MG:CC - My Dividend Growth Portfolio: Final 2023 Recap

2024-01-08 13:09:41 ET

Summary

- I cover all of my sales for the year and the reasoning behind each, as well as the purchases.

- I review the portfolio's goals, guidelines, and a brief history of the portfolio.

- Income exceeded my goals with an increase of 11.1% on the year, while the portfolio value is at an all-time high.

I still think back to why I became a dividend growth investor in the first place. After the crash in 2008-2009, I did some hard thinking about my investment goals. I realized that I had no clear understanding of my investing goals other than that I hoped not to have to work someday. But I didn't really know what it would take to do this.

Did I need a million dollars, five? Ten? More? What if I retired and another crash came the next year? What if I lived a long time? Would there be enough money? It became clear that saving until I retired was not a good plan for me.

For one thing, just hoping that my money doesn't run out in retirement gives me anxiety just thinking about it. For another, I am goal-oriented and need something to work towards to stay motivated. I needed a better way.

I did know two things for sure: First, I lived a good life and made plenty of money that paid my bills and had some left over, and second, I didn't want to work forever. It dawned on me that if I could replace the money from my job with passive income, I would be secure and free from worrying about whether I had saved enough to last. Hence, I became a dividend growth investor.

Something else happened to me during the market crash of 2008-2009. It's only in the last few years that I fully understand it, but it explains my draw to dividends. I'm a simple person. I grew up farming and am grounded in real things. Dividends are like that. They are real. They exist from earnings and cash flows; no hope, dreaming, bad press, irrational exuberance, or any other factor can change them.

On the other hand, stock prices have no ties to real things. Sure, I believe in mean reversion, that stocks will return to the norm over time. However, a stock price is tied to nothing but sentiment at any given time. In 2009, was Microsoft ( MSFT ) suddenly worth 60% less and Aflac ( AFL ) 85% less in a year? I will take dividends from actual earnings any day over emotions. No amount of love (or hate) for a company can fake dividends.

The end of 2023 marks the completion of 14 years as a dividend growth investor. And it's been a relatively smooth ride. Sure, I have made plenty of mistakes, but the journey has been pretty smooth overall. Compared to the gut-wrenching experiences of the dot com crash and the 2008-2009 great financial crises, dividend growth investing has been like traveling on a newly completed stretch of freeway with no traffic in sight!

Every day, I am content in knowing that my income is increasing, regardless of what the market brings. Of course, I remind myself that the last 14 years have been good for every type of investor; everyone has been a winner.

