LLOBF - NatWest: A Banking Phoenix Has Risen

Summary

- NatWest is a British Bank, which at one point was the largest in the world by assets. Since then, the business was bailed out and spent a decade restructuring itself.

- We believe macro conditions will continue to weaken, but believe NatWest is positioned well due to a quality loan book and interest gains.

- The business is now highly profitable and is benefiting from higher interest rates.

- Relative to its European peers, NatWest is performing extremely well. Their net interest margin is market-leading, which bodes well in the medium term.

- We see 11% upside in the stock, with the 4% dividend being maintainable.

Company description

NatWest Group plc ( NWG / RBSPF ) provides banking and financial services to personal, corporate, commercial, and institutional customers internationally, with its primary market being the UK.

NatWest operates through the following segments:

- Retail Banking - offers a range of traditional services, including current and credit accounts, mortgages, personal lending and deposits, banking and other retail services.

- Commercial Banking - offers a range of business services to companies of all sizes, including institutional customers.

- RBS International - offers products and services to institutional customers internationally, alongside offshore services for local markets.

- Private Banking - offers a range of private banking and wealth management products to high-net-worth individuals and their business.

- NatWest Markets - offers clients support with the management of financial risks for achieving short-term and long-term sustainable financial goals. This is the investment banking arm of the Group.

The company was formerly known as The Royal Bank of Scotland Group plc and changed its name to NatWest Group plc in July 2020. They are one of the Big 5 banks in the UK, alongside HSBC , Barclays ( BCS ), Lloyds ( LYG ) and Santander ( SAN ).

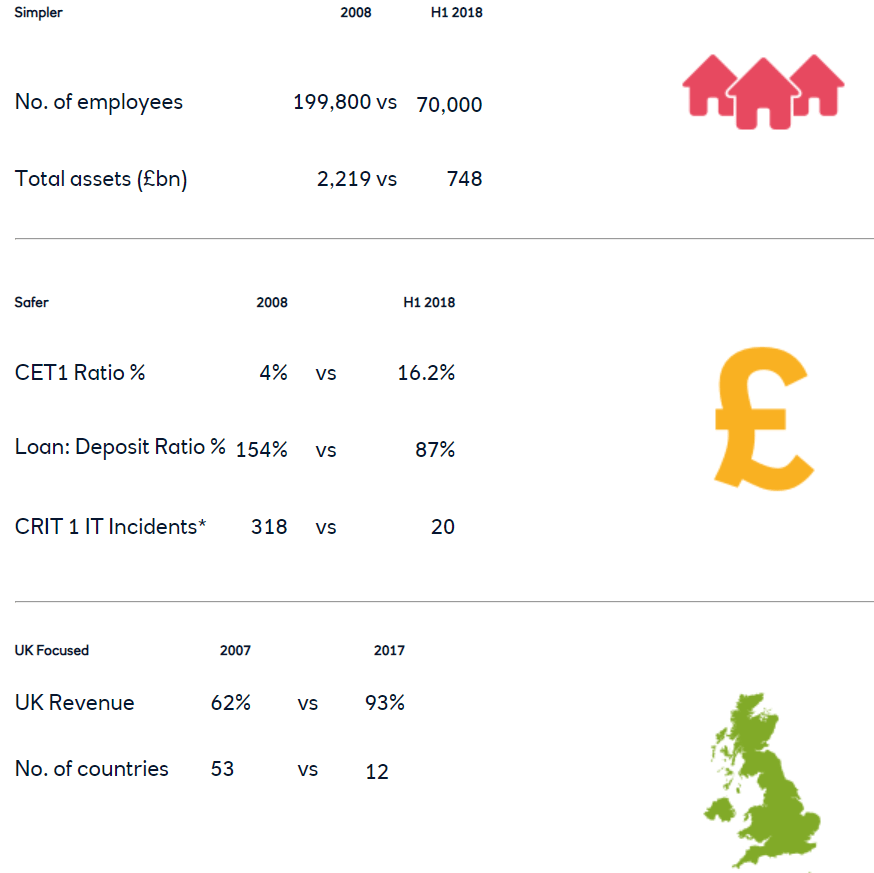

Many have not heard of RBS / NatWest so it may be worth giving a quick history lesson . At one point, NatWest was the largest bank in the world by assets. Shortly after this the business failed. The business grew by expansion and in Oct08 they took over ABN AMRO for EUR 71BN , the largest financial deal in history. Unfortunately, the financial crisis followed suit, leading to liquidity issues, the largest UK corporate loss in history and eventually a bail out by the British Government. It is one of the greatest corporate failures in history. The following illustrates the decade long change in the business:

NatWest business change (Tikr Terminal)

{kind=link}

Although the start to this paper is negative, things have turned around. The UK Government is no longer majority shareholder, believing the business is now financially secure. The business has posted several years of net profitability, following 9 consecutive years of loss-making.

