PMETF - My Top 5 Lithium Juniors

2023-10-24 17:48:10 ET

Summary

- My long-term view is that value will accrue to lithium companies with the ability to produce refined lithium outside of China.

- I provide a detailed methodology for screening the top lithium juniors with a skew towards my core strategy.

- My analysis leads to 1 Strong Buy, 2 Buys, 1 Hold, and 1 Sell amongst my Top 5 Lithium juniors. I hit the highlights on each.

Strategy

In the History Channel's dramatized program, The Men Who Built America , a historian commenting on John D. Rockefeller summarized his strategy: " Whoever could control the refining process could very well have the whole industry ." This quote somewhat reminds me of my strategy for investing in the lithium industry which is to generally own the integrated companies with the technical ability to refine lithium into battery grade quality outside of China . Furthermore, I want them to have the technical ability to pivot whenever the inevitable future advancements in lithium battery technologies arrive. There are only a handful of players in the lithium industry that have the proven ability to consistently produce the refined product with the quality that the automobile industry requires. There are a lot of junior miners racing to mine mostly spodumene ("hard rock") deposits but the question in my mind is, if they can't send it to China, then who is ultimately going to refine the spodumene concentrate? My thinking here is that we are going to eventually see significant value accrue to those with the refining capability outside of China.

Methodology

Before I provide my detailed list of the Top 5 Lithium Juniors, some background on my approach and focus is in order:

- I consider juniors to be those not yet in production.

- Resource amounts generally only include the higher confidence portions of known resources. In some cases, I may use a higher cut-off grade portion of the Resource to emphasize the higher grade nature of the deposit.

- LCE = Lithium Carbonate Equivalent

- Production levels are those announced by companies as their targets or estimates by me based on similar types of projects.

- My valuation assumes an acquirer targeting a 21% return on its invested capital. The formula is [((Net Cash per tonne x Estimated Annual Production in LCE tonnes)/.21)-Initial CAPEX]. These valuations are based exclusively on the flagship project. The market rarely pays for anything else.

- I assume prices of $3,000 per tonne for spodumene producers and $40,000 per tonne for integrated producers of battery grade lithium.

- I generally use significantly higher CAPEX and cost estimates than those found in technical reports. Junior mining projects almost always cost more than estimated and frequently cost significantly more. (I have more confidence in this statement than any other one in this article.)

- Juniors with more or enough cash can continue exploration in development during an extended downturn, potentially without diluting shareholders.

- Companies with higher Resource confidence levels ("Measured & Indicated") or even Reserves ("Proven and Probable" reserves are Resources deemed economic through technical studies) generally deserve higher ranking consideration.

Here is this list with what I think are the most relevant details.

