BTT - Municipal CEF Update: Valuation In The Sweet Spot

2023-07-25 08:31:38 ET

Summary

- In this article, we take a fresh look at the tax-exempt Municipal CEF sector.

- Both Muni CEF discounts and yields are near their decade-high level, making the sector valuation attractive.

- We highlight a number of tailwinds and our picks.

In our last Muni update in Q1 we were fairly upbeat about the sector. And despite a number of wobbles in broader markets, Muni CEF performance was pretty good over Q1, delivering a total NAV return of around 3%.

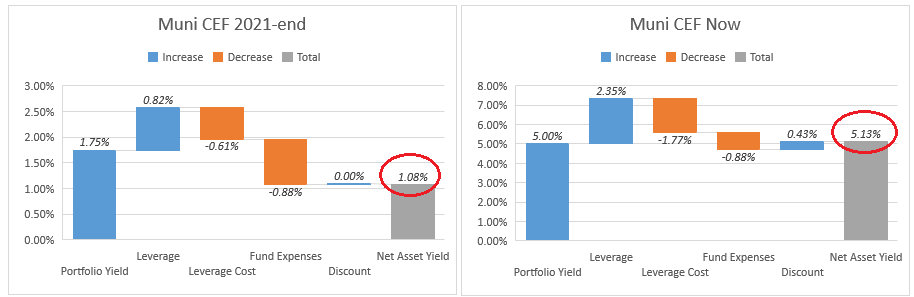

Overall, we continue to like Munis here, particularly via CEF exposure. It's important to keep in mind that despite the sharp rise in leverage costs, Muni CEF yields today are miles above their level at the end of 2021. For instance, today Muni CEFs can deliver portfolio yields north of 5% while in 2021 they could barely scrape together 1%.

{kind=link}

Income investor behavior is often very puzzling. In 2021 investors couldn't get enough of Munis even though bond yields were extremely low. And now that yields are north of 5% (and higher on high-yield Muni bonds and CEFs), the sector has fallen from favor, trading at unusually wide discounts.

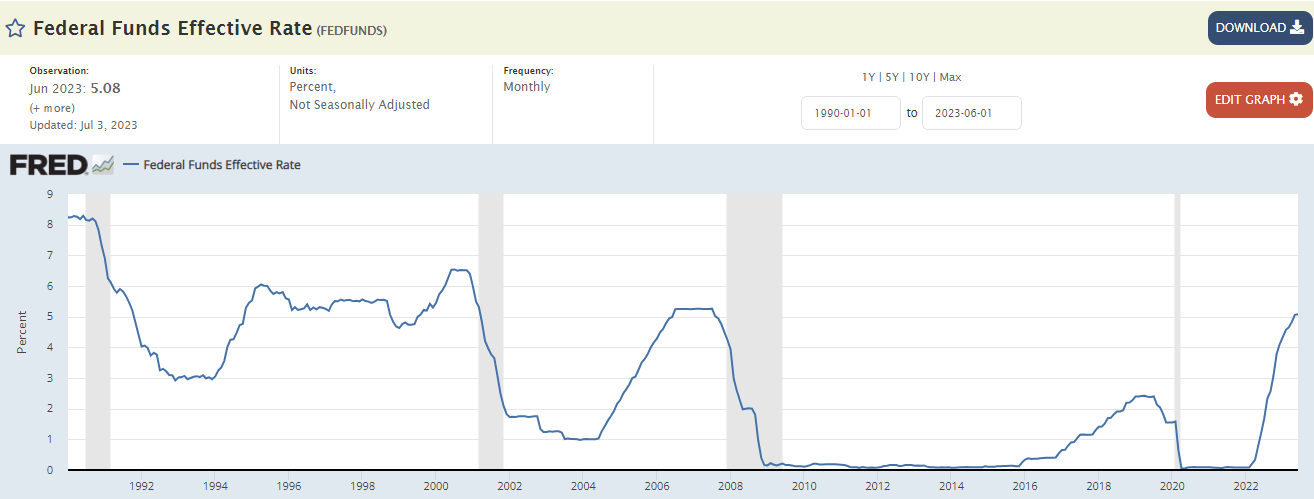

Apart from attractive yields, Munis also stand to benefit from a potential fall in interest rates across the yield curve. It's extremely unlikely that the Fed policy rate does not move below today's level over the next few years.

