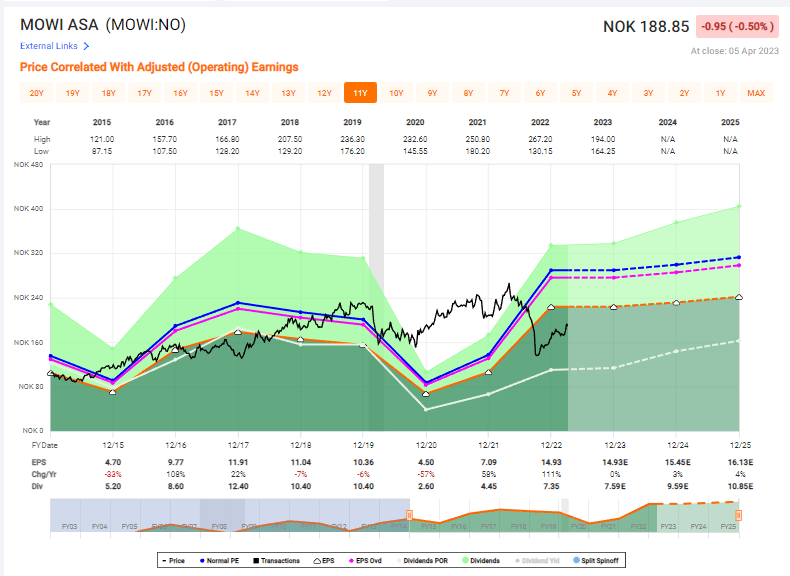

The addition of international equities to F.A.S.T graphs means I no longer have to look at ADRs for any of my international companies. While there isn't much variance most of the time, sometimes these can really change what I present and make readers confused. Here are the native F.A.S.T graphs for Mowi, and its forecasts in context.

{kind=link}

I would generally agree with the thesis/presentation we see here. Overall, I would say Mowi went into 2019-2020 somewhat undervalued given its earnings trends. Since normalization though, and since earnings have stabilized somewhat, I believe the company can be said to be worth more - if not the higher premium you see above.

My previous PT for Mowi was a conservative 235 NOK/share. This is below analyst averages, it's below where the company could likely go, and it's below the 19-20x P/E premium the company, on a historical basis, commands. Because this would imply a share price for 2025E of over 320 NOK/share, basically, I'm impairing the company by at least 25% to get a conservative share price. A full premium would mean an annual upside potential of 25% until 2025E, or 84% in total.

However, the company is currently trading at about 12.5x normalized. Even trading at this, or slightly below this level, would in the context of the forecasted 2-3% EPS growth, mean annualized RoR of 7-9% per year; which if only barely meets my demands, comes to a forecasted share price of less than 200 NOK per share.

That's the conservative case.

The "base" case I see is more of a 15-17x P/e, which goes into the 15-18% annualized, or over 45% total RoR in a few years.

That's where I continue to see Mowi, and that's the reason for my continued, positive thesis.

Thesis

- Mowi is a market leader in the global industry of Salmon and fish farming. The company has good fundamentals, and competitive yield, and more importantly, is quite undervalued despite a recent climb back to higher valuation levels.

- With the proposed legislation essentially canceled at this point due to protests, I believe one of the more essential risks has been removed, which increases the appeal of the company.

- For that reason, I give Mowi a PT of 235 NOK and call it a "BUY".

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

I believe the company fulfills all of my fundamentals and criteria here - it's a "BUY".

For further details see:

Mowi: Opportunities Remain In Salmon Farming