TCTZF - My Portfolio Is Down 22% In 2022. Here's What I Learned

Summary

- In 2022, I made lots of mistakes that I want to share with my audience.

- I got hit hard with the geopolitical risks of my portfolio. I lost 15% of my purchasing power in February.

- These losses could have been made acceptable by proper position sizing and better risk management.

- The following article is part of my annual reflection on my investment decisions in 2022 and a short outlook for 2023.

Summary & Personal Note

2023 has just started, and it's time to be brutally honest about my performance during 2022. 2021 has been a highflyer year for me, with a return of 43,16 % and tons of mistakes . This year has been materially worse, and I had my first negative return of -22,11 % (-7,30 % ex-Russia) . I again learned from some painful mistakes that I want to share with my audience here on Seeking Alpha.

Personally, 2022 has been a good one for me. I finished my studies in autumn with good grades and began working full-time at a law firm. I managed to grow my Seeking Alpha followership to now more than 1,620+ followers, as I'm celebrating the start of my second year as a Contributor. I didn't expect that since I released only 24 articles in total. I am grateful for the support and constructive criticism, and I will continue to uphold quality over quantity. The goal of each article is to be thought-provoking and engaging.

Financial Stats of 2022

This year I had a return of -22,11 %. I've fully written off my investments in Russian ADRs due to precautionary accounting. Without counting the unrealized losses in Russian ADRs, the returns would have been -7,30 %. I don't expect western financial sanctions to ease any time soon. Therefore I believe writing off 100% of these assets makes sense until they are sold in the distant future. In 2022, the NASDAQ ( NDX ) returned -33,89%, the S&P 500 ( SPY ) -19,95 %, the Dow Jones ( DJI ) -9,40 %, and the MSCI World Index ( URTH ) -19,70 %. So I underperformed the market by ~ 1,37 % in total.

From the outside, my returns look like simple beta-farming with high risk tolerance in 2021. As you might discover in this article, it's much more nuanced than that. However, it is true that throughout the whole year of 2021, I've been far more aggressive than in 2022. A defensive switch was necessary for my portfolio because of worsening macroeconomic circumstances. Although I regret not reacting earlier to the obvious warning signs of the restrictive change of the Federal Reserve monetary policy in late 2021.

Portfolio Strategy

My portfolio strategy is not for everyone. I focus on forming a few investment theses with a medium-term time horizon, which fit my macro-outlook. Many of my ideas originate from contrarian thinking, but I'm not ignorant of charts. My portfolio is purposely concentrated because I want to make my high-conviction ideas count. Therefore, I try to limit the number of my investment positions to ~10-15.

In the following article, I will point out the positions that affected my performance for the year the most. I'll outline my thought processes and my learnings, which is why I write these articles in the first place.

The Terrible

2022 started out terrible & terrific. Let's start with the mistake that defined my whole year. I continued holding the Russian companies Gazprom ( OGZPY ) and Polymetal ( POYYF ), and the conflict in Ukraine happened in February of 2022. The western sanctions against Russia made it impossible to sell the ADRs or trade them into original shares. Therefore, I had to regard them as worthless. The ADRs will be sold in the future, and I should receive a fraction of my initial investment. But for now, I count the investments as a total loss.

This loss started off my year being down ~15% in Q1/2022. In retrospect, it's obvious that I got too greedy regarding the dividends and ignored the geopolitical risks. I don't believe the position itself was irrational - economically I was 100% right that Russian Oil & Gas companies would profit from Western green ideology. But the sizing was absolutely not appropriate for the political risk. My whole year would have looked different with a 5% allocation instead of 15%.

It was especially embarrassing because I kept full exposure to Gazprom right after selling 50% of my position at the peak in November of 2021.

Gazprom (tradingview.com)

Polymetal (tradingview.com)

Additionally, in the annual reflection of 2021, the top comment of my article pointed out the very obvious misallocation. Kudos to you, jayurbain. You were 100% correct:

Comment Section (seekingalpha.com)

{kind=link}

The Terrific

On the other hand, I managed to sell 100% of my position in ZIM Integrated Shipping ( ZIM ) in February and April 2022. The position was massive. The timing was good, and ZIM turned out to be one of my biggest wins during 2021 & 2022. Now, it's obvious that my risk tolerance had been off the charts. It was 2021, after all. But I knew about the cyclical environment and jumped off the board radically after I thought the cycle peaked. With all the macroeconomic and financial headwinds visible in Q1/2022, I sold everything. Shortly after, I published my article "The ZIM wave is nearing its breaking point" . It turned out to be one of my personal favorites in 2022 and also my most successful article yet.

ZIM (tradingview.com)

However, I reinvested a good portion of the gains of ZIM in much less cyclical Containership Lessors. I described my thought process in this article . I thought that Container Lessors were still undervalued regarding their free cash flow potential and long-term contracts.

