SEIX - My Fixed Income Portfolio Yields 7% And Is Positioned To Outperform The Index In 2024

2023-12-28 04:00:34 ET

Summary

- My 2024 fixed income portfolio aims to achieve current income in the 6-8% p.a. range and has specific allocations for alternatives, non-US credit, and below-investment grade credit.

- I am investing along three key themes: The Fed's pivot, credit risk expectations, and developing market premium.

- Core quality bonds, including iShares iBoxx $ Investment Grade Corporate Bond ETF, and DFA California Municipal Real Return Portfolio Institutional Class are key holdings in the portfolio.

Introduction

As a new writer for Seeking Alpha this year, I wanted to cap off 2023 with my thoughts on how I am positioning my income portfolio to tackle next year. That way, next December, I can revisit this and describe how I'm making changes moving forward.

Internally, I've named this portfolio the "Diversified Income Fund," or "DIF" for short. For those unaware, this is a reference to gamer slang . Throughout this article, I will refer to the portfolio as "DIF" as well.

Themes

The portfolio's allocation is built around three key themes:

- Taking advantage of the Fed's dovish turn on "peak rates," which I wrote about here. I am buying fixed rate bonds again, as discussed in that article in more detail.

- There is now a divergence between the market's expectation of credit risk and economic indicators. I see asymmetric upside in lower and unrated credit, further down in the "corporate stack" and have added to allocations of BBB-B CLOs and senior loans.

- Emerging and developing market bonds are currently offering incredibly compelling yields for the risk involved, but I prefer active management in this sector to cover my ignorance of ex-US macroeconomics.

Goals

DIF needs to accomplish the following objectives that I've set for it internally:

Note: These are set for my own personal situation and may not be suitable for you in particular.

- Achieves current income in the 6-8% p.a. range

- Has an overall duration of ?7yr

- Presents favorable risk/return metrics and alpha when compared to the Aggregate Bond Index ( AGG ) & the 7-10yr US Treasury Index ( IEF )

- Is composed primarily of US bonds and fixed income instruments or derivatives, but may include up to the following allocations:

- 25% Non-US Credit

- 25% Below-IG Credit

- 15% Alternative Strategies

- Has an annualized standard deviation ("stdev") of ?10%, & a beta of ?0.5

The Portfolio

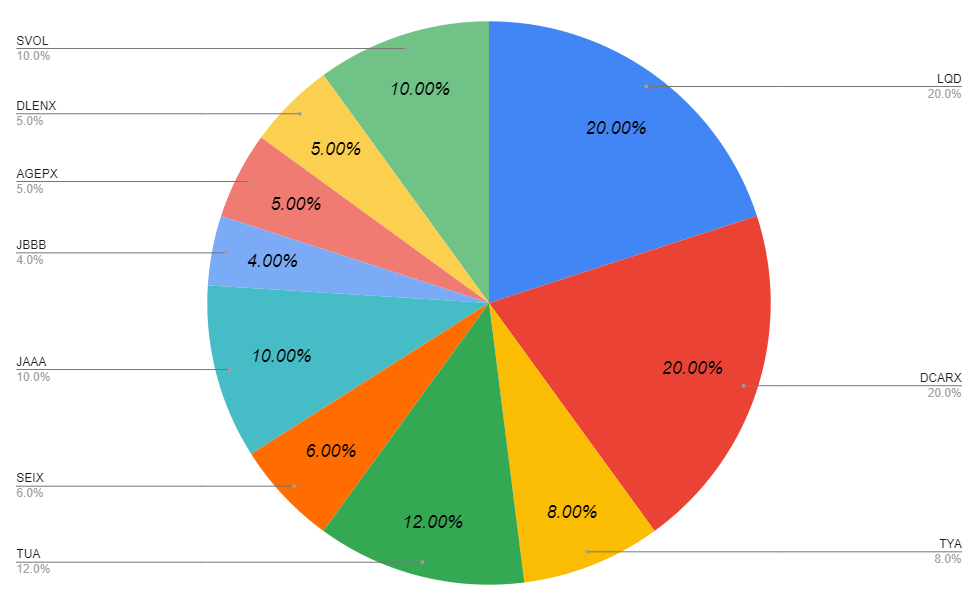

Without further ado,

| Ticker |

| Name |

| Weight |

| LQD |

| iShares iBoxx $ Inv Grade Corporate Bond ETF |

| 20% |

| DCARX |

| DFA California Municipal Real Return Portfolio Institutional Class |

| 20% |

| TYA |

| Simplify Intermediate Term Treasury Futures Strategy ETF |

| 8% |

| TUA |

| Simplify Short Term Treasury Futures Strategy ETF |

| 12% |

| SEIX |

| Virtus Seix Senior Loan ETF |

| 6% |

| JAAA |

| Janus Henderson AAA CLO ETF |

| 10% |

| JBBB |

| Janus Henderson B-BBB CLO ETF |

| 4% |

| AGEPX |

| American Beacon Developing World Income Fund-Investor Class |

| 5% |

| DLENX |

| DoubleLine Emerging Markets Fixed Income Fund Class N |

| 5% |

| SVOL |

| Simplify Volatility Premium ETF |

| 10% |

I've ordered the funds by theme instead of by weight, but I will be covering them in order down the list from top to bottom, or clockwise around the chart in Figure 1.