Goals

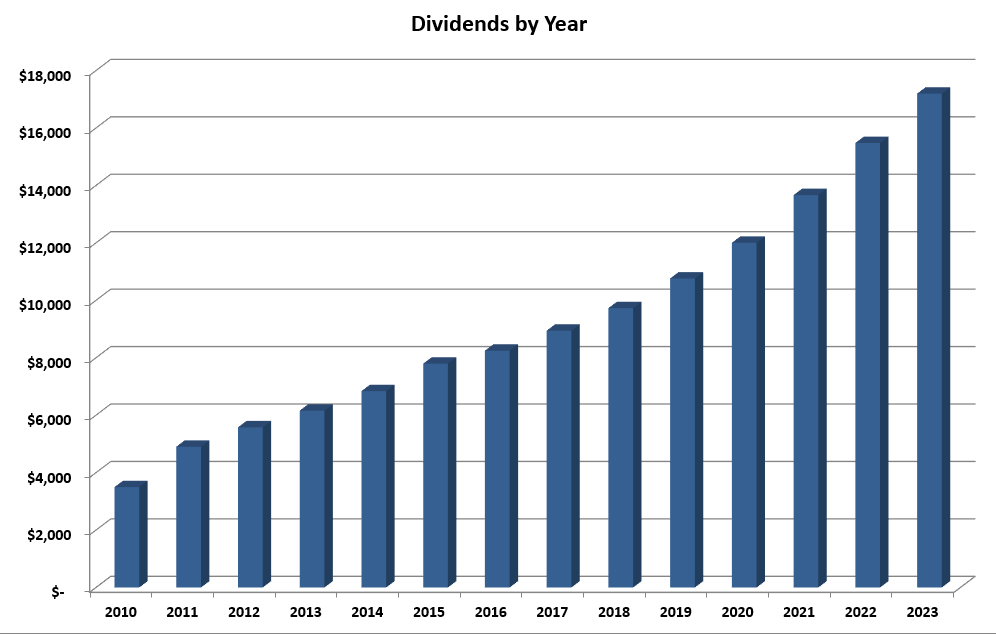

The portfolio goals are simple: Grow the income by 10% annually with dividends reinvested and 7% annually without reinvesting. This goal allows my income to double approximately every seven years while reinvesting and every ten years after I begin withdrawing the dividends. It's important to know that this portfolio has been closed to new capital since 2016. The graph below shows the steady progress of income growth.

Portfolio Guidelines

I use guidelines to achieve my goals rather than rules. Rules imply something hard and fast, whereas guidelines are flexible but give a general direction to follow. I keep these simple, as I have found that complexity adds time without any real benefit. These have evolved over the years, the most recent being the addition of selling covered calls in certain circumstances.

- Invest in companies from the Champions and Contenders list with at least 15 years of dividend growth.

- Look for companies with a 3% starting yield and the potential to maintain a 7% dividend growth for decades. The growth is critical as it's impossible to continue growing income at 7% without reinvesting unless companies raise distributions by at least that amount.

- Replace (or sell covered calls against) significantly overvalued positions if the opportunity exists to reduce risk and increase income. In practice, this usually means higher quality at a higher yield.

- I want to see flat to mild payout ratio creep. A payout ratio growing from 30% to 35% over ten years is acceptable. One that has gone from 30% to 60% is not. I want companies to grow the dividend with earnings, not by increasing the payout ratio.

- Unless it is well-diversified across industries, no single sector should account for more than 20% of the income. This burned me in 2016 when several energy companies cut dividends.

Again, these are just guidelines and are flexible to accommodate what makes sense to achieve my overall goals. I follow a few other items but don't see them as integral to my investing. Instead, these tend to be more personal preferences. They include avoiding foreign companies because I don't enjoy accounting for the taxes and FX rates causing fluctuating dividends.

Positions

At the end of the year, the portfolio is holding 44 positions, down one from last year. The table below shows the complete holdings, their relative size, and the percentage of income produced. A change from previous years is the inclusion of interest income from cash, as before 2023, it was negligible.