Danaos (tradingview.com)

Global Ship Lease (tradingview.com)

Danaos ( DAC ) and Global Ship Lease ( GSL ) were indeed outperforming the Liners during 2022. But still, they peaked around the same time that ZIM peaked. I underestimated how much of the free cash flow of the long-term contracts of these Lessors was already priced in at that time. The whole cyclical container sector tends to move in one direction, only with different betas depending on the company's risk structure. I also bailed on the Lessors due to a lack of positive future catalysts because of macroeconomic headwinds and a poor containership order book for 2023 and 2024. The leases should come in for these companies without much risk. If circumstances change, I might reinvest.

Risk Reduction

After realizing in what kind of macro environment the global economy would be heading, I derisked my whole portfolio at the end of Q1/2022. It only started with the reduction of my exposure to the cyclical container sector. I figured that an environment with higher interest rates wouldn't bode well for any long-duration asset. After participating in (my first) Crypto bull run, I decided to sell everything with the exception of some Bitcoin, which I'll hold for the long run in cold storage.

Bitcoin (tradingview.com)

Ethereum (tradingview.com)

Overall, I made some gains and learned a whole lot about this asset class. I view Crypto as a hedge against monetary devaluation (not inflation). During times of tightening policies of global central banks it won't perform well. However, during 2023, I will start to gradually build up significant exposure towards Bitcoin ( BTC-USD ) (maybe Ethereum ( ETH-USD ) too at a later stage) because I don't believe that Central banks can tighten policy into 2024. The reoccurring bubble of Crypto will likely emerge again in a few years. And I'll be prepared now, having experienced a cycle already. To me, it is very interesting that the public opinion regarding Crypto is either: 'it's going to zero' or 'it's going to infinity'. I believe the world is moving cyclically, not linearly.

Mistakes from the past: China

2021 could have been a 70+ % year if I hadn't bought Chinese equities. I already elaborated on my mistakes in last year's article . During the derisking of my portfolio during late Q1/2022, I also reduced my exposure to long-duration Chinese tech names: Alibaba ( BABA ), Baidu ( BIDU ), Tencent ( TCEHY ). They were cheap, so it was no easy sell. But I figured they would underperform due to the same reasons I believed Crypto would underperform: Tightening monetary policy and a dire macroeconomic outlook for the rest of 2022.

Tencent (tradingview.com)

Baidu (tradingview.com)

Alibaba (tradingview.com)

I didn't want to divest completely, so I swapped a chunk of my position for the KraneShares CSI China Internet ETF ( KWEB ). KWEB is basically Chinese ARKK without overvaluation but with political risks. I reduced my exposure in late 2022, but I plan on holding the position throughout 2023. China is coming out of a deep recession and already accelerates fiscal and monetary stimulus after the reopening of the economy, although the recent measures have somewhat disappointed. I learned from my mistakes with Russian equities, and therefore I will keep a sub-5 % allocation to account for political risks.

KWEB (tradingview.com)

Inflation or Deflation?

What I described until now was the major derisking of my portfolio in the first half of 2022. So what did I do with the freed-up liquidity?

Mainly nothing.

During the majority of Q2-Q4/2022, I held most of my purchasing power (60-70%) in cash or cash equivalents (USD, EUR, CHF, Tbills, etc.).

However, I did make one serious attempt of buying long-duration bonds ( TLT ), as I believed that inflation was in the process of peaking. However, these attempts were too early. I realized that I tried to catch a falling (bond) knife. So I sold 50% of the position. I still believe inflation has peaked, and long-duration yields should fall during 2023. However, I am patiently waiting for the market to signal a bottom. I believe a decelerating economy, along with disinflation or outright deflation during H2/2023, will favor long-duration yields. A 4 % 30Y-yield doesn't seem sustainable to me, given the enormous amounts of US debt to GDP. I'm structurally bearish on fixed income in the very long-term (5-10 years), however.

TLT (tradingview.com)

Tactical Shorts

Additionally, I tactically shorted equities in 2022. I expressed my negative views on long-duration assets by shorting the Nasdaq ( NDX ) twice in 2022 at points where I thought the risk/reward was favorable.

Nasdaq 100 (tradingview.com)

Additionally, I started shorting the DAX ( DAX ), which I still regard as overvalued. Especially when comparing the performance of the DAX to the Dow Jones ( DJI ). I still hold the current short position.