{kind=link}

| Ticker |

| Weight |

| Yield (30d) |

| ER |

| Dur. (YR) |

| Stdev |

| Beta |

| R** |

| LQD |

| 20% |

| 5.59% |

| 0.14% |

| 8.32 |

| 12.52% |

| 0.24 |

| 0.99 |

| DCARX |

| 20% |

| 3.21% |

| 0.26% |

| 1.64 |

| 2.61% |

| 0.04 |

| 0.77 |

| TYA |

| 8% |

| 4.95% |

| 0.17% |

| 16.15 |

| 25.09% |

| 0.11 |

| 0.95 |

| TUA |

| 12% |

| 5.08% |

| 0.16% |

| 8.30 |

| 13.16% |

| -0.07 |

| 0.78 |

| SEIX |

| 6% |

| 13.90% |

| 0.62% |

| 0.13 |

| 3.54% |

| 0.05 |

| 0.37 |

| JAAA |

| 10% |

| 6.80% |

| 0.22% |

| 0.25 |

| 1.57% |

| -0.01 |

| 0.08 |

| JBBB |

| 4% |

| 8.77% |

| 0.50% |

| 0.19 |

| 6.63% |

| -0.01 |

| 0.26 |

| AGEPX |

| 5% |

| 13.72% |

| 1.45% |

| 3.30 |

| 6.92% |

| 0.09 |

| 0.50 |

| DLENX |

| 5% |

| 7.81% |

| 1.15% |

| 4.96 |

| 7.68% |

| 0.10 |

| 0.93 |

| SVOL |

| 10% |

| 15.88%* |

| 1.16% |

| 0.15 |

| 7.80% |

| 0.45 |

| 0.55 |

| Portfolio |

| 100% |

| 7.29% |

| 0.44% |

| 4.75YR |

| 8.76% |

| 0.11 |

| 1.00 |

Intra-portfolio correlation ((IPC)): 0.36

*30-day Distribution yield used here since some income is "return of capital" and is not included in 30-day SEC yields.

**Asset correlation to the whole portfolio.

Core Quality Bonds - LQD & DCARX

My stance on core bond holdings has been and continues to be: investment grade and short-to-mid-duration is king.

The core holdings here consist of two funds, and they make up 40% of the portfolio.

iShares iBoxx $ Inv Grade Corporate Bond ETF ( LQD )

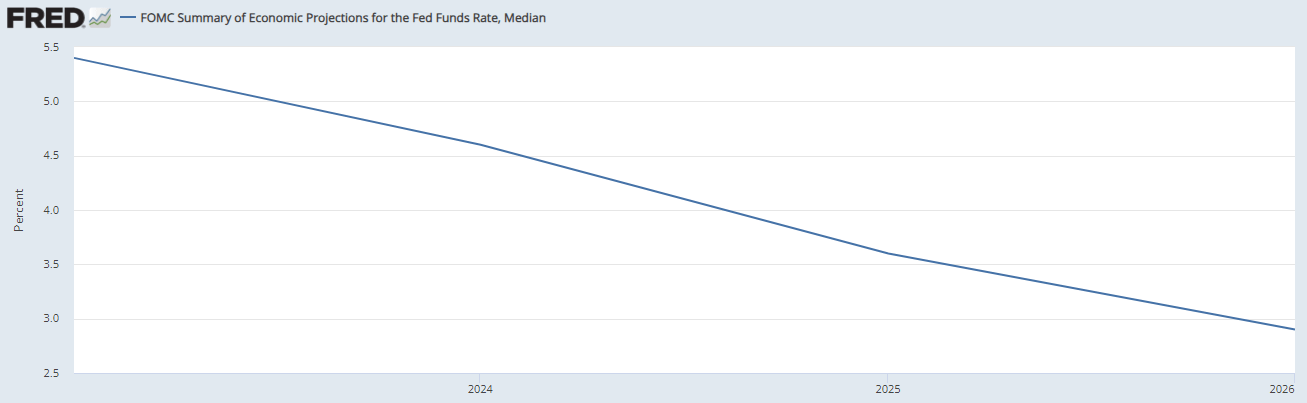

In my recent article on the Fed's newest guidance on rate cuts through next year into 2026, I wrote that I am bullish on corporate floating and fixed-rate bonds .

LQD is poised for a recovery back to its former highs once rates normalize, and all the while, it will be paying heavy dividends.

We're Getting Our Cake and Eating it Too

With a forward yield of 5.59%, corporate bonds are paying well and provide some upside that shorter-term investments paying similar rates do not. This is the gift of duration once you've hit the "rate ceiling," so to speak.

For every 1% in rate cuts, we should see an 8% rise in LQD's price. The Fed intends to cut about that much next year , and so we could be looking at a potential to receive a 5% annual dividend and up to 10% in price upside in 2024.

