AIT - MSC Industrial Direct: The Move Higher Isn't Over Yet

2023-04-25 08:02:37 ET

Summary

- MSC Industrial Direct has done incredibly well from a fundamental and a share price perspective recently, with the stock significantly outperforming the broader market.

- The company most certainly is nearing a point where it won't be attractive any more, but current conditions suggest that recent outperformance can continue for now.

- This all implies that some additional upside still exists for investors at the moment.

The modern economy is made-up of many working parts. Much of it centers around physical structures, such as buildings, roads, bridges, and even smaller structures like furniture, equipment, vehicles, and more. It should come as no surprise, then, that all of these different structures would require certain goods and services aimed at not only producing them, but also maintaining and repairing them. And one company that's engaged in this kind of activity, with an emphasis on the supply of metal working, as well as maintenance, repair, and operations goods, products, and services, is MSC Industrial Direct ( MSM ). Although this may not seem like an area that would seem good given all that's going on in the economy, the management team at the business has done quite well in recent months and shares have benefited tremendously as a result. Although it's unclear how long this trend might continue, shares of the company do you still look reasonably priced on an absolute basis. Though it's also true that they are a bit pricey compared to similar firms, the company is still cheap enough and is exhibiting strong enough growth so as to warrant a soft ‘buy’ rating from me at this time.

Great results continue

When I write a company, unless I state otherwise, my belief is that investors should be prepared to hold the stock in question for the long run in order to generate attractive returns. But sometimes, you don't need to wait that long for upside to occur. A great example of a company that generated attractive performance in a short period of time would be MSC Industrial Direct. In an article that I wrote about the business in early October of last year, I rated the company a ‘buy’ to reflect my belief that it should outperform the broader market for the foreseeable future. This was based on attractive top line and bottom line performance reported by management. It was also based on how cheap the stock looked at that moment. Since then, strong fundamental performance has been instrumental in pushing the stock price higher. In fact, even though the S&P 500 rose and impressive 14.4% since the aforementioned article was published, shares of MSC Industrial Direct have easily outperformed that, experiencing upside of 26.7%.