DAX (tradingview.com)

Current Positions

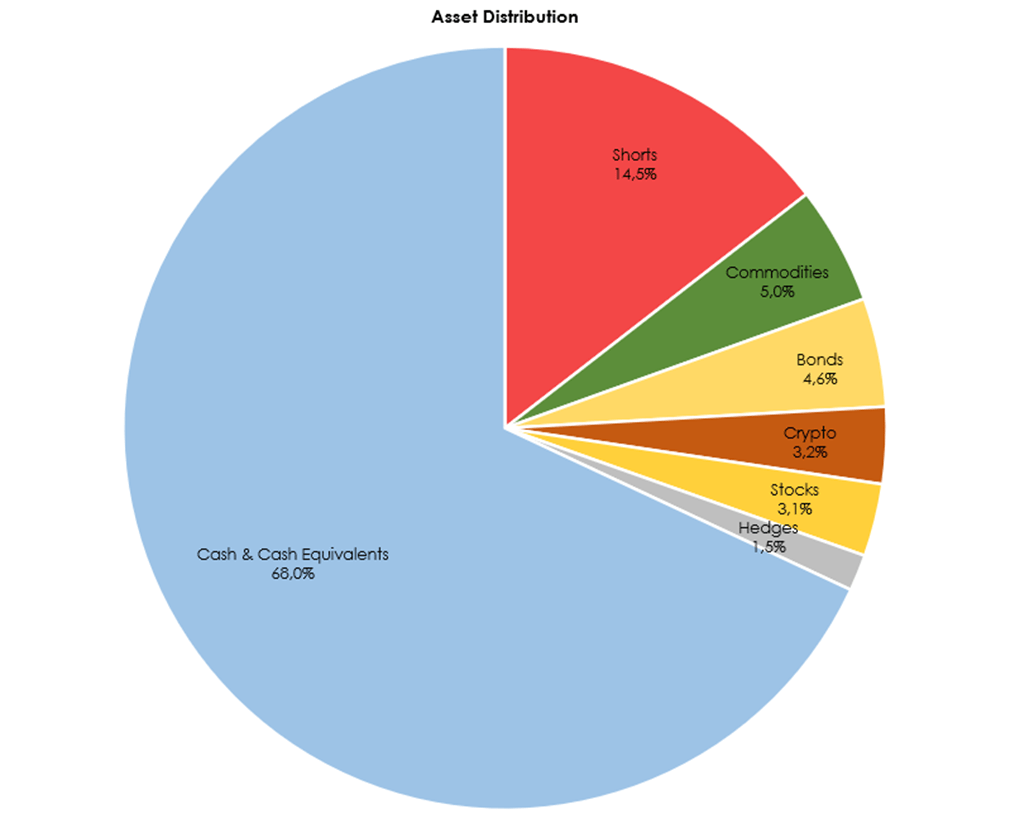

My portfolio is still very defensively structured. I hold about 68% of Cash & Cash Equivalents. These are mainly EUR, USD (T-Bills), and CHF.

Asset Distribution (Author using Excel)

{kind=link}

I am still very short the DAX. I continue to hold physical Uranium via the Sprott Physical Uranium Trust ( SRUUF ). I plan on expanding the long-duration Bond Position during the first quarter of 2023 ( TLT ). I also continue to hold the KWEB position and tactically added a long VIX ( VXX ) position as an additional hedge during the last two weeks.

Individual Assets (ex cash) (Author using Excel)

{kind=link}

2023 Outlook

I'm not yet bullish on equities for 2023 since I believe margin compression is just about to begin, especially in Europe. 2022 was the year of the price shock, and 2023 may be the year of the earnings shock. The US housing market looks fragile. Therefore unemployment is at risk of making a moonshot, and the firefighters of the Federal Reserve won't extinguish the fire before the markets sound the alarm. In my opinion, 'Sounding the alarm' requires an additional drawdown for equities, given current valuations and the relative attractiveness of fixed income.

However, Crypto assets don't have any earnings and primarily depend on yields (i.e. liquidity provision) and devaluation of money (not inflation). Crypto is still far away from positive price movements, while Quantitative Tightening is reducing the balance sheets of the central banks. A dire situation of the economy will never be bullish for Crypto. If unemployment rises, people have to derisk their portfolios, and Crypto Assets are likely the first ones to be liquidated. Another drawdown is likely, but it's starting to get interesting for Bitcoin, in my opinion.

I do have a bullish view regarding the long end of the bond market. Given my current opinion about disinflation or deflation in 2023, a weakening consumer and a worsening economic situation, I'm cautiously bullish on 20Y+ US bonds ( TLT ). I believe 4% for a weakening economy and disinflation seems like a good value proposition, especially in comparison to equities. I'm currently waiting to add to my position during H1/2023.

Personal Note

Thank you for an amazing year on Seeking Alpha! The interactions in the comment section keep me excited to write articles. The goal of this Seeking Alpha profile is to learn, reflect, and to grow together.

I wish you all the best of luck in 2023.

"Ich sage euch: man muss noch Chaos in sich haben, um einen tanzenden Stern gebären zu können." - Friedrich Wilhelm Nietzsche

For further details see:

My Portfolio Is Down 22% In 2022. Here's What I Learned