MTUAF - MTU Aero Engines: A Stock To Buy For The Long Term

2023-07-26 13:48:31 ET

Summary

- MTU Aero Engines' stock has underperformed compared to the S&P 500, despite posting strong financial results, due to a disclosed engine defect from Raytheon Technologies.

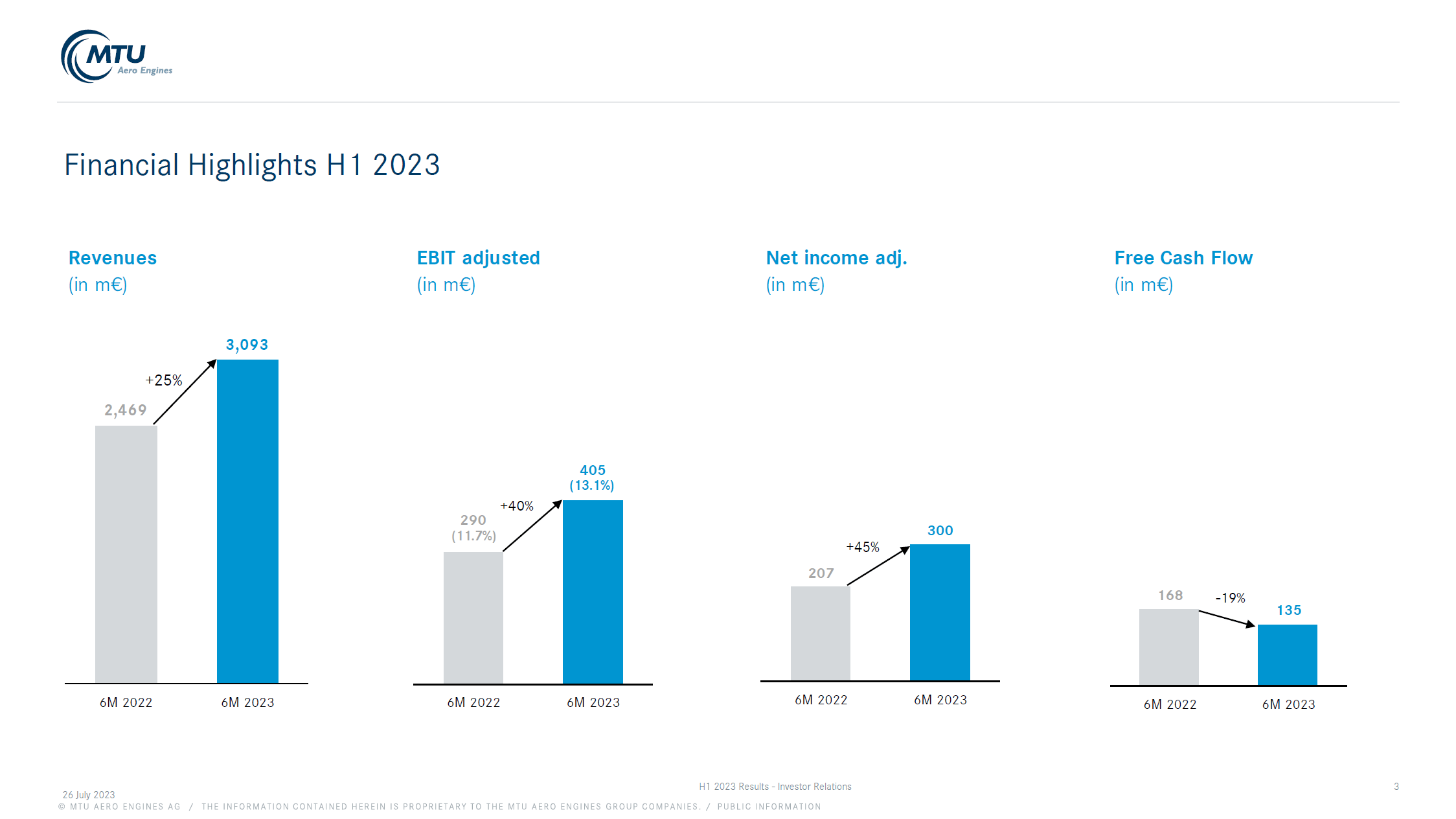

- For H1 2023, MTU Aero Engines' revenues grew 25% to €3.093 billion, with adjusted EBIT growing 40% to €405 million, but free cash flow declined from €168 million to €135 million.

