MYO - Myomo: Game-Changing Medicare Reimbursement Should Create Lasting Value

2023-09-05 09:00:00 ET

Summary

- CMS changed their policy to include Myomo's MyoPro devices as a covered product under Medicare.

- Proposed broad coverage would result in significant operating leverage and sustainable profitability for Myomo.

- Anemic valuation provides outsized return potential.

Overview

The Centers for Medicare & Medicaid Services (CMS, Medicare) have (1) changed their policy about Myomo's (MYO) MyoPro devices, (2) proposed broad coverage and (3) started to pay initial claims through the DME MACs. After 11 years of struggle since the original MyoPro launch, I believe MYO should finally become profitable by the middle or end of next year.

Up until recently, only about 1 in 10 patients whom MYO enrolled in their pipeline ended up receiving a device due to extremely poor insurance coverage. Broad coverage would therefore result in significant operating leverage, steep revenue growth and sustainable profitability.

On its shoestring budget, Myomo adds about 400 patients to its pipeline every quarter, which ONLY includes patients whose insurance company had paid for 1 unit. Most patients are turned away. If these 400 patients could get reimbursed, that alone would translate into ~$75m of revenue per year.

Since the Company's fully diluted market cap ( including the August 24th financing ) is less than $30m, I think there is plenty of upside in the stock. A mere $100m equity value would imply a $3.00 share price. I think MYO should be trading closer to the $200m equity value level.

1. CMS Changed Their Policy

MYO had been unsuccessful in trying to get Medicare (DME MACs) to pay submitted claims since 2019, when they first received their reimbursement code. For example, on the Q4:2019 Earnings Call , the CEO said:

Well, I thought I'd hear back by now, but now I'm expecting in Q2. I mean, the claims have been there, there's been back and forth discussion with provider relations what's called the DME MAC, that's the medical contractors.

But those claims were eventually denied. However , in Q4:2022 CMS made the decision to initiate coverage of MyoPro, and they followed through this year. The CEO reported during the Q4:2022 Earnings Call :

At the end of the fall, we are advised to meet with the DME MAC medical directors and submit MyoPro claims for payments under the individual consideration rules in our HCPCS codes. We expect to meet with the DME MAC medical directors in the near future to review the newest research on patient success with the MyoPro []

The initial claims MYO filed following the CMS recommendation ended up getting paid, as the Company reported last week, and I'll discuss below. Deciding to cover claims which were denied in the past is an obvious and MAJOR shift in CMS policy. Importantly, the DME MAC also had to go through the process of coming up with a price, which is also an important change.