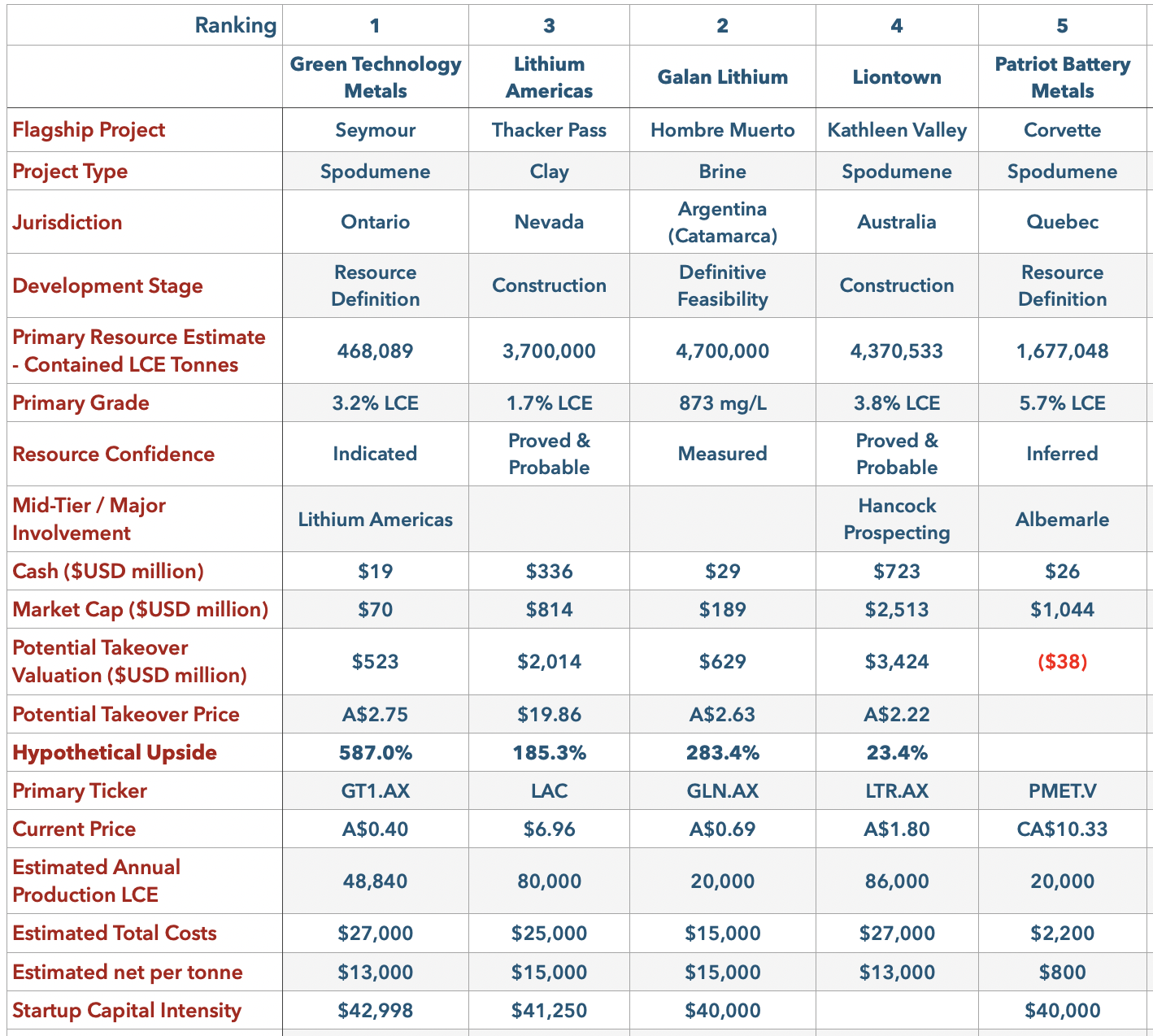

The Top 5

{kind=link}

Source: True Vine Investments

Two points before I discuss these specific companies:

First, obviously Patriot Battery Metals ( OTCQX:PMETF ; PMET:CA ) is not worth less than $0. My valuation method is signaling that the stock is worth significantly less than its current market capitalization perhaps until the company produces a preliminary economic study with more details (e.g., CAPEX, production targets). More on this below in the subsection dedicated to the company.

Second, if you think my total costs are too high, then take a look at the Total Costs for Albemarle ( ALB ) with its integrated production from the best brine and spodumene deposits in the world. (This may be the topic of a future article for me.) Moreover, Albemarle's 2027 targets imply a total cost of $19,000 per tonne. Under these economic scenarios, these projects still end up with net margins in the mid-20% to mid-30% range. My broader, long-term view on the lithium industry is that we are going to see higher prices and higher costs than consensus.

#1 - Green Technology Metals ( OTCPK:GTMLF ; GT1.AX) - Strong Buy

Australian-based Green Technology Metals is targeting an ambitious, multi-deposit, integrated project in Ontario.