- Despite issues with the Geared Turbofan (GTF), MTU Aero Engines maintains its guidance for 2023.

Earlier this year, I initiated coverage for MTU Aero Engines ( MTUAF ) with a strong buy rating. Despite posting strong financial results, the stock is up only 1.2% compared to the >18% return for the S&P 500. A major reason for that seems to be the disclosure from Raytheon Technologies ( RTX ), which disclosed an engine defect on its geared turbofan affecting resulting in around 200 early engine removals and led MTU Aero Engines stock more than 8% lower. Even without that stock price reduction, MTU Aero Engine stock underperformed the market, which I think is also related to somewhat weaker interest in European stocks in general. In this report, I will be discussing the most recent earnings and revisit the stock price target using the evoX Financial Analytics tool and change the rating if need be.

MTU Aero Engines Growth Tapers In Q2

{kind=link}

For H1 2023, the growth rates on all metrics except for the free cash flow moderated, indicating that year-over-year growth for Q2 was weaker than the growth observed in the prior quarter. This is related to flight activity ramping up last year, meaning that each quarter after Q1 2022 would give a more challenging comp in the subsequent year.

Revenues grew 25% to €3.093 billion with adjusted EBIT growing 40% €405 million on a 1.4 pts margin expansion. Net income grew 45% to €300 million and free cash flow declined from €168 million to €135 million, which is a 19% drop for H1 from a 31% drop in Q1. Operating cash flow declined by €11 million primarily driven by an increase in working capital related to supply chain disruptions while ongoing CapEx of €22 million on the PW Geared Turbofan platform further pressured the free cash flow compared to last year.

For the second quarter, we saw OEM commercial revenues grow by 21% and that is pretty much in line with the revenue growth observed in OEM Military and aftermarket sales. Margins for OEM ticked up by 3.1 pts to 23.6% and have the 25% target in sight while MRO margins dipped 1.3 pts due to higher GTF share in the MRO revenues. That is something to keep in mind, the GTF platform provides growth on top line but does provide some margin pressure.

For H1 2023, revenues grew by 40% in OEM Commercial, 7% in OEM Military and 22% in MRO. So, the second quarter growth rates do look significantly different from Q1 and H1, but this is also a comp effect and with a more challenging quarter to compare to it was in line of expectation that the growth rates would taper. Margins for OEM were 24.7% for H1 2023 marking a 3.3 pts expansion reflecting FX tailwinds, and lower costs related to the activities in Germany. The MRO segment had a 6.8% margin marking a 0.5 pts contraction reflecting a higher share of revenues that have a lower margin attached that has yet to mature.