We're in the right place at the right time for corporate bonds. This is my highest conviction position and one of the largest changes I made to the portfolio asset-value wise from 2022, as this capital had previously been in a short duration treasury fund, SGOV, which I wrote about recently here .

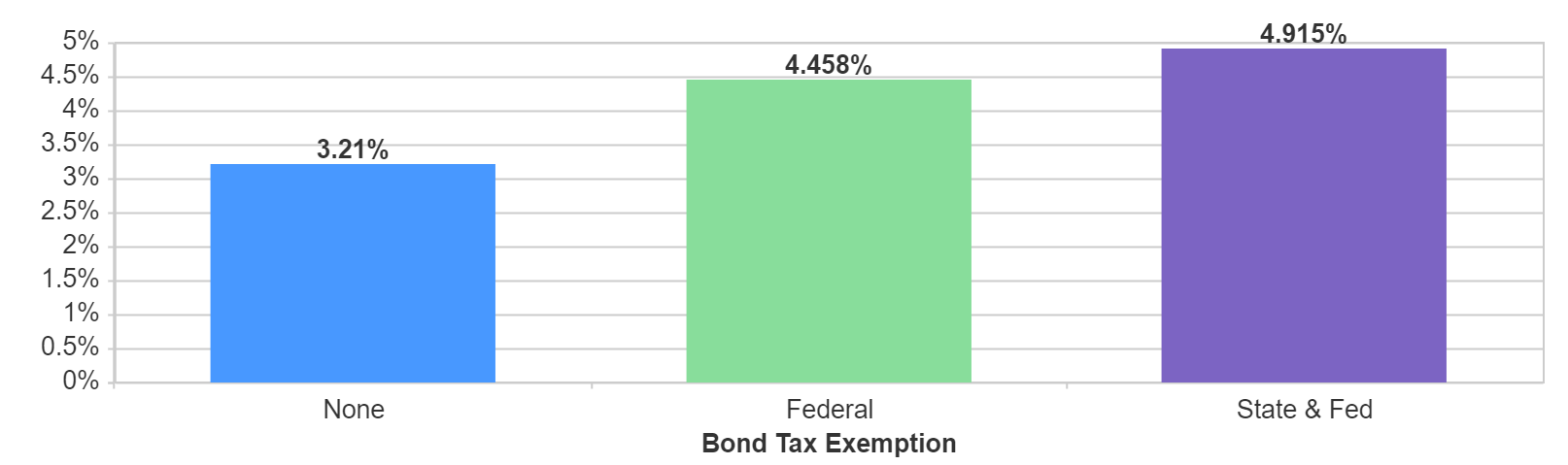

DFA California Municipal Real Return Portfolio Institutional Class ( DCARX )

As a Californian, it's easy for me to like municipal bonds.

They may still make sense for out-of-state investors, depending on your tax situation.

The fund is set to have a yield of 3.21%, the tax-exemptions mean in-state residents keep all of it. This raises the "effective yield" to 4.458% for out-of-state investors and 4.915% for in-state investors for my particular tax bracket. Figure yours out here .

{kind=link}

DCARX is low risk and aims to provide a solid core exposure that keeps our duration and volatility low while providing inflation-beating returns at the minimum. I prefer this strategy to TIPS for its tax efficiency and lower reliance on CPI as a means of measuring inflation.