| Company |

| % of Portfolio |

| % of Income |

| Ameriprise ( AMP ) |

| 7.3% |

| 3.5% |

| Blackstone ( BX ) |

| 7.0% |

| 6.2% |

| Microsoft |

| 6.5% |

| 1.7% |

| Broadcom ( AVGO ) |

| 4.6% |

| 2.8% |

| Visa ( V ) |

| 4.4% |

| 1.1% |

| AbbVie ( ABBV ) |

| 4.1% |

| 5.3% |

| Philip Morris ( PM ) |

| 4.0% |

| 7.1% |

| Apple ( AAPL ) |

| 4.0% |

| 0.7% |

| Lockheed Martin ( LMT ) |

| 3.8% |

| 3.4% |

| Texas Instruments ( TXN ) |

| 3.6% |

| 3.6% |

| Altria ( MO ) |

| 3.5% |

| 10.9% |

| Schwab Value Advantage Money Fund ( SWVXX ) |

| 3.2% |

| 4.0% |

| Cincinnati Financial ( CINF ) |

| 2.9% |

| 2.7% |

| Enterprise Products Partners ( EPD ) |

| 2.7% |

| 6.9% |

| BlackRock ( BLK ) |

| 2.5% |

| 2.1% |

| Aflac |

| 2.5% |

| 1.9% |

| Medtronic ( MDT ) |

| 2.4% |

| 2.6% |

| Phillips 66 ( PSX ) |

| 2.0% |

| 2.0% |

| PepsiCo ( PEP ) |

| 1.9% |

| 1.9% |

| MSA Safety ( MSA ) |

| 1.9% |

| 0.7% |

| Duke Energy ( DUK ) |

| 1.8% |

| 2.5% |

| Johnson & Johnson ( JNJ ) |

| 1.7% |

| 1.7% |

| Starbucks ( SBUX ) |

| 1.6% |

| 1.2% |

| Home Depot ( HD ) |

| 1.4% |

| 1.2% |

| A.O. Smith Corp ( AOS ) |

| 1.4% |

| 0.7% |

| CME Group ( CME ) |

| 1.3% |

| 2.0% |

| Automatic Data Processing ( ADP ) |

| 1.3% |

| 1.0% |

| Abbott Laboratories ( ABT ) |

| 1.3% |

| 0.8% |

| Simon Property Group ( SPG ) |

| 1.1% |

| 1.9% |

| CVS Healthcare (CVS) |

| 1.1% |

| 1.2% |

| Omega Healthcare Investors ( OHI ) |

| 1.0% |

| 2.8% |

| Prudential Financial ( PRU ) |

| 1.0% |

| 1.6% |

| Treasury Bonds |

| 1.0% |

| 1.4% |

| J.M. Smucker ( SJM ) |

| 1.0% |

| 1.1% |

| Intercontinental Exchange ( ICE ) |

| 1.0% |

| 0.4% |

| Best Buy ( BBY ) |

| 0.9% |

| 1.3% |

| Fortune Brands Innovations ( FBIN ) |

| 0.9% |

| 0.4% |

| Ladder Capital ( LADR ) |

| 0.8% |

| 1.9% |

| Unilever ( UL ) |

| 0.8% |

| 1.0% |

| Realty Income ( O ) |

| 0.5% |

| 0.9% |

| Kroger ( KR ) |

| 0.5% |

| 0.4% |

| National Retail Properties ( NNN ) |

| 0.4% |

| 0.7% |

| Snap-on ( SNA ) |

| 0.4% |

| 0.3% |

| Honeywell ( HON ) |

| 0.4% |

| 0.3% |

| Diamond Hill Investment Group ( DHIL ) |

| 0.3% |

| 0.3% |

2023 Income and Performance

For 2023, the income increased to $17,195, an increase of 11.1%. This meets my 10% goal, although it was smaller than the previous two years' increases of over 13%. The chart below shows how the income has grown over time. I'm thrilled with this result, given that the Blackstone dividend reduction was a 3% drag on the income.

{kind=link}

The portfolio hit an all-time high value in July and again in November, with new records set almost daily at the year's end. Even though it is near an all-time high, the portfolio was only up 18.5% on the year, significantly trailing the S&P 500 (SP500). While I have no goals regarding the portfolio's market value, I report it as many readers ask. Keep in mind, however, that my goals are entirely income-oriented.

Sales for the year / Replacements

There are three reasons why I sell companies:

- An acquisition offer - I almost always sell on an offer because of the chance the acquisition will fall through, and the company's price will fall back down.

- Overvaluation - If I feel a company is overvalued to the point that similar quality companies at better yields can be found, I will sell or trim the position. Often, I will do this through the use of covered calls.

- Mixed factors - As dividend growth can be chunky, I can accept a few years of low dividend growth. Sometimes, I allow micro-positions to exist (positions at less than half a percent) when I'm waiting for valuations to come down so I can buy more shares. I even tolerate a few years of poor estimates for a quality company if I'm convinced about long-term prospects. But when there is a combination of these factors, sometimes, it's easier to eliminate the position.

I often basket purchases with the proceeds from a sale to spread risk around, particularly if it was a high-yield position.

