EVN - Municipal CEF Sector Update: 2023 Fed Pause Offers A Good Entry Point

Summary

- The Municipal bond sector has taken a hit this year on the back of high and sticky inflation and the Fed's attempt to bring it to heel.

- We discuss the key themes driving the sector and why the upcoming Fed pause may offer an attractive entry point.

- We also highlight a number of funds worth a look.

This article was first released to Systematic Income subscribers and free trials on Oct. 26.

Municipal yields have risen to attractive levels with the broader sector trading north of 4% while longer-dated Munis are trading around 5% and High-Yield Munis trading well north of 6% yields. In this article, we discuss the key themes driving the tax-exempt Municipal bond sector and why the upcoming Fed pause may offer an attractive entry point for the sector.

The Current Macro Backdrop

This entire year, the focus of the market has been on high and sticky inflation and the Fed's belated and rushed attempt to bring it under control. This has caused bond yields to move sharply higher, pushing down prices of long-duration assets like Municipal bonds.

One important aspect of investing is to make sure not to extrapolate current trends forever. While inflation remains high, it is no longer rising. In fact, most price indicators are reversing be it supply chains, used car prices, commodities etc. Large and lagging components like housing-related inflation will be sticky from the simple mechanics of how they are constructed but because the housing market has clearly crested, it is just a matter of time before even they reverse as well. For what it's worth, most analysts crunching the numbers are expecting inflation to be cut in half - closer to a 3-4% run rate in about a year's time.

This means that the Fed's current 75bp series of hikes is unlikely to last much longer. In fact, the Fed has just begun to finally pivot from its "Infinity and beyond!" stance. James Bullard just came out with "In 2023 I think we’ll be closer to the point where we can run what I would call ordinary monetary policy" and this with only two more full months to go in 2022.

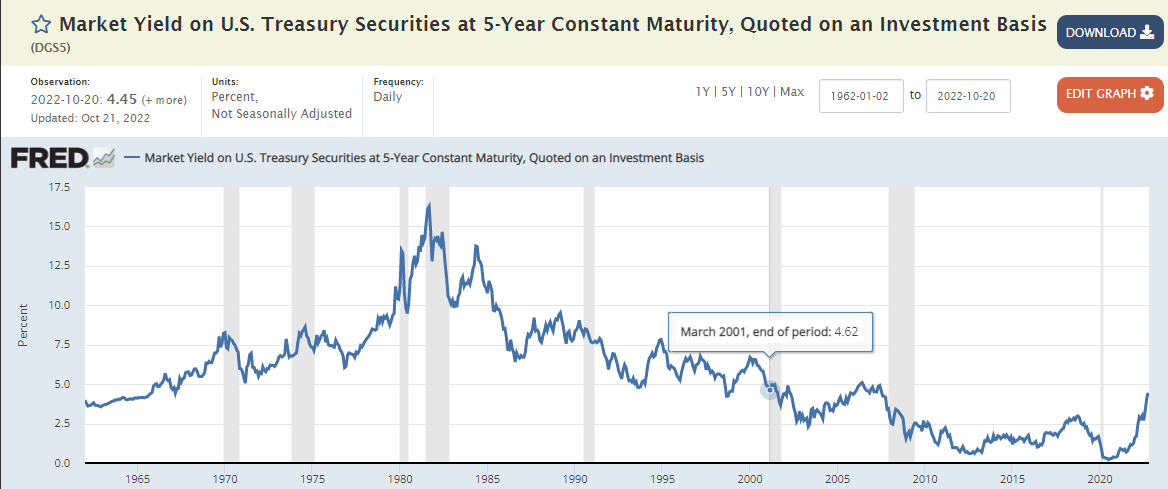

However, the market has continued to push rates higher recently, partly on the back of the mess having to do with the UK bond fallout and partly due to technical factors like QT. As the chart shows below, the last time the 5Y Treasury yield was convincingly higher was prior to the Tech recession.

{kind=link}

This set-up of moderating inflation and moderating Fed suggests that while income investors have been well advised to seek out shorter-duration / floating-rate securities, they should soon start to consider putting new capital to work in longer-duration securities and this includes Munis.

This is particularly the case if the eventual Fed pause and continued disinflation is accompanied by a recession. The combination of all three drivers, which is increasingly becoming the consensus, is likely to lead to a stabilization and a potential fall in longer-term yields. Outside of the very unusual 2020 recession, the previous two recessions saw positive returns in the Muni sector.