2. CMS Proposed Broad Coverage

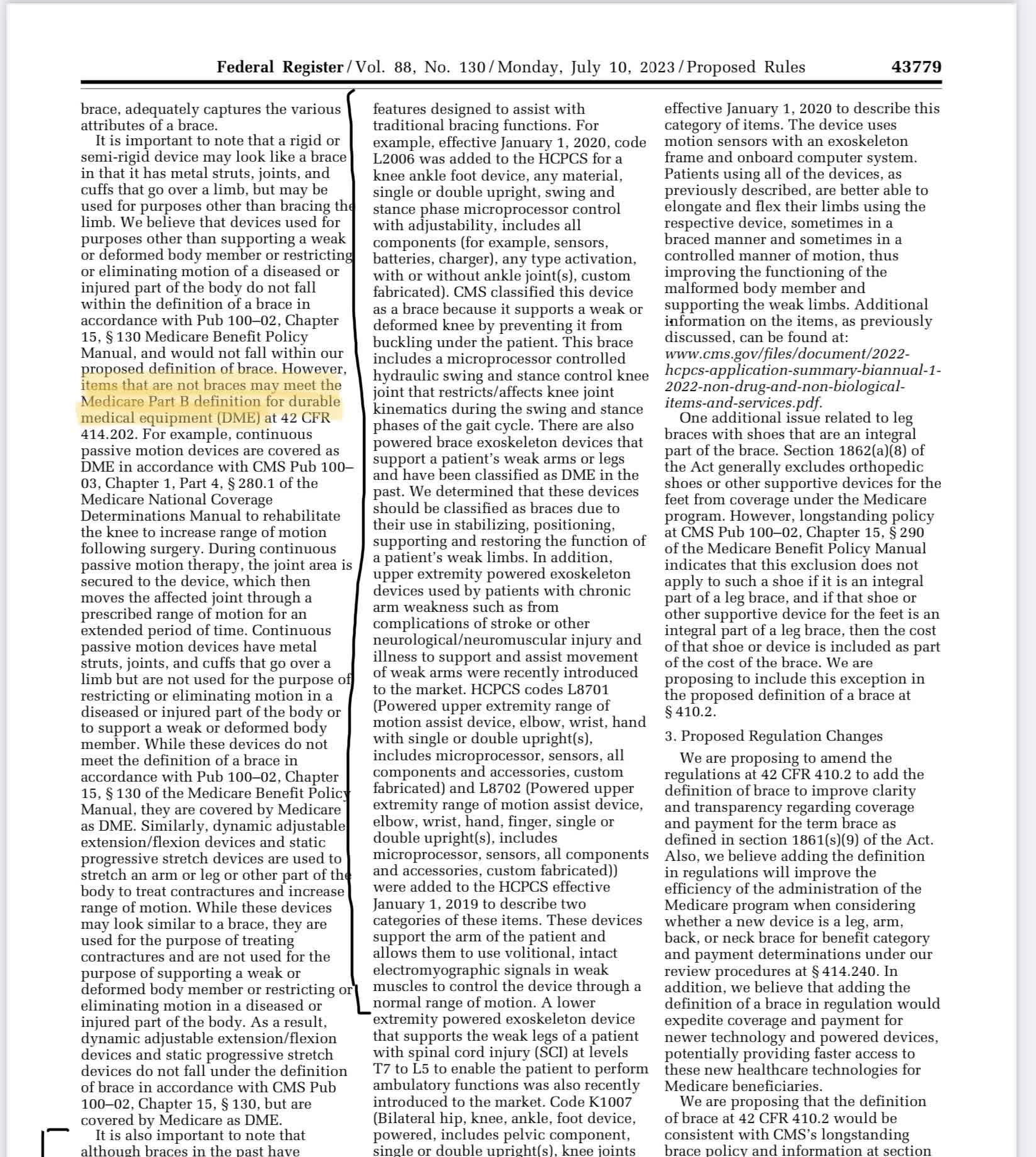

On July 10, 2023, CMS proposed a new rule, which would make the MyoPro devices a covered product under Medicare. This would mean that Medicare and Medicaid HMOs, as well as Fee-For-Service Medicare would be legally obligated to pay for the device according to the "reasonable and necessary" standard. On July 10, 2023, CMS published in the Federal Register a proposed change to the legal definition of "brace" to include powered devices. Since braces are covered products under Medicare, so would be the MyoPro, once this proposal is finalized in the coming months. Page 126 out of 164 of the Federal Register describes the rule change, and CMS highlights the MyoPro devices specifically (HCPCS codes L8701/8702).

{kind=link}

Just to clarify… since braces are already reimbursed, Medicare or the DME MACs will NOT need to issue any Local or National Coverage Decisions to cover the MyoPro. Coverage will be automatic.

3. CMS Started To Pay Claims Through The DME MACs

As I mentioned above, on August 24, 2023, MYO announced that a DME MAC began paying for two Medicare claims submitted by the company, while claims with the other DME MACS are being processed. (Given the muted stock market reaction to this news, the payment of the remaining clams may become an important catalyst for MYO stock.) The yellow highlighted area on the above page explains that before the proposed rule takes effect, the MyoPro has been classified as Durable Medical Equipment (DME), which are reimbursed over a 13-month rental period.

Medicare Reimbursement Price

First of all, just to share my personal opinion for a moment, I believe the $43,700 average selling price for the MyoPro is EXTREMELY cheap to Medicare. It's a one-time/lifetime cost per patient vs. the tens or hundreds of thousands Medicare spends per year per patient on drugs with marginal benefits for a % of the patients taking them. The MyoPro has 100% efficacy, in two ways: it works on everyone wearing it, and it allows patients to do things they otherwise simply would not be able to do .

Secondly, the Company's ASP is artificially lowered by sales to third parties (VA, O&P providers, etc.) vs. direct billing pricing, because they do not include the value of medical services Myomo provides along with the devices. Therefore, I believe the final price Medicare establishes should be above the corporate average.

Third, Myomo actually disclosed in the above press release that the Company is satisfied with the price the Medicare Contractor has established. They wrote:

Appropriate payment amounts received on two MyoPro claims [...]

I believe the only way the Company would be satisfied with the reimbursement and call it "appropriate," if it was comparable to the prices in their direct billing channel. In fact, the most likely method Medicare may use to calculate the final price in this case, is looking at the prices of commercial sales. Since Medicare HMOs have paid for many hundreds of devices, there is a breadth of comparable data at their disposal.

