KHC - My Top 10 High Dividend Yield Companies For December 2023

2023-12-07 18:00:00 ET

Summary

- High dividend yield companies can provide investors with several benefits, such as the generation of income and the reduction of portfolio volatility.

- Furthermore, the companies’ continuous dividend payments can be an indicator of their financial health, particularly if these dividends are sustainable.

- I have selected 10 companies which are characterized by modest Payout Ratios, a strong Profitability, and an attractive Valuation. Moreover, these picks have demonstrated a track record of dividend growth.

Investment Thesis

I consider high dividend yield companies to be a key element of an extensively diversified investment portfolio for any type of investor. This isn’t only because they represent an additional source of income. High dividend yield companies can also play a crucial role in reducing the volatility of your investment portfolio, providing you as an investor with increased stability and more control over your financials. In addition to that, continuous dividend payments often reflect a company’s financial health, particularly when these dividend payments are sustainable over time.

In today’s analysis, I will introduce you to 10 companies which not only provide you as an investor with a relatively high Dividend Yield, but they also exhibit other compelling attributes: the selected picks are characterized by modest Payout Ratios (which decrease the likelihood of a dividend cut and increase the probability of obtaining positive investment outcomes), and a strong Profitability (which is an indicator of a strong competitive position within their respective industry).

Furthermore, the carefully selected picks have demonstrated a consistent track record of dividend growth, underscoring the sustainability of their dividends. Moreover, they have promising growth prospects and I consider their Valuation to be attractive.

Before I introduce you to each of the 10 selected companies, I will explain in greater detail the selection process.

Since I have already described the detailed selection process of high dividend yield companies in a previous article . you can skip the following section written in italics, If you are already familiar with it.

First Step of the Selection Process: Analysis of the Financial Ratios

In order to identify companies with a relatively high Dividend Yield [FWD], I use a filter process to make a pre-selection. From this pre-selection, I will later choose my top 10 high Dividend Yield companies of the month. To be part of this pre-selection of high Dividend Yield stocks, the companies should fulfil the following requirements:

- Market Capitalization > $10B

- Dividend Yield [FWD] > 2.5%

- P/E [FWD] Ratio < 30

In the following, I would like to specify why I have chosen the metrics mentioned above in order to select my top 10 high Dividend Yield stocks of the month.

A Market Capitalization of more than $10B contributes to the fact that the risks attached to your investments are lower, since companies with a higher Market Capitalization tend to have a lower volatility than companies with a low Market Capitalization.

A P/E [FWD] Ratio of less than 30 implies that the price you pay for the company is not extraordinarily high, thus filtering out those that have stock prices in which high growth expectations are priced in. High growth expectations imply strong risks for investors, since the stock price could drop significantly. Again, the filtering process helps us to reduce the risk so that we are more likely to make an excellent investment decision.

Second Step of the Selection Process: Analysis of the Competitive Advantages

In a second step, the companies’ competitive advantages (for example: brand image, innovation, technology, economies of scale, etc.) are analyzed in order to make an even narrower selection. I consider it to be particularly important for companies to have strong competitive advantages in order to stand out against the competition in the long term. Companies without strong competitive advantages have a higher probability of going bankrupt one day, thus representing a strong risk for investors to lose their invested money.

Third Step of the Selection Process: The Valuation of the Companies

In the third step of the selection process, I will dive deeper into the Valuation of the companies.

In order to conduct the Valuation process, I use different methods and criteria, for example, the companies’ current Valuation as according to my DCF Model, the expected compound annual rate of return as according to my DCF Model and/or a deeper analysis of the companies’ P/E [FWD] Ratio. These metrics should serve as an additional filter to only select companies that currently have an attractive Valuation, which helps you to identify companies that are at least fairly valued.

The Fourth and Final Step of the Selection Process: Diversification Over Industries and Countries

In the fourth and final step of the selection process, I have established the following rules for choosing my top picks: in order to help you diversify your investment portfolio, a maximum of two companies should be from the same industry. In addition to that, there should be at least one pick that is from a company that is based outside of the United States, serving as an additional geographical diversification.

My Top 10 High Dividend Yield Companies to Consider Investing in for December 2023

- Allianz ( ALIZY )( ALIZF )

- Altria Group ( MO )

- AT&T ( T )

- Banco Santander ( SAN )

- Morgan Stanley ( MS )

- Petróleo Brasileiro S.A. ( PBR )

- Pfizer ( PFE )

- The Kraft Heinz Company ( KHC )

- United Parcel Service ( UPS )

- Verizon Communications ( VZ )

Overview of the 10 Selected High Dividend Yield Companies to Consider Investing in for December 2023