Last year, there were three position sales in the portfolio and no trims. However, a couple of low-yield positions need to step up the dividend growth for 2024 or risk being put on the chopping block. These are MSA Safety and Fortune Brand Innovation. Below, I discuss each sale and the redistribution of the funds generated.

Intel ( INTC )

When Intel announced a dividend cut in February, I made the knee-jerk reaction to sell. I admit to getting caught up in the negative articles and should have taken a step back. As always happens, when a stock is going up, analysts can't have too much good to say about a company, and when the price is dropping, they can't be overly pessimistic. I still needed to eliminate Intel from the portfolio, but had I taken more time, I probably would have done better on my shares.

INTC was added to the portfolio in 2012 at $24.41 per share. The final selling closeout price averaged $26.35 for the shares sold after the cut. Fortunately, I had the sense to swap 20% of my position in 2018 for Texas Instruments. At the time, Intel was trading above $48 and TXN was below $95. Net of all the buys and sales plus dividends, I recovered 170% of my purchase price (including the sale in 2018). While not a great return for the time, I'm confident the reinvested dividends did much better.

Proceeds from the sale were redistributed into a basket of existing holdings. However, I was unable to replace the lost income fully. Today, INTC is up nearly 70% from my average sales price, so this basket has underperformed as higher yields were purchased to try and offset the income. The list of shares purchased is shown below:

| Company |

| Shares |

| CME Group |

| 2 |

| Realty Income |

| 4 |

| Enterprise Products Partners |

| 34 |

| Home Depot |

| 2 |

| CVS |

| 12 |

| PepsiCo |

| 2 |

| Blackstone Group |

| 2 |

| Prudential Financial |

| 2 |

Cardinal Health ( CAH )

Entering the year, I expected a decent dividend raise from Cardinal Health with the opioid lawsuits wrapping up. Unfortunately, they only announced another 1% increase. So, I took advantage of my gains and the record-high prices to swap into faster dividend companies. Earnings are expected to pick up for the company, and dividend growth might as well, but with the low yield, it was an easy choice to make some swaps.

I used the funds to add to my Home Depot position at $286.34, CME at $180.34, and Automatic Data Processing at $209.34. I originally intended to add more Broadcom, but this was right when the AI hype hit. Even though Cardinal Health has increased in price since the sale, the replacements have also done well.

CAH was added to the portfolio in 2019 and never grew beyond a micro-position at less than 0.5% of the portfolio. The position was held for almost exactly four years and recouped 190% of the purchase price.

Walgreens Boots Alliance ( WBA )

Walgreens has been one of my biggest mistakes, and I made it twice! Initially purchased in 2019, I sold it in December 2022 as tax loss harvesting and repurchased it after the wash date in January 2023. This was great at the time as I repurchased at nearly $5 a share less than when I sold. Of course, then the stock proceeded to fall 40% throughout 2022.

I started looking for an exit when no dividend increase was announced. As I noted in my August update , the earnings for WBA always look brighter just into the future. It has been this way for years and it never seems to materialize. I took advantage of the bounce in price in mid-December to close the position.

All in, net of purchases, sales, and dividends, the company lost me $15 per share over about five years. Fortunately, WBA was never more than a micro-position in the portfolio. The worst part was I had a chance to get out when I sold in 2022 and move on. I don't think I even considered other options, as the rosy analyst earnings projections blinded me. Another lesson for my book, I guess.

The funds haven't been reinvested yet. I intend to put a chunk into my annual EPD purchase and start a new high-yield position, albeit a small one. Right now, I am leaning towards Ares Capital ( ARCC ) or Blackstone Secured Lending Fund ( BXSL ). These moves will more than replace the lost income.

Purchases for the year

The purchases listed above as replacements from sales are generally made with the intent to maintain the quality and total income of the portfolio. This section covers all the regular purchases for the year, which are made based on valuation.