There seems to be a lot of irrational fear in the market about the eventual price Medicare will establish for the MyoPro. When the price does get finally published or disseminated in the market, that should be another major catalyst to MYO stock.

What's Next For Medicare/Myomo?

Even though I believe the next steps are pretty obvious, the market seems to be holding its breath:

- I believe the remaining claims MYO had submitted to the DME MACs will be paid also.

- Since the comment period ended uneventfully, Medicare will make the rule change to the brace category final in November and the MyoPro will become legally covered by Medicare.

- CMS may or may not publish an official price for L8701/L8702 before January 1, however, the DME MACs will keep using the already calculated amount to keep paying claims.

- Starting January 2, 2024, MYO will be submitting claims to Medicare as a brace, and those claims will be getting paid as lump sum payments.

- The conversion rate of claims being paid by Medicare HMOs will substantially improve, as they will be legally obligated to cover the MyoPro.

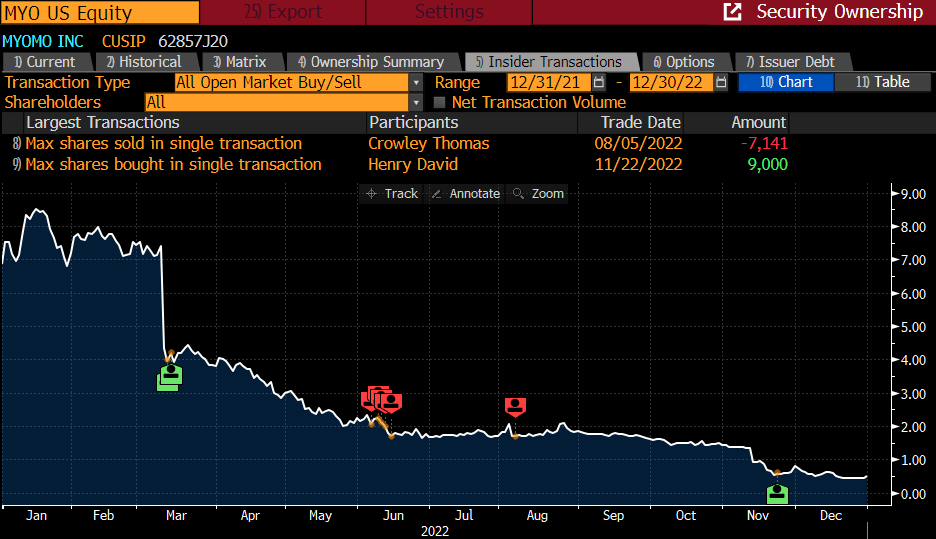

Insider Purchases

Insiders started buying stock late last year after CMS directed the Company to engage the DME MACs and file claims.

{kind=link}

In 2023, not only did the entire senior management purchase stock in the public financings, but the CEO has kept buying stock in the open market , 25% higher than the deal price, and hasn't stopped yet . I would expect these purchases to continue at least, until the market starts to recognize the value of the improved reimbursement landscape.

Valuation & Dilution

MYO currently has 33.3m shares outstanding (including all the 6.8m pre-funded warrants). All the options and other warrants are WAY out of the money. Even at a $10/sh stock price, MYO would only be a ~$300m market cap company, tiny by any measure compared to its market opportunity - US and International. I think it's sad that investors in our day and age are so quick to pay tens of billions of dollars for worthless fads (NFTs, Metaverse, cryptos, meme stocks, etc.) and ignore businesses with actual good news and those that actually make patients' lives better.

Cash Burn

MYO has been burning about $2.7m of cash per quarter. Pro forma for the last financing, they would have about 18 months' of cash at that burn rate. However, given the improved reimbursement landscape, I would expect MYO to become profitable by Q4 of next year. The operating cash burn should start coming down substantially starting in Q2. I would expect MYO to need some kind of bank facility to help fund the working capital to meet the increase in demand.

Risks

Similarly to the FDA, CMS is a black box and can work very slowly. Just like it took over a year to effect a simple change in the arcane legal definition of "brace," so too there can be delays with any other aspect of reimbursement or coverage. MYO could undertake unnecessary and dilutive financings, etc. The downside is to $0/shr, just like any other micro-cap stock. Risk is mitigated by the fact that MYO has a commercial business, which could always be sold for some value.

For further details see:

Myomo: Game-Changing Medicare Reimbursement Should Create Lasting Value