MTU Aero Engines Maintains Updated Guidance For 2023

{kind=link}

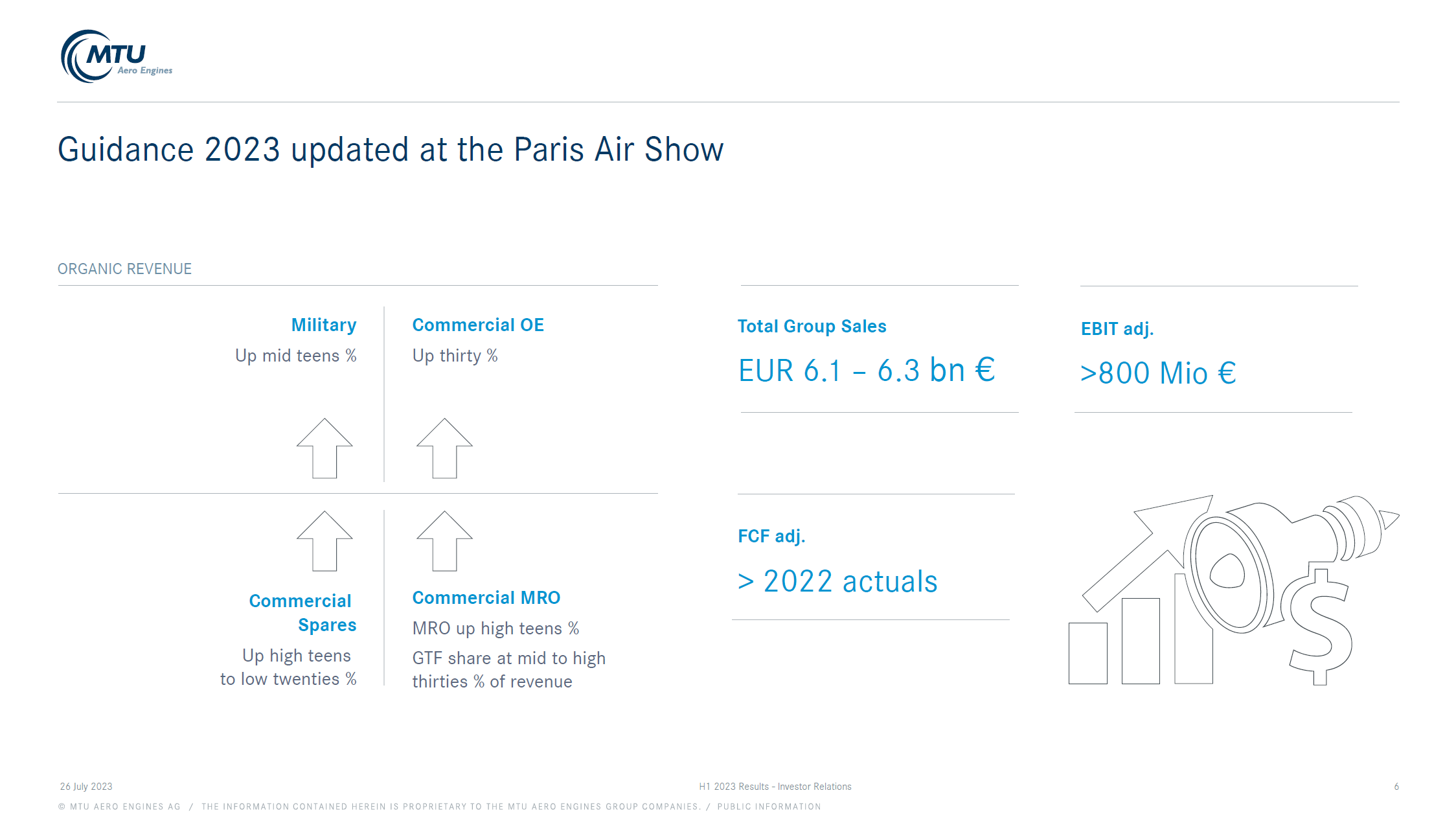

MTU Aero Engines updated its guidance during the Paris Airshow and despite the most recent issues with the GTF, the company has maintained that guidance. One reason is because the exact cost and timing of engine removals and impact, if any, on MTU Aero Engines is not known. Compared to Q1, the revenue guidance remained more or less the same with revenue guided in the €6.1 billion to €6.3 billion range despite the Military sales outlook being increased from up around 10 percent to a mid-teen percentage increase. The company has also provided guidance for a >€800 million adjusted EBIT which represents an EBIT margin of more than 12.5 to 13 percent, which is up slightly from the 12.3% last year and provides EBIT growth of at least 22% and is more or less in line with revenue growth outlook for MTU Aero Engines.

What Are The Risks For MTU Aero Engines?

The risk to MTU Aero Engine stock is what we have seen yesterday and that is the PW Geared Turbofan. Raytheon is progressing on getting those issues fixed, but we see that when one issue is being worked on, another one appears. Currently, any cost impact on MTU Aero Engines is not known, but the progress on solving the issues and increasing the durability of the geared turbofan is something to keep an eye on. Furthermore, it does seem that as a European supplier, there is less eye for MTU Aero Engines which could mean that its stock does not quite appreciate as much as desired but relative to peers that does also create an investing opportunity since an undervaluation for a company such as MTU Aero Engines should not be permanent.

What Is MTU Aero Engines Stock Worth?

