PM - My 3 Top High Dividend Yield Picks (8-11% Yields)

2023-08-08 13:31:05 ET

Summary

- High-yield investments come with a certain degree of controversy.

- You're either getting a high yield because of high risk, or because of certain biases from the investment community.

- Here are 3 top high-yield investment ideas.

Written by Sam Kovacs.

Introduction

There is something about a big fat dividend yield.

Something about the yield that sometimes seems too good to be true.

After all if markets return a total of 8-10% in the long run, how can we expect a single stock to provide a double digit yield consistently without draining its value?

I'll tell you how.

Markets are mostly right about things. It is such that the collective intelligence of individuals is reproduced into markets. This is why you'll see markets crash before the economy, and go up before the economy.

Markets are what you call a leading indicator.

But they aren't a perfect mirror of the future. They are tainted with biases of all sorts which are common to humans.

Among these biases which impact the market and are relevant to the 3 investment opportunities presented today are:

- Recency Bias : The assumption that future events will resemble recent events.

- Status Quo Bias : The preference for maintaining the current situation and opposing actions that might change the state of affairs.

- Cognitive Ease Bias : The preference for information that is easy to digest, and to ignore information which is more complex.

- Collective Self-Righteousness (to not use the woke word): The belief in a supposed morally superior set of thoughts and values and dismissing opposing views.

If the market as a whole, or a sufficient part of market participants is impacted heavily enough by one of these biases, then they will reflect in equity prices, or at scale in overall market prices.

Of course, if these biases differ from reality (as is most often the case), then it is only a matter of time before they correct and reflect better values.

In these cases, high yield investments which are also undervalued present compelling opportunities, as on top of the income, there lies an opportunity for capital appreciation.

These are the high yield investments you want: where something is causing the market to be biased in a certain way which is creating a temporary or persisting discount in the price.

The top of high yield investment you don't want, are those where it is yielding a lot because of higher risk. A lot of high-yield investments are just junk. There is a point with high yields where an extra point of yield comes at an exponential increase in risk.

You see these often with very high yields just before a dividend is cut. These are yield traps. You don't want those.

Here are 3 investment opportunities yielding between 8% and 11% which I believe are mispriced due to market misunderstandings.

Blue Owl Capital Corporation ( OBDC )

Blue Owl Capital Corp is a Business Development Company, or BDC. BDCs are specialty finance companies, which lend money to small and mid-sized companies which have financing needs which are not supported by the public debt market or by banks.

As such, BDCs fill a gap in the market which is often not understood by the public. But cognitive ease isn't the bias which has provided high yields to BDCs. It is the recency bias of the Great Financial Crisis which has created a generational fear and aversion to the financial sector at whole which is at work.

Don't believe me? Just look at the fear of a systemic banking meltdown when Silicon Valley Bank failed.

While the situation looked nothing like what went down in 2008, many investors (including seasoned veterans who should have known better) feared the worst.

They've got the investor's version of PTSD.

OBDC has generated high dividends while maintaining its Net Asset Value between $14 and $15 since 2016, 3 years prior to it going public.

This means that the firm has been successful at generating income from its middle market loans which it has passed on to investors.

We added OBDC to our High Yield portfolio in the spring of 2021 at a price of $14.2. The position has returned 20% since then. All of this return has come from dividends.

And I believe that OBDC offers a very good value proposition. They fund middle market companies and aim for 1-3% position size for each of their borrowers, which reduces significantly the impact of any bankruptcy.

{kind=link}

As rates have increased, OBDC's spreads have remained similar, as they have passed on higher rates to their borrowers, maintaining a 6.7% spread on their loans.

{kind=link}

OBDC has been doing very well in the current environment, where they've continued to find ways to increase their spreads, as management pointed out in the first quarter earnings call .

With the public market mostly unfavorable for new issuance, we continue to see direct lenders financing nearly all of the deals that are coming to market. These opportunities are attractive because they are for high-quality borrowers with enhanced spreads, documentation and leverage levels.

As we've noted before, given continued low repayments, ORCC is currently benefiting from this environment, largely through amendments and other repricing events which continue to help increase the overall spread on our portfolio.