Green Tech is led by CEO Luke Cox who was involved in the development of the Wodgina spodumene deposit in Australia. The Board boasts Chairman John Young who was co-founder and Executive Director of Pilbara Minerals ( OTCPK:PILBF ; PLS.AX) and Executive Director Cameron Henry who helped Primero Group earn recognition for its expertise in developing lithium processing facilities around the world. The company's website n otes:

As Green Technology Metals enters its development phase, "Mr. Henry's wealth of experience and accomplishments in the mining industry become invaluable assets for the company's success. His proven expertise in managing public companies and his specific achievements in lithium processing make him a key contributor to the company's strategic goals and endeavours."

Beyond this, Lithium Americas has taken a 5% stake in the company and I can envision them eventually trying to partner or buy the company to expand their North American footprint beyond Thacker Pass.

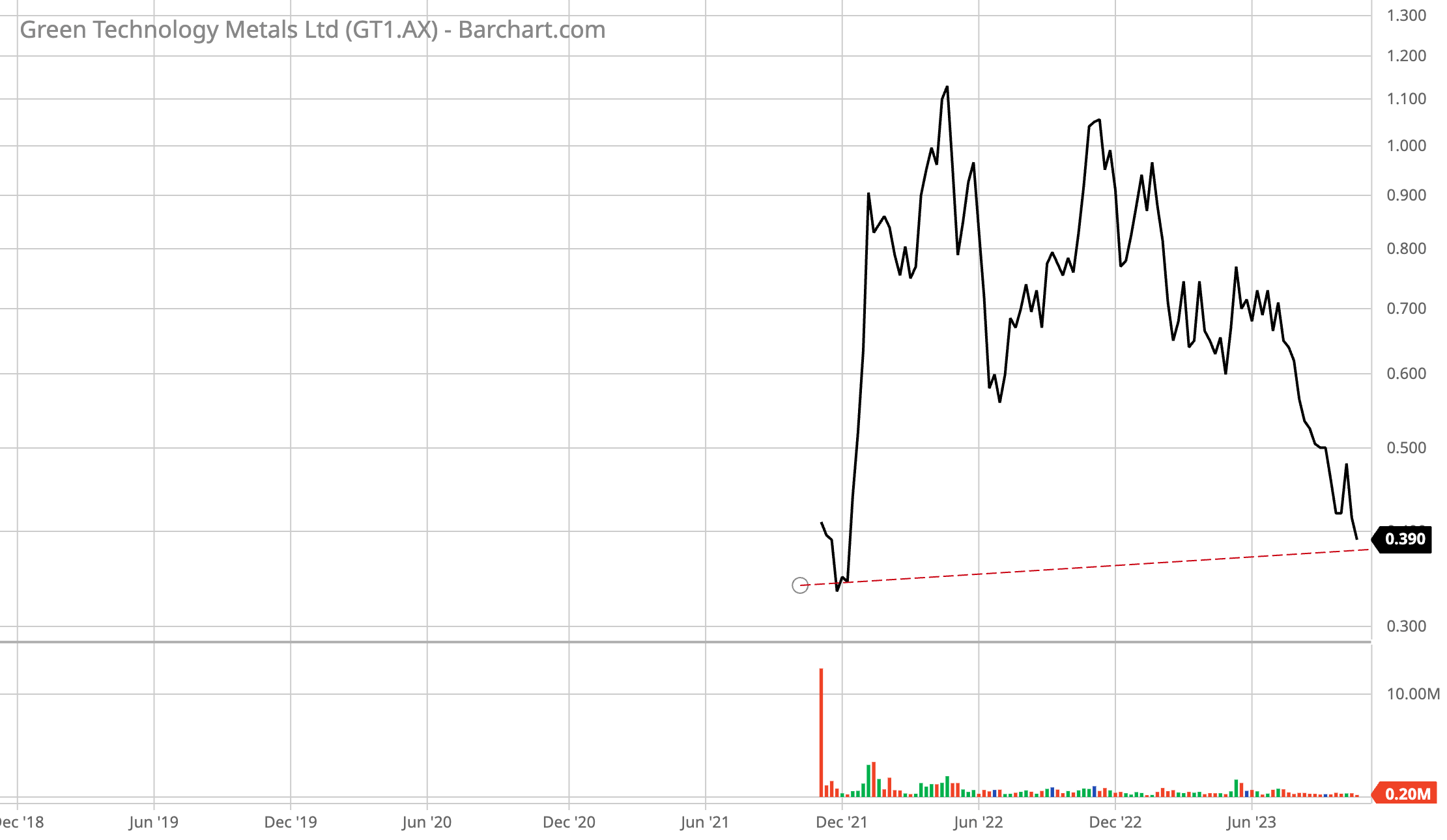

I have estimated initial CAPEX of $2.5 billion for Green Tech to deliver its fully integrated goals. This could be aggressive and is the key risk to my view. The company will soon deliver a preliminary economic assessment which will shine light on this, followed by a feasibility study next year which provide even more details. To the extent that initial CAPEX is below this figure—call it less than $2 billion as I would increase it by at least 25%—then this company has the potential to be even more significantly undervalued. The individual investor will most likely have time to pull the trigger quickly when these details are announced before a potential big swing—up or down—in the shares. Although, with a $70m market cap, I don't see much downside and the shares are approaching longer term support. Here is the weekly log chart:

{kind=link}

The Directors and Management own a little over 7% of the company.

#2 - Lithium Americas ( LAC ) - Buy

The U.S. does not have any significant amount of domestic lithium production. Vancouver-based Lithium Americas is destined to change that. Its recent separation from Lithium Argentina reflects how seriously management is taking the U.S. move to develop its own domestic supply chain.

