NAPRF - Naspers And Prosus: Still Questionable Profitability Of Ex-Tencent Portfolio

2023-11-29 13:26:50 ET

Summary

- Naspers and Prosus released their usual deluge of media and analyst releases, reports and presentations, highlighting improved KPIs.

- However, while improvements are real, overall profitability of the ex-Tencent portfolio will be achieved also thanks to some adjustments and disposals.

- Overall, the NAV discount is unlikely to shrink unless management delivers real and predictable growth.

Naspers and Prosus H1/24 Results

As usual, both Naspers ( NPSNY ) ( NAPRF ) and Prosus ( PROSY ) ( PROSF ) released their H1/24 reports and multiple slide sets. You can find the materials here for Naspers and here for Prosus. (To find the full report, click on "View results online".)

The materials for the two companies differ only in minor details, since Naspers also owns some very small businesses in addition to its 43% Prosus stake. To avoid any confusion, throughout this review, I will refer mainly to the Naspers materials and proportionate results based on the Group's economic interest. In my view, these are the most truthful representation of the economic reality, since consolidated results also include earnings belonging to minority shareholders in partially owned businesses.

Given that the headline results had already been anticipated, there was no surprise relating to the main figures. Moreover, Tencent ( TCEHY ) results are always included with a lag and are obviously already known to the investor base.

What is key to the Naspers/Prosus story goes beyond EPS and revenues: Investors have long been concerned with capital allocation and the many unprofitable businesses the holding has funded over the ZIRP years. Since the cost of capital has now increased substantially, investors finally want to see the light at the end of the tunnel.

To put things into perspective, keep in mind that the Group posted $2.5B of total trading profit from continuing operations. After excluding contributions from Tencent ($2.9B) and corporate costs ($0.1B), its ex-Tencent portfolio of businesses still delivered a trading loss of $249m.

Hence, the buzz is just about this small part of the company. That said, it would be foolish to just overlook it, since this is where Tencent dividends have been sunk into.

For this very reason, management had guided to improving profit margins and overall profitability on an EBIT basis of the ex-Tencent portfolio in the first half of its financial year 2025, i.e. in the second half of the calendar year 2024. This profitability target has now been moved forward to H2/2024.

Does this mean everything is on the right track? - Not so fast.

Adjustment Alert

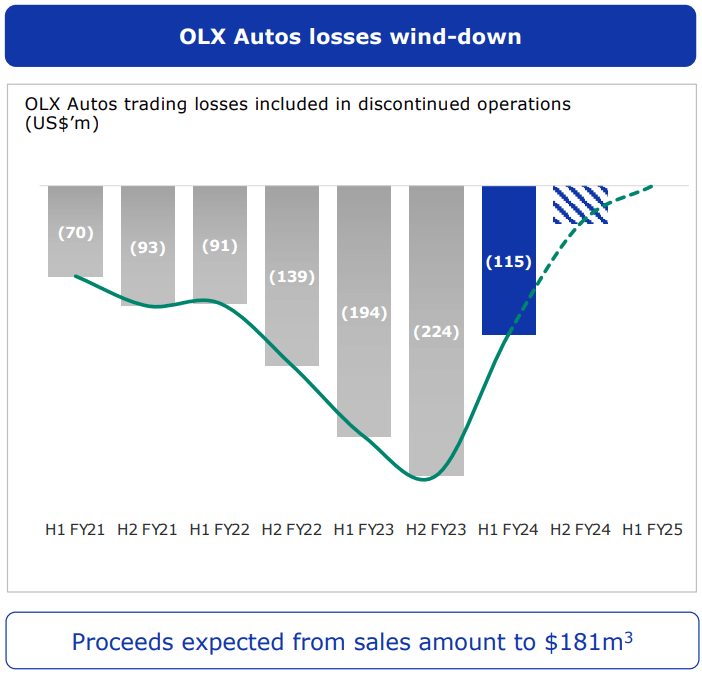

Actually, this achievement was possible only thanks to the sale of unprofitable businesses at a large loss. The slide set includes the example of some OLX Autos businesses, which accumulated losses of $926m over the 3.5 years and were sold for just $181m:

{kind=link}

Actually, when the company states that trading losses improved by $220m, this is after excluding these businesses , which delivered positive EBIT of $17m in H1/23 and a loss of $115m in H1/24. With these businesses factored in, the first half's improvement shrinks to just $88m.

It is clear why these businesses were exited, but it is not clear whether the decision was wise for the long term.

Another huge loss maker is the Edtech segment, which also saw disposals in the period. Last year it delivered $178m of losses on $334m of sales, while after the disposals in this past half year, it delivered $64m of losses on $211m of sales. So losses have effectively come down but still represent 30% of sales (instead of 53% last year).

To sell this as a positive achievement looks like a stretch.

Edtech will have to battle the AI revolution, as it becomes easier than ever to educate oneself online for free or almost free.

Positives

Indisputably positive are the developments of the other segments (continuing operations): Classifieds, Fintech, Food Delivery, and Etail.

Classifieds grew sales by roughly a quarter, but trading profits more than tripled to $110m. This segment was already profitable last year and continues to impress.

Food Delivery grew sales by roughly half a billion dollars and reduced its losses by almost a quarter billion dollars. The $155m of losses in this segment still represent the lion's share of all trading losses in the ex-Tencent portfolio.

Fintech added $111m of sales and reduced its losses by $63m to just $34m. This segment is very likely to deliver nice profit growth going forward.

Etail, despite a difficult environment for retailers, grew sales by 6% and roughly halved its losses to just $27m.

Finally, thanks to low-cost bonds, the company is earning more interest on its cash hoard than it pays to keep it, thus realizing a net interest income of $148m in this first half. These gains are not included in total trading profits (which are pre-tax and pre-interest) but effectively compensate 60% of the ex-Tencent trading losses from continuing operations.

The balance sheet remains pristine, with debt and cash canceling each other out or almost.

Outlook and Conclusions

The Naspers/Prosus story is all about the NAV discount, the reasons of which are manifold: corporate governance deficits, a convoluted holding structure, distrust in capital allocation, management constantly moving goalposts, the lack of liquidity on the Johannesburg stock exchange and indexers forced to sell down their Naspers and Prosus positions as they grow too large, misunderstandings regarding the buyback program, etc.

Finally, everybody understands that without Chinese investments regaining popularity, Tencent itself will likely remain cheap.

Naspers/Prosus management is at least partially addressing investor concerns by executing an open-ended buyback program with excellent financial implications (a detailed analysis can be found here ), although many investors would probably also like to see part of the large cash hoard flow into buybacks.

If management delivers on its profitability targets, it will probably be just considered a first step, as investors will prefer to see a clear, repeatable strategy at work, with reliable, predictable growth patterns before attributing more value to the investment portfolio.

I believe we will get there, sooner or later, and in the meantime, ownership in one of the best Chinese companies out there (personally I believe it is the best) will steadily increase on a per-share basis thanks to the continuing buybacks, which represent nothing else than money printing: selling Tencent for x and buying it back immediately for a bit more than half of x. And the higher and the longer the NAV discount remains, the more Naspers and Prosus shareholders will gain.

As long as Tencent itself is undervalued, Naspers and Prosus both remain excellent buys. Personally, I prefer Naspers, since it is virtually certain to outperform both Tencent and Prosus, as I had predicted one year ago and was proven correct so far.

For further details see:

Naspers And Prosus: Still Questionable Profitability Of Ex-Tencent Portfolio