FMB - Municipal Bond Outlook: We Think Positive Performance Will Continue

2023-08-30 02:00:00 ET

Summary

- Investors who are waiting for a change in Fed policy may miss a rare opportunity, especially in longer maturity municipal bonds.

- After unusually negative performance in 2022, we’ve seen a welcome bounce back in the municipal bond market.

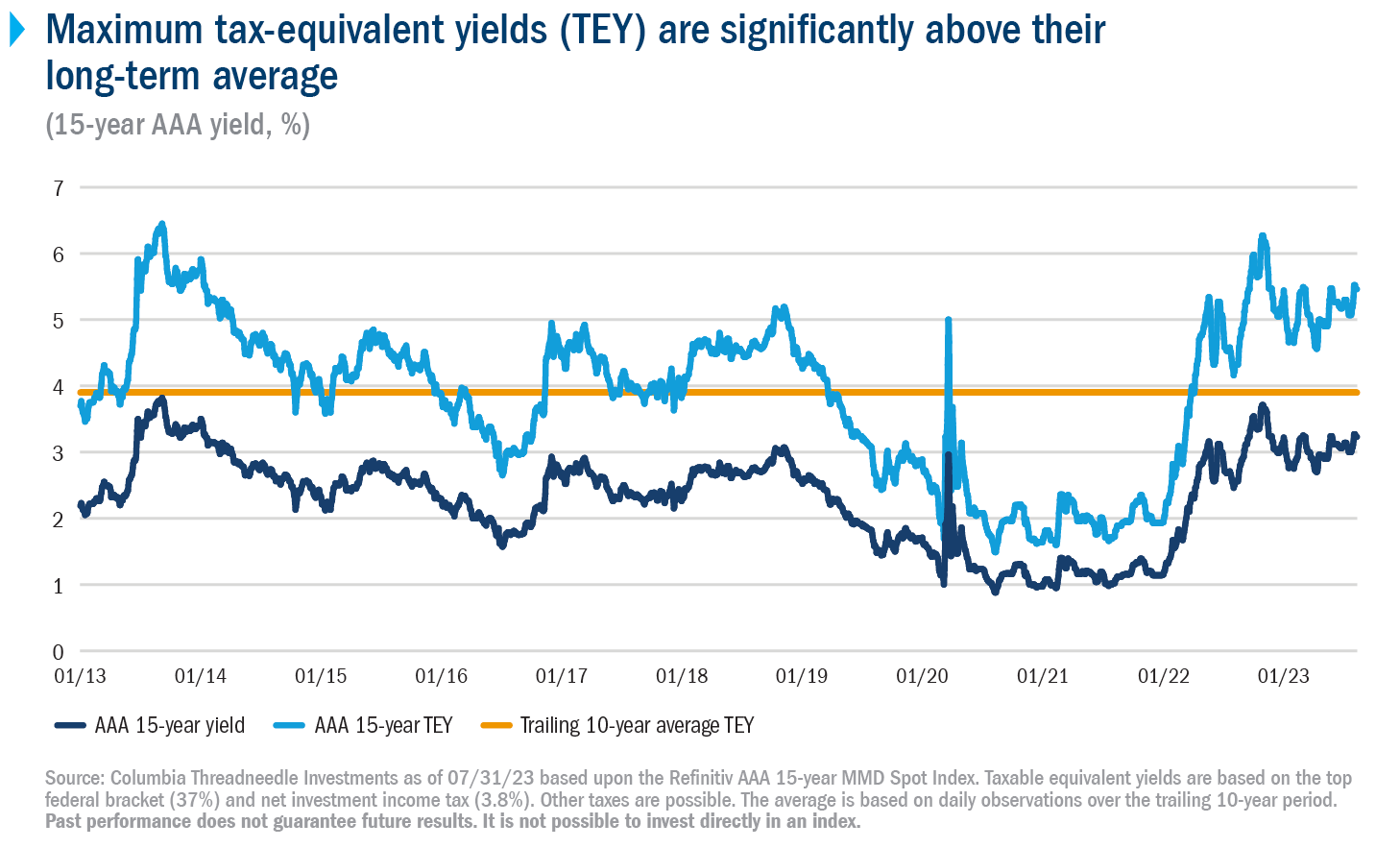

- Municipal bond yields have risen dramatically since their recent lows and now sit above 3.5%.