| ALIZF |

| MO |

| T |

| SAN |

| MS |

| PBR |

| PFE |

| KHC |

| UPS |

| VZ |

| Company Name |

| Allianz SE |

| Altria |

| AT&T |

| Banco Santander |

| Morgan Stanley |

| Petróleo Brasileiro S.A. - Petrobras |

| Pfizer |

| Kraft Heinz |

| United Parcel Service |

| Verizon |

| Sector |

| Financials |

| Consumer Staples |

| Communication Services |

| Financials |

| Financials |

| Energy |

| Health Care |

| Consumer Staples |

| Industrials |

| Communication Services |

| Industry |

| Multi-line Insurance |

| Tobacco |

| Integrated Telecommunication Services |

| Diversified Banks |

| Investment Banking and Brokerage |

| Integrated Oil and Gas |

| Pharmaceuticals |

| Packaged Foods and Meats |

| Air Freight and Logistics |

| Integrated Telecommunication Services |

| Market Cap |

| 99.01B |

| 73.86B |

| 116.55B |

| 66.57B |

| 128.93B |

| 96.68B |

| 169.84B |

| 43.03B |

| 129.74B |

| 158.75B |

| Dividend Yield [FWD] |

| 4.99% |

| 9.39% |

| 6.81% |

| 4.15% |

| 4.33% |

| 9.80% |

| 5.45% |

| 4.61% |

| 4.26% |

| 7.04% |

| Dividend Yield [TTM] |

| 4.99% |

| 9.10% |

| 6.81% |

| 3.65% |

| 4.14% |

| 4.56% |

| 5.45% |

| 4.61% |

| 4.26% |

| 6.95% |

| Payout Ratio |

| 55.88% |

| 76.77% |

| 44.76% |

| 27.44% |

| 55.11% |

| 33.87% |

| 56.79% |

| 52.63% |

| 64.25% |

| 54.41% |

| Dividend Growth 3 Yr [CAGR] |

| 6.58% |

| 3.98% |

| -10.93% |

| 9.56% |

| 32.41% |

| 54.84% |

| 4.43% |

| 0.00% |

| 17.06% |

| 1.98% |

| Dividend Growth 5 Yr [CAGR] |

| 5.72% |

| 5.85% |

| -5.97% |

| -9.64% |

| 24.19% |

| - |

| 4.95% |

| -8.54% |

| 12.23% |

| 2.02% |

| P/E [FWD] |

| 11.61 |

| 9.10 |

| 7.33 |

| 6.16 |

| 13.99 |

| 4.01 |

| 18.74 |

| 13.69 |

| 18.05 |

| 8.45 |

| Net Income Margin |

| 8.04% |

| 42.60% |

| -9.29% |

| 23.63% |

| 18.37% |

| 25.53% |

| 15.29% |

| 11.00% |

| 9.19% |

| 15.58% |

| 24M Beta |

| 0.73 |

| 0.42 |

| 0.57 |

| 1.00 |

| 1.04 |

| 0.20 |

| 0.55 |

| 0.28 |

| 1.02 |

| 0.38 |

Source: Seeking Alpha

Banco Santander

Founded in 1856, Banco Santander is a bank based in Madrid, Spain. It operates through the following segments :

- Retail Banking

- Santander Corporate & Investment Banking

- Wealth Management & Insurance

- PagoNxt

The Spanish bank currently pays a Dividend Yield [FWD] of 4.15%. Moreover, it has shown a Dividend Growth Rate [CAGR] of 9.56% over the past 3 years, suggesting that it can help investors to combine dividend income with dividend growth.

In terms of Valuation, I believe that the bank presents a compelling opportunity, due to its P/E GAAP [FWD] Ratio of 6.16, which is 36.93% below the Sector Median. This number suggests that Banco Santander is currently undervalued. The same is indicated when looking at the bank’s P/E Non-GAAP [FWD] Ratio of 5.96, which is 32.15% below its average from the past 5 years.

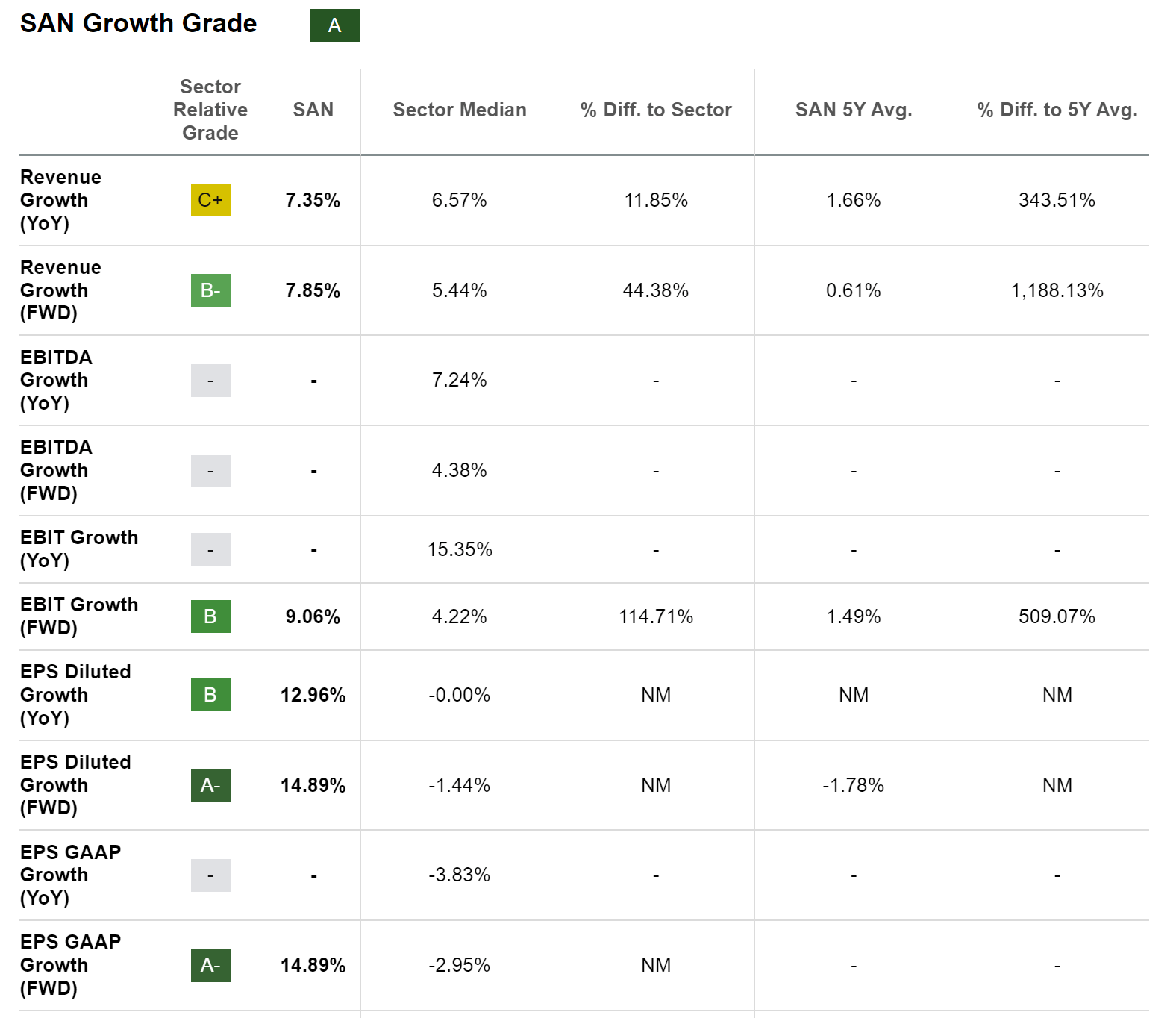

It is further worth noting that the bank has produced impressive results in terms of growth: it has shown an EPS FWD Long Term Growth Rate [3-5Y CAGR] of 16.08%, which is 78.70% above the Sector Median, and an EBIT Growth Rate [FWD] of 9.06%, standing 114.71% above the Sector Median. Below you can find additional growth metrics for Banco Santander.

