MUR - Murphy Oil: Increased Buybacks Can Lift Shares

2023-11-27 20:08:01 ET

Summary

- Murphy Oil is making progress on its balance sheet transformation efforts, which could double capital returns to shareholders by Q3 2023.

- The company's strong production, particularly in the Gulf of Mexico and the Eagle Ford, is driving positive financial results.

- Murphy's offshore presence, particularly in the Gulf of Mexico, provides additional growth opportunities given regulatory support for expansion.

- When debt falls to $1 billion next year, I expect share repurchases to accelerate meaningfully.

Shares of Murphy Oil ( MUR ) have lost about 12% of their value over the past year as commodity prices have come down from their highs in the wake of Russia’s invasion of Ukraine. That said, the company is making material progress on its balance sheet transformation efforts, which are on track to be completed by the third quarter of next year, at which point capital returns to shareholders will likely at least double. This can be a catalyst for share price appreciation next year, assuming similar commodity prices.

{kind=link}

In the company’s third quarter , Murphy earned $1.63 , beating consensus by $0.22. This beat was driven by strong production, particularly out of the Gulf of Mexico. Oil production was up by 5% to 108.8mbo/d (thousands of barrels of oil per day) with total production up over 6% to 201.7mboe/d (thousands of barrels of oil equivalents per day). For a company with a relatively small $8 billion enterprise value, Murphy has varied interests. 44% of its production is offshore, 37% is in Canada, and 19% is onshore in the US, primarily in the Eagle Ford.

The Eagle Ford has been a solidly-performing asset for the company with production of 38mboe/d here—74% of this is oil. Murphy is now producing out of ten wells, seven of which it operates, and we are seeing much faster production out of these wells that had been the norm, leading to quicker cash flow conversion in the wake of capital spending. The Eagle Ford is not unique in being home to strong drilling results for Murphy. In Canada, it has 2 of the top 10 performing natural gas well, and 4 of the top 15.

{kind=link}

Importantly, its onshore locations in the Eagle Ford and Canada have 15 years of inventory at $40 crude, providing ample production opportunities. As the company builds greater scale in its plays, we are also seeing improved economics of scale with lease operating expenses down by nearly 3% from last year, even as production has grown by about 5%, improving per-unit economics by 8%. This further reduces breakevens and enhances the value of Murphy’s developed inventories.

What sets Murphy apart from most mid-sized E&P companies is that it has a large offshore presence. This primarily comes today in the Gulf of Mexico where it produces 86mboe/d and has operated for over seventy years. Production rose by over 10% while operating costs fell by over $2/barrel, in the quarter. Now, it is important to note that Q3 production can be quite volatile depending on the hurricane seasons. Hurricanes, like Ian in 2022, can force drillers to suspend activities, but this year’s hurricane season was fairly light. This likely overstated the true run-rate Q3 level of production.

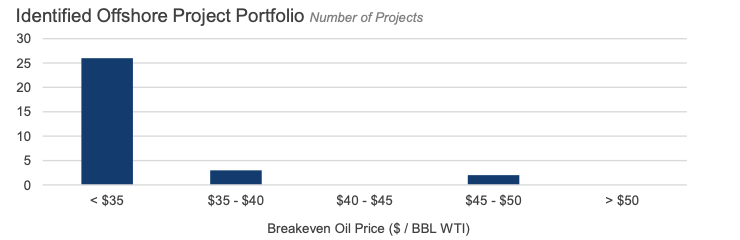

Murphy is committed to this play with 71% of potential offshore projects located in the Gulf of Mexico. These wells are generally less costly than those in deeper, more extreme environments offshore. Indeed, Murphy is essentially only looking at projects that can recoup their cost in a $40 oil price environment. With offshore drilling, regulations can often be a concern. I think it is important to note the Biden Administration is preparing new leases in the Gulf of Mexico as the Inflation Reduction Act requires offshore leasing to enable permits for wind projects, as part of an “all of the above” energy strategy espoused by Senator Joe Manchin of West Virginia. The IRA ensures an ongoing set of lease sales that should allow Murphy to expand and grow production as it wants.

{kind=link}

Now while the Gulf of Mexico is the primary focus of Murphy’s offshore capital program, it is not the only focus. Having received positive well data, Murphy has sanctioned its offshore project in Vietnam, which is expected to come online in 2026. MUR has a 40% interest here, and this play should generate net production of 10-15mboe/d.

Over the medium term, Murphy is targeting 210mboed of production, companywide. Alongside Q3 results, management raised 2023 guidance to 185-187mboed, up by 3mboed at the midpoint with 53% of production being oil. Essentially, Vietnam will account for half of the incremental production growth. Increased activity in its 3 main plays as well as potential activity in the Cote d’Ivoire should drive the balance.

On capital policy, Murphy is currently allocating 75% of free cash flow to debt reduction while it carries $1-1.8 billion in debt with 25% to free cash flow going to equity holders via is $0.275 dividend and buybacks. In Q3, it bought back $75 million of stock while adding $300 million to its authorization for a total of $525 million. This increased authorization was a signal, in my view, as to how capital allocation priorities will be shifting to equity holders.

During Q3, it redeemed $249 million of debt, taking total debt to $1.58 billion with $327 million of cash on the balance sheet. The company is buying back another $250 million in debt this month. That means it will end this year having paid down $500 million in debt with $1.33 billion of debt remaining. Once its debt load falls to $1 billion, a minimum 50% of free cash flow is allocated to dividends and buybacks. That means total buybacks and dividends will double from current levels, at the same commodity price.

Based on the company’s cash flow, this should occur during the middle of next year. Murphy generated $249 million of free cash flow in the quarter. It has generated $305 million year to date; $545 million excluding working capital. Murphy’s capital program is also H1 weighted. It anticipates spending about $1 billion in cap-ex for the full year, and it has already spent $900 million of that through three quarters. Accordingly, Q4 is a strong free cash flow quarter, and given production guidance and current commodity prices, normalized full year free cash flow should be at least $850 million.

One thing that has weighed on free cash flow is that Murphy has had $108 million in unsuccessful well costs from $35 million last year. A positive of offshore drilling is that potential finds can be gigantic and provide oil for longer periods of time than a typical fracking well, but on the downside, exploration is expensive with misses being costly. This increase in well costs is essentially equivalent to $1.10 lower realized oil prices across a full year’s production. If unsuccessful well costs normalize next year, this provides a modest cushion to cash flow.

At $75 oil and $3 natural gas, Murphy has $825-875 million of free cash flow potential. Its dividend costs about $170 million, leaving about $580 million of excess cash. Sometime during Q3 2024, it will have accumulated enough free cash flow to pay down $300 million in debt and bring debt to $1 billion. At that point, it will start returning at least 50% of free cash flow, or a minimum run-rate of $425 million. In reality, we are likely to see returns exceed the 50% benchmark given limited need to reduce debt further. At today’s share price, $425 million provides about a 6.5% capital return yield. I would expect to see MUR begin reducing the share count via buybacks by at least 3%/year with moderate dividend increases.

Given offshore production is riskier than onshore production, I would expect Murphy to trade at a discounted valuation to pure-play fracking companies, like Diamondback (FANG). While I have pegged fair value for FANG at an 8% free cash flow yield, I view a 25% discount or a 10% free cash flow yield for MUR as appropriate as it shifts capital returns over the next year toward equity holders. That still provides a capital return yield of 5-6% and a fair value of at least $52/share. That represents 22% upside. I view MUR as a buy and expect gradually accelerating buybacks and a dividend increase in 2024 to help push shares toward fair value.

For further details see:

Murphy Oil: Increased Buybacks Can Lift Shares