XYLD - My 9% Income Portfolio - Nobody Is Perfect

2023-08-22 01:23:37 ET

Summary

- Perfection is defined as being complete and correct in every way, and can be pursued in various fields, including art and investing.

- For years now, I have been employing all my strength in investing in CEFs and ETFs, plus some “flirtations” with ETNs and BDCs.

- My portfolio is certainly not perfect, but acceptably fulfills the task for which it was designed: namely, to provide me with a steady stream of dividends over time.

- In this article, I take stock of the performance of all my positions over the course of 2023, assessing their strengths and weaknesses.

What Is Perfection?

Aristotle defines perfection as “that which is so good that nothing like it could be better.” Perfection can thus be regarded as freedom from fault or defect, a state of being complete and correct in every way. Each of us tends in our own way toward perfection, a flawless state where everything is exactly right, as in nature and mathematics.

The first to intuit and pursue perfection in art was Piero della Francesca (c. 1412-1492), one of the greatest interpreters of the Italian Renaissance. He was unsurprisingly mathematical and author of three treatises, proving that his painting found its substantial foundation precisely in this subject, to the point of enunciating in almost complete form the mathematical principles of Leon Battista Alberti on perspective, which he regarded as the “science of painting.”

Similarly, modern “investment science” is the application of scientific tools, primarily mathematical, to the study of investments, with the aim of identifying general principles and putting them into practice to reach better decisions. My lack of inclination to study mathematics, however, makes me lean more toward behavioral finance, that branch of economic studies that investigates financial markets by including in its models the principles of psychology related to individual and social behaviors.

The Quest for Perfection

It is probably for this reason that I cannot make the interactions between mathematics and investing my own, where I am increasingly convinced that our relationship with money is psychological and not merely numerical or exclusively based on portfolio management algorithms. Of course, I wish it were possible to strive for perfection in that field as well, but I do not believe that “perfect” portfolios exist: each of us tries to design a portfolio that can meet our needs as much as possible, despite its perfectibility.

For years now, I have been employing all my strength in investing in CEFs and ETFs, plus some “flirtations” with ETNs and BDCs. I am constantly studying new titles to include in my portfolio, but I often stop there, without sinking my teeth in, because in the end I always tell myself “don’t change a winning team.” That mine is a winning team is in fact a personal conviction, but by now I know its merits and flaws, and, all in all, I have gotten used to them. No presumptuous pursuit of perfection, just acceptance of reality and of my limitations.

After years of trial and error, I believe, in fact, I have built a portfolio that sufficiently and acceptably fulfills the task for which it was designed; namely, to provide me with a dividend stream that is as constant as possible over time, without exposing me to irreparable losses, although with a good deal of volatility to digest. It is certainly not a perfect portfolio, but it performs its duties well.

My Income Portfolio

As you may know, my investments are divided into three different income portfolios: Cupolone , my primary CEF portfolio; Giotto , comprised of ETFs that adopt a covered-call strategy; and Masaccio , my “tactical” portfolio. There are 26 securities in total: they all offer monthly distribution with the exception of ARCC, CCAP, and RVT, which have quarterly distributions.

Cupolone Income Portfolio (named after Brunelleschi’s Florentine dome) is my strategic, primary investment portfolio, the backbone of my overall portfolio. Its solid, structured foundation is based on the following sixteen CEFs:

- BlackRock Science and Technology Trust ( BST )

- Calamos Dynamic Convertible and Income ( CCD )

- Calamos Global Total Return ( CGO )

- Eaton Vance Enhanced Equity Income Fund II ( EOS )

- Eaton Vance Tax-Adv. Global Dividend Opps ( ETO )

- Eaton Vance Tax-Adv. Dividend Income ( EVT )

- Guggenheim Strategic Opp ( GOF )

- John Hancock Tax-Adv. Dividend Income ( HTD )

- PIMCO Corporate & Income Strategy ( PCN )

- PIMCO Dynamic Income ( PDI )

- John Hancock Premium Dividend ( PDT )

- PIMCO Corporate & Income Opportunities ( PTY )

- Cohen & Steers Quality Income Realty ( RQI )

- Special Opportunities Fund ( SPE )

- Cohen & Steers Infrastructure ( UTF )

- Reaves Utility Income Fund ( UTG )

Giotto Income Portfolio (named after the fourteenth-century Florentine painter and architect) includes five ETFs that adopt a covered-call strategy.

- JPMorgan Equity Premium Income ( JEPI )

- JPMorgan Nasdaq Equity Premium Income ( JEPQ )

- Global X NASDAQ 100 Covered Call ( QYLD )

- Global X Russell 2000 Covered Call ( RYLD )

- Global X S&P 500 Covered Call ( XYLD )

Masaccio Income Portfolio (named after the founder of Renaissance painting) is my third, “tactical” portfolio, which contains these five securities:

- Ares Capital ( ARCC )

- Crescent Capital ( CCAP )

- Royce Value Trust ( RVT )

- Credit Suisse X-Links Crude Oil Shares Covered Call ETNs ( USOI )

- XAI Octagon FR & Alt Income Term Trust ( XFLT )

My portfolio’s annual distribution is slightly above 9% even if part of the securities within it are at a loss compared to purchase price. Considering the critical issues faced by the financial markets over the past two years, I think it can be normal for a high-dividend portfolio like mine to record some paper losses, given also the type of leveraged instruments it contains. While I am convinced that some of these losses are temporary, and can be recovered with a little patience (to which I am quite trained in), one should not forget the fact that Italian taxation on financial instruments is rather complex and penalizing for us investors.