{kind=link}

The Elevated Risk Factors of an Investment in Banco Santander – The Case for a 3% Limit on Your Overall Portfolio

Given the elevated risk associated with an investment in Banco Santander, particularly due to currency risks, European financial regulatory factors and geopolitical uncertainties in Europe, I suggest limiting the position of Banco Santander to a maximum of 3% of your portfolio. This ensures a reduced company-specific concentration risk and thereby a reduced downside risk for your overall portfolio.

Petróleo Brasileiro S.A. - Petrobras

Petrobras is a Brazilian company from the Integrated Oil and Gas Industry that was founded back in 1953. The company is headquartered in Rio de Janeiro and presently has 45,149 employees. It operates through the following segments :

- Exploration and Production

- Refining

- Transportation and Marketing

- Gas and Power

The company pays a Dividend Yield [FWD] of 9.80%, which makes it an attractive choice for dividend income investors.

At this moment in time, the company has a P/E GAAP [FWD] Ratio of 4.01, which is 62.80% below the Sector Median, indicating that it is presently undervalued. In addition, it’s worth highlighting that Petrobras’ P/E Non-GAAP [FWD] Ratio of 4.16 is 49.56% below its average from the past 5 years, serving as an additional indicator of the company’s undervaluation.

The Elevated Risk Factors of an Investment in Petrobras – The Case for a 3% Limit on Your Overall Portfolio

From my perspective, investing in the Brazilian company carries a relatively high level of risk. This is not only because of the currency risk, where a weakening Brazilian real would have a negative impact on investments. Aside from that, I do not perceive the company’s dividend as being entirely secure.

A possible dividend cut could have a negative impact on the company’s stock price, representing a strong risk factor for you as an investor. For all these reasons, I suggest that you limit the position in Petrobras to a maximum of 3% of your overall investment portfolio, aiming to reduce the downside risk.

Kraft Heinz

Kraft Heinz currently pays its shareholders a Dividend Yield [FWD] of 4.61%, which is particularly attractive when considering the company’s relatively low Payout Ratio of 52.63%.

The company exhibits a Free Cash Flow Yield [TTM] of 5.89%, which shows that it represents an attractive risk/reward profile for investors.

It is further worth highlighting that the Valuation of Kraft Heinz is relatively attractive. This is evidenced through the company’s P/E GAAP [FWD] Ratio of 13.69, which is 25.99% below the Sector Median and 46.39% below its average from the past 5 years. Both metrics confirm the company’s undervaluation.