LAC's $300+ million cash position speaks loudly for the strength of its leadership team. President & CEO John Evans previously held executive and operational management roles with FMC's lithium division (as an interesting aside, he just sold a big chunk of Lithium Argentina ( LAAC ) shares). VP of Growth & Product Strategy Rene Leblanc is highly regarded. He has 17 years of experience in lithium process development, operations, and battery supply chain development including with FMC's lithium division and with Tesla ( TSLA ).

LAC has launched a lithium testing facility in Nevada which Mining.com noted:

"Additionally, the approximately 2,800 m 2 facility will be used to conduct test work on new target ores and brines, and contains a state-of-the-art analytical laboratory capable of analyzing ultra-pure lithium compounds. Lithium Americas and the UNV Reno are collaborating on this commercial work."

This is not something that a Junior does unless they have serious technical capabilities. The reference to " test work on new target ores and brines " is also interesting as it speaks to the longer term ambitions of the company.

LAC's technical capabilities could eventually be further leveraged through an eventual acquisition of Green Tech. Its management has a history of making wise, strategic investments in Resources on the cheap (e.g., Arena Minerals, Millennial Lithium, and Green Tech) instead of buying high with shareholder capital at the top like Albemarle with Liontown and Patriot.

LAC as a 2-phase strategy to produce 80,000 tonnes of LCE in Nevada using commonly used (i.e., highly likely to work) processing technologies and not some unproven (i.e., gimmick) process which is an important consideration, especially since this will likely be the world's first major clay project.

General Motors ( GM ) is the largest shareholder and Thacker Pass may end up being a significant source of Inflation Reduction Act (IRA) compliant lithium for its domestic EV supply chain.

#3 - Galan Lithium ( OTCPK:GLNLF ; GLN.AX) - Buy

Brine projects get no respect in the current market environment and Australian-based Galan has the highest grade brine resource in Argentina. Its flagship project Hombre Muerto project sits adjacent to the other producing Hombre Muerto projects controlled by Livent ( LTHM ), Alkem ( OTCPK:OROCF ; AKE.AX; AKE.TO), and POSCO ( PKX ). This aspect is notable as it points to potential future acquirers.

Galan's Board includes Non-Executive Director Daniel Jimenez who has 28 years of experience with lithium major SQM ( SQM ). Its management team includes lithium consulting, exploration, and geological expertise from time spent at Alkem, Lake Resources ( OTCQB:LLKKF ), NEO Lithium, and SQM.