{kind=link}

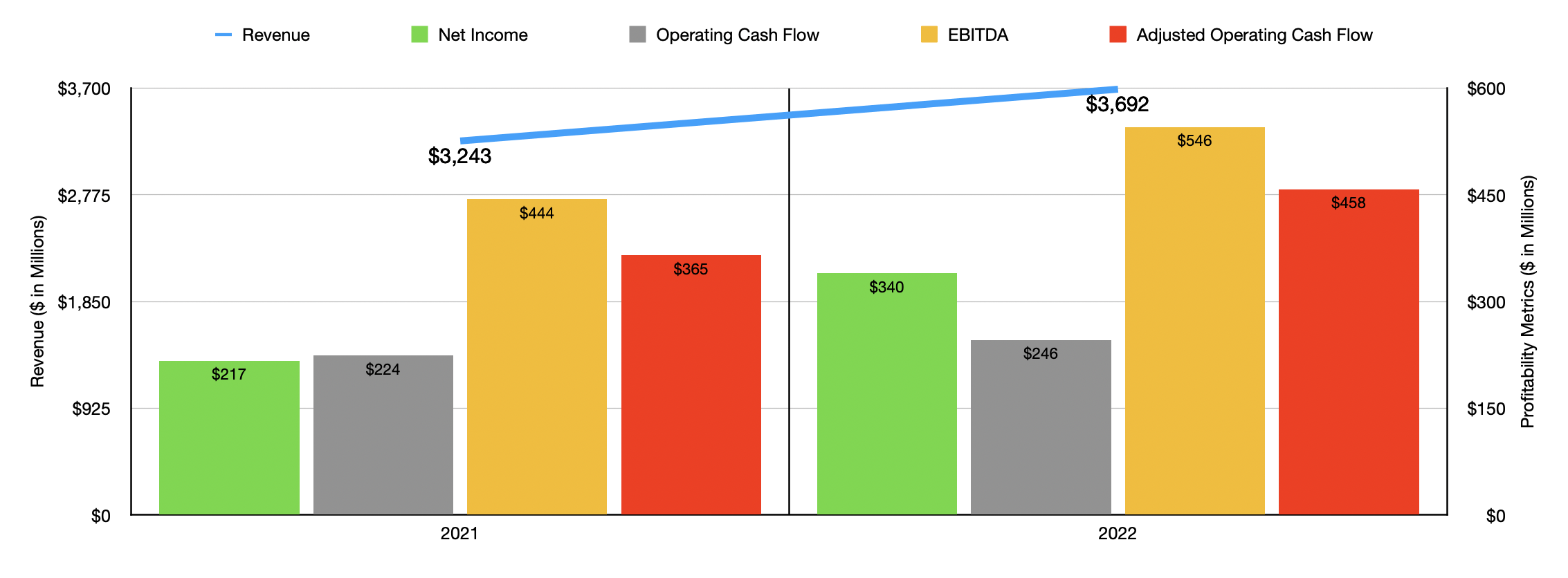

As I said already, this share price performance disparity came on the back of strong fundamental performance reported by management. As you can see in the chart above, MSC Industrial Direct managed to post some really impressive results for the 2022 fiscal year compared to the 2021 fiscal year. Revenue, for instance, jumped 13.8% year over year. Bottom line performance was also rather strong. But I would rather focus our time more on the most recent results of the company than on results that are that old.