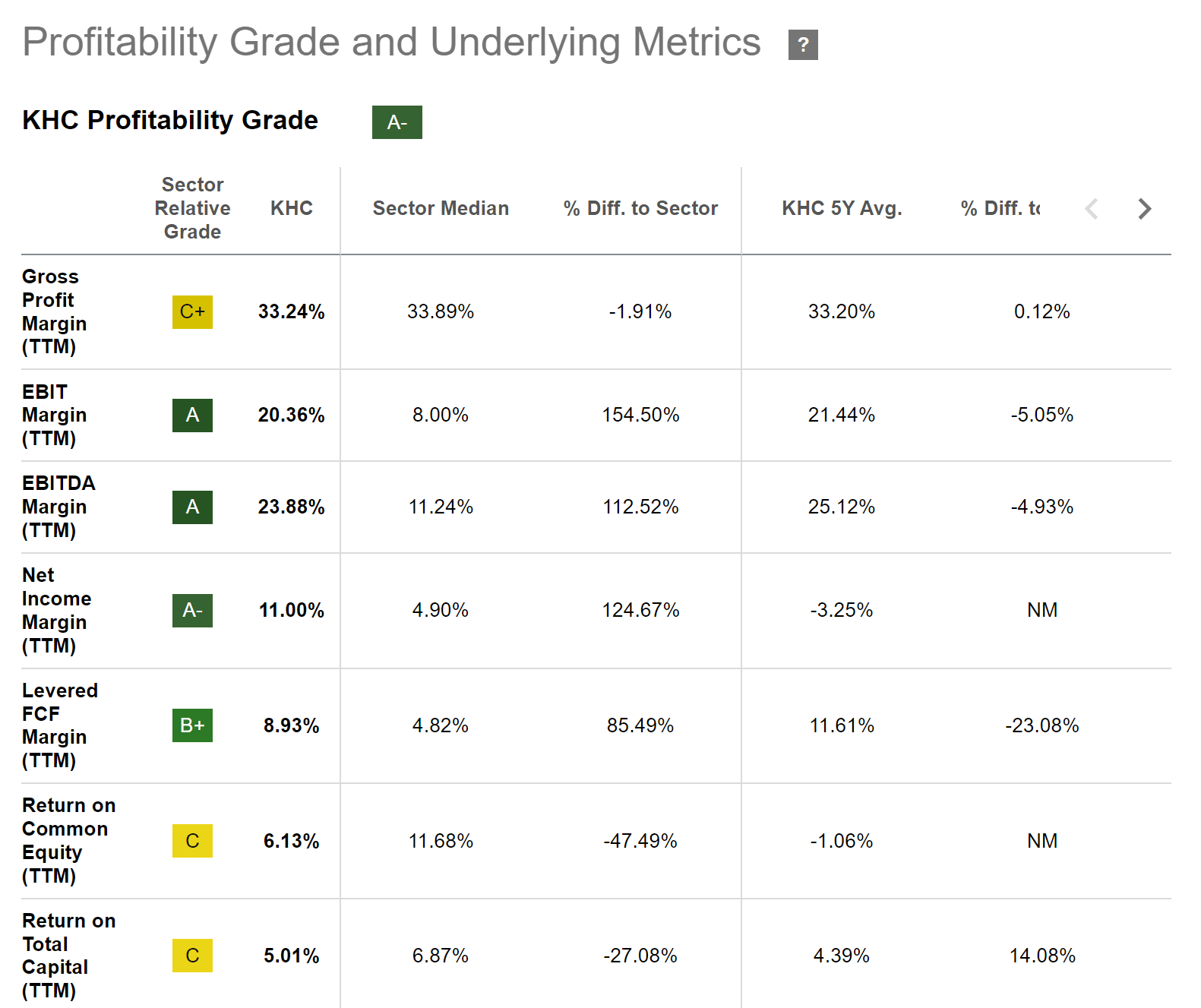

Below you can find the Seeking Alpha Profitability Grades, which confirm the company’s attractiveness in terms of Profitability: Kraft Heinz exhibits an EBIT Margin [TTM] of 23.88%, which is significantly above the Sector Median of 11.24%, and a Net Income Margin [TTM] of 11.00%, which is clearly above the Sector Median of 4.90%.

{kind=link}

Allianz

Allianz’s Aa2 credit rating from Moody’s underscores the company’s financial health and aligns with my investment approach to ensure capital preservation above all.

The German insurance company currently has a P/E [FWD] Ratio of 11.61, which is only slightly above the Sector Median of 9.97, suggesting that it is currently fairly valued.

At the company’s current share price, it pays a Dividend Yield [FWD] of 4.99%, which is significantly above the Sector Median of 3.59%.

Allianz’s Dividend Growth Rate 3Y [CAGR] stands at 6.33%, which underlines that the company is not only an attractive choice in terms of dividend income, but also in terms of dividend growth.

It is worth highlighting that Allianz’s exhibits a Dividend Payout Ratio [TTM] [GAAP] of 55.88%, suggesting that its Dividend should be relatively safe within the coming years.

The company’s 24M Beta Factor of 0.73 further indicates that you can reduce portfolio volatility with its incorporation.

Allianz’s attractive Valuation, its combination of dividend income and dividend growth, its strong Profitability and significant competitive advantages, make the company a potential candidate for incorporation into The Dividend Income Accelerator Portfolio in the coming weeks.

AT&T

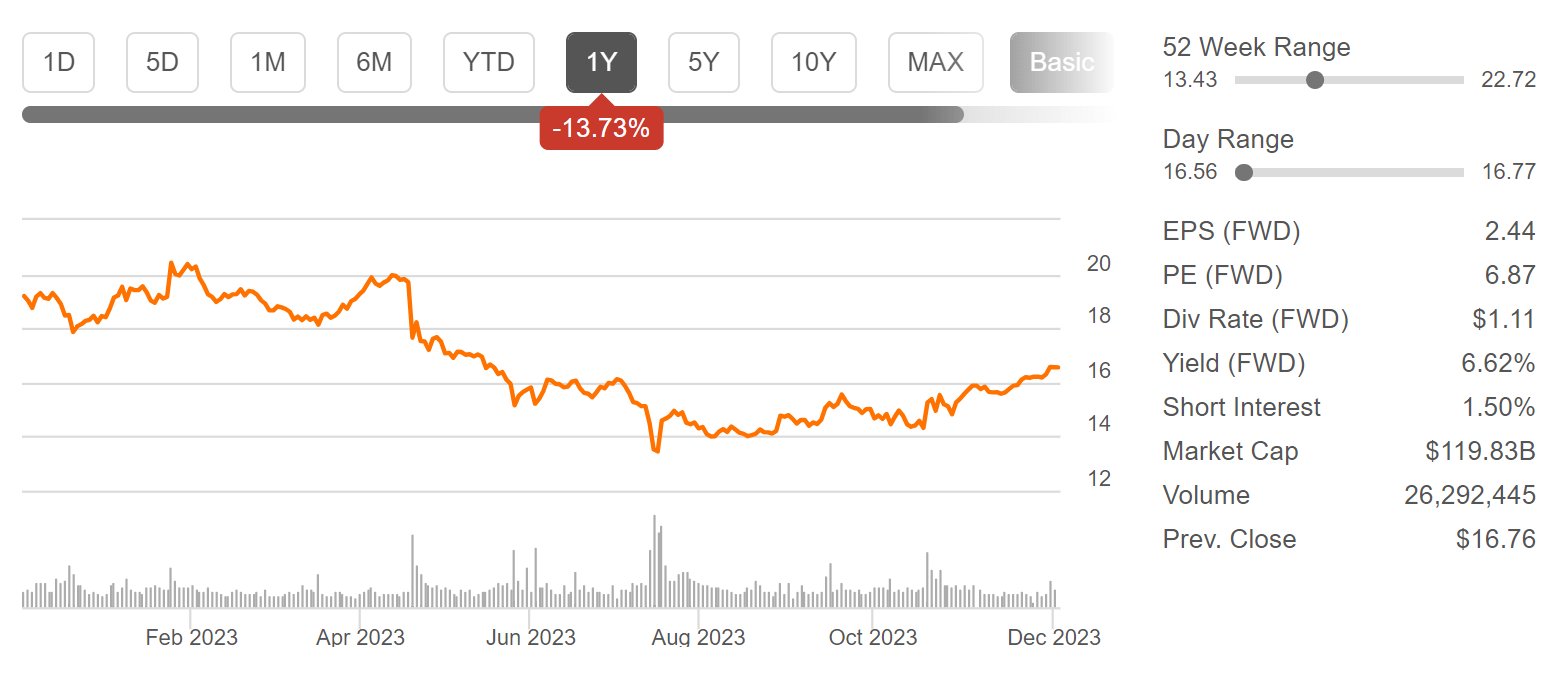

Within the past 12-month period, AT&T has shown a negative Total Return of 13.73%.

{kind=link}

Today, AT&T pays shareholders a Dividend Yield [FWD] of 6.81%. The company’s Free Cash Flow Yield [TTM] stands at 16.44%, indicating that it presently has an attractive risk/reward profile. At this moment in time, AT&T has a P/E [FWD] Ratio of 7.49, which is significantly below its 5 year average of 11.03.