Over the last few years, cash was almost immediately put to work. 2023 was different, as the increase in interest rates afforded time to sit and wait. At the beginning of the year, I used short-term CDs, but it was soon apparent that money market funds offered "close enough" yields with more flexibility.

I did purchase some treasury bonds at the end of October when the 10-year flirted with the 5% mark. I intended to add more regularly; however, I am taking a wait-and-see approach, with the yield falling well below this mark.

The table below outlines the regular purchases made during the year and the average price paid. Kroger is a new position, while all the others were additions to existing positions.

| Symbol |

| Shares |

| Avg Price |

| AOS |

| 1 |

| 60.34 |

| BBY |

| 2 |

| 69.91 |

| CME |

| 3 |

| 180.1 |

| CVS |

| 19 |

| 69.35 |

| HD |

| 2 |

| 285.03 |

| KR |

| 60 |

| 43.38 |

| NNN |

| 4 |

| 46.99 |

| O |

| 1 |

| 48.65 |

| PRU |

| 1 |

| 78.77 |

| TXN |

| 7 |

| 161.01 |

| V |

| 1 |

| 217.47 |

Other Odds and Ends from 2022

I do have other portfolios. Some have overlapping positions with this portfolio, but all are dividend growth portfolios. Altogether, the portfolios contain about 75 individual positions and five ETFs.

I have decided to put more emphasis on a smaller number of select companies in the future. For this reason, quite a few positions were eliminated from my other portfolios, as I had often been buying whatever looked like a good bargain.

During 2022, I closed out of positions in Cardinal Health, Intel, and WBA for the above reasons. Spirit Realty ( SRC ) was sold when it was announced that it would be acquired. Brookfield Asset Management ( BAM ) and Brookfield Corporation ( BN ) were removed as they were small positions.

I sold several companies because they didn't meet my quality or dividend growth expectations: Air Lease ( AL ), Colgate-Palmolive ( CL ), Cisco ( CSCO ), IBM ( IBM ), Micron ( MU ), Rio Tinto ( RIO ), Suncor ( SU ), Tyson ( TSN ), 3M Company ( MMM ), and Magna International ( MGA ). A couple of these were opportunistic purchases at the time and had served their purpose.

New positions were established in Nexstar Media ( NXST ), Fidelity National Information Services ( FIS ), Global Payments ( GPN ), United Parcel Service ( UPS ), Target ( TGT ), U.S. Bancorp ( USB ), and The Toronto-Dominion Bank ( TD ). Nexstar is a speculative investment, but it was yielding 4% at the time, and I believed the risk/reward was worth it. Both banks were purchased during the mini-bank crisis early in the year and have appreciated nicely. I'm not a huge fan of banks, but the historically high yields they offered at the time made them attractive.

I'm happy that my portfolios ended 2023 well above their previous all-time highs. While none beat the S&P 500 for the year, the incomes increased above my expectations.

Final Thoughts

Last year was a bit of a roller coaster. The year began with everyone expecting a recession, myself included and ended up with one of the best market years in history. Of course, many thought the correction at the end of October was the beginning of the end, only to see the market rocket up by nearly 20% into the new year.

Perhaps now that nearly all the bears have been cleared out, we can finally have a recession. However, it would be unusual for a down market in an election year, so there is that.

I end the year with this portfolio holding nearly a year's worth of dividends as cash. That skews my income a bit, as cash is yielding better than 5%, and my typical stock purchase will yield less than 3%. For the time being, however, I will continue to reinvest only 25% of collected dividends and be patient with the right opportunities to move more money into the market.

My full portfolio review and 2024 look ahead will be coming out in the upcoming week. I always enjoy taking the time to look at how the portfolio has evolved over the years. It's also a time to contemplate how I want to shape it going forward. I'm excited to see what the new year brings, and happy 2024 investing to everyone in the Seeking Alpha community!

For further details see:

My Dividend Growth Portfolio: Final 2023 Recap