CAAP - Munich Re Shines Fraport Stagnates K+S Drops: Reviewing My German Stocks After A Year

2023-07-24 12:04:07 ET

Summary

- It's time to review my investments in three German stocks: Munich Re, Fraport, and K+S.

- Munich Re performed exceptionally well, Fraport showed average performance, and K+S dropped by 30%.

- I discuss my expectations for these stocks for the rest of 2023 and beyond.

Back in May 2022, I decided to invest in three German stocks: reinsurer Munich Re ( OTCPK:MURGF , OTCPK:MURGY ), airport operator Fraport ( OTCPK:FPRUF , OTCPK:FPRUY ) and potash producer K+S ( OTCQX:KPLUF , OTCQX:KPLUY ). A year later, it's time for me to look back and assess the performance of these three stocks.

The three names had contrasting fortunes, with one stock doing tremendously well (Munich Re), another showing subdued performance (Fraport) and the third one, K+S, dropping 30%.

The chart above suggests that I would have been better off investing through the German ETF EWG , which returned 16% over the period, rather than my selection, which underperformed the tracker (12% return for an equal-weight blend of the three stocks). I am much more interested in stock-picking, though, and therefore I have no regrets. Let's now review the three stocks and determine whether they are worth holding for the year ahead.

Munich Re: Cream Rises To The Top

In H1 2022, there was a lot of negativity around the reinsurance industry, following years of major loss events and, of course, Covid-19. This turned out to be an excellent entry point in Munich Re, and while I saw this best-in-class reinsurer as primarily a reliable dividend payer, the share price appreciation has been spectacular.

For sure, 2022 had its fair share of major loss events, culminating with hurricane Ian in late September. However, Munich Re was able to navigate this environment and exceed its guidance for the year.

Going forward, further strong performance is expected - though major losses are of course unpredictable - given that recent reinsurance renewals have benefited from firming rates. In addition, a key source of profitability for (re)insurers, the investment return on their float, has been boosted by central bank policies in recent months after years of poor returns in a very low interest rate environment. Against this backdrop, the reinvestment rate for Munich Re rose to 4% as of April 2023.

As a result, earnings projections have been revised upwards for the company:

| 2023 est. |

| 2024 est. |

| 2025 est. |

| EBITDA (in million USD) |

| 7,004.52 USD |

| 7,179.58 USD |

| 7,302.99 USD |

| Net Income (in million USD) |

| 4,713.60 USD |

| 5,132.74 USD |

| 5,447.00 USD |

| Price/Earnings ratio |

| 10.72 |

| 9.60 |

| 9.00 |

| Dividend yield |

| 3.88 % |

| 4.10 % |

| 4.31 % |

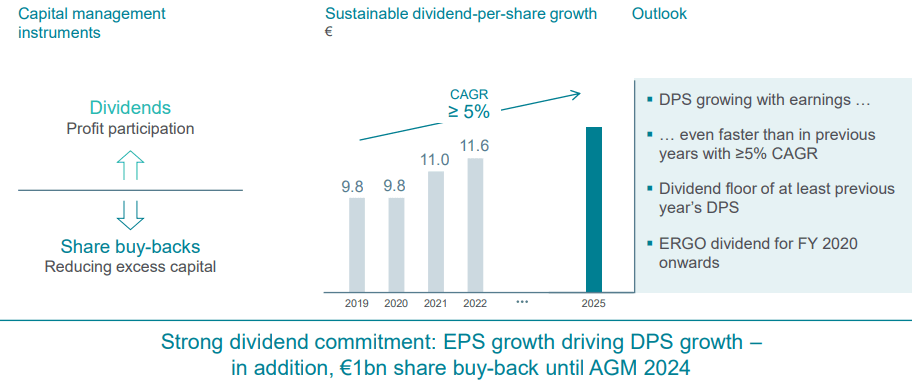

Of course, the share price appreciation makes the dividend yield less attractive, but I have no plan to sell the shares, which will remain part of the income portfolio. It's worth noting, too, that share buybacks are on the agenda to juice up shareholder returns:

{kind=link}

The potential for share price appreciation is, presumably, limited at this stage. However, the stock by no means ;looks overpriced, with a P/E ratio of 11 for 2023. For capital gains, I will rely on Paris-based SCOR SE ( OTCPK:SCRYY , OTCPK:SZCRF ), which seems to have turned the corner after a difficult couple of years.

