BSMO - Municipal Midyear Outlook: Come On In The Water's Fine

2023-07-13 03:10:00 ET

Summary

- With the highest yields in years, the muni bond market looks increasingly attractive.

- After the worst showing in four decades in 2022, the muni market regained some ground in 2023.

- There was some chop along the way, but the Bloomberg Municipal Bond Index etched a 2.67% return through June 30.

By Matthew Norton and Daryl Clements

With the highest yields in years, the muni bond market looks increasingly attractive.

After the worst showing in four decades in 2022, the muni market regained some ground in 2023. There was some chop along the way, but the Bloomberg Municipal Bond Index etched a 2.67% return through June 30.

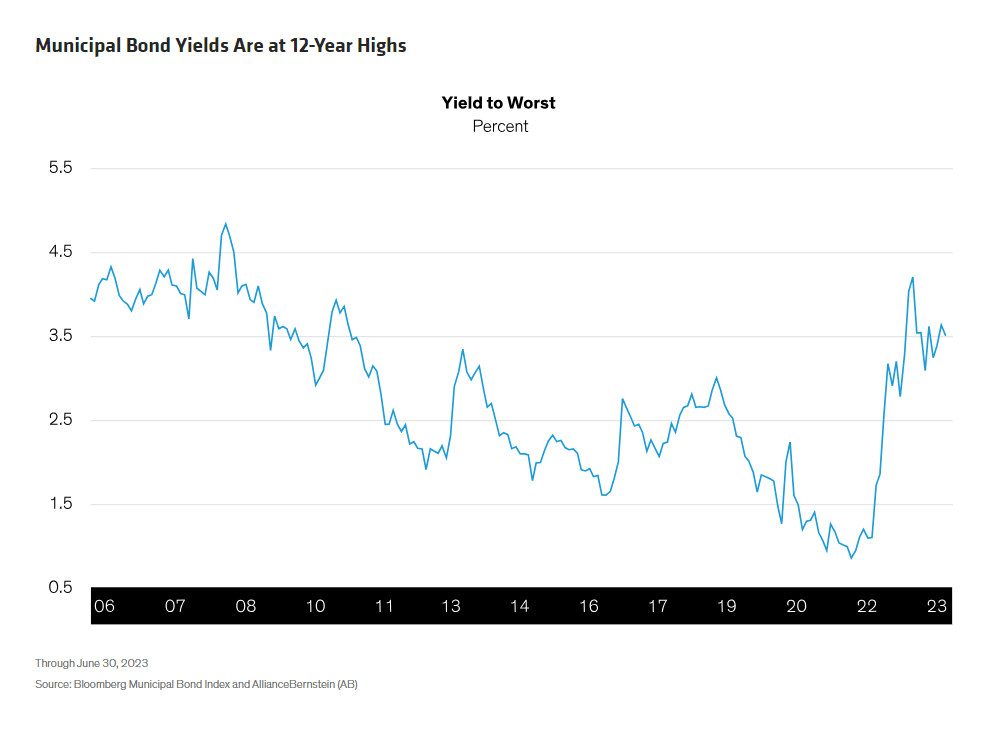

As anxieties tempered toward midyear, investors gradually returned to the market. Most were attracted by strong muni issuer fundamentals, the likelihood the Fed is nearing the end of its rate-hike cycle and historically high yields ( Display ).

{kind=link}

Midyear Muni Strategies in an Improving Market

To us, this seems like a very compelling entry point for munis. Yet many investors remain parked in cash or cash equivalents, waiting to see what happens.

Not only have they missed attractive returns compared to US Treasuries (munis have outperformed Treasuries since late 2022), but they’re now giving up significant potential return. Here’s how we think they can take advantage of today’s environment.

Extend your duration target. As we see it, longer duration should be muni investors’ most powerful ally since we expect yields to be lower in 12 to 18 months.

For example, for an investor in the top federal tax bracket of 40.8%, a three-month Treasury bill currently offers an after-tax yield of 3.21%. Compare this to 3.52% for the Bloomberg Municipal Bond Index, which has an average duration of six years as of June 30.