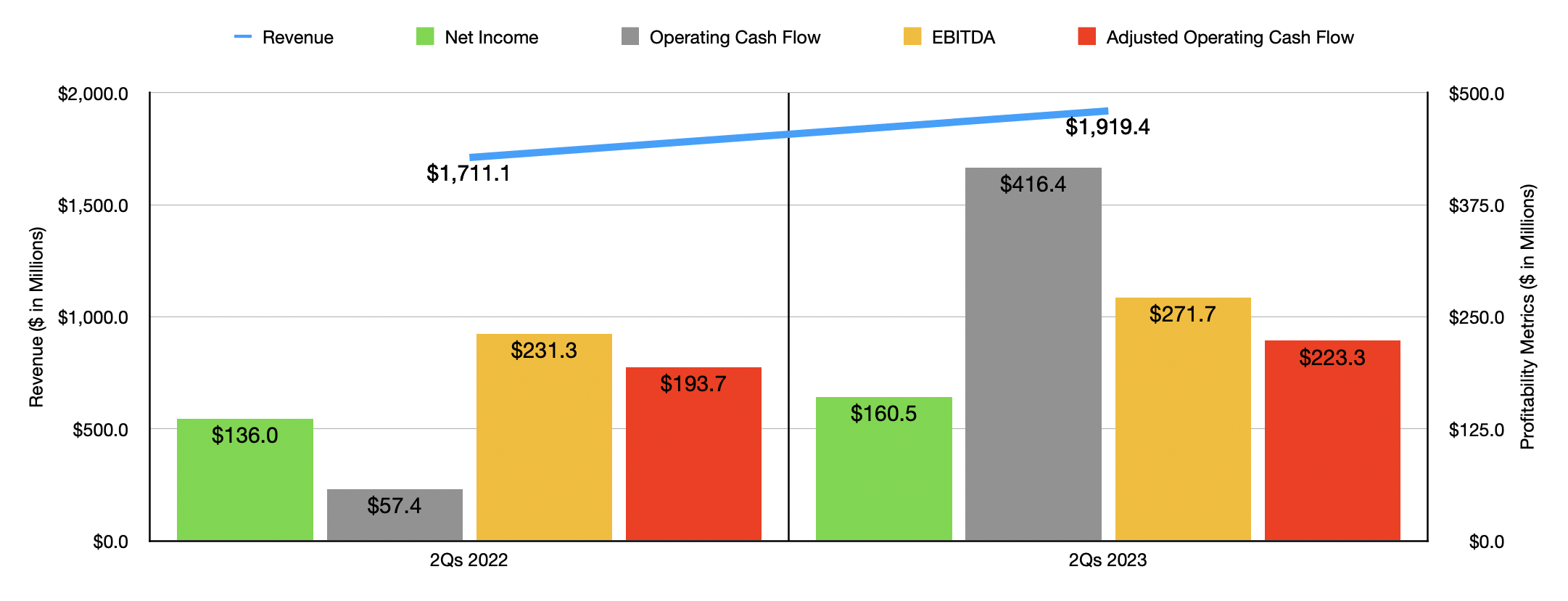

This brings us to how the company has been performing throughout 2023. For the first two quarters of the year, management reported revenue of $1.92 billion. That's 12.2% higher than the $1.71 billion the company reported one year earlier. This increase, totaling about $208.3 million, was driven by multiple factors. $98 million of the increase, for instance, came from higher pricing on the company's products. A combination of changes in product mix, discounting, and other factors, helped on this front as well. $61.9 million of additional revenue came from acquisitions, while $52 million was attributable to higher sales volume. Sales would have been slightly higher had it not been for a $3.6 million impact associated with foreign currency fluctuations.

{kind=link}

On the bottom line, the overall picture for the company was stronger year over year as well. Net income, for instance, shot up from $136 million in the first half of 2022 to $160.5 million the same time this year. Of course, we should also be paying attention to other profitability metrics. One of the most important, in my opinion, is operating cash flow. This metric skyrocketed year over year, climbing from $57.4 million to $416.4 million. But if we adjust for changes in working capital, the increase would have been more modest from $193.7 million to $223.3 million.

Given the state of the economy, I can understand why some investors might be cautious about the business at this time. However, management has been very clear that they see the demand environment as being particularly robust. At least that is what they stated in their latest earnings conference call. For the year as a whole, management is even forecasting revenue growth of between 5% and 9%. Even if the company does see some weakness in the near term, it has been building in long term recipes for success. Starting in 2020, for instance, management embarked on a plan to reduce costs materially over the ensuing years. This year, that number is slated to be around $15 million. If this comes to fruition, it would take total annual savings since the start of what management calls Mission Critical to roughly $100 million or more.

In the event that we see some temporary weakness, investors can comfort themselves knowing that the enterprise Is still a small player in a massive market. According to management, the total addressable market for the industrial distribution space is worth around $215 billion. Management has successfully captured market share in this space over the years. In fact, this year alone, about 4% of the growth the company is expecting should relate to market capture. And with the aforementioned cost cuts, as well as benefits that the company should continue to achieve from general economies of scale, should help the company’s bottom line materially from here.