By Catherine Stienstra, Head of Municipal Bond Investments

Investors who are waiting for a change in Fed policy may miss a rare opportunity, especially in longer maturity municipal bonds.

After unusually negative performance in 2022, we’ve seen a welcome bounce back in the municipal bond market. Investors - especially those who are waiting for a change in Fed policy - may be missing out. However, here’s why we think investors should start allocating to municipal bonds now.

Tax-equivalent yields offer an exceptional income opportunity

Municipal bond yields have risen dramatically since their recent lows and now sit above 3.5%. 1

But while high absolute yields on high-quality assets like municipal bonds are compelling, the real story is tax-equivalent yields, which started the year at unprecedented levels and have become more compelling.

Right now, investors in tax-free municipal bonds can get attractive taxable equivalent yields. 2

{kind=link}

These current higher yields offer investors an opportunity to lock in income, especially in longer maturity bonds, that may not be on the table if and when the Fed ends its tightening cycle and rates start to fall.

Muni yields are essentially in the same place as when the year began, so investors have not missed out on the attractive opportunity.

Fundamentals and technicals are favorable and resilient

Overall, underlying creditworthiness in the municipal market is strong and stable. Against continued economic uncertainty and the possibility of a recession, state government rainy day funds are at a record high.

Municipal credit upgrades are still well outpacing downgrades, which reflects sustained budget surpluses set aside for a potential economic downturn.

A favorable technical environment has also been beneficial this year, and we expect that to continue.

The supply/demand imbalance we started the year with remains — issuers that are flush with cash are being patient, waiting for lower rates to either refund or issue new debt.

This relative supply scarcity in the primary market continues to support the market and benefit investors.

Municipal bonds are poised to outperform

While volatility has continued in the rates market, municipals have proven resilient, and year-to-date the Bloomberg Municipal Bond Index has outperformed both the Bloomberg Treasury Bond Index and the Bloomberg Aggregate Bond Index.

Since the low of October 26, 2022, the Bloomberg Municipal Bond Index has rallied 8.41% (as of July 31) with lower investment grade, high yield and longer duration outperforming due to income being the main driver of returns. With the positively sloped yield curve from 10-30 years, this gives us a strong conviction for longer duration with the higher income component.

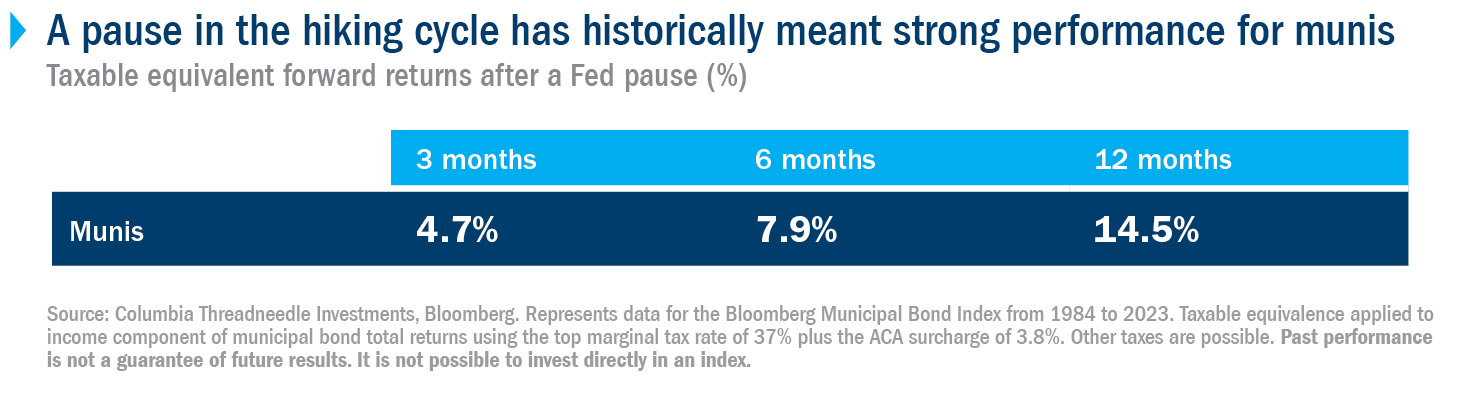

We don’t need to see Fed rate cuts for a rally from here, as higher yields should support performance.