{kind=link}

Management does expect some challenges in the upcoming quarters, and it will be interesting to see the second quarter results to see how these things are evolving. Mostly management doesn't expect to see any major issues which will cause a major threat to OBDC.

We are closely monitoring the interest coverage levels of our borrowers. As we expected, reported interest coverage continued to decline, finishing the quarter with a weighted average coverage ratio of 2.2x.

We fully recognize that the current rate environment, as it works its way through borrowers' financials, will reduce interest coverage levels over the course of the year. We believe average interest coverage on our portfolio will trough around 1.5x in the second half of this year. This will undoubtedly pressure liquidity at some borrowers more than others. However, we believe we have good visibility into the small number of borrowers, which could be most affected, and therefore, we think that these challenges will be manageable.

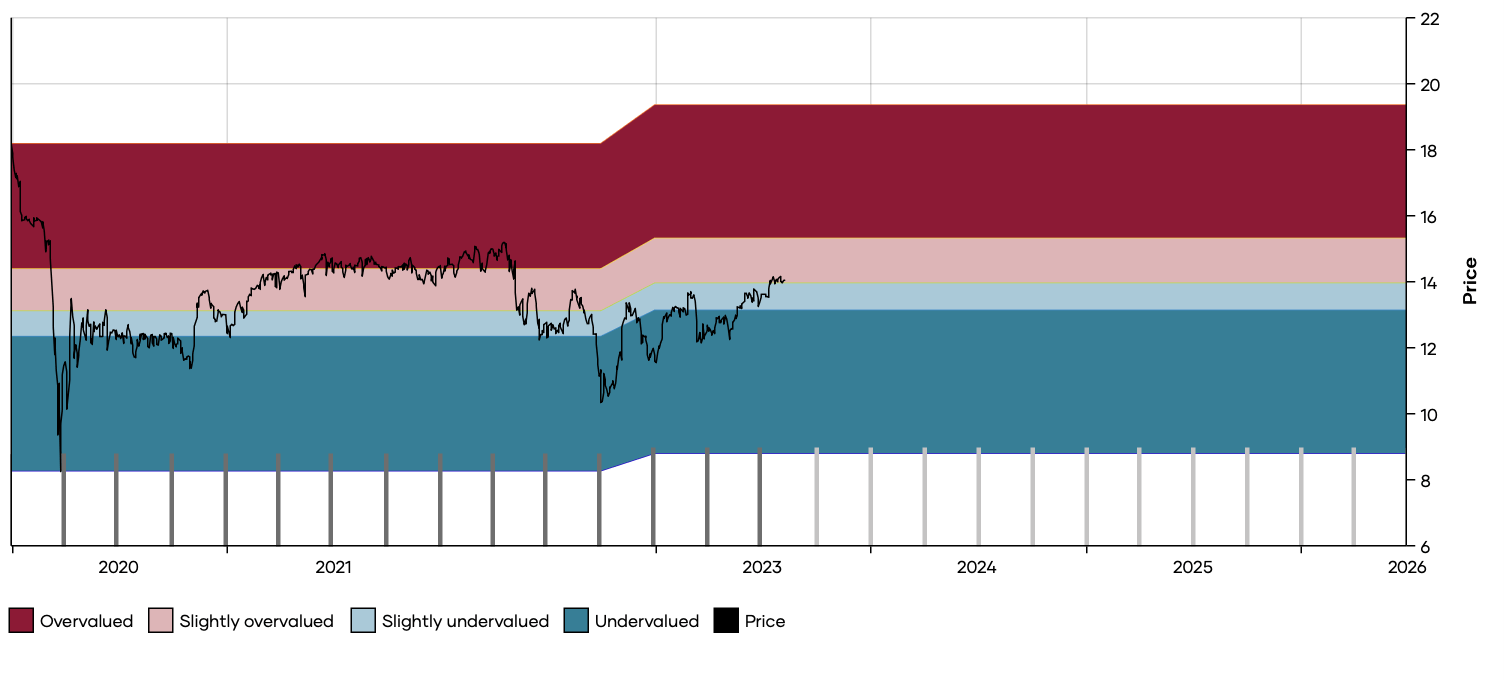

OBDC, since 2019, has been trading in a way which has converged towards a 9.4% median yield.