Thus, if I were to sell a CEF at a gain I would pay taxes on it, but if I sold the same CEF at a loss I could not offset it against the gain of another CEF, on which I would equally pay taxes. In fact, losses can only offset (within five years) gains obtained from individual stocks or ETNs, which implies a great deal of caution before dismantling loss-making positions if you do not have adequate financial instruments to offset gains. Should you wish to sell at a loss in Italy, you must be very convinced that you made a mistake. Otherwise, you risk making two: selling at a loss and not being able to recoup some of it through a tax benefit.

August Check-Up

In 2023, stock markets trended broadly positive, despite the banking sector crisis that put them under pressure in March. The rise in the U.S. stock market, though, was led by a small group of large cap stocks, all belonging to the Nasdaq, whose earnings exceeded expectations.

August is not usually a stock market friendly month, with investors often taking advantage of a seasonality that is not always favorable to take home profits. Financial markets have been reporting corrections in recent weeks, triggered by the U.S. credit rating cut by Fitch, to which have added concerns about further increases of interest rates and troubling news from Chinese real estate.

Let us briefly look at how the securities present in my three portfolios performed over the course of 2023 starting with the sixteen CEFs that make up Cupolone, then examining the five Giotto ETFs and finally the remaining five CEFs/BDCs/ETNs in Masaccio.

As I have pointed out in previous articles, when choosing what percentages to allocate to the securities in my portfolio, I decided some years ago to look at their performance over time, identifying the NAV trend (and thus possible value creation or destruction) as a compass.

I won’t say that all the funds or stocks in my portfolio always show a positive NAV performance since launch, but rather that I prefer to avoid those trending inexorably downward, giving me very little hope of reversing. Following this criterion, I decided to favor securities that have a sinusoidal path largely related to market cycles.

Cupolone Income Portfolio

{kind=link}

YCharts

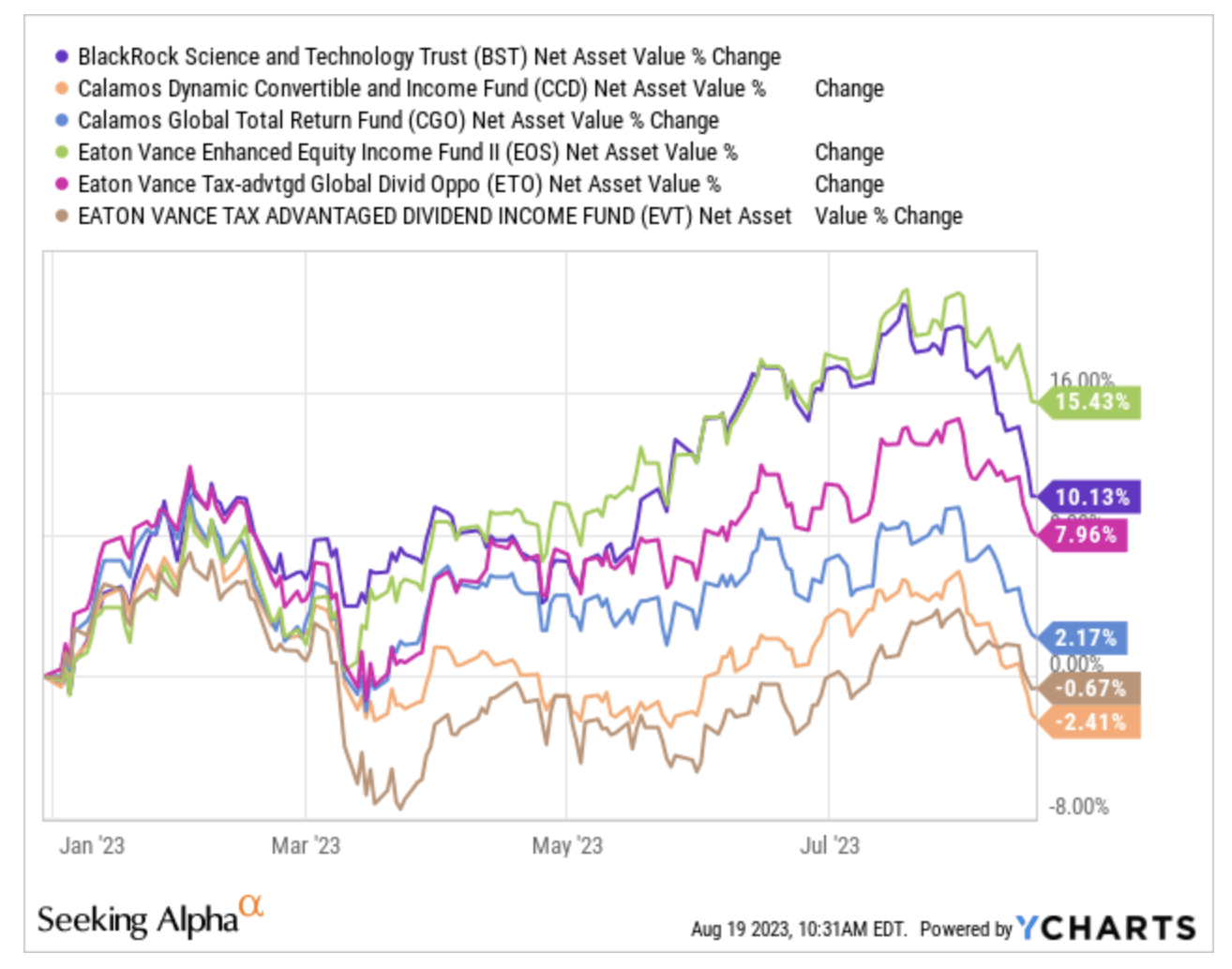

BST is a fund launched by BlackRock in late 2014 and dramatically grown for a full seven years until late 2021, parallel to the trend of the technology sector it refers to. In 2023 it showed a substantial rebound from the losses of 2022 even if my purchase price is still much higher than the current market price. No reason to reduce or close my position, though, for its largely positive track record since launch.