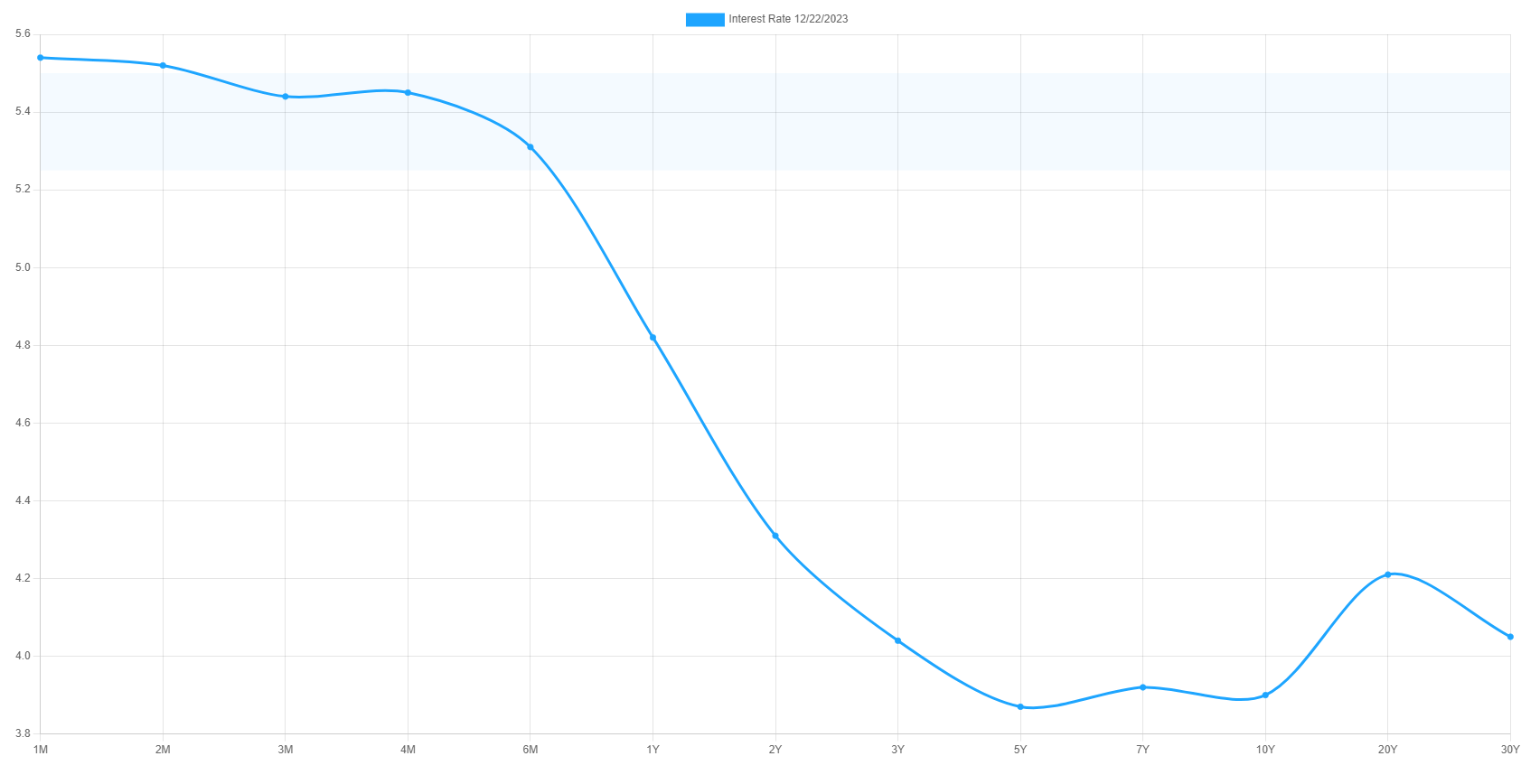

A Bet on the Curve Reverting - TYA & TUA

The yield curve is still very steep, just as much as it was when I first wrote about how to play the inversion back in October .

{kind=link}

When the market stops pricing in recession and the "higher for longer" narrative comes to an end, this curve will revert to its " typical " shape when the bond market is not pricing in a potential recession.

This should happen, all else being equal, over the next three years.

{kind=link}

As this happens, we will want to be positioned in longer duration bonds. However, as we established in Figure 7, they don't pay nearly as well as shorter duration bonds.

Simplify offers a solution. TYA and TUA are leveraged funds, using treasury futures to increase their exposure to short-term bonds up to 3x-5x times, mimicking the return profile of longer duration bonds.

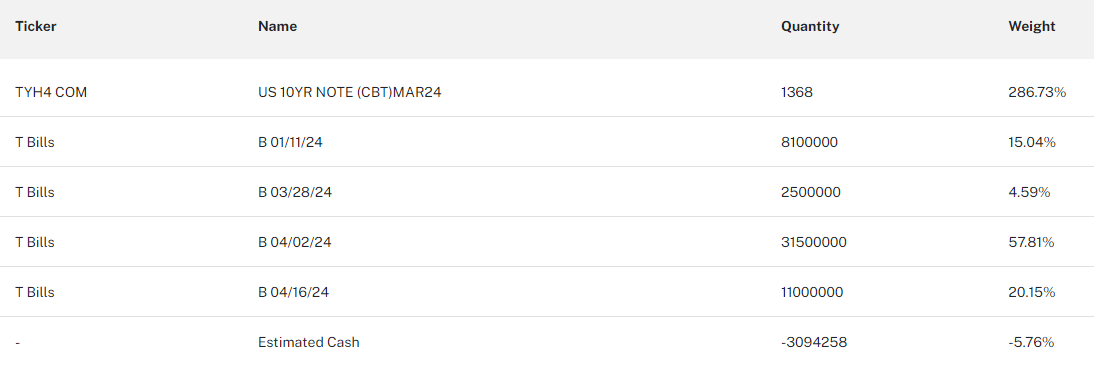

Simplify Intermediate Term Treasury Futures Strategy ETF ( TYA )

Via Simplify, who says it better than I can:

The Simplify Intermediate Term Treasury Futures Strategy ETF ((TYA)) seeks to provide total return, before fees and expenses, that matches or outperforms the performance of the ICE US Treasury 20+ Year Index on a calendar quarter basis. The Fund does not seek to achieve its stated investment objective over a period of time different than a full calendar quarter. The fund looks to target the duration of the ICE 20+ Year US Treasury Index by investing in Treasury futures in the intermediate portion of the curve using 10-Year US Treasury futures contracts. The fund is designed to provide significant duration from only a modest capital allocation while simultaneously attempting to harvest yield curve efficiencies from the belly of the curve. The fund can be used as a replacement for less efficient long duration holdings, as a means of increasing capital efficiency of intermediate duration portfolio allocations, or as a building block within innovative portfolio solutions such as risk parity.