{kind=link}

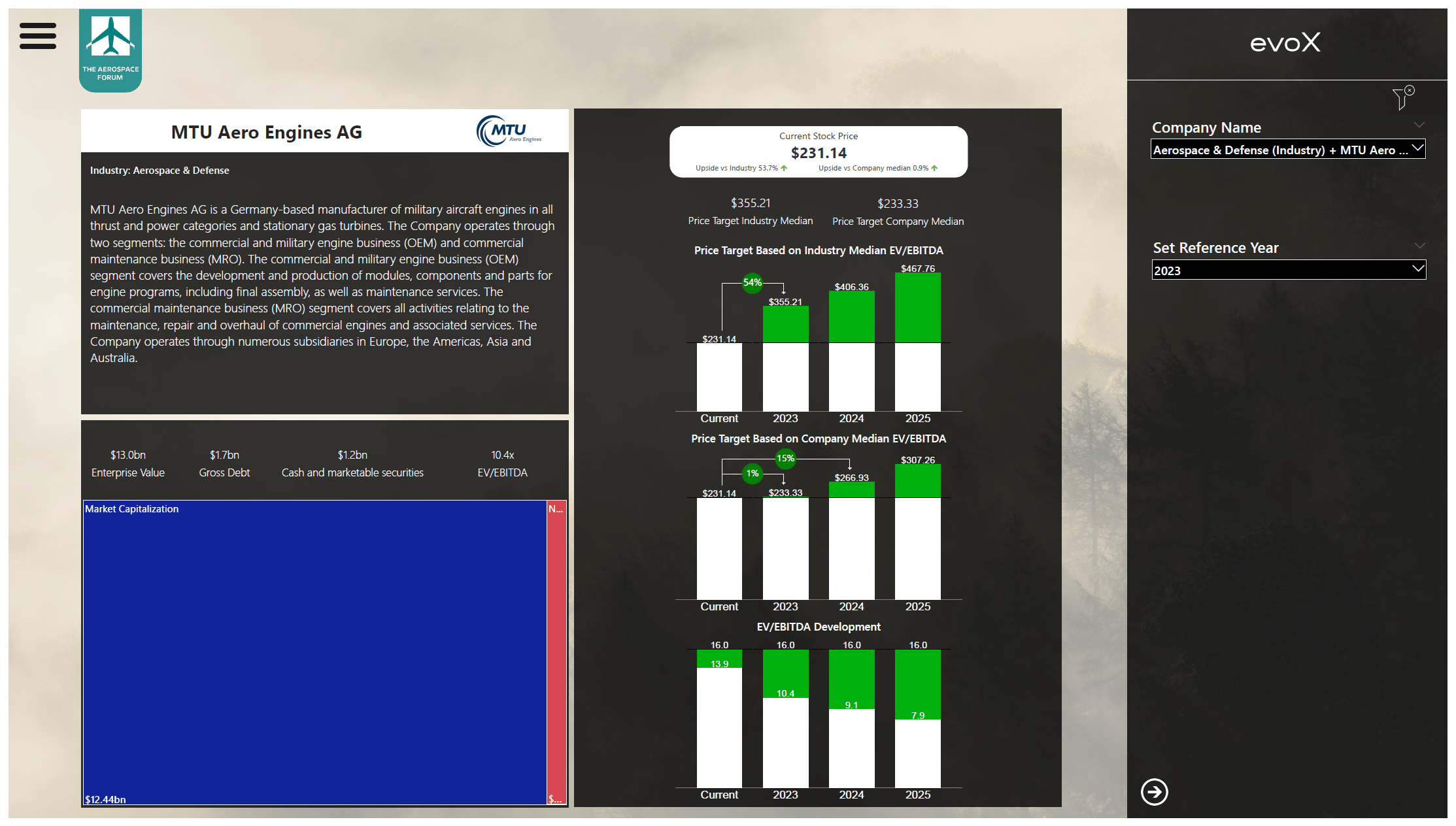

Valuing a stock can be challenging, not necessarily because of the fundamental information that I entered into the model but because we have to see what the typical multiples for a company are. Is the company typically trading in line with the industry or is there a big discrepancy that justifies expansion in the multiple or is the company typically trading it ahead of its earnings. For MTU Aero Engines, it seems to be the latter. Current year earnings are pretty much priced in and as time progresses, the market should start reflecting the 2024 earnings into the share price which I believe provides 15% upside to the stock.

Conclusion: MTU Aero Engines Remains A Long-Term Growth Opportunity

I previously had a strong buy rating on MTU Aero Engines and while the results really are quite good, I think a new assessment on the fundamentals and the expectations warrants a Buy rating instead. I continue to like the company with aftermarket exposure as well as OEM exposure and commercial and defense end markets. That is what I am looking for. Furthermore, over the longer term, there is some dividend growth to be expected but that is more a nice to have element since the dividend yield of 1.5% is far from juicy, So, this is more of a buy for the long-term in a long-term oriented market.

For further details see:

MTU Aero Engines: A Stock To Buy For The Long Term