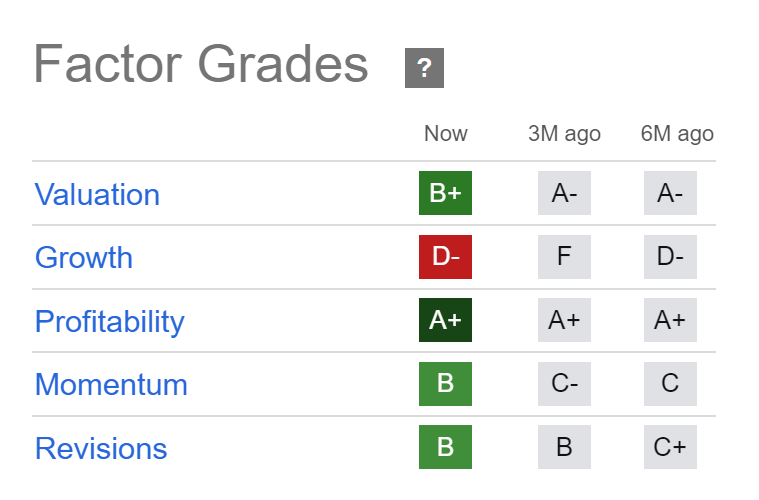

The Seeking Alpha Factor Grades confirm my investment thesis that AT&T is an attractive choice in terms of Profitability and Valuation. The company is rated with an A+ for Profitability, and with a B+ for Valuation.

{kind=link}

Due to the company’s limited growth potential, I suggest underweighting it in a long-term oriented investment portfolio.

United Parcel Service

In addition to Allianz, I also see United Parcel Service as a potential candidate for future incorporation into The Dividend Income Accelerator Portfolio. This is due to its combination of dividend income (Dividend Yield [FWD] of 4.26%) and dividend growth (3 Year Dividend Growth Rate [CAGR] of 17.06%), its strong Profitability (Return on Equity of 47.35%), and its attractive Valuation (P/E [FWD] Ratio of 18.48, which is 12.74% below the Sector Median), in addition to its significant competitive advantages.

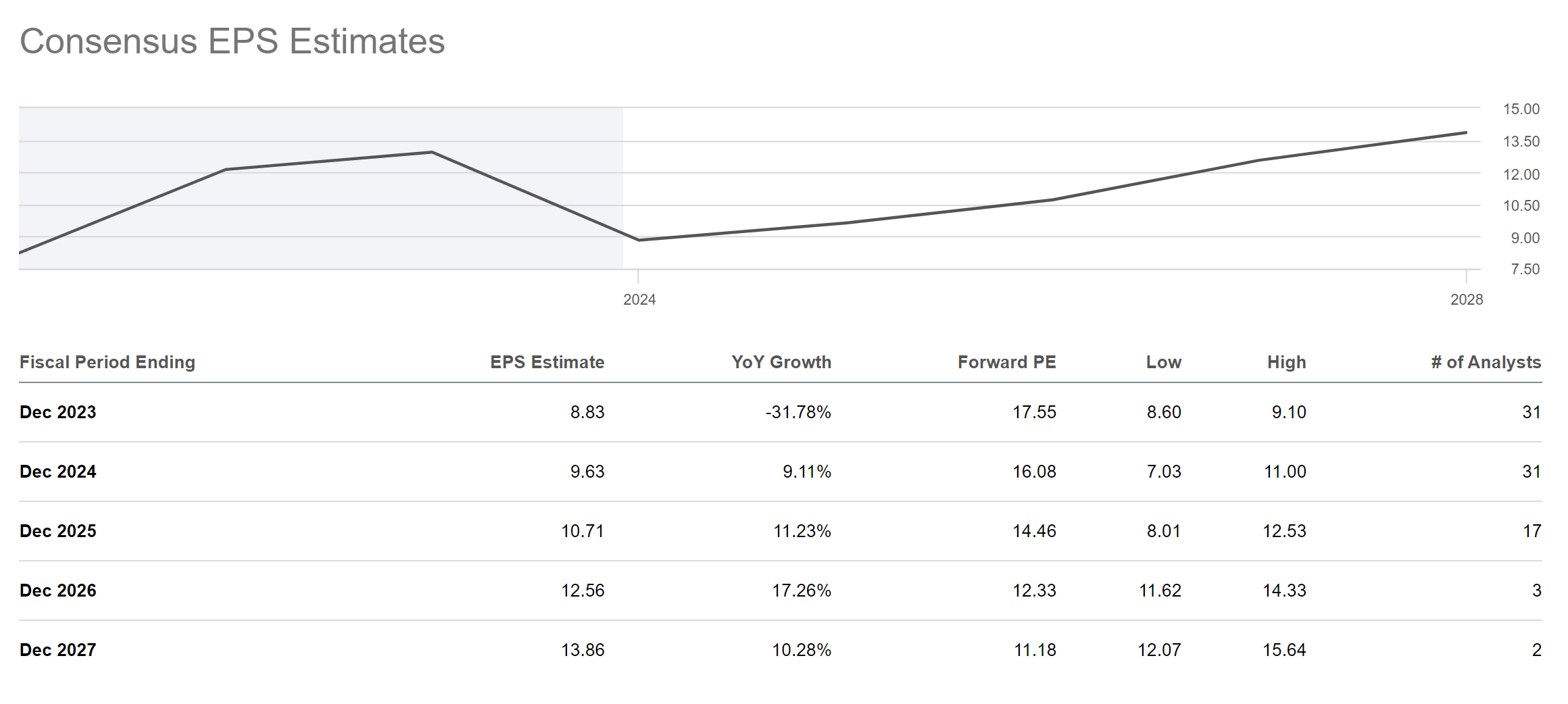

Below you can find EPS Estimates for United Parcel Service. EPS Estimates are $8.83 for 2023, $9.63 for 2024, $10.71 for 2025, $12.56 for 2026, and $13.86 for 2027.

{kind=link}

By comparing United Parcel Service with competitor FedEx ( FDX ), it can be highlighted that United Parcel Service provides shareholders with the significantly higher Dividend Yield [FWD] (4.18% compared to 1.91%). This suggests that it's the more adequate pick for investors focusing on dividend income.