Fraport: Good Prospects On Paper, But Uncertainty Remains

Fraport has been somewhat frustrating for me, due to the opportunity cost of holding a stock whose price has barely increased since May 2022. I've been an airport bull for years, for reasons that I explained in this article presenting the various listed airports globally: Investing In Airports: A World Of Opportunities .

The problem is that Fraport's main asset, the airport of Frankfurt, may not benefit much from the secular tailwinds that underpin passenger traffic growth worldwide. With an increasing number of Europeans concerned about the climate impact of the industry, and the renewed push for high-speed rail, growth should be slower than was assumed a few years back for Frankfurt. In fact, the airport has not yet recovered from Covid-19 traffic-wise (in Q1 it reached about 80% of its 2019 passenger traffic) - strikes have not helped either.

The reason why I remain invested is the portfolio of international airports that Fraport Group operates. Peru (Lima airport, where Fraport just finished a new runway) and Brazil are growth avenues for sure, while Greece has enjoyed great success. The joint venture for Antalya in Turkey also has potential. However, it could take several years before the international airports make a meaningful contribution to net result.

{kind=link}

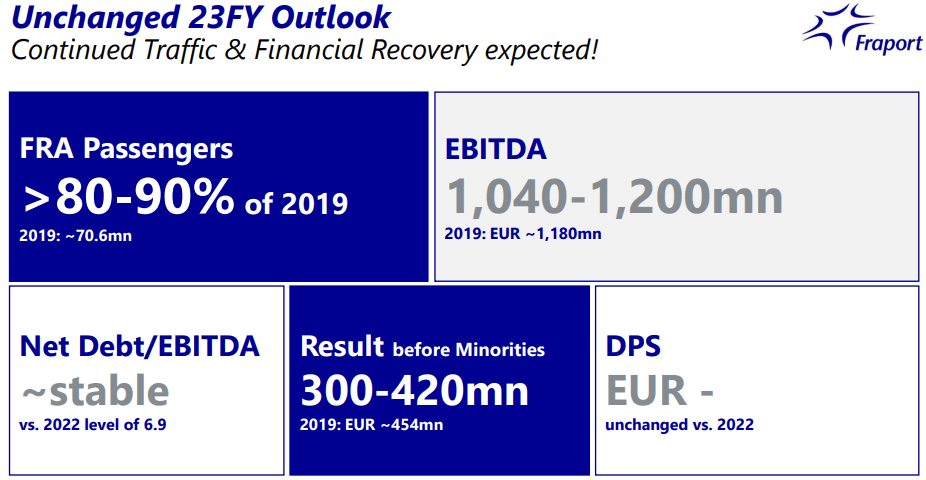

The company confirmed its outlook for 2023, which points to a financial performance close to that of 2019 (with cost management offsetting lower traffic in Frankfurt).

{kind=link}

On that basis, and assuming that the recovery continues beyond that, the stock is not expensive for an infrastructure play with no time limit on its main asset (Frankfurt airport is a freehold, not a concession).

| 2023 est. |

| 2024 est. |

| 2025 est. |

| EBITDA (in million EUR) |

| 1,153.84 |

| 1,327.13 |

| 1,430.84 |

| Net Income (in million EUR) |

| 324.62 |

| 422.01 |

| 480.63 |

| Price/Earnings ratio |

| 14.05 |

| 10.85 |

| 9.50 |

| Dividend yield |

| 0 % |

| 2.07 % |

| 2.34 % |

Source: Finanzen.net

To conclude, I am not really enthusiastic about Fraport, but there are some positives and I will probably hold the stock for another year, and see from there. However, if I were looking for a fast-growing airport operator, and didn't already have a sizable position in Corporacion America Airports ( CAAP ), I would probably trade my Fraport shares for CAAP ones.

K+S: Potash Market Weakness Takes A Toll

The performance of my investment in K+S AG has been poor to say the least, with the stock declining by a third since I bought it. My timing was not good: I bought on the first dip after the sharp rise triggered by the war in Ukraine (seen as a catalyst for non-Russian/Belarussian fertilizer producers).

Fertilizers, like most commodities, are cyclical, and the cycles can be very short. Potash prices have dropped sharply over the past six months, for several reasons. While fertilizers are important to crop yields, their application can be delayed or reduced when prices are too high - in fact, the price sensitivity should not be underestimated in this field (pardon the pun).