CCD and CGO are two Calamos funds: the former invests mainly in convertible bonds; the latter is a fairly diversified Global Allocation equity with low capitalization and rather thin trading. In 2023, CCD’s performance was fairly flat and today it is just below January values. CGO on the other hand has hinted at a rebound, limited however to a few percentage points. Two steeply losing positions in my portfolio, but the one I am most concerned about is CGO: during 2023 I reduced my exposure, although its NAV has already shown major recoveries in its history. I am monitoring both of them while waiting to make a decision on their future, but it is likely that CGO will be liquidated if it recovers its losses.

Of the three Eaton Vance funds, EOS is an inclusion from 2022, while ETO and EVT have been in my portfolio since 2020. EOS invests in growth stocks among diversified sectors and also generates its earnings from selling call options; ETO is a Global Allocation equity rather diversified in both sectors and countries; EVT is a 70-85% equity fund that invests mainly in the U.S. market. All three of these funds have lost a lot during 2022, but over the course of 2023 EOS and ETO have shown a convincing recovery, while EVT is around January values. All three are steadily part of my portfolio, although EOS is a slightly loss-making position, while ETO and EVT are largely positive relative to the purchase price.

{kind=link}

YCharts

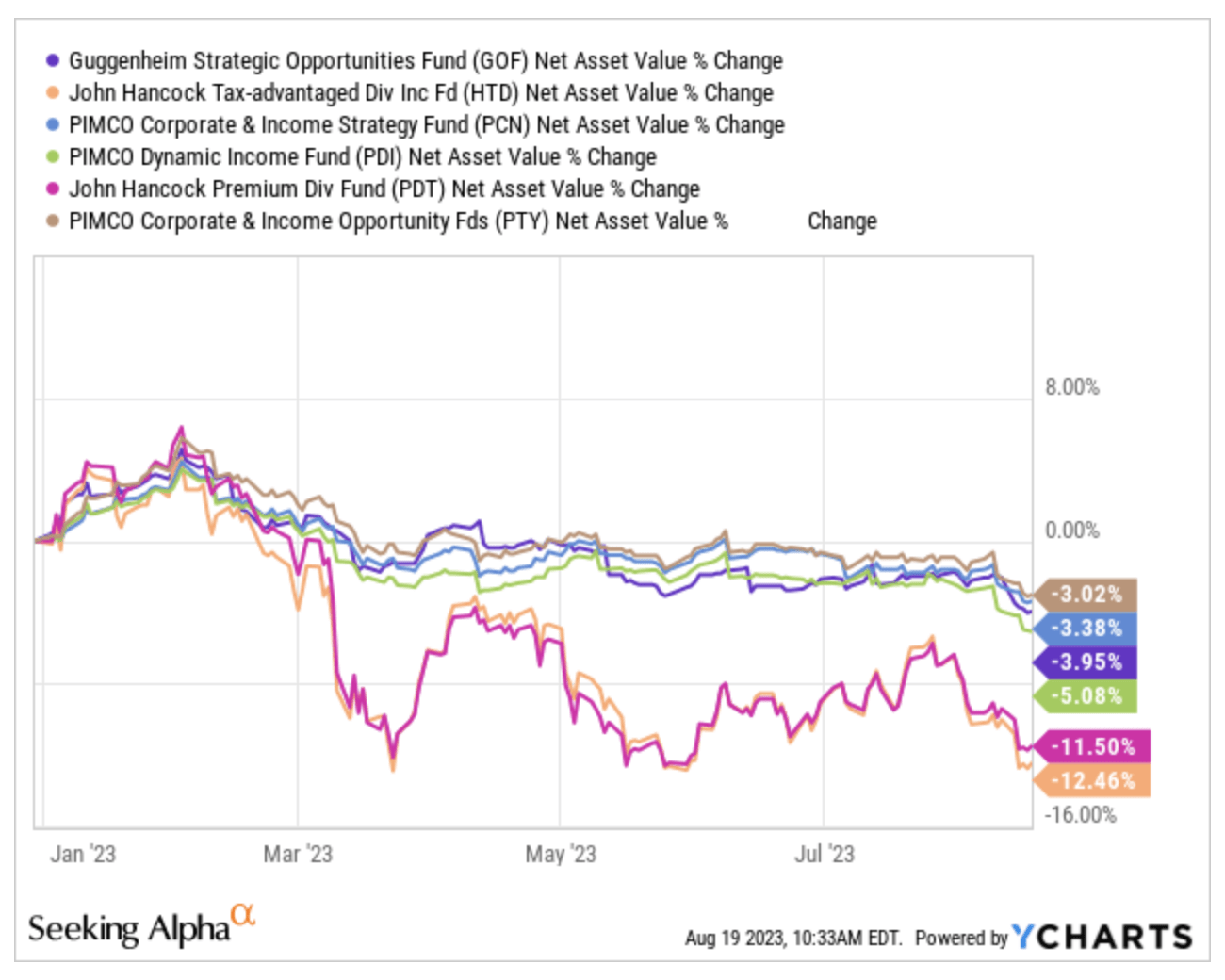

GOF is a multi-sector fixed income fund from Guggenheim, about which I continue to have many misgivings, despite the fact that 2023 performance shows only a slight loss (and that its market price sells at premium of about 30% to NAV). Over the course of 2023 I have reduced my exposure to this fund, which today occupies around 3% of my portfolio, but I have growing doubts about the sustainability of its dividend, although the market seems to have a different opinion about it. I still have not made any decision about its future, although I have strong doubts about its chances of recovery.