In terms of Dividend Growth, however, I see FedEx as being ahead of UPS, given the company’s higher 3 Year Dividend Growth Rate of 15.95% (compared to UPS’ 12.23%) and its significantly lower Payout Ratio of 29.98% (compared to 64.25%). For this reason, If you prefer the company with the higher dividend growth potential, you might select FedEx over UPS.

Pfizer

The Dividend Income Accelerator Portfolio already holds an indirect investment in Pfizer through its stake in Schwab U.S. Dividend Equity ETF ( SCHD ). However, I am considering incorporating Pfizer as a direct investment in the following weeks.

It is worth highlighting that Pfizer’s Dividend Yield [FWD] of 5.45% is significantly above the one of competitors such as Johnson & Johnson ( JNJ ) and Merck & Co ( MRK ), which offer Dividend Yields [FWD] of 3.01%, and 2.98% respectively.

When compared to competitor Johnson & Johnson, Pfizer has further shown a higher 3 Year Revenue Growth Rate [CAGR] (28.46% compared to 6.86%) and a higher 3 Year EBIT Growth Rate [CAGR] (31.31% compared to 11.23%).

Pfizer’s 3 Year Dividend Growth Rate [CAGR] of 4.43% and its Payout Ratio of 56.79%, underscore my theory that the company is an attractive candidate for potential inclusion into The Dividend Income Accelerator Portfolio.

Presently, Pfizer has a P/E Non-GAAP [FWD] Ratio of 18.48, which is in line with the Sector Median of 18.71, suggesting that the company is fairly valued at its current price levels.

Altria

Founded in 1822, Altria presently has 6300 employees and boasts a Market Capitalization of $75.34B. Given the company’s current Valuation (P/E [FWD] Ratio of 9.28), its high Dividend Yield [FWD] of 9.20%, in combination with its Payout Ratio of 76.77% and its 53 Consecutive Years of Dividend Growth, Altria is worth taking a closer look at, particularly when aiming to combine dividend income with dividend growth.

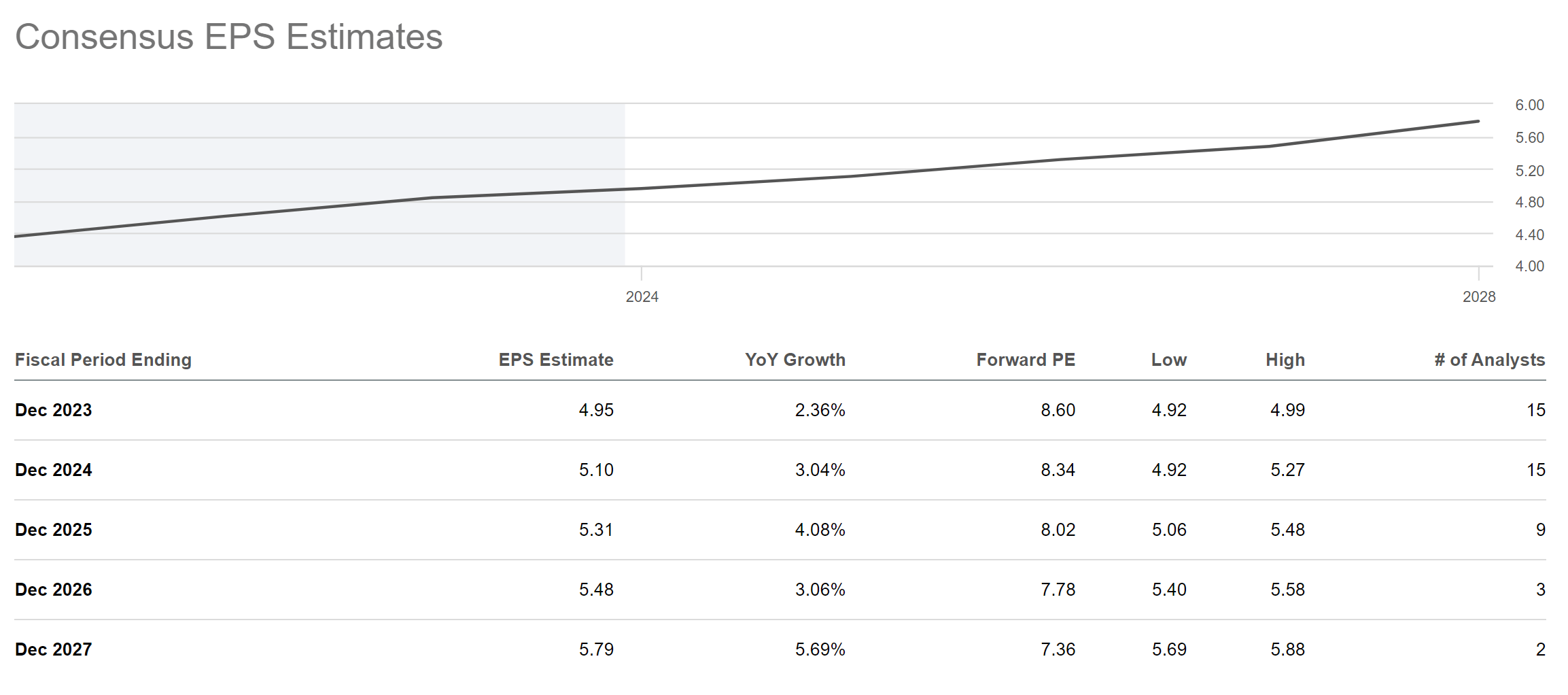

EPS Estimates are at $4.95 for 2023, $5.10 for 2024, $5.31 for 2025, $5.48 for 2026, and $5.79 for 2027, which implies a steady EPS Growth Rate for the company in the years ahead, further underscoring my investment thesis that Altria is an excellent pick for dividend income and dividend growth investors.

{kind=link}

Morgan Stanley

Morgan Stanley’s current Dividend Yield [FWD] of 4.33% is presently attractive for investors. This is especially the case when considering the company’s Payout Ratio of 55.11%, its 3 Year Dividend Growth Rate [CAGR] of 32.41%, in combination with 10 Consecutive Years of Dividend Growth and 26 Consecutive Years of Dividend Payments.