We can consider this position exposure to 100% T-Bills and 300% 10yr Treasury note with some carry cost for the leverage. This will offer us the yield of the 10yr note and T-bills (minus LIBOR-ish, futures carry is complicated) and the duration of the 20yr bond.

{kind=link}

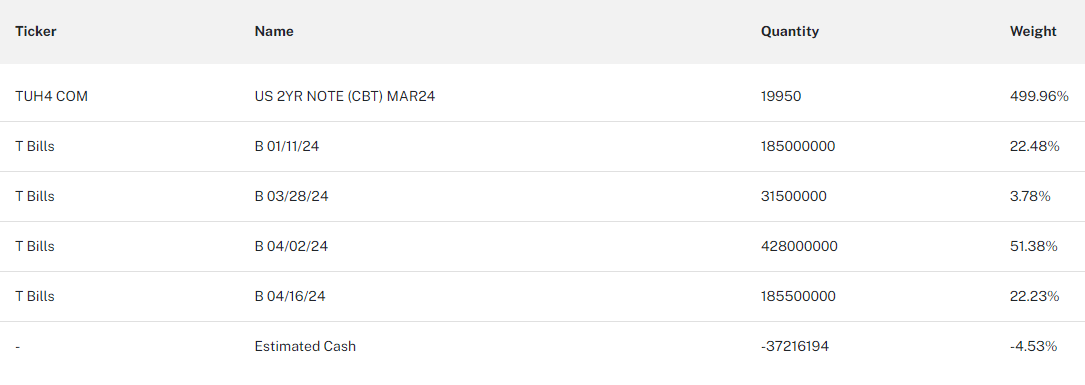

Simplify Short Term Treasury Futures Strategy ETF ( TUA )

Similarly, TUA uses the same strategy but with the 2yr note. This gives us 500% exposure to the 2yr note and targets the duration of the 10yr UST.

{kind=link}

Since both of these funds have already taken a hefty beating already, they are presenting a great time to buy and ride the wave back up.

TYA and TUA are also new additions to the portfolio that I am adding to currently.

The "Corporate Stack"

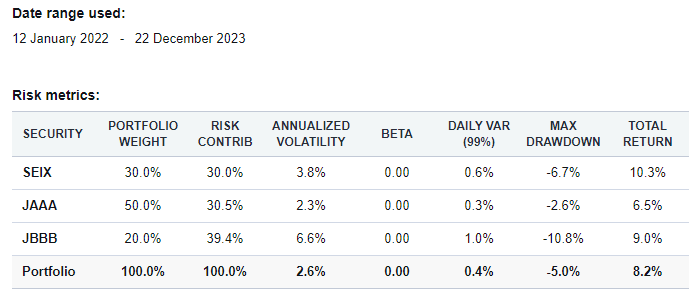

Bank Loans & CLOs - SEIX , JAAA , & JBBB

I won't cover this much here because I have already written about this topic before. You can find why I rate JAAA and JBBB a strong buy here .

Instead, in this column, I want to explain what I meant earlier by "there is now a divergence between the market's expectation of credit risk and economic indicators," in my themes section.

Currently, we are seeing an exceptional default rate priced into lower credit rating CLOs.

Figure 12 (Van Eck)

The dislocation between these spreads and the indicators of business success has caught my attention, and I think that offering 20% of my portfolio to this sector gives us a better opportunity than the market is expecting.

{kind=link}

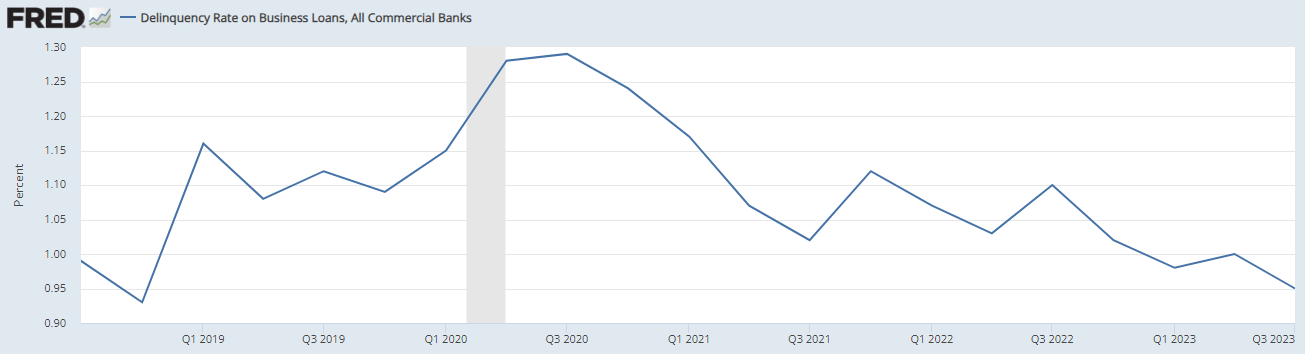

Delinquency rates for business loans are back at their 2019 lows, giving us a clear indicator that businesses are not being hit as hard as might have been expected a few months ago.