Now is a great time to consider the quality of the business. We have previously looked at Barclays ( linked ) and HSBC ( linked ), having looked favourably on both. We will consider the economic conditions currently, what the turnaround has resulted in and what the outlook for the business is.

Macroeconomic considerations:

During much of 2022, we saw a reversal in fortunes with markets falling and growth slowing. The primary contributing factor for this was inflation. This is being driven by many factors including the Russian invasion of Ukraine, aggressive money printing during 2020/2021, a decade of record low interest rates and supply chain disruptions. The response to this has been interest rate hikes, with the US going for a gradual approach and UK making fewer large increases. The UK's interest rate currently sits at 3.5% , with markets expecting it to peak at 4.75% in 2023.

The impact on inflation has mediocre in the UK. The US has seen successive months of falling inflation, but the UK has yet to see a reversal. The reason for this is energy prices, which is a far larger issue for European countries than the US.

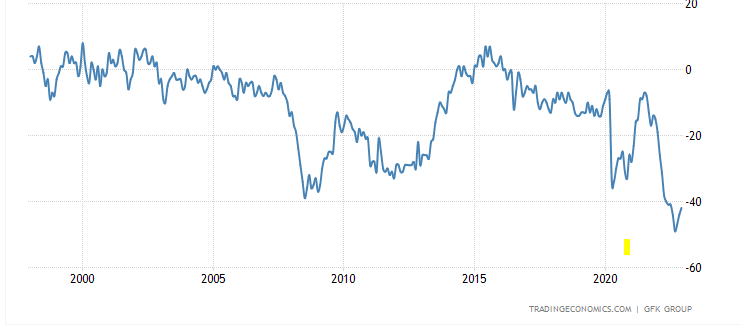

Moving onto growth, the UK is very marginal, having exceeded expectations by growing at 0.1% in November . This is on the back of strong services performance. It is clear that heightened interest rates are taking their toll, with daily news articles on the cost-of-living crisis. Consumers are suffering from both greater borrowing costs and greater expenditure, with wage inflation lagging. It is unsurprising that consumer sentiment is at record low levels, reflecting this.

UK Consumer Confidence (Trading Economics)

{kind=link}

Going forward into 2023, our view is that a recession feels highly likely. Rates hikes are still required, and demand can only remain so resilient. This could lead to a sharper decline in inflation, but things will likely stabilize in early 2024. We are seeing evidence of this on the yield curve, which is sharply inverted in late 2022. Notably, this is the 10Y / 3M curve which historically has inverted immediately preceding a recession.

{kind=link}

With NatWest being a bank, the impact on them is very complex. Firstly, with interest rates increasing, the bank has scope to increase its revenue should it be able to pass on rate hikes without paying out an equal amount of additional interest. Net interest margin has increased 600 bps since FY20, to an impressive 82% (Net int / interest income - Source: Tikr Terminal ). What is significant here is the scope to generate outsized future returns. In the UK, most people fix their mortgage for 2-3 years and then subsequently remortgage for the same period. With rates increasing, many people are having to remortgage at much higher rates and are locking in for longer periods out of fears for where rates could go. NatWest is one of the largest mortgage providers in the UK and is highly considered by consumers. Therefore, we believe the scope for greater interest income into the future is highly likely, even if rates begin aggressively falling from Q4 onwards.

On the opposing side, demand falling is a concern. The yield curve inversion is an illustration of investors' concern about the future of the economy, seeking the safety of long-dated bonds, driving down yields. This leads to a problem for banks, who borrow short to lend long, thus acting as a deterrent for expansionary lending.

The net impact of both has yet to be seen but we believe the heightened interest rate level adds a nuance which could mean a soft landing for NatWest, meaning outperformance relative to expectations.

Banking industry

Looking more long-term, we will now consider the key themes in the banking industry and how NatWest is navigating these.

Fintech/payments/challenger banks:

The rise of fintech businesses, specifically challenger banks and payments, has been a great wave in the UK. Revolut, the leading challenger bank in the UK, was valued at $33BN in its most recent funding round . The explosion in these businesses stem from historical under investment in digital platforms by the traditional banks due to post financial crisis issues and record low interest rates. Even still, the UK banking and payments industry was far more developed than most countries, yet consumers sought further improvements. Businesses like Monzo, Revolut and Starling offered such services and have gained market share. In response, NatWest and others have improved their services, but it is difficult to draw back consumers who have left and are now happy.

