NPSNY - Naspers: Looming Concerns

Summary

- We believe Naspers' latest surge is unwarranted.

- Speculating on the company's exposure to China's reopening is a roll of the dice.

- Naspers and Prosus present secular growth, but at what cost to their investors?

- Valuation remains a concern and desirable dividends are astray.

- Naspers' South African ventures exhibit solid growth. However, an inflection point awaits.

Naspers' (NPSNY) stock has climbed by more than 20% in the past month, subsequently luring investors' attention. However, we believe the security's latest surge is not warranted as fault lines remain.

We have watched Naspers closely for many years. The stock provided shareholders with immense returns in its initial years as a publicly traded asset. However, Naspers' gains have been underwhelming in recent years as the financial markets have priced most of its prospects.

In recent times, Naspers fell victim to political instability in China and the Russia-Ukraine war due to its regional interests, which added significant volatility to its stock. Moreover, technology stocks performed poorly during 2022 but have rebounded sharply since the turn of the year.

Many investors might be licking their lips after seeing Naspers' latest surge. However, we urge market participants to throw caution to the wind; here is why.

Operational Update

Let us start off with a few positives pertaining to Naspers' operational prowess.

Naspers' near 25% month-over-month surge is partly due to China's reopening. The company owns nearly 27% of Tencent (TCEHY), meaning its reliance on the Chinese economy is substantial. Furthermore, growth stocks have come alive in 2023 , acting as a systemic tailwind to Naspers. Even though Naspers' latest surge is likely market-based, the company is showing signs of operational growth. Let's run through a few features.

Portfolio Companies

Naspers owns several companies. However, I want to highlight some of its key holdings, starting with Takealot. Although yet to be profitable , Takealot is showing immense potential as a mid to downstream delivery service. Having lived in both the United Kingdom and South Africa, I can tell you that there is little difference in the quality of service between Takealot and Amazon ( AMZN ).

As of the middle of last year, Takealot's top line grew by 27% year-over-year, reaching approximately $606 million. Despite the company's $6 million loss, the signs are positive, with cost-cutting and profitability on the horizon.

Furthermore, Naspers' media business is snowballing. It was revealed in June last year that Media24's revenue surged 12% year-over-year while profitability reached $17 million. Africa's media business is growing exponentially with increased decentralization and growing digitalization. However, anecdotally speaking, the company's target market's spending power is a concern, limiting the feasibility of a hard-priced subscription-based business model.