{kind=link}

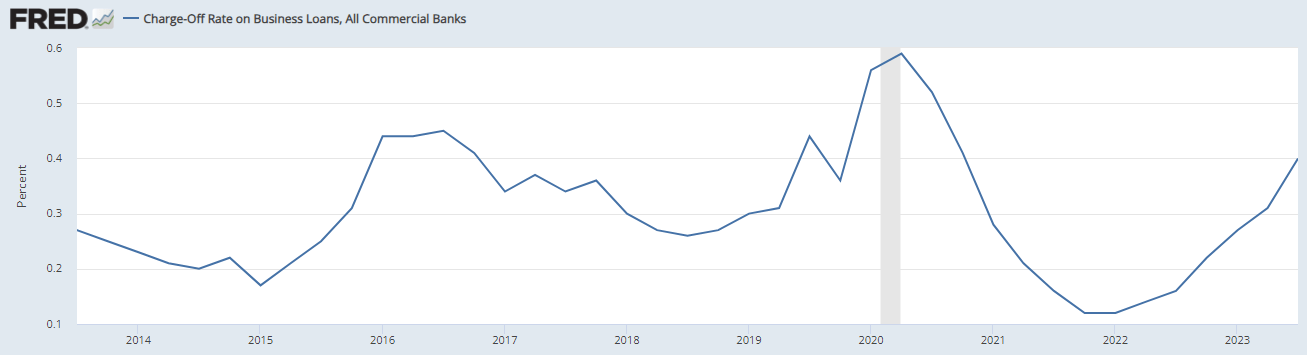

Charge-off rates are higher than the average for this year, which could be a cyclical effect that will level out in the coming months, but recent lower-lows in charge-off rates last year are a good sign of business health.

It is also important to note that some of this rise in charge-offs is due to even riskier debt strategies like "Manco Loans" and "NAV Financing" that are excluded from the funds I'm presenting.

This indicator should be watched carefully and is a primary reason why these three are held in the weights I have them. They are weighted roughly into risk-parity, meaning that they all contribute the same amount of risk to the position relative to their weight. This is why I overweight SEIX, which holds first and second lien loans, and JAAA, which holds investment-grade tranches compared to the non-investment grade JBBB, which only occupied 4% of the overall portfolio.

{kind=link}

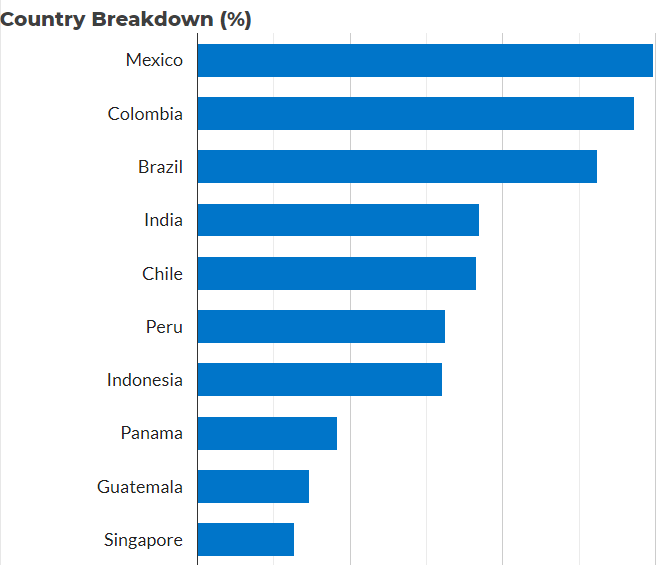

Emerging and Developed Markets - AGEPX & DLENX

Ex-US debt occupies very little space of the allowed 25% allocation. For now, I'm keeping the allocation at 10% on fears of global chaos, such as the current ongoing conflicts in Ukraine and Israel .

Boiling tensions over the South China Sea and Taiwanese sovereignty also stand a specter in geopolitics currently, which gives me pause when I consider investments in these regions.

To this end, I prefer my ex-US exposure to be actively managed so that the managers can screen out corporate and sovereign issuers that have too much exposure to geopolitical and macroeconomic risk factors that I'm not aware of.

American Beacon Developing World Income Fund-Investor Class ( AGEPX )

This fund invests in bonds from frontier markets, countries in the earliest stages of economic development. This is a market that requires a deep level of expertise in, which I do not have as an analyst who primarily follows the US.

From American Beacon Funds:

The Fund is sub-advised by two complementary fixed-income managers that invest as follows:

abrdn: Bottom-up investment process that applies fundamental research to select countries and corporate issuers.

Global Evolution: Top-down investment process that focuses on macroeconomic and political risk, as well as country-specific risk.

Here are their top 10 holdings. They aim to invest in 45-50 countries at a time.

Figure 16 (American Beacon Funds)

It is funny to think that I have a credit card with a lower interest rate than several of the bonds held by this fund.