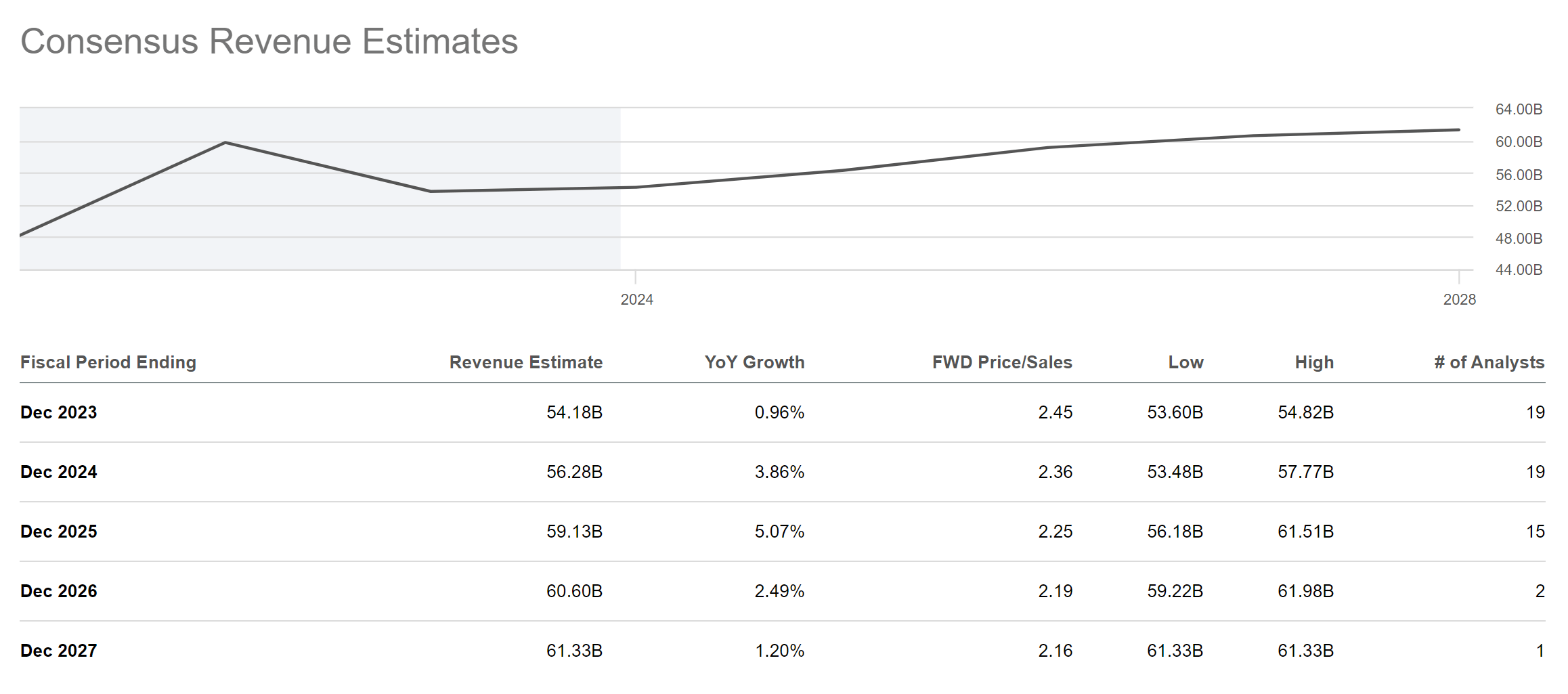

Below you can find Revenue Estimates for Morgan Stanley for the coming years. These Revenue Estimates imply a YoY Revenue Growth of 0.96% for 2023, 3.86% for 2024, 5.07% for 2025, 2.49% for 2026, and 1.20% for 2027, underscoring my theory that the bank should be able to provide you with a steadily increasing income stream in the years ahead.

{kind=link}

Morgan Stanley’s current Dividend Yield [FWD] of 4.20% is presently significantly above the one of Bank of America ( BAC ) (Dividend Yield [FWD] of 3.10%) and JPMorgan ( JPM ) (2.68%).

However, given Bank of America and JPMorgan’s significantly lower Payout Ratio (25.21% and 24.18% respectively compared to Morgan Stanley’s 55.11%), and their higher EPS Growth Diluted [FWD] (-2.80% and 0.17% compared to Morgan Stanley’s -5.69%), I consider their Dividend to be more secure than Morgan Stanley’s.

I further see Bank of America and JP Morgan being ahead of Morgan Stanley in terms of Profitability (Net Income Margin of 31.52% and 35.98% respectively compared to 18.37%) and Valuation (P/E [FWD] Ratio of 9.12 and 9.44 respectively compared to 14.48).

These metrics underline that Morgan Stanley is particularly attractive for dividend income investors. However, investors seeking an option with a lower Valuation and an even higher Profitability might opt for selecting Bank of America or JPMorgan over Morgan Stanley.