{kind=link}

Tencent & Prosus

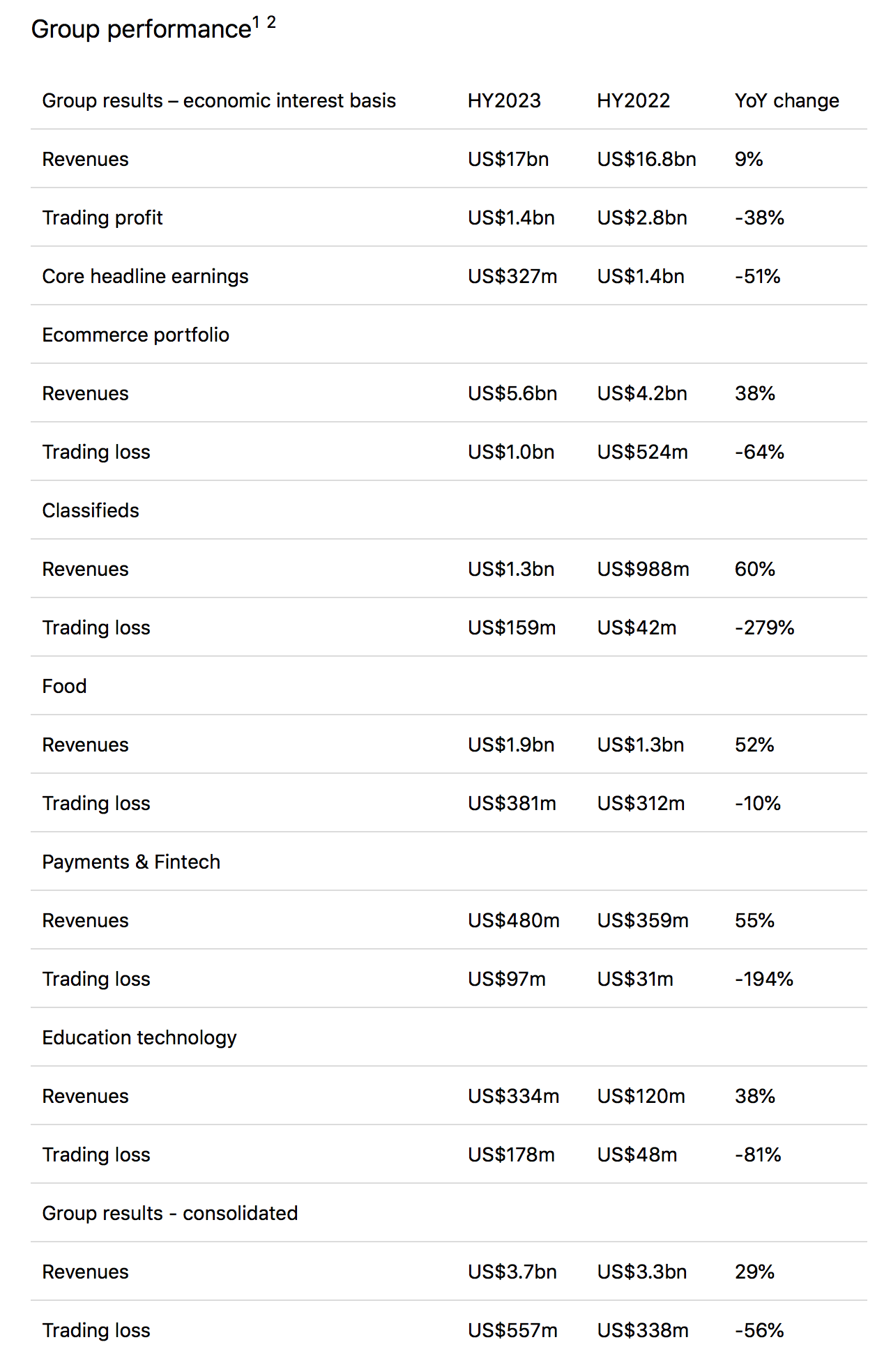

Due to their sheer size, I wanted to discuss Tencent and Prosus ( PROSY ) independently. Naspers owns approximately 27% and 55% of the respective entities and consolidates its interest under IFRS accounting laws.

Naspers released its H1 financial results in November, and as evident in Exhibit 1, the group experienced revenue growth across the board; however, severe trading losses were incurred due to continuous reinvestment in growth opportunities. Investors can anticipate this as a regular feature for Naspers as it is a growth-centric holdings company that exhibits cyclical bottom-line earnings adjacent to its investment cycles.

{kind=link}

Looking ahead, Naspers' secular growth could continue, especially considering the pandemic reopening in China, which could lead to improved prospects for Tencent.

Furthermore, Prosus is likely to benefit from a recovering Eurozone . The company owns a vast range of technology interests ranging from retail to edu-tech. Although the entity has global exposure, its main interests are based in central Europe; thus, a potential EU economic recovery will add tremendous value to the company's prospects.

Valuation & Dividends

As mentioned, Naspers' residual value negatively correlates to its investment cycle. Rising interest rates and elevated equity risk premiums could taper the firm's investment cycle in the coming quarters, resulting in a more favorable valuation framework. Nevertheless, the stock's current valuation multiples need to be assessed to formulate an objective conclusion.

Naspers' stock currently trades at 5.72x sales. One could argue that Naspers' elevated price-to-sales ratio is justified given the company's 13% 10-year compound annual growth rate. However, the stock's forward P/E of 36.96x throws more fuel to the fire as it exceeds the sector average by more than 94%.

Furthermore, Naspers doesn't provide much in terms of dividends. Its 0.39% dividend yield is underwhelming, while its -$646 million in cash from operations provides a serious dividend safety concern.

In a nutshell, Naspers is overvalued on a relative basis and provides an unappealing dividend profile. The stock's valuation could realign once Naspers exits its current investment cycle. However, we are not willing to bank on it.

Risks

Although China's reopening is good news for Naspers, the region's pandemic restrictions have been inconsistent. Thus, it can not be said with certainty that China's latest pandemic reopening will be sustained.

Furthermore, times are tough in South Africa, with factors such as an electricity crisis, political unrest, and a lack of industrialization shunning job growth. Therefore the question beckons: Can companies such as Takealot and Media24 sustain their current growth trajectories?

Lastly, and as mentioned before, Naspers' stock is overvalued relative to its sector. In addition, the asset provides little income-based opportunities as its dividend yield is underwhelming.

Final Word

Naspers does have a solid corporate portfolio, which has illustrated growth in recent years. However, the stock is undesirable at its current valuation, especially given Naspers' exposure to uncertainties such as inconsistent covid-19 policies in China and a failing South African economy. As such, we deem the stock a hold, concurrently encouraging investors to be wary of herding after the stock's latest surge.

For further details see:

Naspers: Looming Concerns