HTD and PDT are twin funds of John Hancock, both with 50-75% equity allocation mainly in the utilities sector, with a preferred stock component, which is more relevant in PDT. Their trend was largely negative in 2023 but I intend to continue maintaining them in my portfolio because I consider them to be good funds, both performing in positive territory since launch.

Workhorses of many high-yield portfolios, mainly because of the fame attached to their managers’ names, the three Pimco’s multi-sector fixed income funds ( PCN , PDI , PTY ) show a slightly negative trend during 2023 and a loss well above 20% since launch. Despite this, PCN and PTY are two positive positions relative to my purchase price, while PDI is at a very large loss with no signs of abating. No intention however to liquidate its position at the moment, although I have strong doubts about the sustainability of the dividend (more than 14% at today’s share price.)

{kind=link}

YCharts

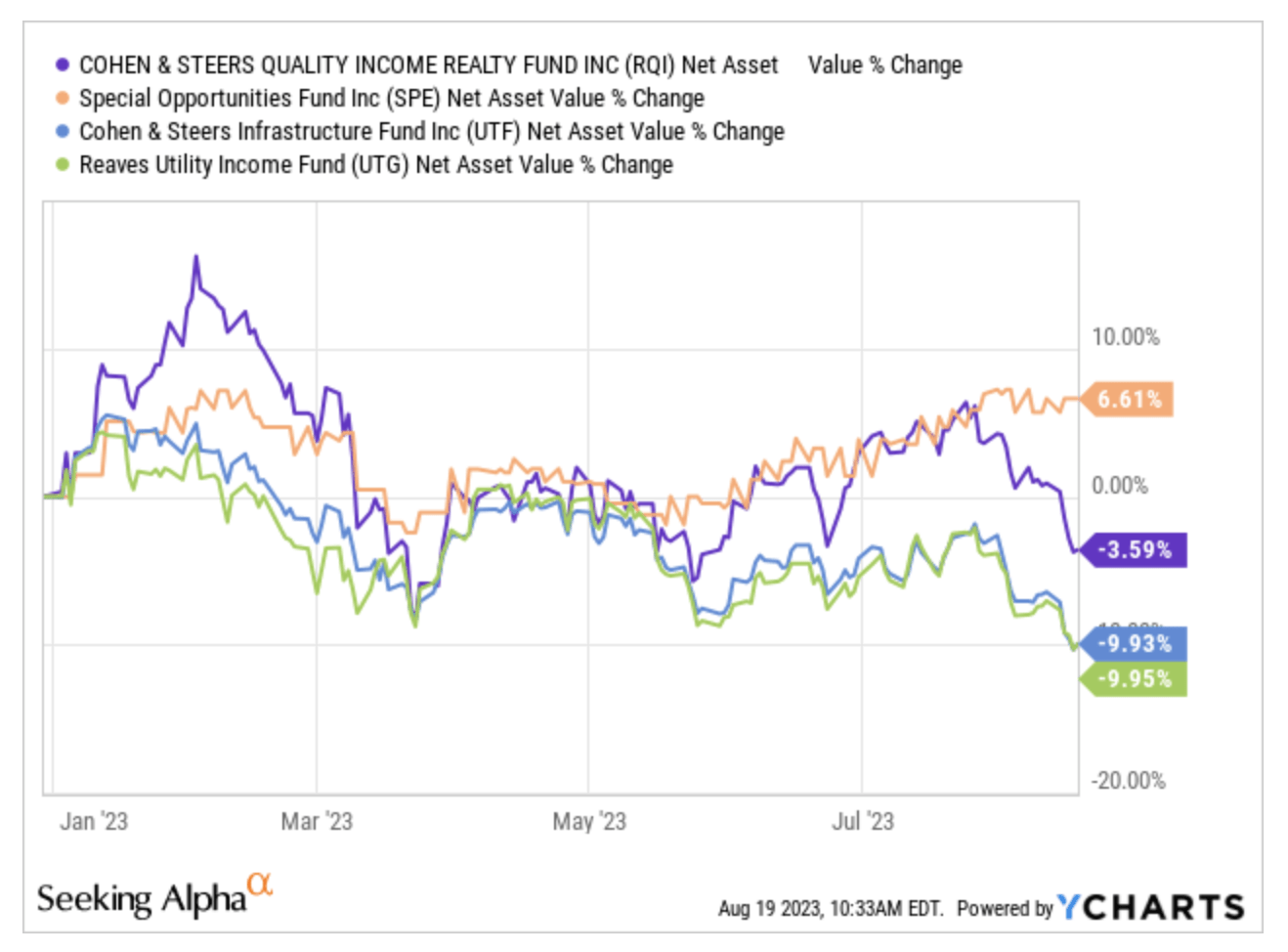

RQI and UTF are two Cohen & Steers funds: the former is a Real Estate CEF, while the latter invests in infrastructures and utilities. Sideways trend for RQI in 2023, with slightly negative values compared to January, while UTF is losing about ten percentage points. Steadily part of my team, both positions are in gain in my portfolio compared to their purchase prices.

SPE is a CEF from Bulldog Investors classified as Tactical Allocation, a definition that implies a diversified blend of equity, bond, BDC and SPAC investments. Positive performance during 2023 for this fund, whose retention in the portfolio does not cause me particular concern even though my position is at a loss relative to the purchase price.

UTG , finally, is a Reaves fund that invests in utilities, among the best and most stable in my entire portfolio. A steady upward trend for more than a decade, in 2023 has so far lost about ten percentage points and shows a trend that mirrors that of UTF. Slightly losing position in my portfolio but of no concern at this time.