DoubleLine Emerging Markets Fixed Income Fund Class N ( DLENX )

DoubleLine is a value-oriented investment management firm and this fund is no different from their usual philosophy.

{kind=link}

For the other half of our total 10% allocation to emerging and developing markets, I have chosen to diversify management. They invest in a different level of development than American Beacon, so it provides a more global rounding to the portfolio.

{kind=link}

Yields that Keep on Giving

Emerging market issuers have to pay steep rates to compete with safer bonds, and this is a trend that isn't likely to go away soon.

Alternative: Volatility Premium ((SVOL))

I've written extensively about the Simplify Volatility Premium ETF ( SVOL ) and recommend you check out my initial coverage of the fund here , where I explain how it produces income and does the fund justice compared to this summary.

Currently, I have SVOL rated as a hold, but I am still holding onto 10% of the portfolio set in this strategy. That capital has 100% exposure to T-Bills and 20-30% exposure to being short the VIX, plus futures carry.

All of that to say, it has been holding to a fairly tight price band and has had a total return that has outpaced the S&P 500 since its inception and kept pace with it this year.

You can check out my most recent covered where I downgraded SVOL to a hold here .

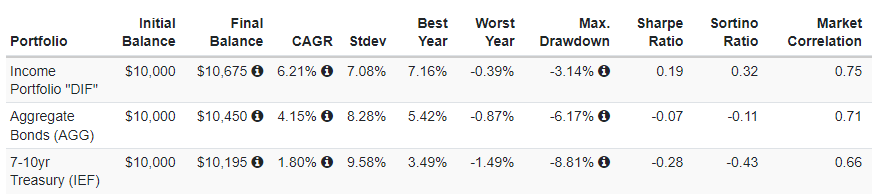

Performance

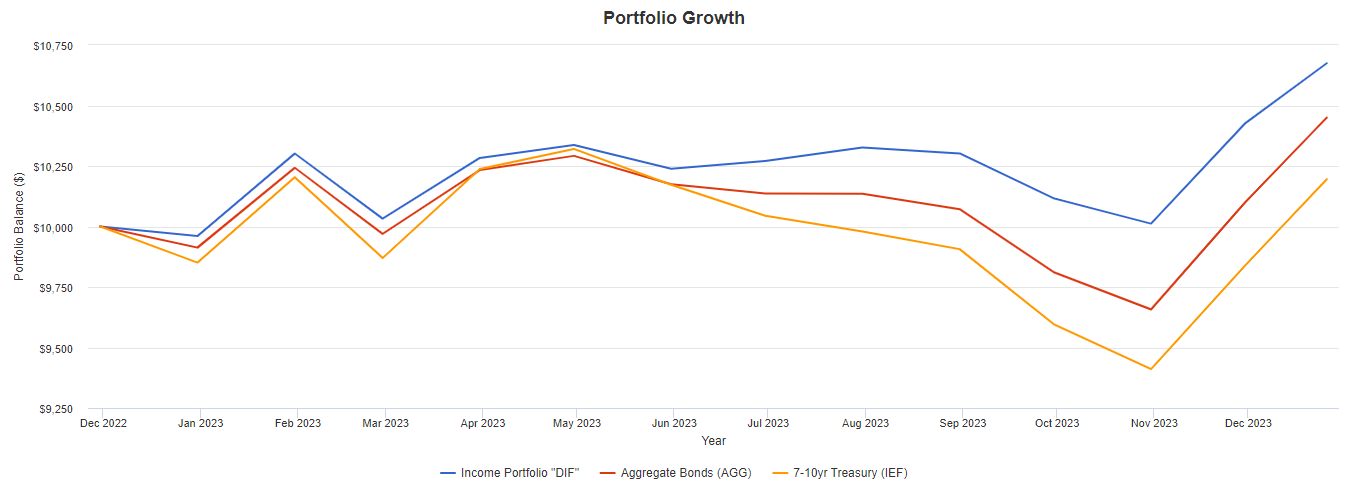

After all that, let's see how this thing actually performs. We're limited to backtesting only a year, so we can consider this a review of the 2022 performance, more or less.

Here are the results from 12/1/22 - 12/27/23 for this portfolio's total return against the total return of AGG and IEF, my two benchmarks.

{kind=link}

Keep in mind that this also doesn't include any of the tax benefits that some components of DIF and IEF would provide in the real world.