Not only is the Fed intent on pushing inflation back down to 2% even if it means a recession, the structure of the US economy is very unlikely to be able to support a 5-6% Fed Funds rate for an indefinite future as the following chart suggests.

{kind=link}

This means that the rise in leverage costs since 2022 will very likely partly reverse in the medium term. It could also lead to capital gains if Muni yields fall from today's high levels. This double-barreled benefit from lower rates is one that investors should keep in mind for the sector.

Finally, Muni CEF discounts remain unusually wide. As we touched on above, this is explained by the fact that many income investors approach bond allocation from a price momentum perspective. Higher prices create more demand and vice-versa. This dynamic is a benefit to investors who, instead, allocate on the basis of yield and who, like us, find Munis much more attractive assets today than they did in 2021.

Systematic Income

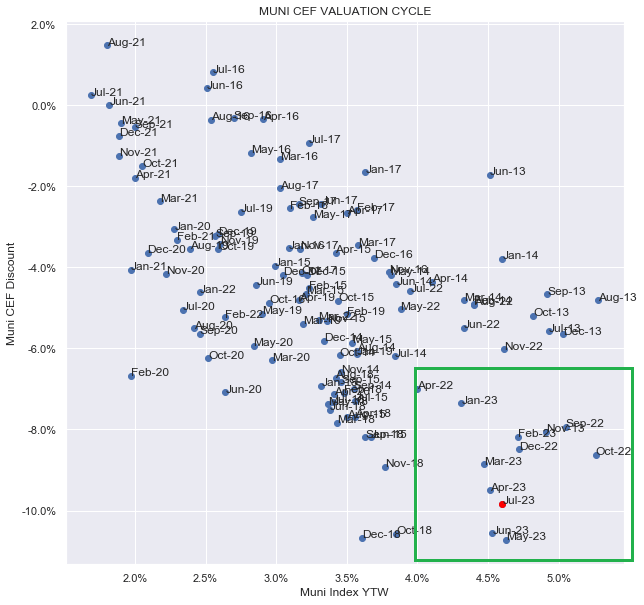

Overall, the market environment for Muni CEF allocation remains favorable. The chart below shows the two key dimensions of Muni CEF valuations: discounts (y-axis) and underlying bond yields (x-axis). We are currently in the bottom-right quadrant (current value is marked by red dot) which highlights that both discounts and underlying yields are historically attractive.

{kind=link}

Key Themes

In this section we highlight some of the key themes of the tax-exempt Muni sector.

Yields remain at decade-high levels across both high-yield and investment-grade Munis.

Systematic Income

The tax-exempt yield curve is still upward sloping (i.e. shorter-term rates are below longer-term rates). This means Muni CEF net income is not hurt as much as net income of taxable bond funds from high leverage costs.

BOA

Muni issuance has been fairly tepid this year.

UBS

This, plus outflows since 2022 set up a favorable supply/demand dynamic for the sector.

BOA

The economy has remained more robust than many have predicted. A positive feedback loop of companies keeping workers for fear of losing them (as many did in 2020) and workers enjoying a solid employment situation and continuing to spend is supporting the economy and markets.

This suggests that the Fed will likely have to push the economy into recession in order to cool the labor market. This, in turn, is likely to lead to lower interest rates across the yield curve and support Municipal bonds.

Some Ideas

We continue to focus on funds that have outperformed the sector and trade at wide discounts such as the funds in the bottom-right quadrant of the chart below.

Systematic Income

Within the CEF sleeve, we continue to hold the following funds in our Muni Income Portfolio:

- BlackRock Municipal 2030 Target Term Trust ( BTT ), trading at a 3.2% yield and a 10.7% discount. The fund has a term structure which provides asymmetric upside in case of termination.

- Nuveen Municipal Credit Income Fund ( NZF ), trading at a 4.5% yield and a 14% discount. NZF has a higher-yield profile due to its larger than average unrated and sub-investment-grade allocation.

-

Nuveen Quality Municipal Income Fund ( NAD ), trading at a 4.1% yield and a 14% discount. NAD is a fairly typical high-quality Muni CEF.

Municipal bonds have been out of favor, however, high underlying yields, attractive discounts and potential changes in interest rates make Muni CEFs compelling holds in the current environment.

For further details see:

Municipal CEF Update: Valuation In The Sweet Spot