Galan's strategy is to gradually scale production to 60,000 tonnes. This will take quite some time and brine expansions are notorious for taking longer than expected. Because of this, I'm only targeting the 20,000 tonnes of LCE from the first phase of production but also significantly less CAPEX.

The Directors and Management own 13% of the company.

#4 - Liontown Resources ( OTCPK:LINRF ; LTR.AX) - Hold

Everyone who reads financial news knows who Australian-based Liontown is now. I have them ranked #4 due to limited valuation upside, but they have a huge high grade Resource at Kathleen Valley and strong management. Their only weakness would seem to be the technical capability required to integrate and produce the refined product. Albemarle would have been a logical acquirer in this respect. Hancock Prospecting won't help here. At present, the company is analyzing a potential downstream partnership with Sumitomo ( OTCPK:SSUMF ; OTCPK:SSUMY ), as stated here :

"Downstream Strategy: Liontown has progressed the “partner” pillar of its downstream strategy through an agreement with Japan’s Sumitomo Corporation, a global participant in commodity processing and marketing, to investigate the development of a lithium supply chain between Australia and Japan. The agreement will support a jointly-funded study that explores the feasibility of using Liontown’s spodumene, or a future lithium sulphate product produced in a Western Australia based plant, to produce lithium hydroxide in Japan. The study is non-binding and is expected to be undertaken over a period of two years."

Liontown is expected to ship its first ore soon so time is running out on this company continuing to be included in my junior list. This is one to keep an eye on longer term though.

A solid 17% of shares are held by the Board and Management.

#5 - Patriot Battery Metals ( OTCQX:PMETF ; PMET.V) - Sell

Shares of Patriot soared last year after significant high grade drill results at its Corvette project in James Bay, Quebec led to an Inferred spodumene Resource which is now the largest in the Western Hemisphere. Note that the Resource size I used above is only a higher grade portion of the overall, much larger Resource.

Patriot is Chaired by Ken Brinsden who was previously the CEO of Pilbara Minerals and thus knows a lot about building a large scale spodumene operation. Like Liontown, Patriot doesn't have any notable technical expertise when it comes to refined lithium processing and a potential takeover would likely be the best option for shareholders. Moreover, this appears to be the strategy of the company, keep drilling to define a very large, high-grade Resource and then sell out. A lot of this is baked into the valuation cake.

Patriot has yet to produce an economic study. Importantly, this will shine some light on the potential capital costs to develop the project. Patriot can likely benefit from hydroelectric power but it is in Northern Quebec which could present labor challenges.

Board and management only owns about 2% of the company.

My rational for ranking Patriot a sell is (1) rich valuation, (2) uncertainties remaining around project economics and permitting challenges, namely around the requirement to partially drain a lake, and (3) lack of any path to becoming an integrated producer (on its own). This is definitely one to watch though because once solid amount economic studies have been completed, a buyer could quickly emerge. Potential acquirers have to be cognizant of the former Nemaska disaster in Quebec where there was an embarrassing lack of due diligence completed. This could lead to a slower acquisition process.