{kind=link}

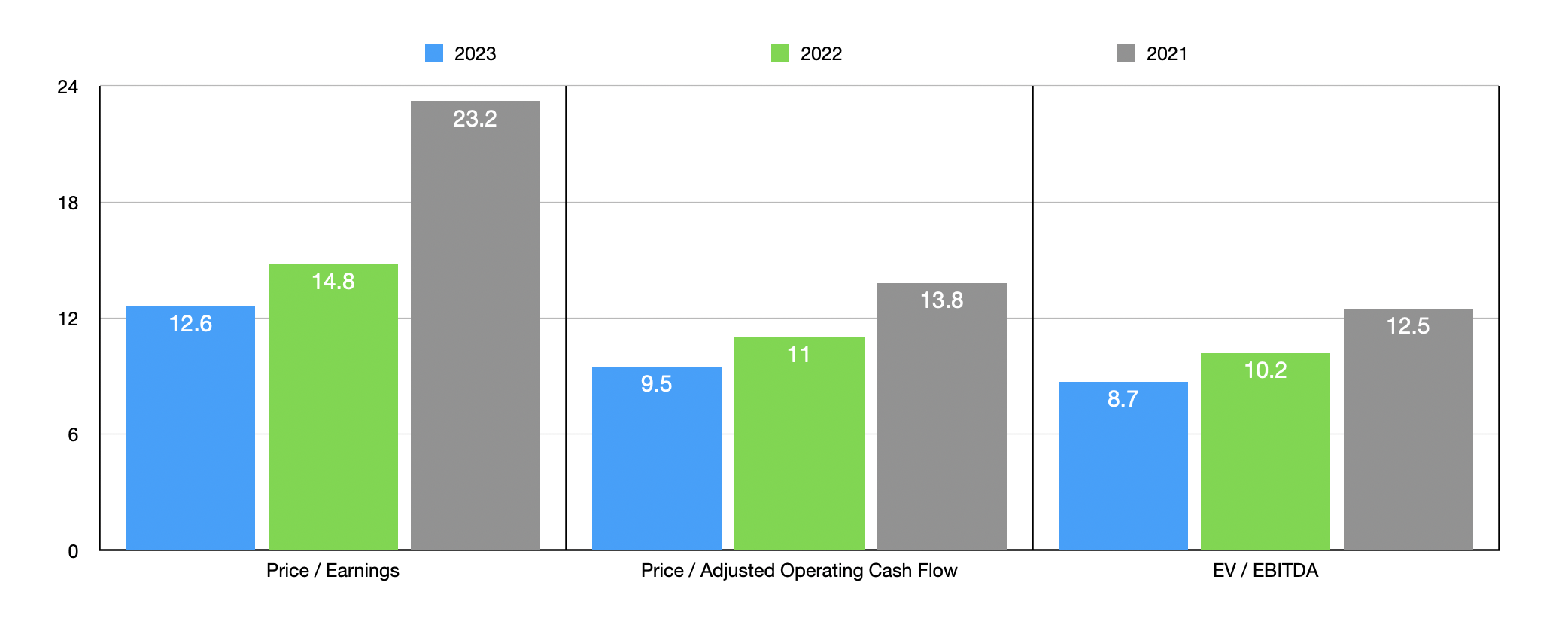

In the absence of more detailed guidance, I projected out what I believe financial results might look like for the rest of the fiscal year. For 2023 as a whole, I suspect that the company would generate net profits of around $401 million. Adjusted operating cash flow should be around $527.8 million, while EBITDA should come in at around $640.9 million. As you can see in the chart above, shares of the company are quite affordable on a forward basis. But even if we use data from 2021 or 2022, the picture doesn't look anywhere close to bad. This is not to say that the company is all around cheap. I did compare it with some similar enterprises in the table below. Using both the price to earnings approach and the EV to EBITDA approach to valuing the company, I found that four of the five competitors I compared it to were cheaper than it. Our prospect is only cheap on a relative basis if we use the price to operating cash flow multiple as our guide. In this case, only one of the five firms was cheaper than our prospect.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| MSC Industrial Direct |

| 12.6 |

| 9.5 |

| 8.7 |

| Applied Industrial Technologies ( AIT ) |

| 17.6 |

| 27.5 |

| 12.2 |

| Univar Solutions ( UNVR ) |

| 10.9 |

| 10.8 |

| 7.3 |

| Beacon Roofing Supply ( BECN ) |

| 10.8 |

| 10.3 |

| 7.0 |

| WESCO International ( WCC ) |

| 9.3 |

| 672.9 |

| 7.6 |

| BlueLinx Holdings ( BXC ) |

| 2.3 |

| 1.7 |

| 1.4 |

Takeaway

At this moment, I must say that I am impressed by how much shares of MSC Industrial Direct appreciated. When I last wrote about the business, I believed that the stock was undervalued materially. But I didn't expect it to rise so much and so quickly. The good news for investors is that, while shares may not be as cheap as they were, they do still look affordable on an absolute basis. Add on top of this management's continued dedication to cost cutting, as well as favorable industry conditions, and I do believe that the company warrants a soft ‘buy’ at this time.

For further details see:

MSC Industrial Direct: The Move Higher Isn't Over Yet