Long term, competition will remain high, but we are not overly concerned. The reason for this is that the banking industry in Europe is inherently unattractive compared to other regions, such as the US. The reason for this is heavy regulation following the financial crisis. For this reason, it is difficult to be profitable while maintaining high quality services and so the transition to profitability for these fintech businesses will be difficult.

Wealth management:

Deloitte sees wealth management within banks as a great opportunity, impacted by macro conditions. Customers are seeking a holistic service with more tailored client-centric offerings, as opposed to a product suite.

NatWest is a player in this market but is dwarfed by both some of the other Big 5 and specialist wealth managers . The UK market is highly mature, dating back hundreds of years, with many of the largest players having over a century track record (f.e. Brewin Dolphin, James Hambro and Rothschild). NatWest's value here comes with Coutts, the 331-year-old secretive bank for the rich. It is famous for having an impressive client list which included the late Queen Elizabeth of England. Although scale is not available (Coutts operates independently without a banking workforce), this is a great selling point for NatWest as it is arguably the most famous standalone private bank in the world. The opportunities for cross-selling are very high.

Investment banking, market infrastructure and commercial services:

NatWest has scaled its investment banking service bank significantly, but still provides some services. The majority of its non-consumer facing business is now in the commercial space. NatWest holds the largest share of current accounts in Great Britain for businesses with a turnover greater than £2m. The expectation from this sector is similar to what we have already identified, further innovation and investment in services. With economic conditions weakening, businesses will look for more flexible support and a partnership-like relationship with their bank. NatWest has recently won awards for private placement dealing and money market activities .

Retail banking services:

As part of their 2023 banking outlook, Deloitte believes there will be greater pressure on banks to develop their product offering, ensuring they are supporting consumers in many different facets. This involves support services for those struggling, greater complementary services, ESG development and innovation.

NatWest has won many awards for customer service and generally is well regarded in the UK , when compared to the other Big 5. Further, EY have found that UK banks are leaders in governance and ESG reporting and incorporating key social factors into their strategy.

Overall, the banking industry's key theme is innovation. Consumers and corporates are looking for improvements in services and a more expansive and flexible offering. NatWest has shown some evidence to suggest it is a market leader, but equally has much scope to improve. With bank conditions potentially improving in the medium-term, it is now a great time to reinvest in their services.

Financials:

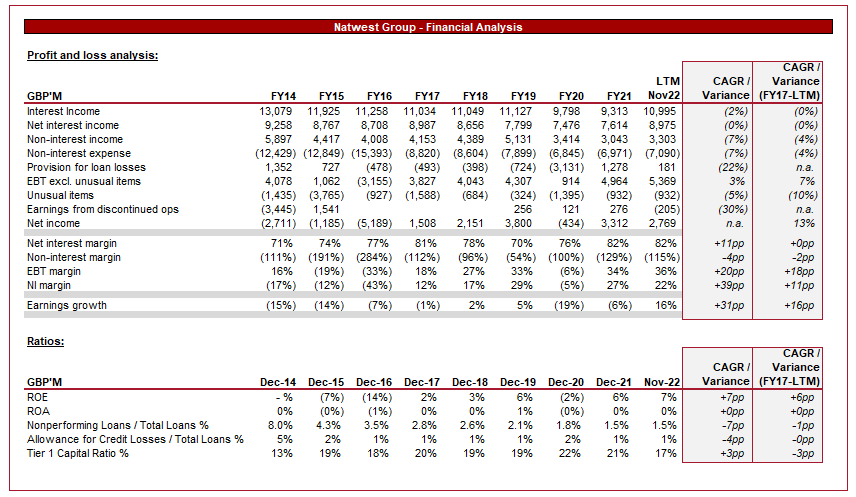

When considering NatWest's financials, we must accept that the business has been in an incredibly large turnaround which is likely unfinished. The business has transformed from an unsustainable high-flying international bank to a more focused, sustainable retail and commercial bank. For this reason, comparisons to prior periods can be deceiving, nonetheless the comparison gives us a peg. We believe the first phase transformation was complete in 2017, as net profitability was achieved for the first time in 9 years. For this reason, we have a variance comparison to both FY14 and FY17.

NWG Financials (Tikr Terminal)

{kind=link}

As mentioned previously, net interest income margin has improved, although earnings have remained flat across the historical period. The business has moved away from non-core services, which we observe as a reduction in non-interest income and expense. These services were generally low margin and have fundamentally changed post financial crisis.