Timing Considerations & Strategic Conclusion

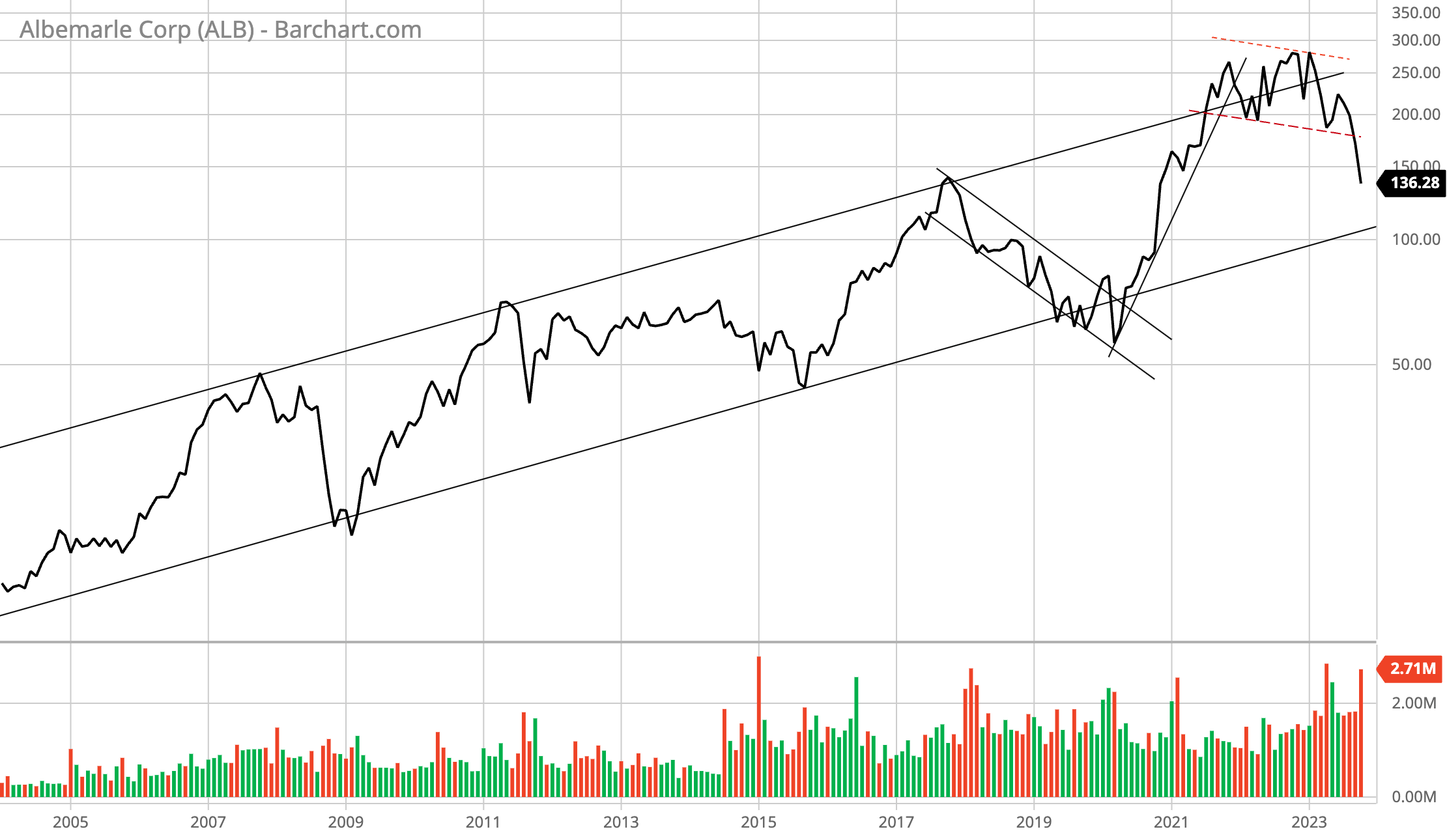

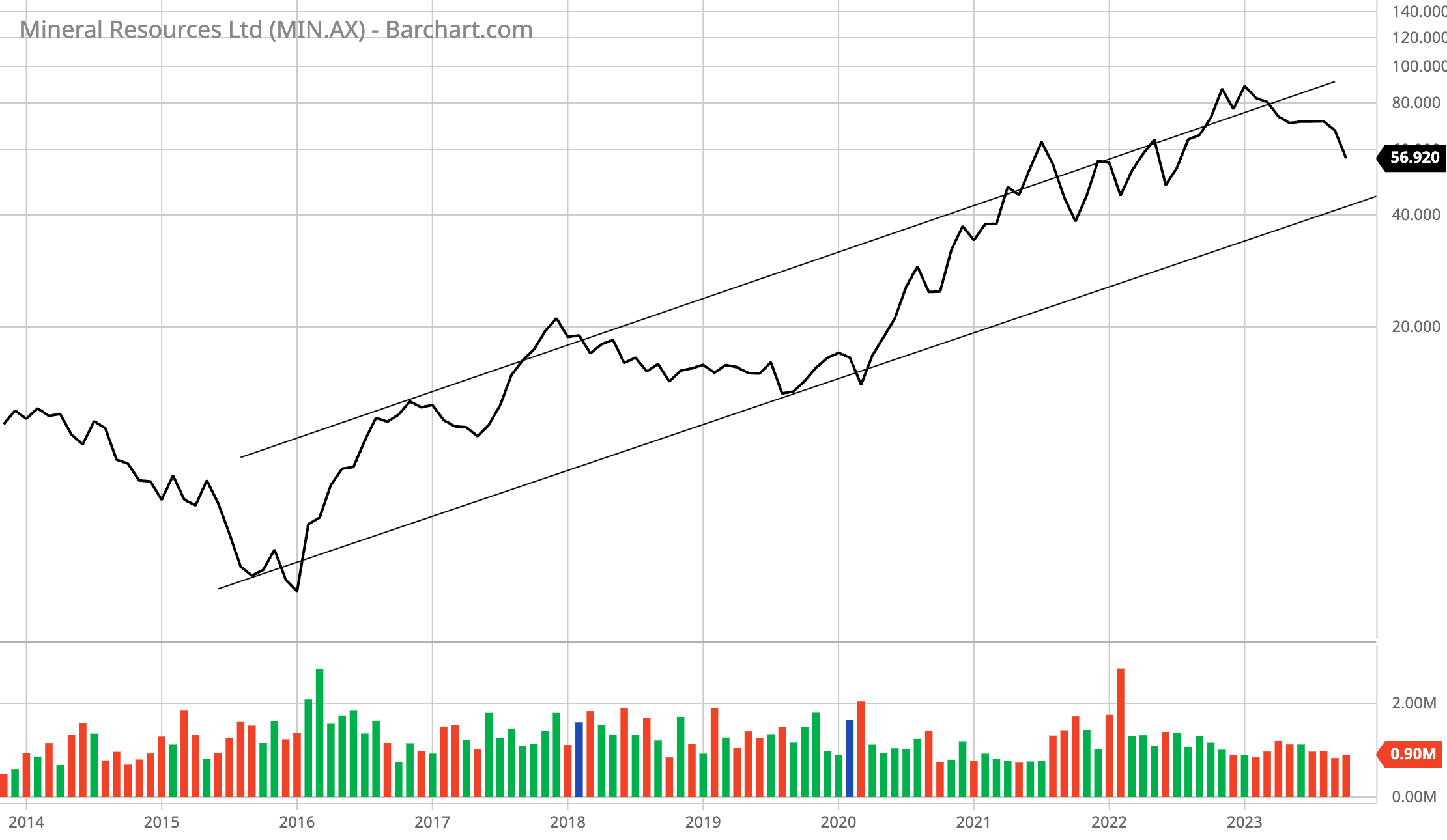

Lithium shares are in free fall but a nice buying opportunity is coming. Two gauges that I am watching to help me determine when are the monthly log charts of Albemarle and Mineral Resources ( OTCPK:MALRF ; OTCPK:MALRY ; MIN.AX), shown here:

{kind=link}

Albemarle has huge long-term support at $110 which points to the potential for another ~20% or so of downside given the downside momentum that we are seeing.

{kind=link}

Just like Albemarle, MinRes also has about 20% more downside to its significant long-term support. I also eyeballed the monthly charts of SQM and Pilbara Minerals and they have similar downside potential.

I think long-term investors should consider initial or additional stakes in Green Tech, LAC, and Galan as this bottoming process occurs.

For further details see:

My Top 5 Lithium Juniors