{kind=link}

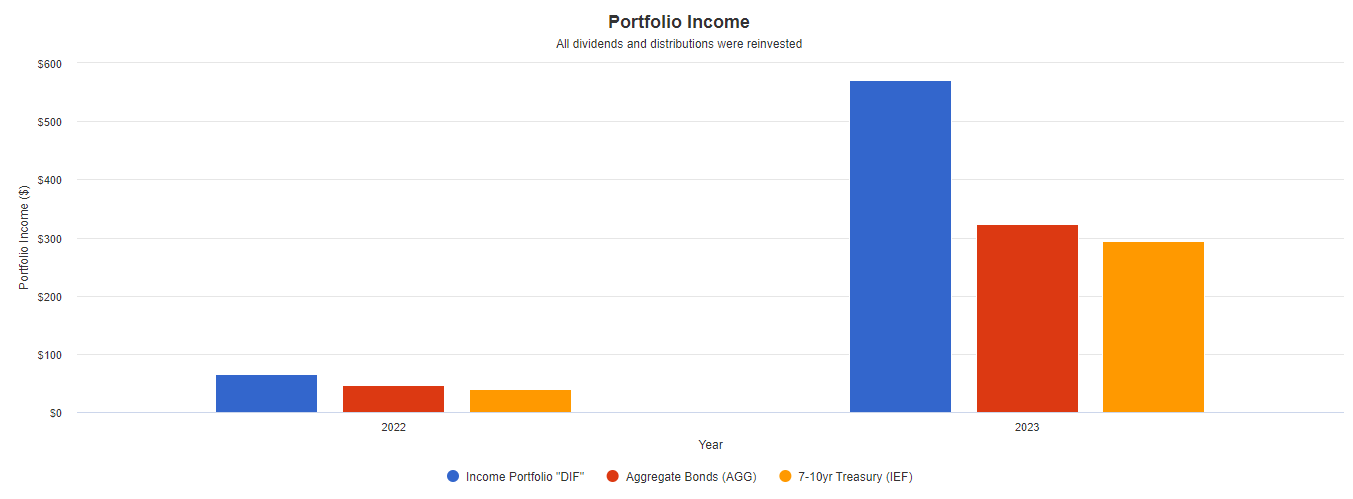

Some of that return is income, shown below.

{kind=link}

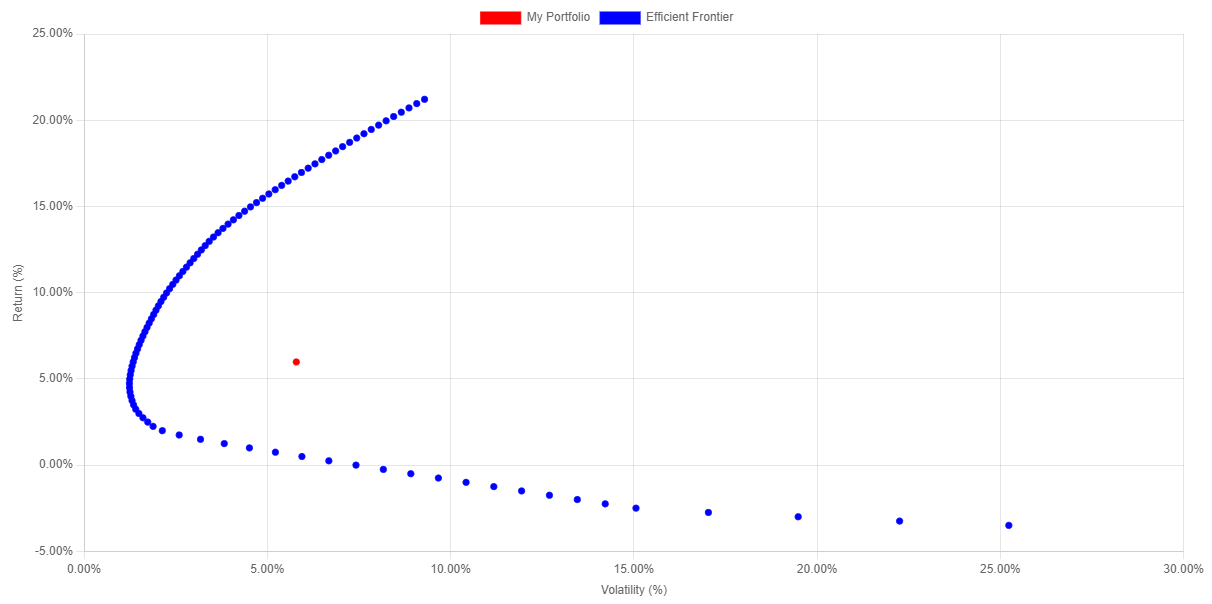

The risk/return metrics provide the most compelling use case for the portfolio and show off its potential to withstand drawdowns better than the index.

This is primarily due to the portfolio's lukewarm correlation. Its IPC, correlation between assets, is 0.36. That's considered "mild" in data science.

{kind=link}

As far as efficient weighting is concerned, I do my best to fit my income needs alongside my safety needs and have optimizing DIF decently according to modern portfolio theory .

{kind=link}

Conclusion

I am investing in three major themes that I expect to play out in 2024:

- A dovish Fed pivot into rate cuts

- Continued divergence between expected risk and realized risk in CLOs and bank loans

- Sustained high rates across quality sovereign frontier, developing, and emerging markets

These have led me to construct this portfolio, which has a forward yield of 7% and an expected volatility lower than the index.

If you are interested in getting an update on this portfolio sooner than a year (quarterly if I make changes?) or if you have any specific questions about the holdings, please comment below.

Thank you for reading.

For further details see:

My Fixed Income Portfolio Yields 7% And Is Positioned To Outperform The Index In 2024