Loan provisions look to normalized to a realistic level now, although 2023 could lead to an uptick in defaults. NatWest's loan book currently looks much healthier, so we see no material risk present. Currently, non-performing loans represent only 1.5% of their book, a record low level.

NatWest book (Q3 pack)

Noise in the financials is finally disappearing, with discontinued operations and unusual items falling in size. These primarily relate to historic M&A activity, which again is no longer attractive. The current process relates to the disposal of Ulster Bank assets in the RoI to AIB.

At >20% NI margin and 7% ROE, the business is suddenly looking attractive. The business should be able to issue sustainable dividends while reinvesting in its services. This has been achieved with a tier 1 ratio of 17%, meaning substantial headroom, and much in the way of high-quality assets.

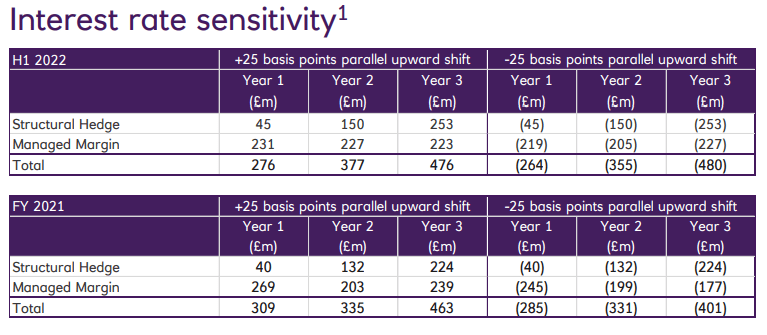

Although interest rates falling are unlikely, the following is a sensitivity of such an event:

Interest rate sensitivity (Q3 Pack)

{kind=link}

Peer group comparison and valuation:

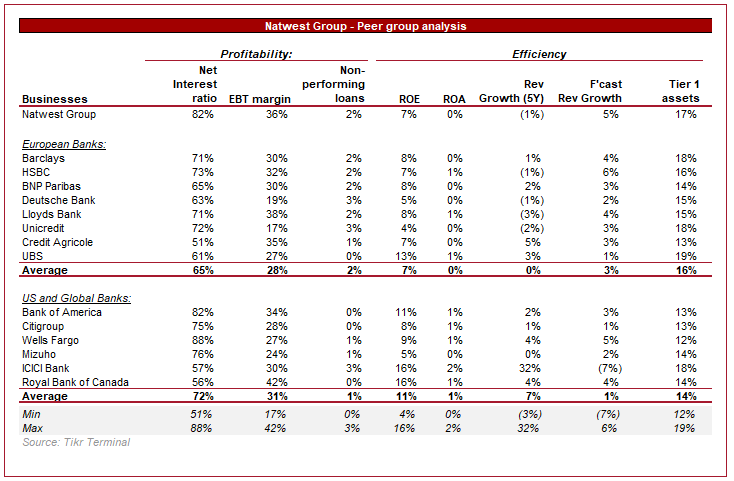

Peer group analysis (Tikr Terminal)

{kind=link}

When comparing NatWest to its peers, the business stands up very well. It is more profitable than all but one of its European peer group, while having a marginally larger tier 1 asset base. As mentioned previously, the banking industry is weak in Europe, with not much growth achieved or forecast. That said, analysts are forecasting superior growth for NatWest.

Comparing to US and some international banks is not appropriate, as the environment in my opinion is far more favourable for them. When comparing retail / commercial banking KPIs, NatWest does moderately, only lagging behind marginally.

Peer group valuation (Tikr Terminal)

NatWest is up 20% since November, which has taken its valuation in line with / slightly exceeding its European counterparts. That would have been the perfect time, with upside now more limited. Analysts still see 27% growth available. Our view is more prudent, seeing the possibility for P/BV to expand to 0.9x from 0.81x, suggesting an upside of 11%.

This said, investors must also appreciate that NatWest presents a low volatility stock which is well placed to maintain dividends and withstand further economic weakening.

Final thoughts

NatWest has achieved an almighty turnover. It will never reach the heights it had previously, but those levels were built on toxic assets. The current business is far more focused, and management has a clear strategy, focusing on retail and commercial banking. Economic conditions are weakening but heightened interest rates will buffer the impact somewhat through greater income from mortgages.

The valuation is our only area of hesitancy, with a large rise in late Q42022. We believe the stock is still marginally undervalued and so deserves a buy rating, but our conviction is less certain. That said, with a medium-term view, NatWest will certainly perform well.

For further details see:

NatWest: A Banking Phoenix Has Risen