{kind=link}

This is about a 7-8% discount to NAV currently. When you add the supplemental dividends which OBDC have been paying this year thanks to higher income, you get to an estimated 11% yield.

Now let's be clear: I expect NO capital appreciation from OBDC. I expect the company will continue to maintain NAV somewhere between $14 and $15, and generate about 10% in dividends per year.

And frankly, I'll take it.

With BDC's, the ability to retain their NAV over time is extremely important.

If you look at Eagle Point Credit ( ECC ) over time, you'll see that they have failed to maintain their NAV due to constant share emissions which have consistently diluted shareholders and led to a declining price over time, as a direct relation to the declining NAV.

Arbor Realty Trust, Inc. ( ABR )

In March, a short report from a bogus research company tanked ABR's stock.

We read it, and our instant reaction was: "this is BS." So I wrote a piece putting my neck on the line saying that ABR was a great investment and that the short report had no basis. At the time Arbor yielded 13.9%.

Since then ABR has increased by 49%.

Seeking Alpha

Today, ABR trades at $16.7 and yields 8.6%.

The company increased its dividend for the 12th time in the past 14 quarters.

It's second quarter results were impressive, with management showing its expertise once again.

I do appreciate the conservative view they've taken, to weather the current downturn in real estate. From the last earnings call :

We produced distributable earnings of $0.57 per share, which is well in excess of our current dividend, representing a payout ratio of around 75%. The dividend policy that we have implemented with our Board of keeping such a wide disparity between our earnings and dividend provides us with a huge cushion and was a very strategic knowing full well that we're entering into a market of dislocation. This has enabled us to raise our dividend, grow our book value and create reserves, and we believe we're uniquely positioned as one of the only companies in that space with a very sustainable protected dividend even in this challenging environment.

Management shared their macro views about the market in upcoming months:

So let me give you a little bit about macro view on this one that we've had for quite some time. And one that has obviously put us in a very favorable position in terms of liquidity and strategy and personnel and resources. It's been our view that generally, these downturns last 18 to 24 months and on the outside of it. And if it's a downturn, that's short-term, it's 15 months. We've been at this already for at least five quarters, and that's why we think that there could be another two to three quarters left. Having been for multiple cycles, we feel now we're pretty much on the bottom of the cycle and that we're going to work our way out of it shortly. But the bottom is the most difficult period of time.

So, the company will likely continue to build reserves in upcoming quarters, as it has done in the past couple of quarters. The fact that it has been able to grow its reserves, increase its dividend, and at the same time increase its book value is clearly a testament to the strength of Arbor's platform.

Which is why I scoff somewhat when the likes of Piper Sandler downgrade Arbor on the basis of its premium to its peers being too rich.

This is the worst reason to downgrade Arbor.

Book Value isn't so important in mortgage REITs, cashflow generation is what matters.

Arbor generates plenty of cashflow, amply enough to cover the dividend and to leave room for a blow in the next couple of months.

How have peers been doing? Well, book value certainly hasn't been going up.

Chimera ( CIM ) has repeatedly cut its dividend. PennyMac ( PMT ) has again cut its dividend this year, AG Mortgage Trust ( MITT )'s dividend never truly recovered since 2020, and Blackstone Mortgage Trust ( BXMT ) hasn't increased its dividend in over 8 years.

Comparing these "peers" on a price/book ratio to guide your investment decisions is quite amateurish, but once again a route of cognitive ease for certain sell-side analysts.

{kind=link}

Arbor has returned to its late 2021 prices, as we're entering what management expects are the worst two to three quarters in this downturn.

Yet the stock has been strongly trending up.

What do I expect from here? Some short-term consolidation is definitely possible as we see how bad the next two quarters really are, but then the markets will turn to what will likely be an environment in which rates have topped and are likely to come down, when we'll see Arbor thrive once again.

I personally think Arbor should be a $20 stock, and wouldn't be surprised to see it rise all the way to $25-$27 in the next up cycle.