Giotto Income Portfolio

{kind=link}

YCharts

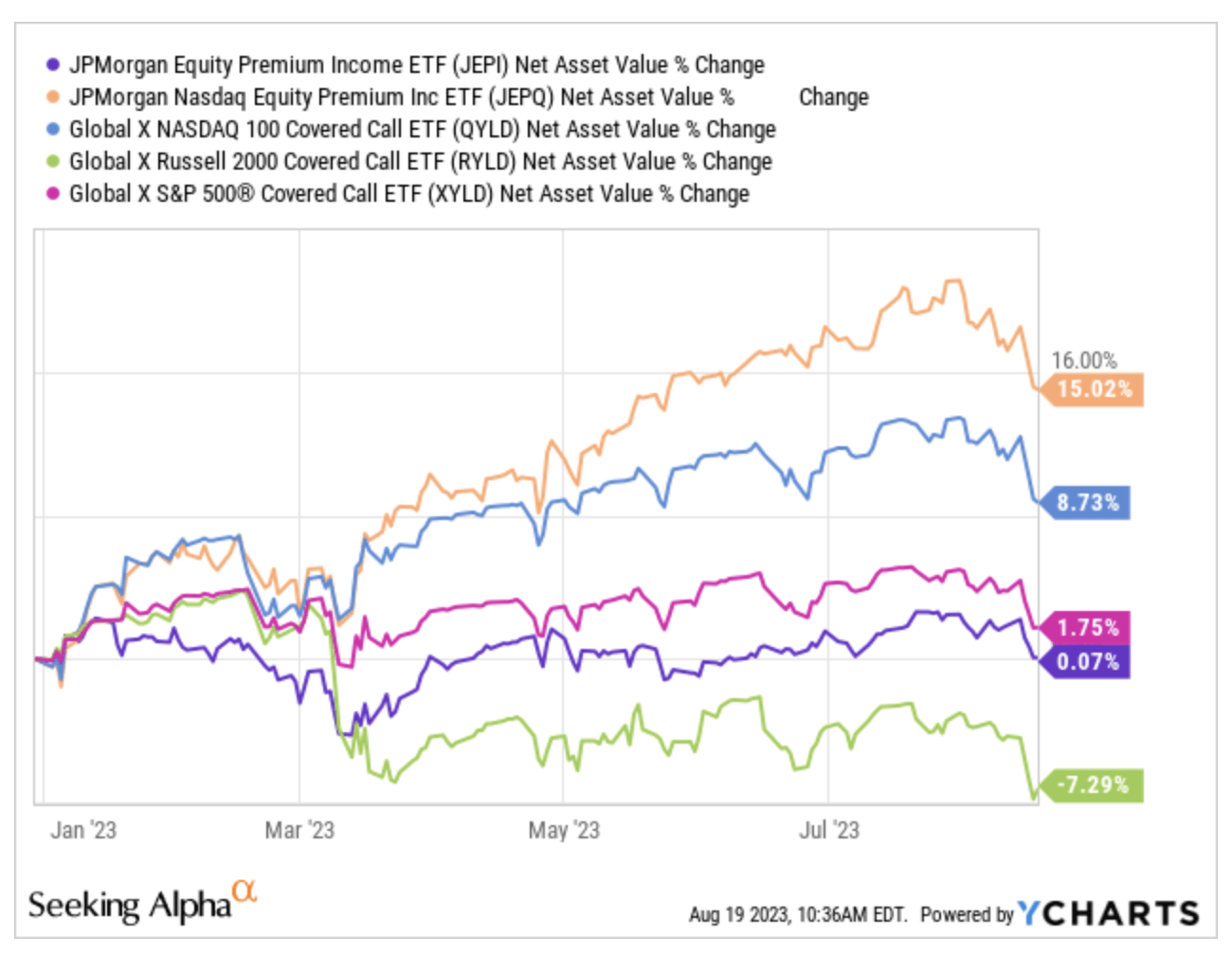

JEPI and JEPQ are two JP Morgan covered call ETFs, the former launched in 2020, the latter in 2022. JEPI is a huge ETF, with nearly 30 billion in capitalization, which trades on the S&P 500 with derivatives, while its younger brother, JEPQ, adopts the same strategy on the NASDAQ. JEPI’s performance in 2023 has been relatively even, while JEPQ shows a significant gain, in line with the performance of its benchmark index. Both of these ETFs occupy an important role within my portfolio, and I have no intention of giving up their contribution to my total income.