BOA

Review Of Key Themes

In this section we discuss some of the key themes driving the sector.

The first key theme driving the performance of Municipal funds, which won't come as a surprise to anyone, is their long duration . However, one element which may be surprising is the tilt of municipal CEFs themselves.

Specifically, if we look at the total return of income sectors this year, we see that Munis have outperformed most other income sectors such as High-Yield corporate bonds.

Systematic Income

However, when we look at sector performance across CEFs we get a very different picture - Muni CEFs have underperformed most other income sectors, including High Yield corporate bonds in total NAV terms.

Systematic Income

The reason for this is that Muni CEFs tend to tilt toward longer-duration bonds, which makes them more sensitive to a back-up in interest rates than the broader Municipal sector itself. A big part of the reason for this is that the Municipal yield curve is upward sloping and longer-dated bonds are more attractive to active managers because of their higher yields. However, as we have just seen, this comes at their increased sensitivity to changes in rates.

The second interesting theme this year, which we also see across other fixed-income sectors, is the rise in leverage costs . Municipal bonds rely almost exclusively on floating-rate leverage instruments such as tender option bonds and variable rate preferreds. This means their leverage costs have risen sharply this year and remain an income headwind for leveraged CEFs.

Systematic Income

The third theme is that most Muni CEFs have seen an increase in leverage this year. This is because most funds have not deleveraged as much as their portfolios have fallen in value. Many funds started the year with relatively modest leverage levels of 30-35% and are now trading at levels of 40-45%. All else equal, CEFs like to avoid a forced deleveraging because it can lock in economic losses for the fund and lower the amount of income it generates.

Systematic Income

Clearly, not all funds have been able to avoid a sharp deleveraging. PIMCO Muni CEFs, for instance, had a sizable deleveraging in July because of their high starting leverage levels.

Systematic Income

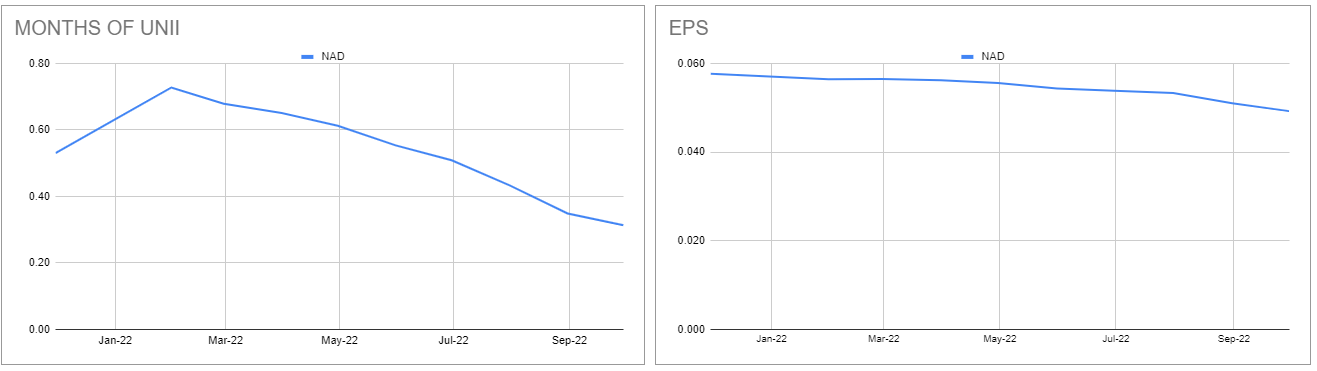

The increase in leverage costs, the flattening of the Muni yield curve and broadbased deleveraging across the sector means Muni income levels have been on a downtrend this year. The chart below shows both the monthly net income and UNII levels for NAD. Investors who strictly look at distribution coverage may get the wrong picture because many funds have cut distributions this year, pushing coverage higher.

{kind=link}

Which brings us to distribution cuts . Overall, the sector has cut distributions by around 12%, as shown below in the extract from our CEF Tool, as a result of some of the themes highlighted above.

Systematic Income CEF Tool

The volatility in the sector and distribution cuts have pushed the Municipal sector discount to very wide levels, as the following chart shows. The sector discount has been wider this century but, outside of the GFC, only for brief periods.