Verizon

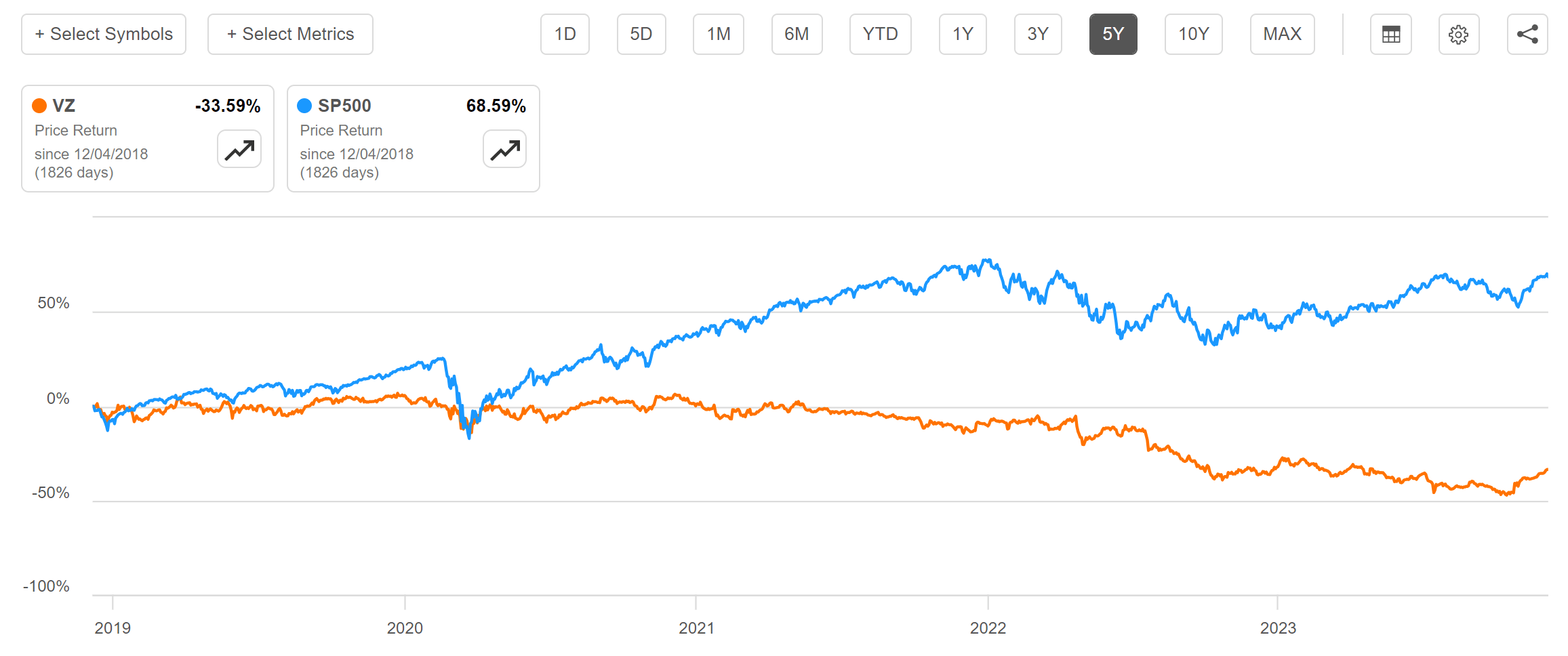

Considering the past 5 years, the S&P 500 has clearly outperformed Verizon: while the S&P 500 has shown a positive performance of 68.59%, Verizon’s performance has been negative (-33.59%).

{kind=link}

Despite the company’s negative performance over this period, Verizon currently seems an attractive pick for investors, given its high Dividend Yield [FWD] of 7.04%, its relatively low Valuation (P/E [FWD] Ratio of 8.63 (which is 19.06% below its average from the past 5 years), its strong Profitability (Return on Equity of 22.56%, which is clearly above the Sector Median of 3.21%), and its relatively low Payout Ratio of 54.41%.

These characteristics make Verizon an attractive candidate for potential inclusion into The Dividend Income Accelerator Portfolio, which is already invested in the company through its stake in Schwab U.S. Dividend Equity ETF.

With a proportion of 4.44%, Verizon is currently the largest position of Schwab U.S. Dividend Equity ETF.

This implies that Verizon might seem a less attractive choice for those investors that already hold Schwab U.S. Dividend Equity ETF as one of their largest positions. Adding Verizon might lead to an over-concentration in the company, implying a higher risk level for their portfolio.

I consider adding Verizon to The Dividend Income Accelerator Portfolio, but only after achieving greater diversification to ensure Verizon does not represent a disproportionately large share of the overall portfolio.

Another reason why I would avoid giving Verizon a disproportionally high share of the overall portfolio is its limited growth prospect, reflected by a Revenue Growth Rate [FWD] of 0.48%.

Overview of The Companies’ Dividend Yield and Their Payout Ratios

In the graphic below you can find an overview of the current Dividend Yield [FWD] of the 10 selected companies that I consider worth investing in for December 2023:

Source: The Author, data from Seeking Alpha

The chart below illustrates the Payout Ratio of the 10 selected companies. A low Payout Ratio can serve as an indicator of a company’s sustainable dividend.

Source: The Author, data from Seeking Alpha

It is worth highlighting that even though I consider the Payout Ratio to be an important indicator for the sustainability of a company’s dividend, other metrics should also be considered (such as the EPS Growth Rate for example) for a more comprehensive analysis of the sustainability of dividends.

Conclusion

Companies which pay attractive dividends can be particularly beneficial for investors. They not only provide investors with a steady income stream; they can also contribute to reducing portfolio volatility. In addition to that, dividend payments can be an indicator of a company’s financial health, particularly if the dividend payments are sustainable over time.

Different metrics can help us to identify companies that pay sustainable dividends. Among other financial metrics, I consider the Payout Ratio and the EPS Growth Rate to be important metrics aiming to identify companies that pay sustainable dividends.

In this article, I have introduced you to 10 companies that could help you generate an income stream via dividend payments. Not only do they pay a relatively high Dividend Yield; they are also characterized by a relatively low Payout Ratio and a strong Profitability. Furthermore, their Valuation is attractive and their growth outlook is positive.

From my perspective, strategically balancing high dividend yield companies with those focusing on dividend growth offers substantial benefits for investors. This approach not only facilitates the generation of additional income via dividends in the present, but also ensures constantly increasing dividends in the future. This strategy allows investors to have greater control over their financials, blending immediate income with attractive financial outcomes over the long term.

For this reason, here on Seeking Alpha, I am constructing and transparently detailing the approach of The Dividend Income Accelerator Portfolio, in which I carefully integrate both high dividend yield companies and those with a focus on dividend growth. The objective is to combine the strength of both categories, optimizing and maximizing the benefits for you as an investor.

Author’s Note: I would appreciate hearing your opinion on my selection of high dividend yield companies to consider buying in December 2023. Do you already own or plan to acquire any of the picks? Which are currently your favorite high dividend yield companies?

For further details see:

My Top 10 High Dividend Yield Companies For December 2023