Another factor that may have been underestimated is the speed at which Russia (and possibly Belarus) were able to redirect more of their exports to China, weighing on global prices. In fact, though K+S itself does not ship much to China, the disappointing price of the new Canpotex-China contract will have a severe impact on the German company's revenue:

On June 6, 2023, Canpotex (export organization of the North American competitors Nutrien and Mosaic) publicly announced the conclusion of a contract with Chinese customers for the supply of potassium chloride until the end of the year at a price of USD 307 per tonne [...] In case that the Chinese potassium chloride price radiates accordingly into the other markets and there is no price recovery in these markets from the levels then reached until the end of 2023, this would result in total EBITDA of about EUR 0.8 billion for K+S in 2023.

Source: K+S AG's press release , author's emphasis

Analysts have obviously revised their estimates downward. It's worth noting that K+S delivered an EBITDA of €453M in Q1 '23. The fact that yearly EBITDA is expected to be only in the €800-€850M bracket shows the extent of the weak market conditions for the rest of 2023.

| 2023 est. |

| 2024 est. |

| 2025 est. |

| EBITDA (in million EUR) |

| 856.38 EUR |

| 766.00 EUR |

| 732.05 EUR |

| Net Income (in million EUR) |

| 287,03 EUR |

| 222.04 EUR |

| 191.68 EUR |

| Price/Earnings ratio |

| 11.93 |

| 14.51 |

| 16.74 |

| Dividend yield |

| 4.71 % |

| 3.03 % |

| 2.35 % |

Source: Finanzen.net

For comparison purposes, let me show the table as it stood a year ago:

| Old estimates from May 2022 |

| 2023 est. |

| 2024 est. |

| EBITDA (in million EUR) |

| 1,928.08 EUR |

| 1,208.77 EUR |

| Net Income (in million EUR) |

| 1,110.81 EUR |

| 541.74 EUR |

| Price/Earnings ratio |

| 5.04 |

| 10.04 |

| Dividend yield |

| 3.69 % |

| 2.60 % |

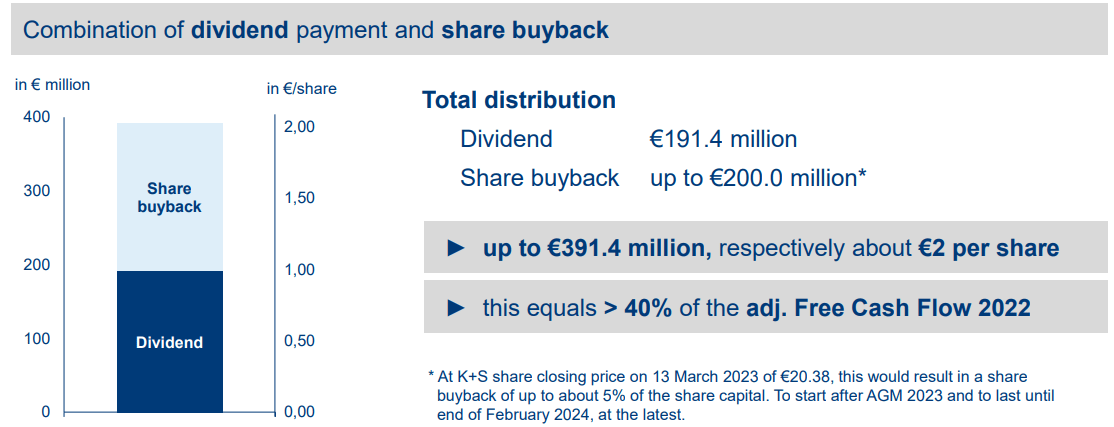

These metrics, for sure, make the stock less attractive, despite K+S' commitment to boost shareholder returns through buybacks:

{kind=link}

Despite the weaker results, I have no intention of selling the stock as I want to keep exposure to this vital industry, across all continents, and K+S is the only investable European potash producer. However, I will not add to my current position, and, instead, I've been buying shares of Israel Chemicals ( ICL ). ICL has a logistical advantage when serving key potash markets in India and South-East Asia, and is also a leading producer of phosphate and bromine.

For further details see:

Munich Re Shines, Fraport Stagnates, K+S Drops: Reviewing My German Stocks After A Year