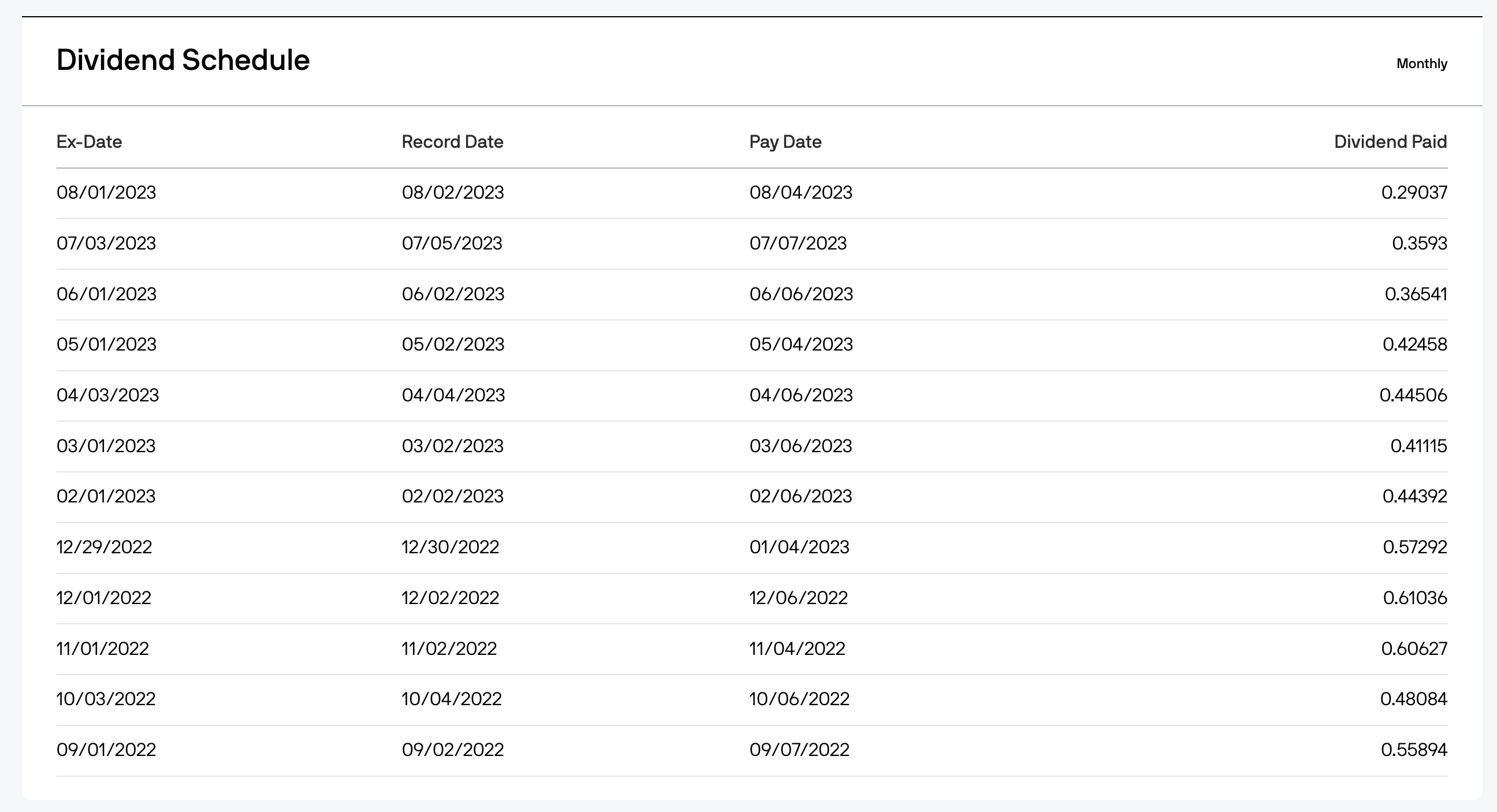

I recently lightened my position in JEPI, which was the largest in my overall portfolio, because of the fickleness of its dividend, which fell this month to its lowest in a year, as can be seen from the table below. I had exposed myself a little too much on this fund, and I preferred to take a step back.

{kind=link}

JPMorgan

Dividend Schedule for JEPI.

Pending decision on its future use, the cash from the easing of my position in JEPI has been temporarily parked in SGOV (iShares 0-3 Month Treasury Bond), an ETF that offers vanilla exposure to ultra-short-maturing fixed income securities of the US Treasury market.

QYLD , RYLD and XYLD are three Global X covered call ETFs that invest in the NASDAQ, Russell 2000 and S&P 500, respectively. QYLD’s performance was rather positive in 2023, while XYLD gained only a few percentage points. On the other hand, RYLD’s performance was disappointing, tied to the performance of a sector that has not yet shown signs of recovery. In any case, QYLD and RYLD play their game within my portfolio, and at the moment I have no intention of giving up their contribution to my total income.

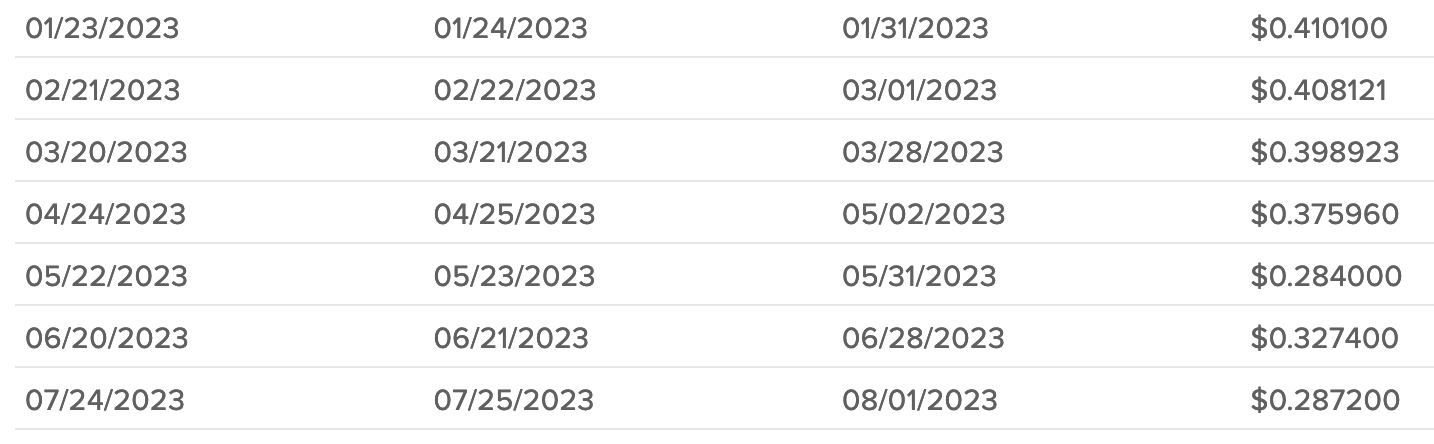

As for XYLD, I recently lightened my its position, which was the second largest in my overall portfolio, also in this case because of the fickleness of its dividend, which has fallen to historic lows in recent months, as can be seen from the table below. Again, I felt I had exposed myself a bit too much on this fund, and I preferred to take a step back.