Altria Group, Inc. ( MO )

In the introduction to this article, I mentioned a few biases which could lead to prices of assets being dislocated from reality.

The two stock picks above carry some elements of recency bias and cognitive ease bias in their valuations.

But I kept the self-righteousness bias for last.

Every time I write an article on tobacco, I get a bunch of investors barge into the comment section on their white horse explaining how they'd never invest in something that is so deadly and kills people.

I always wonder how many of these individuals own The Coca-Cola Company ( KO ), McDonald's ( MCD ), or PepsiCo ( PEP ) stock, and don't realize the hypocrisy of pointing fingers at vile tobacco: obesity kills more people than tobacco, but the ultra-processed products that lead to obesity aren't nearly as vilified as tobacco.

Now, I'm not saying tobacco is good, or better than Coke, I'm saying that as an investor I don't care.

If people can use their free will to smoke and get fat, I can use my free will to profit from it.

If you don't want to invest because of your convictions, so be it, but respect that others don't share your convictions.

The thing is though, that at large the market shares these convictions. The widespread "woke" wave has vilified tobacco, and investing in tobacco. Wokeness is wanting a diversity of everything, except of thought.

Only a fraction of pension funds and institutional investors will still consider investing in the sector, because of the importance of keeping appearances up and looking like good, proud, responsible citizens.

Whatever. This means that the demand for tobacco stocks is skewed negatively relative to other industries, which means that the equilibrium price which we can expect for assets within the industry, is much lower than other industries.

Philip Morris ( PM ) yields 5.2%. British American Tobacco ( BTI ) yields over 8.5%. So does Altria ( MO ).

This diverges significantly from the yields of consumer staples in the food and beverage industries, such as those that I mentioned above.

The bad news is that there is likely no going back. Investors have chosen to express their ideological and political views through their investments, which while anti-capitalistic, is the reality we have to deal with.

In 2017 Altria yielded 3%. I don't think we're ever going back to that.

Today, Altria trades at $44, and yields 8.5%, significantly more than its 10-year median yield of 5%.

{kind=link}

What is impressive is that Altria has been increasing its earnings like clockwork, despite volumes of cigarettes declining.

This has been the case for years. This sort of headline has become a common occurrence for Altria:

Altria sees profit rise even as cigarette demand falls in the U.S.

The problem is that now, price increases are not enough to increase revenues.

This is something that I had forecast would happen, when I looked at the numbers.

In 2020, I looked at the price elasticities of cigarettes at different price points globally to figure out when Altria's price increases would lead to a decrease in demand large enough to cut revenues:

I concluded that:

Depending on the number of future increases, this effectively gives the company a 3 to 5-year runway before price increases would result in lower revenues.

Unfortunately, I think the reality is likely on the shorter end of that range.

For this reason Altria needs one of its new segments to truly take off within the next 5 years.

And while both PM and BTI have both had very successful no-combustion platforms with IQOS and Vuze, Altria has failed again and again in the space.

JUUL was a bust. Their attempt to go live with IQOS in the U.S. was a bust.

Now they're counting on their latest acquisition NJOY, to be the star non-combustible product... let's see how it goes.

{kind=link}

Nonetheless, EPS increased on the back of a 2% buyback yield, and increases in operating income, as Altria manages to continue to work its magic as it seeks to increase its income in years to come.

The dividend continues to be covered by free cash flow, and while smokeless revenues are just 10% of Altria's business, its sizeable investment in AB Inbev also provides repeating incomes.

All of MO's competitors have managed to hack the smokeless market, it is about time MO did so.

It is clear to me that the company will manage to keep at least stable cashflow generation for another few years thanks to share buybacks and cost optimization, which hopefully will give it the time to catch up and develop a strong smokeless platform.

Hopefully, we sit back, and NJOY the ride.

Conclusion

Buying high-yield investments which are also high quality usually comes with either a degree of complexity, stigma, misunderstanding or all three.

Yet high yield positions can supplement any portfolio brilliantly, and provide consistent income throughout any market environment.

Investors just need to make shrewd decisions.

For further details see:

My 3 Top High Dividend Yield Picks (8-11% Yields)