Investors who want to capture the full cycle of stronger performance may want to consider investing now or building a position over time, incrementally adding to their bond allocation before (and then while) rates fall rather than waiting for an all clear on tightening from the Fed.

For now, investors may have the opportunity to purchase bonds at attractive yields before the path of declining rates is priced in.

{kind=link}

Opportunities in the long end of the curve, especially among high-quality issuers

While opportunities currently exist on both ends of the muni bond curve, the real value is on the longer end, where we see a robust opportunity in high-quality municipal bonds with maturities of 10 years or more, both for their healthy yields and potential for price appreciation if the rate environment turns.

Quality in this case means not only AAA or AA rated general obligation bonds, but also higher quality issuers within certain sectors. If the economy tips toward recession, investors moving out of equities may turn to municipal bonds, especially longer durations, as they seek a high-quality, less recession-sensitive alternative to stocks.

In such an environment, sourcing attractive bonds could become even more difficult than it is now.

This year, we’ve also seen higher-than-usual rates at the short end of the curve while the municipal yield curve has been inverted - a highly unusual and likely temporary situation driven by the Fed’s persistent and aggressive tightening.

While there are income opportunities to take advantage of in shorter-term investments, the attractiveness will fall as the Fed gets closer to rate cuts.

The bottom line

Historic tax-equivalent yields alone are a good enough reason to consider allocating into municipal bonds. Doing it in the current yield environment also allows investors to pursue a longer-term buffer against the potential for falling interest rates or the impacts of a recession.

1 S&P Municipal Bond Index Yield to Worst as of 07/31/23

2 Based on the Bloomberg Municipal Bond Index and the Bloomberg U.S. Treasury Index yields as of 07/31/23

Disclosures

Investing involves risk including the risk of loss of principal. Bonds involve credit risk and bond prices decrease when rates rise. Income from tax-exempt municipal bonds or municipal bond funds may be subject to state and local taxes, and a portion of income may be subject to the federal and/or state alternative minimum tax for certain investors. Federal and state income tax rules will apply to any capital gains.

© 2016-2023 Columbia Management Investment Advisers, LLC. All rights reserved.

Use of products, materials and services available through Columbia Threadneedle Investments may be subject to approval by your home office.

With respect to mutual funds, ETFs and Tri-Continental Corporation, investors should consider the investment objectives, risks, charges and expenses of a fund carefully before investing. To learn more about this and other important information about each fund, download a free prospectus . The prospectus should be read carefully before investing. Investors should consider the investment objectives, risks, charges, and expenses of Columbia Seligman Premium Technology Growth Fund carefully before investing. To obtain the Fund's most recent periodic reports and other regulatory filings, contact your financial advisor or download reports here . These reports and other filings can also be found on the Securities and Exchange Commission's EDGAR Database. You should read these reports and other filings carefully before investing.

The views expressed are as of the date given, may change as market or other conditions change and may differ from views expressed by other Columbia Management Investment Advisers, LLC ((CMIA)) associates or affiliates. Actual investments or investment decisions made by CMIA and its affiliates, whether for its own account or on behalf of clients, may not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not take into consideration individual investor circumstances. Investment decisions should always be made based on an investor's specific financial needs, objectives, goals, time horizon and risk tolerance. Asset classes described may not be appropriate for all investors. Past performance does not guarantee future results, and no forecast should be considered a guarantee either. Since economic and market conditions change frequently, there can be no assurance that the trends described here will continue or that any forecasts are accurate.

Columbia Funds and Columbia Acorn Funds are distributed by Columbia Management Investment Distributors, Inc., member FINRA . Columbia Funds are managed by Columbia Management Investment Advisers, LLC and Columbia Acorn Funds are managed by Columbia Wanger Asset Management, LLC, a subsidiary of Columbia Management Investment Advisers, LLC. ETFs are distributed by ALPS Distributors, Inc., member FINRA , an unaffiliated entity.

Columbia Threadneedle Investments (Columbia Threadneedle) is the global brand name of the Columbia and Threadneedle group of companies.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Municipal Bond Outlook: We Think Positive Performance Will Continue