{kind=link}

GlobalX

Dividend Schedule for XYLD.

Pending decision on its future use, the cash from the easing of my position in XYLD has been temporarily parked in SGOV (iShares 0-3 Month Treasury Bond), an ETF that offers vanilla exposure to ultra-short-maturing fixed income securities of the US Treasury market.

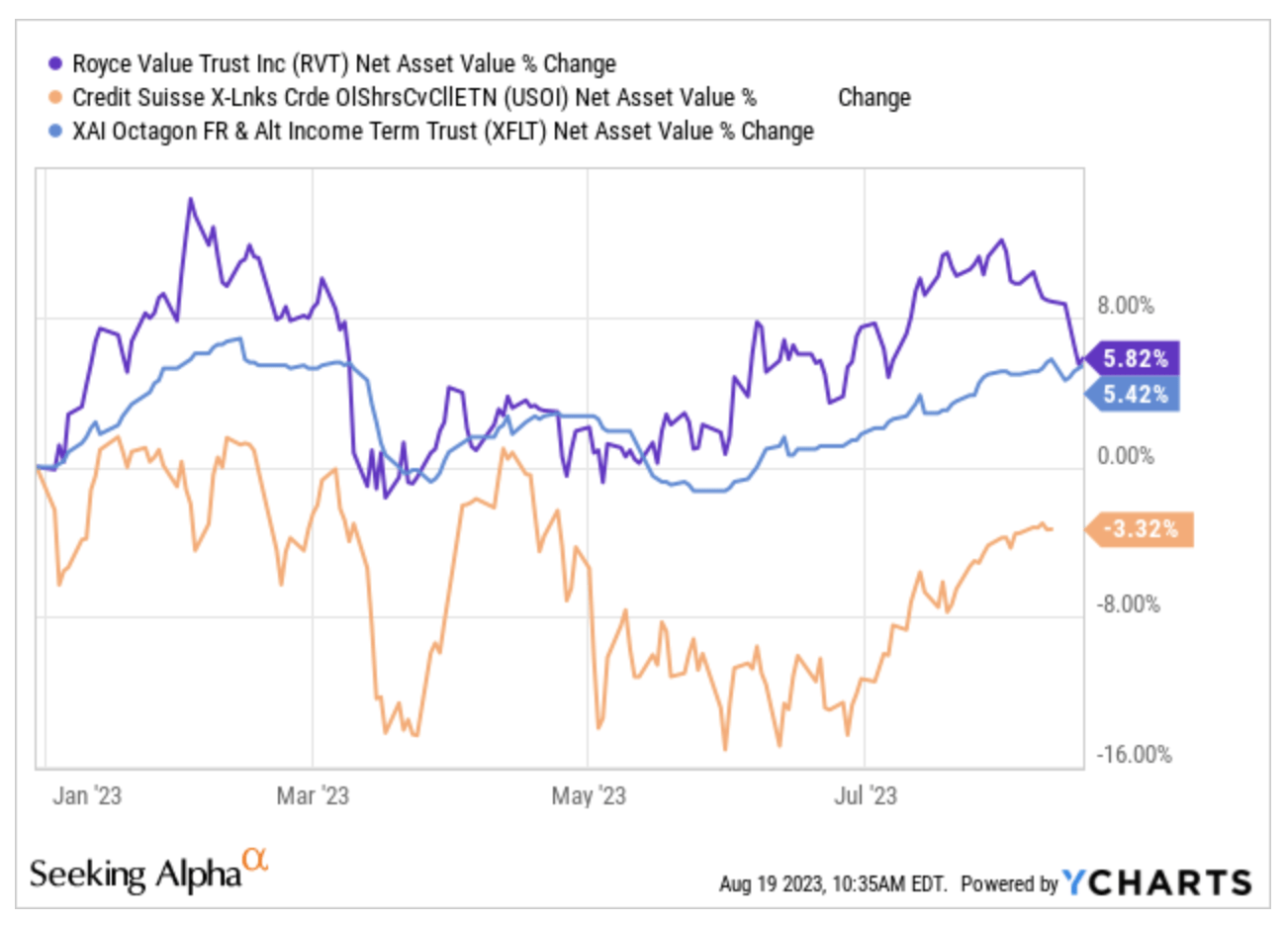

Masaccio Income Portfolio

{kind=link}

YCharts

RVT is a small-cap focused CEF managed by Royce Investment Partners that has been in the market for several decades. Its NAV shows a positive trend for 2023, recovering after losses in past years. A stable presence in my portfolio due to its largely positive performance since launch, although its recent distributions have hit record lows.

USOI is a Credit Suisse covered call ETN, whose performance shows a slight loss in 2023. This security is in my portfolio because of its peculiar dividend feature for me as an Italian, being able to offset with it my past losses. A few years ago I also had GLDI and SLVO, but at the moment I decided to limit the presence of ETNs in my portfolio to USOI alone, which is the most capitalized and traded of all three. Considering that its dividend is “tax free” for me because it helps me offset previous losses, I decided it may be worth keeping some shares in my portfolio.

XFLT is a CEF of XA Investments that invests in Collateralized Loan Obligations (CLOs) and shows a positive NAV performance in this 2023. Its excellent distribution and management reputation make it a “complementary” presence in my portfolio, increasing its diversification in an otherwise for me uncovered sector.