Systematic Income

The sector also looks attractively valued relative to other CEF sectors - it has a wider average discount and a much lower discount percentile along with other metrics.

Systematic Income CEF Tool

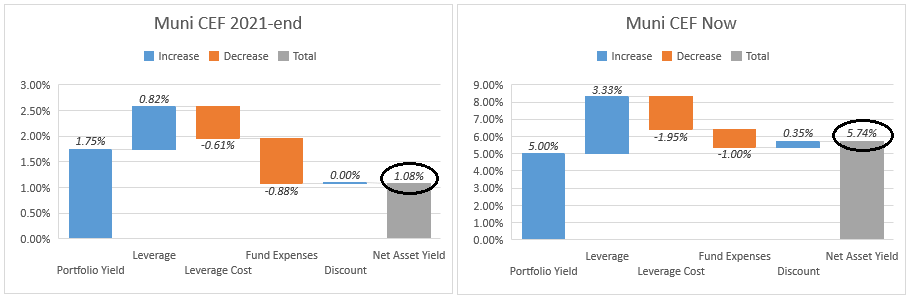

Despite some deleveraging and a rise in leverage costs, the sector is generating much more attractive yields than we saw at the end of last year. A yield disaggregation chart for a generic Muni CEF at the end of 2021 vs. now is shown below.

{kind=link}

Municipal bonds also look attractive on valuation grounds themselves. As the table below shows, credit spreads are not far off their wides this year. This stands in contrast to the corporate bond sector, where high-yield corporate bond spreads are more than 1% below their 6% peak this year.

BOA

Finally, the back-up in yields means many Municipal bonds have moved to trade much closer to par. This makes it much easier for investors to understand what is going on.

BOA

Many investors were looking at Muni CEFs in 2021, convinced that they were truly "earning" 4-5% yields. However, as we have repeatedly pointed out, this was incorrect. Investors were looking at current yields (grey bars) and interpreting them as "yields-to-maturity / yields-to-worst". At prices of $115-120 there is a massive gap between the two. At par, there is no gap between the two. With many bonds trading close to par, what you see via distribution rates is what you get in the sector and CEFs really are earning yields close to their distribution rates.

Systematic Income

Stance And Takeaways

We continue to see value in Municipal bonds given elevated yields and credit spreads, particularly in an environment where the Fed has begun to hint at a pause over the next few months. It may seem counter-intuitive to want to hold long-duration assets in the current environment. However, they are likely to outperform in a typical recession when credit spreads rise and Treasury yields fall.

The key question for investors is whether to hold Municipal bond exposure via CEFs or OEFs. Both structures offer pros and cons right now. CEFs are trading at unusually wide discounts, however, high leverage costs limit the amount of income generated by the leveraged portion of the fund.

CEFs will appeal to more tactical investors who expect medium-term capital gains from the sector from falling Treasury yields and/or falling credit spreads as well as eventually lower short-term rates. On the other hand, OEFs will appeal to investors more concerned with potential downside from high leverage levels of CEFs and discount widening.

Here we highlight a number of funds we continue to find attractive.

The Nuveen Short Duration High Yield Municipal Bond Fund ( NVHAX ) is trading at a 3.7% current yield. The fund's yield is likely understated given the fact that shorter-duration high-yield municipal bonds have a similar yield as longer-maturity bonds as shown below. The fund has delivered a total return this year of -10.3% or about half of the drop of the broader Muni sector and is attractive for investors worried about further rises in yields.

Nuveen

The Nuveen Intermediate Duration Quality Municipal Term Fund ( NIQ ) is worth a look for investors looking to hedge against further discount widening in the sector. The fund has a term structure with a June-2023 expected termination date. It will hold a tender offer at NAV in the first half of 2023 and currently trades at a 3.4% discount meaning the entire 3.4% is alpha on top of its 3% current yield.

The MainStay MacKay Defined Term Municipal Opportunities Fund ( MMD ) has generated superior results in both absolute and risk-adjusted terms. It has also outperformed this year in total NAV and total price terms. The fund trades at a 6.6% current yield and a 2.3% discount.

The Eaton Vance Municipal Income Trust ( EVN ) offers a more generic tax-exempt Muni exposure. It has outperformed the sector historically in total NAV terms. The fund trades at a 5.2% current yield and a 10.6% discount.

For further details see:

Municipal CEF Sector Update: 2023 Fed Pause Offers A Good Entry Point