If muni yields drop just 50 basis points over the next year, this would add 3.00% in price gains to the 3.52% yield, for a total after-tax return of 6.52%. If three-month Treasury yields decline 50 bps, it would result in just 0.12% in price appreciation, for a total after-tax return of 3.33%.

Consider a barbelled maturity structure. While extending duration today can help capitalize on the interest-rate cycle’s next phase, there’s no all-weather strategy to reach a duration target. A laddered or bulleted approach to maturities works well in certain yield-curve environments.

But with today’s inverted yield curve - when short-term yields are higher than those for longer-term bonds - a barbell approach that pairs both short and longer issues may lead to better investment outcomes as the yield curve moves toward a more normal upward slope.

Take advantage of attractive credit spreads. Look to muni credit, such as BBB-rated bonds, for added return potential. The yield premium offered for these bonds relative to AAA-rated munis is nearly twice its historical average.

But be selective, not just across issuers but among sectors, too. States remain in excellent financial health as we approach a likely economic slowdown, and while many muni sectors can benefit from states’ strength, not all will.

However, muni issuers in general are resilient and have rarely defaulted , thanks to their inherent power to tax, raise revenues and cut expenses. Since 1970, the 10-year cumulative default rate for investment-grade municipal bonds has been 0.1%, compared to 2.2% for similarly rated corporate bonds.

For now, municipals have the advantage over Treasuries. And given today’s starting yields, we believe munis will likely benefit much more than Treasuries when yields start to fall.

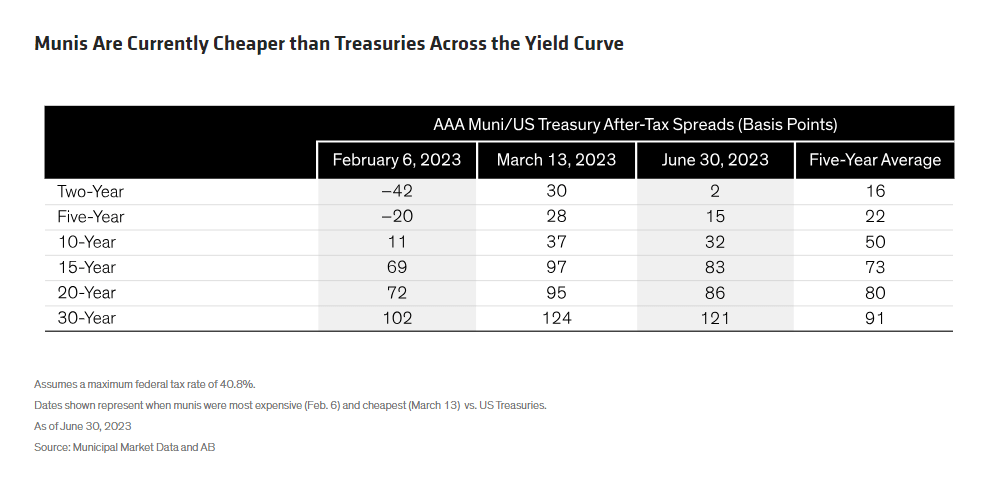

The after-tax yield relationship between US Treasuries and munis can be highly variable. For example, at the start of the year, Treasuries had the advantage over short-term munis, and we took advantage.

But by midyear, AAA-rated munis had become more appealing. In fact, based on spreads, they’re now priced from cheaper to fair value relative to Treasuries across the yield curve - with most very close to their five-year average ( Display ).

{kind=link}

But conditions can be fleeting, and if munis become relatively more expensive, it would make sense to rotate back to Treasuries. Here, flexibility is key.

Barring a significant economic downturn, we think the muni market will continue to perform well in 2023. The emerging “summer technical” should be especially price supportive, as an expected reinvestment of $94 billion in coupons and maturing bonds through August chases historically low supply and scant new issuance.

For investors still waiting on the sidelines, we think now is the right time to dip back in. Those who stuck around should stay flexible and willing to lengthen duration and add credit to continue enjoying the water.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Municipal Midyear Outlook: Come On In, The Water's Fine