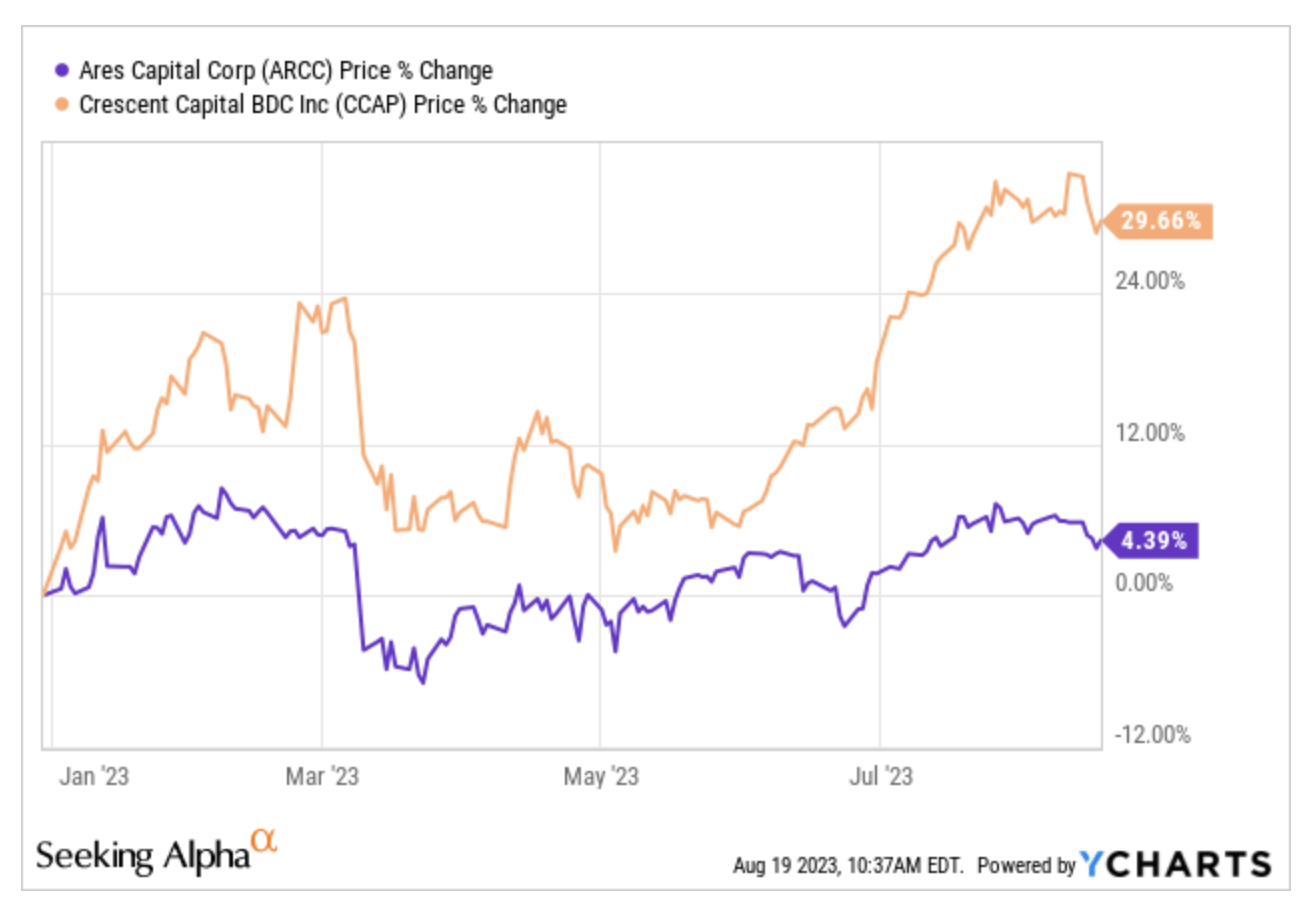

{kind=link}

YCharts

ARCC is one of the best Business Development Companies (BDCs) on the market, included in my portfolio because of its quality, revealed by its performance since launch and confirmed by the small progress also shown in 2023. Although tax inefficient for me because of how its dividends are taxed in Italy, it contributes significantly to total income. The chart shows the price trend, which quotes at a slight premium to NAV (+3.77%) according to Closed-End Fund Advisors.

The same holds for CCAP from the tax point of view, but I decided to put this BDC into my portfolio because of its prospects. Extremely positive performance for 2023 accompanied by a juicy distribution, so no intention to give up its contribution within my portfolio. The graph shows the price trend, which quotes at a steep discount to NAV (-15.37%) according to Closed-End Fund Advisors.

Bottom Line

Universally admired for the rigorous formal construction of his paintings, Piero della Francesca was a refined and influential intellectual who placed art at the service of the idea, as in a Mondrian rationalist canvas. His paintings reflect a geometric order that makes them resemble abstract representations, with lines, planes and volumes creating a harmonic rhythm that transforms each composition into a perfect mathematical construction. A modern, rational scientificity based on mathematical foundations.

Similarly, scientific investing means learning the mechanisms underlying financial markets to generate consistent profits over the long term. But the scientific approach cannot be separated from the study and knowledge of ourselves and our emotions. Our portfolios do not live by numbers alone, as Piero’s paintings are not just math.

Over the past two years, I have gotten to test my psychological resilience in the face of the barrage of stimuli that bombarded me from all sides, starting with the daily and pervasive recession pronouncements. Although not all the choices of my titles turned out to be optimal, I still believe that it has been worthwhile to stand firm in my positions and continue to have confidence in the decisions made a few years ago. There will be adjustments to be made in the future, but my long-term horizon does not put me in a hurry.

P.S. Starting with this article I would like to convert the usual report on my portfolio from monthly to quarterly. Thus, at SA’s pleasure, I plan to publish the next report at the end of this year, and from there on every quarter-end, possibly interspersing them with more general articles on CEFs, ETFs, and other investment tools, when the opportunity arises.

For further details see:

My 9% Income Portfolio - Nobody Is Perfect